TripleWin: Fixed-Point Equilibrium Pricing for Data-Model Coupled Markets

Pith reviewed 2026-05-18 00:41 UTC · model grok-4.3

The pith

Coupled data and model markets reach unique equilibrium prices by proving their joint pricing operator is a standard interference function.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

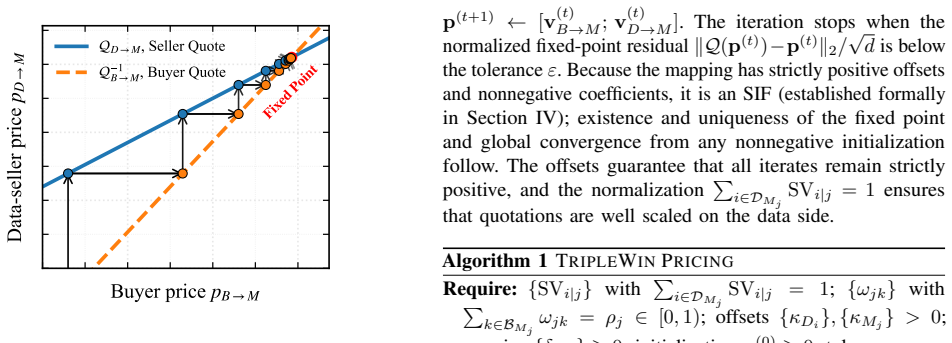

We propose a unified data-model coupled market that treats dataset and model trading as a single system. A supply-side mapping transforms dataset payments into buyer-visible model quotations, while a demand-side mapping propagates buyer prices back to datasets through Shapley-based allocation. Together, they form a closed loop that links four interactions: supply-demand propagation in both directions and mutual coupling among buyers and among sellers. We prove that the joint operator is a standard interference function (SIF), guaranteeing existence, uniqueness, and global convergence of equilibrium prices.

What carries the argument

The joint operator formed by the supply-side mapping from dataset payments to model quotations and the demand-side mapping from buyer prices to Shapley allocations, shown to be a standard interference function.

If this is right

- Equilibrium prices exist and are unique in the coupled market.

- Global convergence of prices occurs through iterative updates from any initial values.

- Payments achieve greater fairness across data sellers, model producers, and buyers than broker-centric methods.

- Convergence remains efficient, stabilizing after few iterations in tested market sizes.

Where Pith is reading between the lines

- The closed-loop design could support real-time price adjustments as new buyers or sellers enter the market.

- Similar fixed-point analyses might apply to other interdependent resource markets in AI such as data and compute bundles.

- Approximations in Shapley calculations for large datasets would require separate verification that the interference property still holds.

Load-bearing premise

The supply-side mapping from dataset payments to model quotations and the demand-side mapping from buyer prices back to datasets via Shapley allocation together form a closed loop that accurately captures the four interactions without additional external market assumptions.

What would settle it

Simulating the market with multiple participants and iterating the price updates from diverse starting points to check if they all arrive at the identical equilibrium price vector or if some paths lead to different outcomes or fail to stabilize.

Figures

read the original abstract

The rise of the machine learning (ML) model economy has intertwined markets for training datasets and pre-trained models. However, most pricing approaches still separate data and model transactions or rely on broker-centric pipelines that favor one side. Recent studies of data markets with externalities capture buyer interactions but do not yield a simultaneous and symmetric mechanism across data sellers, model producers, and model buyers. We propose a unified data-model coupled market that treats dataset and model trading as a single system. A supply-side mapping transforms dataset payments into buyer-visible model quotations, while a demand-side mapping propagates buyer prices back to datasets through Shapley-based allocation. Together, they form a closed loop that links four interactions: supply-demand propagation in both directions and mutual coupling among buyers and among sellers. We prove that the joint operator is a standard interference function (SIF), guaranteeing existence, uniqueness, and global convergence of equilibrium prices. Experiments demonstrate efficient convergence and improved fairness compared with broker-centric and one-sided baselines. The code is available on https://github.com/HongrunRen1109/Triple-Win-Pricing.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces TripleWin, a unified fixed-point pricing framework for data-model coupled markets. It defines a supply-side mapping from dataset payments to model quotations and a demand-side mapping from buyer prices back to datasets via Shapley value allocation; these compose into a joint operator. The central claim is that this operator is a standard interference function (SIF), which implies existence, uniqueness, and global convergence of equilibrium prices. Experiments on synthetic and real datasets show faster convergence and better fairness metrics than broker-centric and one-sided baselines; code is released.

