New Confidence Regions for Linear Regression Parameters with Stationary-Ergodic Dependent Errors

Pith reviewed 2026-05-21 03:05 UTC · model grok-4.3

The pith

A random-smoothing estimator with an auxiliary sample produces valid joint confidence regions for linear regression coefficients under stationary ergodic errors without estimating long-run variance.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under stationarity, ergodicity, and finite second moments, the random-smoothing estimator applied to a vector of regression and second-moment statistics is asymptotically normal and yields Wald confidence regions and simultaneous confidence intervals without direct long-run variance estimation or a parametric dependence model.

What carries the argument

The random-smoothing estimator, which uses an independent auxiliary sample and shrinking bandwidth applied to the vector of regression and second-moment statistics.

If this is right

- Wald confidence regions can be formed directly from the smoothed estimator without separate long-run variance estimation.

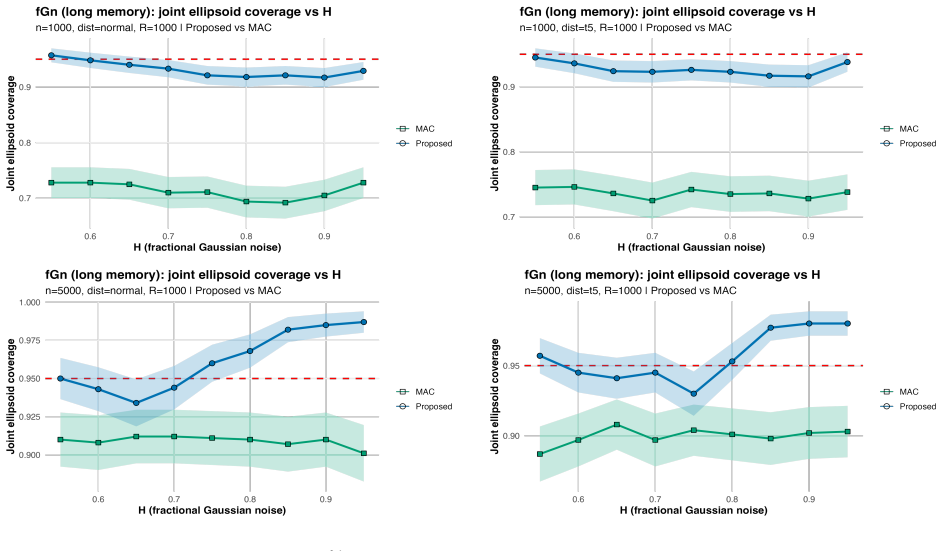

- The procedure applies to diverse dependence structures including ARMA, ARFIMA, copula-based Markov chains, and fractional Gaussian noise.

- A scaled version with data-driven bandwidth and mild truncation yields improved finite-sample stability.

- Simulations demonstrate near-nominal coverage and competitive region volumes relative to Newey-West and MAC estimators.

Where Pith is reading between the lines

- The method might reduce the practical burden of covariance estimation in other linear models with time-series dependence.

- Extensions could test performance when the auxiliary sample size is chosen adaptively rather than fixed.

- Similar smoothing could be applied to construct intervals for nonlinear functionals of the same stationary ergodic data.

Load-bearing premise

The regressors and errors are jointly stationary and ergodic with finite second moments, the auxiliary sample is independent of the main sample, and the bandwidth shrinks at a suitable rate.

What would settle it

If large-sample simulations or applications from jointly stationary ergodic processes show empirical coverage of the constructed regions falling substantially below nominal levels, the asymptotic normality and validity claim would be falsified.

