Predictable Relative Forward Performance Processes: Multi-Agent and Mean Field Games for Portfolio Management

Pith reviewed 2026-05-24 06:15 UTC · model grok-4.3

The pith

Relative performance concerns can lead agents to short stocks with positive expected excess returns.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Predictable relative forward performance processes admit explicit construction for CARA initial data in both multi-agent and mean-field games, producing equilibrium strategies in which relative performance concerns do not necessarily increase investment in the risky asset and, for some parameter values, induce agents to short a stock that has positive expected excess return.

What carries the argument

Predictable relative forward performance processes (PRFPPs), which incorporate relative performance criteria into forward performance processes and enable closed-form equilibrium strategies in a binomial market driven by a hidden regime factor.

If this is right

- Equilibrium holdings of the risky asset can be smaller than in the absence of relative concerns.

- Short positions can arise even when the stock offers positive expected excess return.

- Changes in the skewness of the binomial return distribution alter the equilibrium investment levels.

- The mean-field approximation yields strategies that remain useful for large but finite populations.

- The non-traded regime factor creates market incompleteness that interacts with the relative performance objective.

Where Pith is reading between the lines

- The finding implies that relative benchmarks in asset management may sometimes dampen rather than amplify aggregate risk-taking.

- Similar shorting behavior might appear in other incomplete-market settings if the CARA restriction can be lifted.

- Empirical tests could examine whether portfolio managers with relative-performance mandates reduce exposure to high-skewness assets.

- The framework suggests a mechanism by which competition stabilizes markets through reduced long positions.

Load-bearing premise

The agents' initial performance criteria belong to the constant absolute risk aversion class and each trades a distinct binomial stock whose positive-return probability is governed by a non-traded stochastic market regime factor.

What would settle it

Fix a parameter set in which the model predicts a negative position in the stock; simulate or observe the market regime path and verify whether the agent's realized holdings are indeed negative while the stock's expected excess return remains positive.

