Recognition: 2 theorem links

· Lean TheoremThe Screening Cost of Liquidity

Pith reviewed 2026-05-10 18:12 UTC · model grok-4.3

The pith

A principal with cheap capital optimally forces the counterparty to borrow at above-market rates because the form of finance itself screens types.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

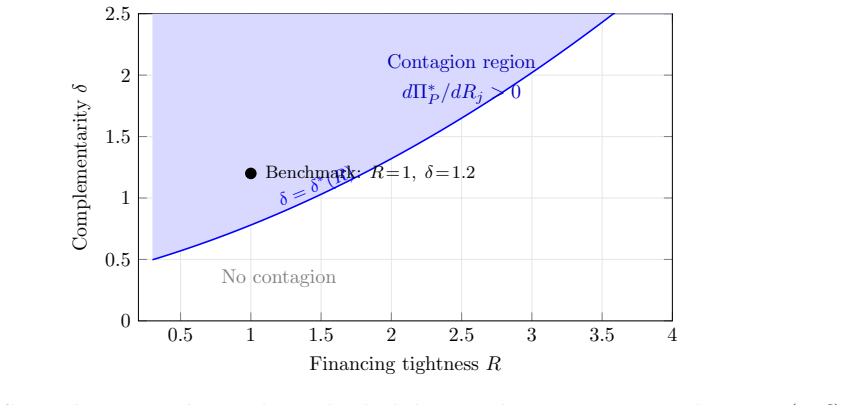

The optimal contract preserves outside-finance exposure to maintain screening power. Advances provide liquidity but pool types; contingent transfers separate types, but, because they are not pledgeable, impose financing costs. Two sufficient statistics pin down the optimal advance share. With complementary counterparties, a uniform subsidy that cheapens finance across every relationship can reduce the value of each.

What carries the argument

The optimal advance share, chosen to balance liquidity provision against the screening value of forcing the counterparty to use costly outside finance for the contingent portion.

If this is right

- Early payment and contingent compensation coexist in the same contract even when the principal could supply all funds cheaply.

- A uniform reduction in borrowing costs across all relationships can lower joint surplus when the parties' efforts or outputs are complements.

- The same contract form appears in trade credit, venture capital, and internal capital markets because each features a cheap-capital principal facing a less-well-financed counterparty.

- Changing the pledgeability of contingent claims would directly alter the optimal advance share.

Where Pith is reading between the lines

- The result suggests that observed reliance on expensive external finance in some deals may be an intentional feature of screening rather than a market friction.

- Policy efforts to subsidize all forms of finance uniformly could unintentionally weaken screening in complementary production settings.

- Empirical tests could examine whether the mix of advance size and contingent pay varies with measurable differences in outside borrowing rates across industries.

Load-bearing premise

Contingent transfers cannot be pledged, so they always cost the counterparty more to finance than the principal's own cheap capital.

What would settle it

Direct observation that counterparties in these relationships never use any outside borrowing for the contingent part of the contract, or that contingent claims can be pledged at the same low rate as advances.

Figures

read the original abstract

A principal with cheap capital optimally forces her counterparty to borrow at above-market rates. The reason: the form of finance is a screening device. Advances provide liquidity but pool types; contingent transfers separate types, but, because they are not pledgeable, impose financing costs. The optimal contract preserves outside-finance exposure to maintain screening power. Two sufficient statistics pin down the optimal advance share. With complementary counterparties, a uniform subsidy that cheapens finance across every relationship can reduce the value of each. This explains the coexistence of early payment and contingent compensation in trade credit, venture capital, and internal capital markets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models a principal with cheap capital who optimally forces her counterparty to maintain outside borrowing at above-market rates. Advances supply liquidity but pool types, while contingent transfers separate types yet are non-pledgeable and therefore carry higher financing costs. The optimal contract therefore preserves some outside-finance exposure to retain screening power. Two sufficient statistics determine the optimal advance share. When counterparties are complementary, a uniform subsidy that cheapens finance across relationships can reduce total value, rationalizing the observed mix of early payment and contingent compensation in trade credit, venture capital, and internal capital markets.