Figures

read the original abstract

We develop joint confidence regions for linear regression coefficients when the regressors and errors are jointly stationary and ergodic with unspecified serial dependence. The method applies random smoothing, using an independent auxiliary sample and shrinking bandwidth, to a vector of regression and second-moment statistics. Under stationarity, ergodicity, and finite second moments, the estimator is asymptotically normal and yields Wald confidence regions and simultaneous confidence intervals without direct long-run variance estimation or a parametric dependence model. For implementation, we introduce a scaled estimator with data-driven bandwidth selection and a mild truncation that improves finite-sample stability. Simulations under ARMA, ARFIMA, copula-based Markov errors, and fractional Gaussian noise, with Gaussian and heavy-tailed margins, show near-nominal coverage and competitive region volumes relative to Newey-West HAC and MAC. A winter Beijing PM2.5 application illustrates the procedure. Keywords: Random smoothing, Joint inference, Confidence regions, Dependent errors, Long memory, Regression inference

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops a random-smoothing estimator for constructing joint Wald confidence regions and simultaneous intervals for linear regression coefficients when regressors and errors are jointly stationary and ergodic with unspecified serial dependence. An independent auxiliary sample and shrinking bandwidth are applied to a vector of regression and second-moment statistics; under stationarity, ergodicity, and finite second moments the estimator is shown to be asymptotically normal, yielding the regions without direct long-run variance estimation or a parametric dependence model. A scaled version with data-driven bandwidth selection and mild truncation is proposed for implementation. Simulations under ARMA, ARFIMA, copula Markov, and fractional Gaussian noise (Gaussian and heavy-tailed) demonstrate near-nominal coverage and competitive volumes relative to Newey-West HAC and MAC; a Beijing PM2.5 application is included.

Significance. If the central asymptotic normality result holds under the stated conditions, the approach supplies a flexible, model-free alternative to HAC-based inference for time-series regression, particularly useful when dependence is complex or long-range. The avoidance of explicit long-run variance estimation and the data-driven bandwidth are practical strengths. Reproducible simulation code and coverage across diverse dependence structures (including long-memory cases) add value; the method could see use in environmental and econometric applications where standard HAC procedures are sensitive to bandwidth choice.

major comments (2)

- [Asymptotic theory section] Asymptotic theory section: the statement of asymptotic normality requires explicit rates on the bandwidth h_n (e.g., h_n → 0 with n h_n → ∞ or analogous) and on the auxiliary-sample size relative to the main sample; without these rates stated as assumptions or lemmas, it is impossible to confirm that the Wald-region construction follows directly from the limiting normal distribution under only stationarity, ergodicity, and second-moment finiteness.

- [Implementation and simulation sections] Implementation and simulation sections: the data-driven bandwidth procedure is described as scaled and truncated, yet no consistency result or rate condition is supplied showing that the selected bandwidth satisfies the requirements of the asymptotic theory; this leaves a gap between the theoretical justification and the practical estimator used in the reported coverage probabilities.

minor comments (2)

- [Abstract] Abstract: the claim of 'without direct long-run variance estimation' is correct but could briefly note that random smoothing still produces an implicit smoothed covariance; a one-sentence clarification would avoid potential misreading.

- [Simulation tables] Simulation tables: for the fractional-Gaussian-noise heavy-tailed case the reported region volumes are larger than those of MAC; adding a short discussion of this trade-off would help readers decide when the new method is preferable.

Simulated Author's Rebuttal

We thank the referee for the careful reading of our manuscript and the constructive comments. We respond to each major comment below.

read point-by-point responses

-

Referee: [Asymptotic theory section] Asymptotic theory section: the statement of asymptotic normality requires explicit rates on the bandwidth h_n (e.g., h_n → 0 with n h_n → ∞ or analogous) and on the auxiliary-sample size relative to the main sample; without these rates stated as assumptions or lemmas, it is impossible to confirm that the Wald-region construction follows directly from the limiting normal distribution under only stationarity, ergodicity, and second-moment finiteness.