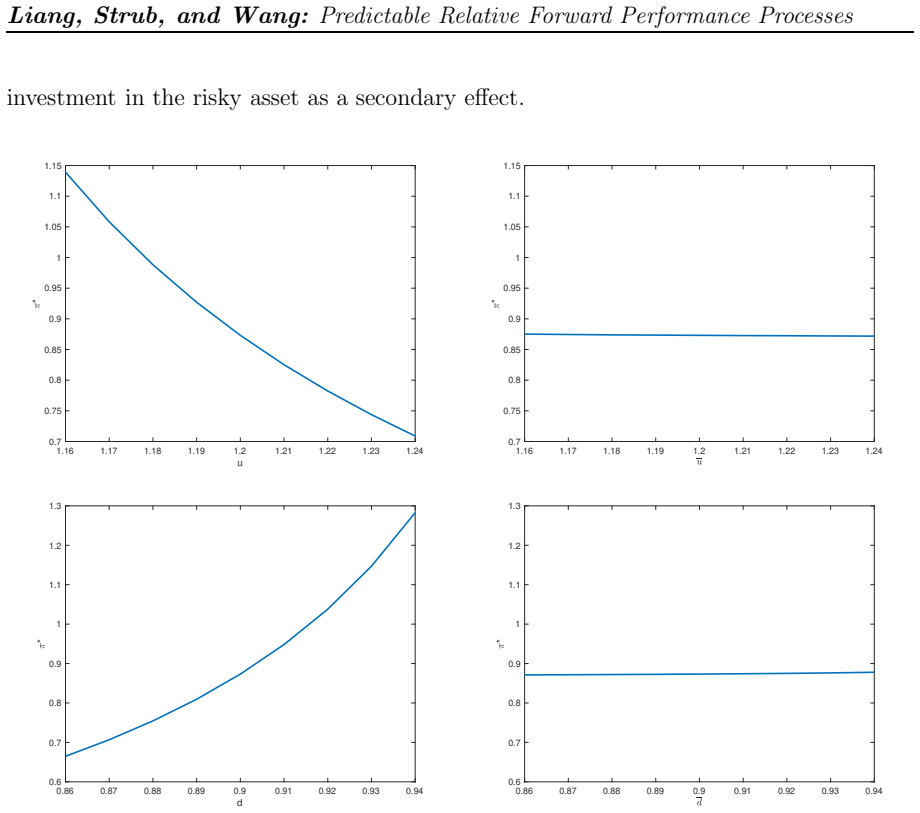

Figures

read the original abstract

We introduce predictable relative forward performance processes (PRFPP) as a new framework for studying portfolio management within a competitive and incomplete market environment. Each agent trades a distinct stock following a binomial distribution with probabilities for a positive return depending on the market regime characterized by a non-traded stochastic factor. For both the finite population and mean field games, we construct and analyse PRFPPs for initial data of the CARA class along with the associated equilibrium strategies. We find that relative performance concerns do not necessarily lead to more investment in the risky asset compared to when there are no such concerns. Under some parameter constellations, agents short a stock with positive expected excess return. The binomial market setting facilitates a straightforward adjustment of risky asset skewness, enabling an analysis of its impact on investment behavior, an aspect that continuous-time frameworks cannot capture.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces predictable relative forward performance processes (PRFPPs) as a framework for multi-agent and mean-field portfolio management in incomplete markets. Each agent trades a distinct binomial stock whose up-move probability depends on a non-traded regime factor. Explicit constructions of PRFPPs are given for CARA initial data in both the finite-population and mean-field settings, together with the associated Nash equilibrium strategies. The central finding is that relative performance concerns need not increase holdings of the risky asset and, for some parameter values, produce short positions in a stock with positive expected excess return; the binomial structure is used to examine the effect of skewness on these strategies.

Significance. If the explicit constructions hold, the work supplies a concrete, verifiable example of how relative performance can generate counter-intuitive portfolio choices (including short sales of positive-alpha assets) that are not visible in standard absolute-performance models. The binomial market permits direct control of skewness, an analysis unavailable in continuous-time settings. The mean-field limit extends the results to large populations. The explicit, closed-form nature of the CARA constructions is a clear strength, as it makes the equilibrium strategies and the short-position phenomenon directly computable from the primitives.

minor comments (3)

- The transition from the finite-N equilibrium to the mean-field limit is stated but the rate or mode of convergence is not quantified; a brief remark on the sense in which the mean-field strategy approximates the finite-N strategy would strengthen the claim.

- Notation for the regime factor and the binomial probabilities is introduced in §2 but reused in the equilibrium characterization without a forward reference; a short table collecting the main symbols would improve readability.

- The abstract asserts that the binomial setting 'facilitates a straightforward adjustment of risky asset skewness'; the corresponding numerical illustration or parameter sweep appears only in the final section and could be moved earlier or cross-referenced from the main theorems.

Simulated Author's Rebuttal

We thank the referee for the positive and constructive report, which correctly identifies the paper's core contributions: explicit PRFPP constructions for CARA agents in both finite-population and mean-field binomial settings, and the finding that relative concerns can produce short positions in positive-excess-return assets. The recommendation for minor revision is noted. No specific major comments were enumerated in the report, so we have no point-by-point rebuttals to provide at this stage.

Circularity Check

No significant circularity detected

full rationale

The paper explicitly constructs PRFPPs for given CARA initial data in finite-population and mean-field games using the binomial market with regime-dependent probabilities. Equilibrium strategies and the central claims (relative performance not necessarily increasing risky investment, and possible short positions despite positive excess returns) are derived directly as consequences of the solved optimization problems and explicit comparisons to the no-relative-performance benchmark. No load-bearing steps reduce by definition or self-citation to the inputs; the binomial structure permits parameter-free explicit computation without fitting or renaming. The derivation is self-contained.