Significance. If the SIF property is established without hidden linearity assumptions, the work supplies a symmetric, closed-loop mechanism that simultaneously prices data sellers, model producers, and buyers—an advance over separated or broker-mediated schemes. The public code and convergence experiments are positive for reproducibility. The result would be of interest to mechanism-design and data-market communities, but its impact is limited by the unresolved scalability step in the SIF argument.

major comments (2)

- [§4.3, Theorem 2] §4.3 (SIF proof, Theorem 2): the scalability claim T(αp) < α T(p) for α > 1 is asserted after composing the supply mapping with the Shapley allocation. However, Shapley values are linear combinations of marginal contributions v(S ∪ {i}) − v(S), where v is the model-performance or revenue function induced by the price vector. If v exhibits concavity or diminishing returns (common in ML utility models), then v(αp) ≠ α v(p) and the composed operator need not satisfy strict scalability. The proof sketch does not state the functional form of v or provide a counter-example check; this is load-bearing for uniqueness and global convergence.

- [§3.2] §3.2 (demand-side mapping): the Shapley allocation is defined on buyer prices without an explicit statement of whether the characteristic function v is recomputed from scratch or approximated on the same data used for model training. If the two coincide, the closed-loop operator risks circularity, weakening the claim that the four interactions are captured without external market assumptions.

minor comments (2)

- [§3, §5] Notation for the joint operator T is introduced in §3 but reused without redefinition in the convergence plots of §5; a single equation reference would improve readability.

- [Table 2] Table 2 reports fairness improvements but omits standard deviations across the 10 random seeds mentioned in the text; adding error bars would strengthen the experimental claims.

Simulated Author's Rebuttal

We are grateful to the referee for the detailed and insightful comments on our paper. We respond to each major comment below and indicate the revisions made to the manuscript.

read point-by-point responses

-

Referee: [§4.3, Theorem 2] §4.3 (SIF proof, Theorem 2): the scalability claim T(αp) < α T(p) for α > 1 is asserted after composing the supply mapping with the Shapley allocation. However, Shapley values are linear combinations of marginal contributions v(S ∪ {i}) − v(S), where v is the model-performance or revenue function induced by the price vector. If v exhibits concavity or diminishing returns (common in ML utility models), then v(αp) ≠ α v(p) and the composed operator need not satisfy strict scalability. The proof sketch does not state the functional form of v or provide a counter-example check; this is load-bearing for uniqueness and global convergence.

Authors: We appreciate the referee pointing out this potential issue with the scalability property. In the TripleWin framework, the revenue function v is constructed to be linear in the price vector, ensuring v(αp) = α v(p) for α > 0. This linearity arises from the proportional payment structure in the market mechanism. We have revised the manuscript in §4.3 to explicitly state this assumption and added a paragraph explaining why concavity does not apply in our model. We also included an empirical verification in the appendix demonstrating that the scalability holds in our experiments. If the referee has a specific concave v in mind, we would be happy to discuss further. revision: yes

-

Referee: [§3.2] §3.2 (demand-side mapping): the Shapley allocation is defined on buyer prices without an explicit statement of whether the characteristic function v is recomputed from scratch or approximated on the same data used for model training. If the two coincide, the closed-loop operator risks circularity, weakening the claim that the four interactions are captured without external market assumptions.

Authors: We thank the referee for this comment. The characteristic function v is recomputed from scratch at each iteration of the fixed-point algorithm using the current buyer price vector to calculate the marginal contributions for the Shapley values. It is not approximated on the training data in a way that creates circularity; the model performance is evaluated based on the datasets allocated according to the current prices. This iterative recomputation is part of the closed-loop mechanism. We have updated the description in §3.2 to make this process explicit and to emphasize that no external market assumptions are needed beyond the defined mappings. revision: yes

Circularity Check

No circularity: SIF proof is independent verification on defined operator

full rationale

The paper defines a joint operator via explicit supply-side mapping (dataset payments to model quotations) and demand-side mapping (buyer prices to datasets via Shapley allocation), then proves this operator satisfies the three SIF axioms (positivity, monotonicity, scalability). This is a direct mathematical check of properties on the constructed function, not a reduction of the claimed existence/uniqueness/convergence result to a fitted parameter, self-citation chain, or input by construction. The SIF concept is an external standard from the literature; the proof supplies independent content by verifying the axioms hold for the paper's specific closed-loop definitions. No load-bearing step collapses to renaming or tautology.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The supply-side and demand-side mappings form a closed loop linking supply-demand propagation and mutual couplings among buyers and sellers

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

We prove that the joint operator is a standard interference function (SIF), guaranteeing existence, uniqueness, and global convergence of equilibrium prices.