Significance. If the central mechanism holds, the paper supplies a screening rationale for why cheap capital is not fully advanced and why mixed financing persists across several institutional settings. The two-statistic characterization and the subsidy result are potentially portable to other contract-design problems.

major comments (2)

- [model primitives / abstract] The non-pledgeability of contingent transfers is stated as a primitive (abstract and model-setup section) rather than derived from verifiability, limited commitment, or the type space. Because this cost differential is load-bearing for the claim that outside exposure must be preserved, an endogenous derivation or a robustness check that relaxes the assumption would be required to support the central result.

- [optimal-contract section] The claim that two sufficient statistics fully pin down the optimal advance share is presented without an explicit derivation or statement of the statistics themselves. Without the relevant proposition or appendix, it is impossible to verify whether the characterization is parameter-free or relies on normalizations that could affect the screening trade-off.

minor comments (2)

- Notation for the two sufficient statistics should be introduced earlier and used consistently in the text and any figures.

- The discussion of complementary counterparties would benefit from a brief numerical illustration showing how the subsidy reduces relationship value.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on the paper. We address each major comment in turn below.

read point-by-point responses

-

Referee: The non-pledgeability of contingent transfers is stated as a primitive (abstract and model-setup section) rather than derived from verifiability, limited commitment, or the type space. Because this cost differential is load-bearing for the claim that outside exposure must be preserved, an endogenous derivation or a robustness check that relaxes the assumption would be required to support the central result.

Authors: We acknowledge that non-pledgeability is introduced as a modeling primitive. This choice isolates the screening mechanism without requiring an auxiliary enforcement or verifiability layer that would complicate the analysis. An endogenous derivation from first principles would necessitate specifying a detailed information structure or limited-commitment technology, which we view as orthogonal to the paper's focus on the liquidity-screening trade-off. To address the concern, we will add a dedicated robustness subsection that varies the cost differential between pledgeable and non-pledgeable transfers and confirms that the qualitative results (including the preservation of outside exposure) hold for any strictly positive differential. We will also include a short discussion of standard microfoundations for the assumption in the model-setup section. revision: partial

-

Referee: The claim that two sufficient statistics fully pin down the optimal advance share is presented without an explicit derivation or statement of the statistics themselves. Without the relevant proposition or appendix, it is impossible to verify whether the characterization is parameter-free or relies on normalizations that could affect the screening trade-off.

Authors: We apologize for the lack of explicitness in the current draft. In the revision we will insert a formal proposition in the optimal-contract section that states the two sufficient statistics and derives the optimal advance share as a function of them. The full proof will be moved to the appendix (or a new appendix subsection) so that readers can directly verify the characterization and confirm that it depends only on the maintained primitives rather than on auxiliary normalizations. revision: yes

Circularity Check

No circularity detected; assumptions stated as primitives without self-referential reduction

full rationale

The provided abstract states non-pledgeability of contingent transfers directly as a premise ('because they are not pledgeable, impose financing costs') and describes the optimal contract preserving outside-finance exposure, but contains no equations or derivation steps. Without the full manuscript's specific equations, sections, or self-citations, no load-bearing step can be shown to reduce by construction to its own inputs or to a self-citation chain. The model is therefore treated as self-contained against external benchmarks, with the two sufficient statistics and screening logic presented as following from the stated assumptions rather than being forced by definition or fit.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The optimal contract equates the marginal liquidity benefit of the advance with the marginal information cost of the resulting contract flattening... Φℓ(K−a∗;R) = ∂/∂a E[b∗1 μ′(θ)(1−F)/f | q=1]

-

IndisputableMonolith/Foundation/AbsoluteFloorClosure.leanabsolute_floor_iff_bare_distinguishability unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

Assumption [NP] (Non-pledgeability) The contingent transfer T(x) cannot be pledged to outside lenders at date 0.