Axiom & Free-Parameter Ledger

free parameters (2)

- CARA risk-aversion coefficient

- regime-dependent binomial probabilities

axioms (1)

- domain assumption Each agent trades a distinct stock whose return distribution is binomial and modulated by a non-traded stochastic factor

invented entities (1)

-

Predictable Relative Forward Performance Process (PRFPP)

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Equilibria of dynamic games with many players: Existence, approximation, and market structure

Sachin Adlakha, Ramesh Johari, and Gabriel Y Weintraub. Equilibria of dynamic games with many players: Existence, approximation, and market structure. Journal of Economic Theory, 156: 0 269--316, 2015

work page 2015

-

[2]

Predictable forward performance processes in complete markets

Bahman Angoshtari. Predictable forward performance processes in complete markets. Probability, Uncertainty and Quantitative Risk, 8 0 (2): 0 141--176, 2023

work page 2023

-

[3]

Predictable forward performance processes: The binomial case

Bahman Angoshtari, Thaleia Zariphopoulou, and Xun Yu Zhou. Predictable forward performance processes: The binomial case. SIAM Journal on Control and Optimization, 58 0 (1): 0 327--347, 2020

work page 2020

-

[4]

Competition in fund management and forward relative performance criteria

Michail Anthropelos, Tianran Geng, and Thaleia Zariphopoulou. Competition in fund management and forward relative performance criteria. SIAM Journal on Financial Mathematics, 13 0 (4): 0 1271--1301, 2022

work page 2022

-

[5]

Risk and the required return on equity

Fred D Arditti. Risk and the required return on equity. The Journal of Finance, 22 0 (1): 0 19--36, 1967

work page 1967

-

[6]

Levon Avanesyan, Mykhaylo Shkolnikov, and Ronnie Sircar. Construction of a class of forward performance processes in stochastic factor models, and an extension of widder theorem. Finance and Stochastics, 24 0 (4): 0 981–1011, 2020

work page 2020

-

[7]

Playing for real: a text on game theory

Ken Binmore. Playing for real: a text on game theory. Oxford University Press, 2007

work page 2007

-

[8]

Power forward performance in semimartingale markets with stochastic integrated factors

Lijun Bo, Agostino Capponi, and Chao Zhou. Power forward performance in semimartingale markets with stochastic integrated factors. Mathematics of Operations Research, 48 0 (1): 0 288--312, 2023

work page 2023

-

[9]

Correlated equilibria for mean field games with progressive strategies

Ofelia Bonesini, Luciano Campi, and Markus Fischer. Correlated equilibria for mean field games with progressive strategies. arXiv preprint arXiv:2212.01656, 2022

-

[10]

Of tournaments and temptations: An analysis of managerial incentives in the mutual fund industry

Keith C Brown, W Van Harlow, and Laura T Starks. Of tournaments and temptations: An analysis of managerial incentives in the mutual fund industry. The Journal of Finance, 51 0 (1): 0 85--110, 1996

work page 1996

-

[11]

Optimal beliefs, asset prices, and the preference for skewed returns

Markus K Brunnermeier, Christian Gollier, and Jonathan A Parker. Optimal beliefs, asset prices, and the preference for skewed returns. American Economic Review, 97 0 (2): 0 159--165, 2007

work page 2007

-

[12]

Correlated equilibria and mean field games: a simple model

Luciano Campi and Markus Fischer. Correlated equilibria and mean field games: a simple model. Mathematics of Operations Research, 47 0 (3): 0 2240--2259, 2022

work page 2022

-

[13]

Risk taking by mutual funds as a response to incentives

Judith Chevalier and Glenn Ellison. Risk taking by mutual funds as a response to incentives. Journal of Political Economy, 105 0 (6): 0 1167--1200, 1997

work page 1997

-

[14]

Wing Fung Chong. Pricing and hedging equity-linked life insurance contracts beyond the classical paradigm: The principle of equivalent forward preferences. Insurance: Mathematics and Economics, 88: 0 93--107, 2019

work page 2019

-

[15]

Minimal hellinger martingale measures of order q

Tahir Choulli, Christophe Stricker, and Jia Li. Minimal hellinger martingale measures of order q. Finance and Stochastics, 11 0 (3): 0 399--427, 2007

work page 2007

-

[16]