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The mapping Q ... is positive, monotone, and scalable.

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Y . Pan, Z. Su, Y . Wang, H. Liu, R. Li, and A. Benslimane, “Knowledge- aware privacy-preserving model customization in zero-trust federated learning model marketplaces,”IEEE J. Sel. Areas Commun., vol. 43, no. 6, pp. 1923–1937, 2025

work page 1923

-

[2]

Dealer: An end-to-end model marketplace with differential privacy,

J. Liu, J. Lou, J. Liu, L. Xiong, J. Pei, and J. Sun, “Dealer: An end-to-end model marketplace with differential privacy,”Proceedings of the VLDB Endowment, vol. 14, no. 6, pp. 957–969, 2021

work page 2021

-

[3]

Data pricing in machine learning pipelines,

Z. Cong, X. Luo, J. Pei, F. Zhu, and Y . Zhang, “Data pricing in machine learning pipelines,”Knowledge and Information Systems, vol. 64, no. 6, pp. 1417–1455, 2022

work page 2022

-

[4]

A survey on data pricing: From economics to data science,

J. Pei, “A survey on data pricing: From economics to data science,” IEEE Transactions on Knowledge and Data Engineering, vol. 34, no. 10, pp. 4586–4608, 2022

work page 2022

-

[5]

Modelplace: The marketplace for ai models

M. Inc, “Modelplace: The marketplace for ai models.” https://modelplace. ai/models, 2025

work page 2025

-

[6]

Datarade: Find the right data, effortlessly

D. Inc, “Datarade: Find the right data, effortlessly.” https://datarade.ai/, 2025

work page 2025

-

[7]

On scalable query pricing in data marketplaces,

H. Peng, X. Miao, Y . Fu, J. Zhang, S. Deng, and J. Yin, “On scalable query pricing in data marketplaces,” in41st IEEE International Conference on Data Engineering, ICDE 2025, Hong Kong, May 19-23, 2025, pp. 3140– 3152, IEEE, 2025

work page 2025

-

[8]

J. Lu, T. Huang, S. Cao, S. Yu, R. Jia, and M. Li, “PIECE: incentivizing personalized privacy-preserving for multi-version model marketplace in federated learning,”IEEE Trans. Inf. Forensics Secur., vol. 20, pp. 9387– 9398, 2025

work page 2025

-

[9]

A marketplace for data: An algorithmic solution,

A. Agarwal, M. A. Dahleh, and T. Sarkar, “A marketplace for data: An algorithmic solution,” inProceedings of the 2019 ACM Conference on Economics and Computation (EC), pp. 701–726, ACM, 2019

work page 2019

-

[10]

Selling data to a machine learner: Pricing via costly signaling,

J. Chen, M. Li, and H. Xu, “Selling data to a machine learner: Pricing via costly signaling,” inProceedings of International Conference on Machine Learning (ICML), pp. 3336–3359, PMLR, 2022

work page 2022

-

[11]

Towards model-based pricing for machine learning in a data marketplace,

L. Chen, P. Koutris, and A. Kumar, “Towards model-based pricing for machine learning in a data marketplace,” inProceedings of the 2019 International Conference on Management of Data (SIGMOD), pp. 1535– 1552, ACM, 2019

work page 2019

-

[12]

Golden grain: Building a secure and decentralized model marketplace for mlaas,

J. Weng, J. Weng, C. Cai, H. Huang, and C. Wang, “Golden grain: Building a secure and decentralized model marketplace for mlaas,”IEEE Trans. Dependable Secur. Comput., vol. 19, no. 5, pp. 3149–3167, 2022

work page 2022

-

[13]

Survey of artificial intelligence model marketplace,

M. Qian, A. A. Musa, M. Biswas, Y . Guo, W. Liao, and W. Yu, “Survey of artificial intelligence model marketplace,”Future Internet, vol. 17, no. 1, p. 35, 2025

work page 2025

-

[14]

A profit-maximizing model marketplace with differentially private federated learning,

P. Sun, X. Chen, G. Liao, and J. Huang, “A profit-maximizing model marketplace with differentially private federated learning,” inProceedings of 2022 IEEE Conference on Computer Communications (INFOCOM), pp. 1439–1448, IEEE, 2022

work page 2022

-

[15]