Authors: We appreciate the referee highlighting this point. The proof of Theorem 1 does rely on the bandwidth satisfying h_n → 0 and n h_n → ∞ (to ensure vanishing bias while retaining sufficient variability for the random smoothing) together with the auxiliary sample size m_n satisfying m_n = o(n) (to preserve the joint stationarity-ergodicity and independence from the main sample). These rates are used to establish the limiting normal distribution and the subsequent Wald construction. We will revise the asymptotic theory section to state these conditions explicitly as assumptions and add a short lemma that isolates the limiting result under the stated rates. This will make the passage from asymptotic normality to the confidence regions fully transparent. revision: yes

-

Referee: [Implementation and simulation sections] Implementation and simulation sections: the data-driven bandwidth procedure is described as scaled and truncated, yet no consistency result or rate condition is supplied showing that the selected bandwidth satisfies the requirements of the asymptotic theory; this leaves a gap between the theoretical justification and the practical estimator used in the reported coverage probabilities.

Authors: We agree that a formal consistency result for the data-driven selector would close the theoretical gap. Under the fully nonparametric stationary-ergodic setting, however, proving that the selected bandwidth automatically satisfies the required rates would demand additional structure (e.g., specific mixing coefficients or long-memory parameters) that we deliberately avoid. The scaling and mild truncation are instead constructed to keep the chosen h_n inside the admissible range for the asymptotics, and the extensive simulation study (ARMA, ARFIMA, copula Markov, fractional Gaussian noise, both Gaussian and heavy-tailed) shows near-nominal coverage. In the revision we will add a paragraph in the implementation section that explicitly acknowledges the heuristic character of the selector, states the truncation bounds, and reports supplementary simulation results that compare the data-driven choice against fixed bandwidths known to obey the rates. revision: partial

Circularity Check

No significant circularity in derivation chain

full rationale

The paper derives asymptotic normality of the random-smoothing estimator directly from joint stationarity, ergodicity, and finite second-moment assumptions on regressors and errors, together with an independent auxiliary sample and bandwidth shrinking at a suitable rate. Wald regions and simultaneous intervals are then obtained from the limiting normal distribution without any redefinition of the long-run variance or fitting of the target quantity to the same data. No self-citation is invoked as a load-bearing uniqueness theorem, no ansatz is smuggled via prior work, and the data-driven bandwidth is presented as a tuning parameter rather than a circular re-expression of the quantity being estimated. The derivation therefore remains self-contained against external asymptotic theory and does not reduce to its inputs by construction.

Axiom & Free-Parameter Ledger

free parameters (1)

- bandwidth

axioms (2)

- domain assumption Regressors and errors are jointly stationary and ergodic with finite second moments

- domain assumption Auxiliary sample is independent of the main sample

Reference graph

Works this paper leans on

-

[1]

Andrews, Donald W. K. , title =. Econometrica , volume =. 1991 , doi =

work page 1991

-

[2]

Kiefer, Nicholas M. and Vogelsang, Timothy J. , title =. Econometric Theory , volume =. 2002 , doi =

work page 2002

-

[3]

Journal of the Royal Statistical Society: Series B (Statistical Methodology) , volume =

Shao, Xiaofeng , title =. Journal of the Royal Statistical Society: Series B (Statistical Methodology) , volume =. 2010 , doi =

work page 2010

-

[4]

The Jackknife and the Bootstrap for General Stationary Observations , journal =

K. The Jackknife and the Bootstrap for General Stationary Observations , journal =. 1989 , doi =

work page 1989

-

[5]

Politis, Dimitris N. and Romano, Joseph P. , title =. Journal of the American Statistical Association , volume =. 1994 , doi =

work page 1994

-

[6]

The Annals of Statistics , volume =

Yajima, Yoshihiro , title =. The Annals of Statistics , volume =

-

[7]

Robinson, Peter M. and Hidalgo, Javier , title =. The Annals of Statistics , volume =. 1997 , doi =

work page 1997

-

[8]

Ibragimov, Rustam and Kim, Jihyun and Skrobotov, Anton , title =. Econometric Theory , volume =. 2024 , doi =

work page 2024

-

[9]