Home bias at home: Local equity preference in domestic portfolios

Joshua D Coval and Tobias J Moskowitz. Home bias at home: Local equity preference in domestic portfolios. The Journal of Finance, 54 0 (6): 0 2045--2073, 1999

work page 2045

-

[17]

Managerial incentives and competition

Rachel Croson and Arie Schinnar. Managerial incentives and competition. In Experimental Business Research, pages 171--184. Springer, 2005

work page 2005

-

[18]

Discrete mean field games: Existence of equilibria and convergence

Josu Doncel, Nicolas Gast, and Bruno Gaujal. Discrete mean field games: Existence of equilibria and convergence. Journal of Dynamics and Games, 6 0 (3): 0 1--19, 2019

work page 2019

-

[19]

Forward utilities and mean-field games under relative performance concerns

Goncalo Dos Reis and Vadim Platonov. Forward utilities and mean-field games under relative performance concerns. In From Particle Systems to Partial Differential Equations: International Conference, Particle Systems and PDEs. ICPS 2019, ICPS 2018, ICPS 2017, pages 227--251. Springer Proceedings in Mathematics & Statistics, 2021

work page 2019

-

[20]

Forward utility and market adjustments in relative investment-consumption games of many players

Goncalo Dos Reis and Vadim Platonov. Forward utility and market adjustments in relative investment-consumption games of many players. SIAM Journal on Financial Mathematics, 13 0 (3): 0 844--876, 2022

work page 2022

-

[21]

Skewness preferences in choice under risk

Sebastian Ebert and Paul Karehnke. Skewness preferences in choice under risk. Available at SSRN 3903202, 2021

work page 2021

-

[22]

An exact connection between two solvable SDE s and a nonlinear utility stochastic PDE

Nicole El Karoui and Mohamed Mrad. An exact connection between two solvable SDE s and a nonlinear utility stochastic PDE . SIAM Journal on Financial Mathematics, 4 0 (1): 0 697, 2013

work page 2013

-

[23]

Recover dynamic utility from observable process: Application to the economic equilibrium

Nicole El Karoui and Mohamed Mrad. Recover dynamic utility from observable process: Application to the economic equilibrium. SIAM Journal on Financial Mathematics, 12 0 (1): 0 189--225, 2021

work page 2021

-

[24]

Affine long term yield curves: an application of the R amsey rule with progressive utility

Nicole El Karoui, Caroline Hillairet, and Mohamed Mrad. Affine long term yield curves: an application of the R amsey rule with progressive utility. International Journal of Financial Engineering, 1 0 (1): 0 1450003, 24, 2014

work page 2014

-

[25]

Consistent utility of investment and consumption: a forward/backward SPDE viewpoint

Nicole El Karoui, Caroline Hillairet, and Mohamed Mrad. Consistent utility of investment and consumption: a forward/backward SPDE viewpoint. Stochastics, 90 0 (6): 0 927--954, 2018

work page 2018

-

[26]

Ramsey rule with forward/backward utility for long-term yield curves modeling

Nicole El Karoui, Caroline Hillairet, and Mohamed Mrad. Ramsey rule with forward/backward utility for long-term yield curves modeling. Decisions in Economics and Finance, 45 0 (1): 0 375--414, 2022

work page 2022

-

[27]

Optimal investment under relative performance concerns

Gilles-Edouard Espinosa and Nizar Touzi. Optimal investment under relative performance concerns. Mathematical Finance, 25 0 (2): 0 221--257, 2015

work page 2015

-

[28]

Competition and cooperation in mutual fund families

Richard Burtis Evans, Melissa Porras Prado, and Rafael Zambrana. Competition and cooperation in mutual fund families. Journal of Financial Economics, 136 0 (1): 0 168--188, 2020

work page 2020

-

[29]

The determinants of mutual fund performance: A cross-country study

Miguel A Ferreira, Aneel Keswani, Ant \'o nio F Miguel, and Sofia B Ramos. The determinants of mutual fund performance: A cross-country study. Review of Finance, 17 0 (2): 0 483--525, 2013

work page 2013

-

[30]