A dynamic data trading marketplace with externalities,

S. Wang and D. H. K. Tsang, “A dynamic data trading marketplace with externalities,”IEEE Internet Things J., vol. 11, no. 7, pp. 12745–12754, 2024

work page 2024

-

[16]

A stackelberg game pricing for blockchain-based industrial internet of things data market,

T. Gao, S. Wang, X. Geng, L. Zhang, M. Jing, T. Yu, and J. Yu, “A stackelberg game pricing for blockchain-based industrial internet of things data market,” in28th International Conference on Computer Supported Cooperative Work in Design, CSCWD 2025, Compiegne, France, May 5-7, 2025(W. Shen, M. Abel, N. Matta, J. A. Barthès, J. Luo, J. Zhang, H. Zhu, and K...

work page 2025

-

[17]

A framework for uplink power control in cellular radio systems,

R. D. Yates, “A framework for uplink power control in cellular radio systems,”IEEE Journal on selected areas in communications, vol. 13, no. 7, pp. 1341–1347, 2002

work page 2002

-

[18]

Dataprice: An interactive system for pricing datasets in data marketplaces,

Y . Zhu, H. Zhang, J. Zhang, J. Liu, and K. Ren, “Dataprice: An interactive system for pricing datasets in data marketplaces,”Proc. VLDB Endow., vol. 17, no. 12, pp. 4433–4436, 2024

work page 2024

-

[19]

On designing market model and pricing mechanisms for iot data exchange,

Z. Zheng, W. Mao, Y . Xing, and F. Wu, “On designing market model and pricing mechanisms for iot data exchange,”IEEE Trans. Mob. Comput., vol. 23, no. 11, pp. 10202–10218, 2024

work page 2024

-

[20]

A socially optimal data marketplace with differentially private federated learning,

P. Sun, G. Liao, X. Chen, and J. Huang, “A socially optimal data marketplace with differentially private federated learning,”IEEE/ACM Trans. Netw., vol. 32, no. 3, pp. 2221–2236, 2024

work page 2024

-

[21]

Semi-private computation of data similarity with applications to data valuation and pricing,

R. B. Christensen, S. R. Pandey, and P. Popovski, “Semi-private computation of data similarity with applications to data valuation and pricing,”IEEE Trans. Inf. Forensics Secur., vol. 18, pp. 1978–1988, 2023

work page 1978

-

[22]

Towards query pricing on incomplete data,

X. Miao, Y . Gao, L. Chen, H. Peng, J. Yin, and Q. Li, “Towards query pricing on incomplete data,”IEEE Trans. Knowl. Data Eng., vol. 34, no. 8, pp. 4024–4036, 2022

work page 2022

-

[23]

Personal big data pricing method based on differential privacy,

Y . Shen, B. Guo, Y . Shen, X. Duan, X. Dong, H. Zhang, C. Zhang, and Y . Jiang, “Personal big data pricing method based on differential privacy,” Comput. Secur., vol. 113, p. 102529, 2022

work page 2022

-

[24]

Online query-based data pricing with time-discounting valuations,

Y . Fu, X. Miao, H. Peng, C. Na, S. Deng, and J. Yin, “Online query-based data pricing with time-discounting valuations,” in40th IEEE International Conference on Data Engineering, ICDE 2024, Utrecht, The Netherlands, May 13-16, 2024, pp. 3449–3461, IEEE, 2024

work page 2024

-

[25]

Privdata network: A privacy-preserving on-chain data factory and trading market,

T. Lu, B. Zhang, and K. Ren, “Privdata network: A privacy-preserving on-chain data factory and trading market,”IEEE Trans. Dependable Secur. Comput., vol. 21, no. 3, pp. 1424–1436, 2024

work page 2024

-

[26]

When crowdsourcing meets data markets: A fair data value metric for data trading,

Y . Liu, Z. Zheng, F. Wu, and G. Chen, “When crowdsourcing meets data markets: A fair data value metric for data trading,”J. Comput. Sci. Technol., vol. 39, no. 3, pp. 671–690, 2024

work page 2024

-

[27]

Mone- tizing personal data: A two-sided market approach,

A. S. Bataineh, R. Mizouni, M. E. Barachi, and J. Bentahar, “Mone- tizing personal data: A two-sided market approach,” inProceedings of the 7th International Conference on Ambient Systems, Networks and Technologies (ANT), pp. 472–479, Elsevier, 2016

work page 2016

-

[28]

