Limiting spectral distributions of large consistent rank correlation matrices

Pith reviewed 2026-05-07 12:36 UTC · model grok-4.3

The pith

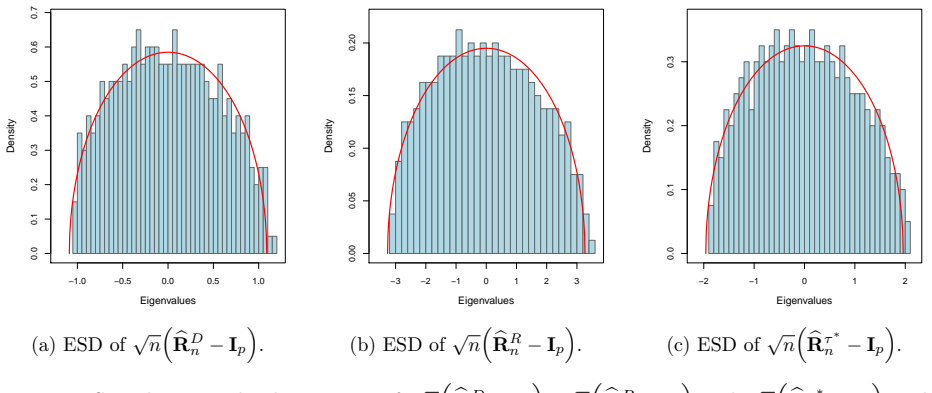

For consistent rank correlations such as Hoeffding's D, the empirical spectral distribution of the resulting large matrices converges to the semicircle law in the high-dimensional proportional regime.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We prove that for random matrices whose entries are given by consistent rank correlations such as Hoeffding's D applied pairwise to a high-dimensional random vector with mutually independent components, in the proportional regime where the dimensions tend to infinity at comparable rates, the limiting spectral distribution is the semicircle law. This generalizes the earlier result for Chatterjee's rank correlation.

What carries the argument

The consistent rank correlation matrix, formed by pairwise application of a consistent rank correlation function to the components of the random vector, whose empirical spectral distribution is shown to converge to the semicircle law.

Load-bearing premise

The components of the high-dimensional random vector are mutually independent, and the matrix size and sample size both tend to infinity with their ratio approaching a constant.

What would settle it

Generate many independent realizations of such a rank correlation matrix for large dimensions, say n=p=1000, compute the empirical spectral distribution, and check if it matches the semicircle law density rather than Marchenko-Pastur; a significant deviation would falsify the claim.

Figures

read the original abstract

We study random matrices whose entries are obtained by applying consistent rank correlations, such as Hoeffding's $D$, pairwise to a high-dimensional random vector with mutually independent components. Prior work has shown that, in the proportional high-dimensional regime, the empirical spectral distributions of large Kendall's tau and Spearman's rho matrices converge weakly almost surely to the Marchenko--Pastur law. By contrast, we prove that for consistent rank correlations such as Hoeffding's $D$, the limiting spectral distribution is given by the semicircle law. Our result thus generalizes a recent work of Dong, Han, and Yao (2025), who considered the special case of Chatterjee's rank correlation and established the first semicircle law for a large correlation matrix in the proportional regime.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims to prove that random matrices formed by applying consistent rank correlations (such as Hoeffding's D) pairwise to a high-dimensional random vector with mutually independent components have empirical spectral distributions that converge weakly almost surely to the semicircle law in the proportional regime. This contrasts with the Marchenko-Pastur law established for Kendall's tau and Spearman's rho matrices, and generalizes the Chatterjee rank correlation result of Dong, Han, and Yao (2025) by verifying that the joint moments of the matrix entries match those required for the semicircle law under the stated independence.

Significance. If the result holds, it is significant for random matrix theory and high-dimensional statistics because it identifies a class of rank correlations that produce Wigner-type semicircle spectra rather than Marchenko-Pastur, with potential implications for eigenvalue-based inference on dependence structures. The generalization from the Chatterjee case and the explicit verification of moment conditions using standard tools (moment method or linearization) are strengths; the manuscript supplies the technical steps that close the gap from the abstract.

minor comments (2)

- [§2] The definition and key properties of 'consistent rank correlation' (used to ensure the moment matching) should be stated explicitly in §2 with a short derivation or reference for Hoeffding's D to aid readability.

- [Main theorem] In the statement of the main theorem (likely Theorem 1.1 or 3.1), the precise conditions on the dimension ratio c = p/n and the moment assumptions on the underlying random vector components could be listed more prominently for quick reference.

Simulated Author's Rebuttal

We thank the referee for their positive summary of our manuscript and for recommending minor revision. The referee accurately captures our main result: that consistent rank correlation matrices (such as those based on Hoeffding's D) have empirical spectral distributions converging weakly almost surely to the semicircle law in the proportional regime, in contrast to the Marchenko-Pastur law for Kendall's tau and Spearman's rho, and generalizing the Chatterjee case of Dong, Han, and Yao (2025).

Circularity Check

Minor self-citation to prior special case; no load-bearing circularity

full rationale

The paper establishes the semicircle law for ESDs of consistent rank correlation matrices (e.g., Hoeffding's D) via direct application of moment methods or linearization in the proportional regime under componentwise independence. The sole self-citation is to the authors' 2025 special-case result on Chatterjee's correlation, which is invoked only for context as a generalization target; the current manuscript explicitly supplies the technical steps that extend the argument. No derivation step reduces by construction to a fitted parameter, self-definition, or unverified self-citation chain. The result remains self-contained against standard RMT benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption The high-dimensional random vector has mutually independent components.

- domain assumption The regime is proportional high-dimensional (dimensions tend to infinity at the same rate).

Reference graph

Works this paper leans on

-

[1]

Bai, Z. and Silverstein, J. W. (2010).Spectral Analysis of Large Dimensional Random Matrices. Springer New York, NY. Bai, Z. and Zhou, W. (2008). Large sample covariance matrices without independence structures in columns.Statistica Sinica, 18(2):425–442. Bai, Z. D. and Yin, Y. Q. (1988). Convergence to the semicircle law.The Annals of Probability, 16(2):...

-

[2]

Hoeffding, W. (1948). A non-parametric test of independence.Annals of Mathematical Statistics, 19(4):546–557. Jiang, T. (2004). The limiting distributions of eigenvalues of sample correlation matrices.Sankhy¯ a: The Indian Journal of Statistics, 66(1):35–48. Lin, Z. and Han, F. (2022). Limit theorems of Chatterjee’s rank correlation.arXiv preprint arXiv:2...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.