Christoph Frei and Goncalo Dos Reis. A financial market with interacting investors: does an equilibrium exist? Mathematics and Financial Economics, 4: 0 161--182, 2011

work page 2011

-

[31]

Discrete time, finite state space mean field games

Diogo A Gomes, Joana Mohr, and Rafael Rigao Souza. Discrete time, finite state space mean field games. Journal de math \'e matiques pures et appliqu \'e es , 93 0 (3): 0 308--328, 2010

work page 2010

-

[32]

Xin Guo, Anran Hu, Renyuan Xu, and Junzi Zhang. Learning mean-field games. Advances in Neural Information Processing Systems, 32, 2019

work page 2019

-

[33]

MF-OMO : An optimization formulation of mean-field games

Xin Guo, Anran Hu, and Junzi Zhang. MF-OMO : An optimization formulation of mean-field games. arXiv preprint arXiv:2206.09608, 2022

-

[34]

Forward rank-dependent performance criteria: Time-consistent investment under probability distortion

Xue Dong He, Moris S Strub, and Thaleia Zariphopoulou. Forward rank-dependent performance criteria: Time-consistent investment under probability distortion. Mathematical Finance, 31 0 (2): 0 683--721, 2021

work page 2021

-

[35]

Equilibria in symmetric games: Theory and applications

Andreas Hefti. Equilibria in symmetric games: Theory and applications. Theoretical Economics, 12 0 (3): 0 979--1002, 2017

work page 2017

-

[36]

Horizon-unbiased utility functions

Vicky Henderson and David Hobson. Horizon-unbiased utility functions. Stochastic Processes and their Applications, 117 0 (11): 0 1621--1641, 2007

work page 2007

-

[37]

Bengt Holmstrom. Moral hazard in teams. The Bell Journal of Economics, pages 324--340, 1982

work page 1982

-

[38]

Systems of ergodic BSDE s arising in regime switching forward performance processes

Ying Hu, Gechun Liang, and Shanjian Tang. Systems of ergodic BSDE s arising in regime switching forward performance processes. SIAM Journal on Control and Optimization, 58 0 (4): 0 2503--2534, 2020

work page 2020

-

[39]

Mean field stochastic games with discrete states and mixed players

Minyi Huang. Mean field stochastic games with discrete states and mixed players. In Game Theory for Networks: Third International ICST Conference, GameNets 2012, Vancouver, BC, Canada, May 24-26, 2012, Revised Selected Papers 3, pages 138--151. Springer, 2012

work page 2012

-

[40]

Minyi Huang, Roland P Malham \'e , and Peter E Caines. Large population stochastic dynamic games: Closed-loop mckean-vlasov systems and the nash certainty equivalence principle. Communications in Information and Systems, 6 0 (3): 0 221--252, 2006

work page 2006

-

[41]

On the industry concentration of actively managed equity mutual funds

Marcin Kacperczyk, Clemens Sialm, and Lu Zheng. On the industry concentration of actively managed equity mutual funds. The Journal of Finance, 60 0 (4): 0 1983--2011, 2005

work page 1983

-

[42]

Black's inverse investment problem and forward criteria with consumption

Sigrid Kallblad. Black's inverse investment problem and forward criteria with consumption. SIAM Journal on Financial Mathematics, 11 0 (2): 0 494--525, 2020

work page 2020

-

[43]

Dynamically consistent investment under model uncertainty: the robust forward criteria

Sigrid K \"a llblad, Jan Ob \'o j, and Thaleia Zariphopoulou. Dynamically consistent investment under model uncertainty: the robust forward criteria. Finance and Stochastics, 22 0 (4): 0 879--918, 2018

work page 2018

-

[44]

Many-player games of optimal consumption and investment under relative performance criteria

Daniel Lacker and Agathe Soret. Many-player games of optimal consumption and investment under relative performance criteria. Mathematics and Financial Economics, 14 0 (2): 0 263--281, 2020

work page 2020

-

[45]