Baillie, Richard T. and Diebold, Francis X. and Kapetanios, George and Kim, Kun Ho and Mora, Aaron , title =. The Econometrics Journal , volume =. 2025 , doi =

work page 2025

-

[10]

Statistics & Probability Letters , volume =

Ko, Kyungduk and Lee, Jaechoul and Lund, Robert , title =. Statistics & Probability Letters , volume =. 2008 , doi =

work page 2008

-

[11]

Dependence and mixing for perturbations of copula-based Markov chains , journal =

Martial Longla and Mathias. Dependence and mixing for perturbations of copula-based Markov chains , journal =. 2021 , issn =. doi:10.1016/j.spl.2021.109239 , url =

-

[12]

and Distaso, Walter and Giraitis, Liudas , title =

Abadir, Karim M. and Distaso, Walter and Giraitis, Liudas , title =. Journal of Econometrics , volume =. 2009 , doi =

work page 2009

- [13]

-

[14]

Newey, Whitney K. and West, Kenneth D. , title =. Econometrica , year =

-

[15]

Newey, Whitney K. and West, Kenneth D. , title =. Review of Economic Studies , year =

- [16]

-

[17]

Journal of Time Series Analysis , year =

Geweke, John and Porter-Hudak, Susan , title =. Journal of Time Series Analysis , year =

-

[18]

and Deo, Rohit and Brodsky, Jonathan , title =

Hurvich, Clifford M. and Deo, Rohit and Brodsky, Jonathan , title =. Journal of Time Series Analysis , year =

- [19]

-

[20]

Candanedo, Luis M. and Feldheim, V. Data driven prediction models of energy use of appliances in a low-energy house , journal =. 2017 , doi =

work page 2017

- [21]

-

[22]

Aimino, R. and Nicol, M. and Vaienti, S. , title =. Probability Theory and Related Fields , year =

-

[23]

Billingsley, Patrick , title =

-

[24]

Annals of Probability , volume =

Peligrad, Magda and Utev, Sergey , title =. Annals of Probability , volume =. 1997 , publisher =

work page 1997

- [25]

- [26]

-

[27]

The Annals of Probability , volume =

Ou Zhao and Michael Woodroofe , title =. The Annals of Probability , volume =. 2008 , month = jan, publisher =

work page 2008

-

[28]

C. Cuny and M. Peligrad , title =. Journal of Theoretical Probability , volume =. 2012 , doi =

work page 2012

-

[29]

Cuny, C. and Merlev. On martingale approximations and the quenched weak invariance principle , journal =. 2014 , volume =

work page 2014

-

[30]

Dedecker, J. and Merlev. Necessary and sufficient conditions for the conditional central limit theorem , journal =. 2002 , volume =

work page 2002

-

[31]

A spectral approach for quenched limit theorems for random expanding dynamical systems , journal =

Dragi. A spectral approach for quenched limit theorems for random expanding dynamical systems , journal =. 2018 , volume =

work page 2018

-

[32]

Almost sure invariance principle for random piecewise expanding maps , journal =

Dragi. Almost sure invariance principle for random piecewise expanding maps , journal =. 2018 , volume =

work page 2018

- [33]

-

[34]

Rosenblatt, M. , title =. Proceedings of the National Academy of Sciences of the United States of America , year =. doi:10.1073/pnas.42.1.43 , url =

- [35]

- [36]

-

[37]

Quenched central limit theorems for sums of stationary processes , journal =

Voln. Quenched central limit theorems for sums of stationary processes , journal =. 2014 , volume =

work page 2014

-

[38]

Quenched central limit theorems for a stationary linear process , journal =

Voln. Quenched central limit theorems for a stationary linear process , journal =. 2017 , volume =

work page 2017

-

[39]

Volkonskii, V. A. and Rozanov, Yu. A. , title =. Theory of Probability and Its Applications , year =. doi:10.1137/1104018 , mrnumber =