Data quality scores for pricing on data marketplaces,

F. Stahl and G. V ossen, “Data quality scores for pricing on data marketplaces,” inProceedings of 8th Asian Conference on Intelligent Information and Database Systems, pp. 215–224, Springer, 2016

work page 2016

-

[29]

Data and AI model markets: Opportunities for data and model sharing, discovery, and integration,

J. Pei, R. C. Fernandez, and X. Yu, “Data and AI model markets: Opportunities for data and model sharing, discovery, and integration,” Proc. VLDB Endow., vol. 16, no. 12, pp. 3872–3873, 2023

work page 2023

-

[30]

A framework for reusing earth science data on data and model marketplaces,

C. Huang, J. Chang, C. Sun, T. Wang, W. Chen, H. H. Yu, W. Chang, and F. Lin, “A framework for reusing earth science data on data and model marketplaces,” inAsia Pacific Signal and Information Processing Association Annual Summit and Conference, APSIPA ASC 2023, Taipei, Taiwan, October 31 - Nov. 3, 2023, pp. 2256–2260, IEEE, 2023

work page 2023

-

[31]

N. Jagannath, C. Wong, B. McGrath, M. F. Hossain, A. A. Okon, A. Ja- malipour, and K. S. Munasinghe, “Enhancing trust in AI marketplaces: Evaluating on-chain verification of personalized AI models using zk- snarks,”CoRR, vol. abs/2504.04794, 2025

-

[32]

Flmarket: Enabling privacy-preserved pre-training data pricing for federated learning,

Z. Wen, W. Feng, D. Wu, H. Hu, C. Xu, B. Qian, Z. Hong, C. Wang, and S. Ji, “Flmarket: Enabling privacy-preserved pre-training data pricing for federated learning,” inProceedings of the 31st ACM SIGKDD Conference on Knowledge Discovery and Data Mining, V .1, KDD 2025, Toronto, ON, Canada, August 3-7, 2025, pp. 1587–1598, ACM, 2025

work page 2025

-

[33]

Share: Stackelberg- nash based data markets,

Y . Bi, J. Liu, C. Zhao, J. Zhao, K. Ren, and L. Xiong, “Share: Stackelberg- nash based data markets,” in40th IEEE International Conference on Data Engineering, ICDE 2024, Utrecht, The Netherlands, May 13-16, 2024, pp. 3573–3586, IEEE, 2024

work page 2024

-

[34]

Pricing-based stackelberg game for spectrum trading in self-organised heterogeneous networks,

S. Haddadi and A. Ghasemi, “Pricing-based stackelberg game for spectrum trading in self-organised heterogeneous networks,”IET Com- munications, vol. 10, no. 11, pp. 1374–1383, 2016

work page 2016

-

[35]

A stackelberg game pricing through balancing trilateral profits in big data market,

Z. Xiao, D. He, and J. Du, “A stackelberg game pricing through balancing trilateral profits in big data market,”IEEE Internet of Things Journal, vol. 8, no. 16, pp. 12658–12668, 2021

work page 2021

-

[36]

Oligopoly pricing and advertising in isoelastic adoption models,

K. Helmes and R. Schlosser, “Oligopoly pricing and advertising in isoelastic adoption models,”Dynamic Games and Applications, vol. 5, no. 3, pp. 334–360, 2015

work page 2015

-

[37]

A pricing game for federated learning supporting lightweight local model training,

F. Tian, M. Wang, Y . Zhang, G. Deng, L. Liang, and X. Zhang, “A pricing game for federated learning supporting lightweight local model training,”IEEE Trans. Mob. Comput., vol. 24, no. 11, pp. 12264–12281, 2025

work page 2025

-

[38]

Towards efficient data valuation based on the shapley value,

R. Jia, D. Dao, B. Wang, F. A. Hubis, N. Hynes, N. M. Gürel, B. Li, C. Zhang, D. Song, and C. J. Spanos, “Towards efficient data valuation based on the shapley value,” inProceedings of the 22nd International Conference on Artificial Intelligence and Statistics (AISTATS), pp. 1167– 1176, PMLR, 2019

work page 2019

-

[39]

Online data valuation and pricing for machine learning tasks in mobile health,

A. Xu, Z. Zheng, F. Wu, and G. Chen, “Online data valuation and pricing for machine learning tasks in mobile health,” inProceedings of 2022 IEEE Conference on Computer Communications (INFOCOM), pp. 850–859, IEEE, 2022

work page 2022

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.