Mean field and n-agent games for optimal investment under relative performance criteria

Daniel Lacker and Thaleia Zariphopoulou. Mean field and n-agent games for optimal investment under relative performance criteria. Mathematical Finance, 29 0 (4): 0 1003--1038, 2019

work page 2019

-

[46]

Jean-Michel Lasry and Pierre-Louis Lions. Mean field games. Japanese journal of mathematics, 2 0 (1): 0 229--260, 2007

work page 2007

-

[47]

Gechun Liang and Thaleia Zariphopoulou. Representation of homothetic forward performance processes in stochastic factor models via ergodic and infinite horizon BSDE . SIAM Journal on Financial Mathematics, 8 0 (1): 0 344--372, 2017

work page 2017

-

[48]

Gechun Liang, Moris S Strub, and Yuwei Wang. Predictable forward performance processes: Infrequent evaluation and applications to human-machine interactions. Mathematical Finance, 33 0 (4): 0 1248--1286, 2023

work page 2023

-

[49]

A simple model of capital market equilibrium with incomplete information

Robert C Merton et al. A simple model of capital market equilibrium with incomplete information. The Journal of Finance, 42: 0 483--510, 1987

work page 1987

-

[50]

Forward exponential indifference valuation in an incomplete binomial model

M Musiela, E Sokolova, and T Zariphopoulou. Forward exponential indifference valuation in an incomplete binomial model. In Advanced Modelling in Mathematical Finance, pages 277--302. Springer, 2016

work page 2016

-

[51]

Investments and forward utilities

Marek Musiela and Thaleia Zariphopoulou. Investments and forward utilities. Technical report, University of Texas at Austin, 2006

work page 2006

-

[52]

Optimal asset allocation under forward exponential performance criteria

Marek Musiela and Thaleia Zariphopoulou. Optimal asset allocation under forward exponential performance criteria. Markov Processes and Related Topics: a Festschrift for Thomas G. Kurtz, 4: 0 285--300, 2008

work page 2008

-

[53]

Portfolio choice under dynamic investment performance criteria

Marek Musiela and Thaleia Zariphopoulou. Portfolio choice under dynamic investment performance criteria. Quantitative Finance, 9 0 (2): 0 161--170, 2009

work page 2009

-

[54]

Portfolio choice under space-time monotone performance criteria

Marek Musiela and Thaleia Zariphopoulou. Portfolio choice under space-time monotone performance criteria. SIAM Journal on Financial Mathematics, 1 0 (1): 0 326--365, 2010

work page 2010

-

[55]

Optimal investment for all time horizons and M artin boundary of space-time diffusions

Sergey Nadtochiy and Michael Tehranchi. Optimal investment for all time horizons and M artin boundary of space-time diffusions. Mathematical Finance, 27 0 (2): 0 438--470, 2017

work page 2017

-

[56]

On the direction of preference for moments of higher order than the variance

Robert C Scott and Philip A Horvath. On the direction of preference for moments of higher order than the variance. The Journal of finance, 35 0 (4): 0 915--919, 1980

work page 1980

-

[57]

Mykhaylo Shkolnikov, Ronnie Sircar, and Thaleia Zariphopoulou. Asymptotic analysis of forward performance processes in incomplete markets and their ill-posed HJB equations. SIAM Journal on Financial Mathematics, 7 0 (1): 0 588--618, 2016

work page 2016

-

[58]

Evolution of the A rrow-- P ratt measure of risk-tolerance for predictable forward utility processes

Moris S Strub and Xun Yu Zhou. Evolution of the A rrow-- P ratt measure of risk-tolerance for predictable forward utility processes. Finance and Stochastics, 25 0 (2): 0 331--358, 2021

work page 2021

-

[59]

A dual characterization of self-generation and exponential forward performances

Gordan Z itkovi \'c . A dual characterization of self-generation and exponential forward performances. The Annals of Applied Probability, 19 0 (6): 0 2176--2210, 2009

work page 2009

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.