-

[40]

Volkonskii, V. A. and Rozanov, Yu. A. , title =. Theory of Probability and Its Applications , year =

-

[41]

Ibragimov, I.A. , title =. Theory of Probability and Its Applications , year =. doi:10.1137/1107036 , url =

- [42]

-

[43]

Huang, J. S. and Kotz, S. , title =. Metrika , year =

-

[44]

Lai, C. D. and Xie, M. , title =. Statistics & Probability Letters , year =

- [45]

-

[46]

A new class of bivariate copulas , journal =

Rodr\'. A new class of bivariate copulas , journal =. 2004 , volume =

work page 2004

-

[47]

The Annals of Mathematical Statistics , volume =

Murray Rosenblatt , title =. The Annals of Mathematical Statistics , volume =. 1952 , month = sep, publisher =

work page 1952

- [48]

- [49]

- [50]

- [51]

- [52]

-

[53]

Birkhoff, George D. , title =. Proc. Natl. Acad. Sci. USA , issn =. 1931 , language =. doi:10.1073/pnas.17.12.656 , keywords =

-

[54]

Dependence in a background risk model , journal =

C. Dependence in a background risk model , journal =. 2019 , volume =

work page 2019

- [55]

-

[56]

Johnson, N. L. and Kott, S. , title =. Communications in Statistics , volume =

- [57]

-

[58]

Kolmogorov, A. N. , title =. Mathematische Annalen , year =

-

[59]

R. H. Somers , title =. American Sociological Review , year =. doi:10.2307/2090408 , jstor =

- [60]

-

[61]

The American Journal of Psychology , volume =

Spearman, Charles , title =. The American Journal of Psychology , volume =. 1904 , publisher =

work page 1904

-

[62]

Kendall, Maurice G. and Stuart, Alan , title =. 1961 , address =

work page 1961

-

[63]

and Chakraborti, Subhabrata , title =

Gibbons, John D. and Chakraborti, Subhabrata , title =

-

[64]

Conover, W. J. , title =

-

[65]

Psychological Reports , volume =

Gerjuoy, Harold , title =. Psychological Reports , volume =. 1962 , doi =

work page 1962

-

[66]

Journal of Multivariate Analysis , volume =

Schmid, Friedrich and Schmidt, Rafael , title =. Journal of Multivariate Analysis , volume =. 2007 , issn =

work page 2007

-

[67]

Journal of Statistical Planning and Inference , volume =

On the Relationship between Spearman’s Rho and Kendall’s Tau for Pairs of Continuous Random Variables , author =. Journal of Statistical Planning and Inference , volume =. 2007 , doi =

work page 2007

-

[68]

Lehmann, E. L. , title =. 1975 , address =

work page 1975

-

[69]

Caperaa, G. and Genest, C. , title =. Journal of Nonparametric Statistics , volume =

-

[70]

Leo A. Goodman and William H. Kruskal , title =. Journal of the American Statistical Association , year =. doi:10.2307/2281536 , jstor =

- [71]

-

[72]

Comparative study of estimation methods for a new family of copula based reversible Markov chains , author=

- [73]

- [74]

-

[75]

Recent development in copula and its applications to the energy, forestry and environmental sciences , journal =. 2019 , author =

work page 2019

-

[76]

On the strong law of large numbers for a class of stochastic processes , journal =. 1963 , author =

work page 1963

-

[77]

On the \( \)-mixing condition for stationary random sequences , journal =. 1983 , author =

work page 1983

-

[78]

Annals of Probability , volume =

Peligrad, Magda , title =. Annals of Probability , volume =. 1998 , doi =

work page 1998

-

[79]

Nadaraya, E. A. , title =. Theory of Probability & Its Applications , volume =. 1964 , doi =

work page 1964

-

[80]

Watson, G. S. , title =. Sankhy\=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.