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

The network origins of aggregate fluctuations

Acemoglu, D., V.\ M.\ Carvalho, A.\ Ozdaglar, and A.\ Tahbaz-Salehi (2012). The network origins of aggregate fluctuations. Econometrica, 80(5), 1977--2016

2012

-

[2]

Trade credit and industry dynamics: Evidence from trucking firms

Barrot, J.-N.\ (2016). Trade credit and industry dynamics: Evidence from trucking firms. Journal of Finance, 71(5), 1975--2016

2016

-

[3]

Dynamic security design: Convergence to continuous time and asset pricing implications

Biais, B., T.\ Mariotti, G.\ Plantin, and J.-C.\ Rochet (2007). Dynamic security design: Convergence to continuous time and asset pricing implications. Review of Economic Studies, 74(2), 345--390

2007

-

[4]

A theory of predation based on agency problems in financial contracting

Bolton, P.\ and D.\ S.\ Scharfstein (1990). A theory of predation based on agency problems in financial contracting. American Economic Review, 80(1), 93--106

1990

-

[5]

In-kind finance: A theory of trade credit

Burkart, M.\ and T.\ Ellingsen (2004). In-kind finance: A theory of trade credit. American Economic Review, 94(3), 569--590

2004

-

[6]

Standard auctions with financially constrained bidders

Che, Y.-K.\ and I.\ Gale (1998). Standard auctions with financially constrained bidders. Review of Economic Studies, 65(1), 1--21

1998

-

[7]

Sufficient statistics for welfare analysis: A bridge between structural and reduced-form methods

Chetty, R.\ (2009). Sufficient statistics for welfare analysis: A bridge between structural and reduced-form methods. Annual Review of Economics, 1(1), 451--488

2009

-

[8]

Trade credit: Suppliers as debt collectors and insurance providers

Cu\ n at, V.\ (2007). Trade credit: Suppliers as debt collectors and insurance providers. Review of Financial Studies, 20(2), 491--527

2007

-

[9]

The pooling and tranching of securities: A model of informed intermediation

DeMarzo, P.\ M.\ (2005). The pooling and tranching of securities: A model of informed intermediation. Review of Financial Studies, 18(1), 1--35

2005

-

[10]

A liquidity-based model of security design

DeMarzo, P.\ M.\ and D.\ Duffie (1999). A liquidity-based model of security design. Econometrica, 67(1), 65--99

1999

-

[11]

Optimal long-term financial contracting

DeMarzo, P.\ M.\ and M.\ J.\ Fishman (2007). Optimal long-term financial contracting. Review of Financial Studies, 20(6), 2079--2128

2007

-

[12]

Bidding with securities: Auctions and security design

DeMarzo, P.\ M., I.\ Kremer, and A.\ Skrzypacz (2005). Bidding with securities: Auctions and security design. American Economic Review, 95(4), 936--959

2005

-

[13]

Internal versus external capital markets

Gertner, R.\ H., D.\ S.\ Scharfstein, and J.\ C.\ Stein (1994). Internal versus external capital markets. Quarterly Journal of Economics, 109(4), 1211--1230

1994

-

[14]

What you sell is what you lend? Explaining trade credit contracts

Giannetti, M., M.\ Burkart, and T.\ Ellingsen (2011). What you sell is what you lend? Explaining trade credit contracts. Review of Financial Studies, 24(4), 1261--1298

2011

-

[15]

Financial intermediation, loanable funds, and the real sector

Holmstr\" o m, B.\ and J.\ Tirole (1997). Financial intermediation, loanable funds, and the real sector. Quarterly Journal of Economics, 112(3), 663--691

1997

-

[16]

Incentives in internal capital markets: Capital constraints, competition, and investment opportunities

Inderst, R.\ and C.\ Laux (2005). Incentives in internal capital markets: Capital constraints, competition, and investment opportunities. RAND Journal of Economics, 36(1), 215--228

2005

-

[17]

Limited liability and incentive contracting with ex-ante action choices

Innes, R.\ D.\ (1990). Limited liability and incentive contracting with ex-ante action choices. Journal of Economic Theory, 52(1), 45--67

1990

-

[18]

Financial contracting theory meets the real world: An empirical analysis of venture capital contracts

Kaplan, S.\ N.\ and P.\ Str\" o mberg (2003). Financial contracting theory meets the real world: An empirical analysis of venture capital contracts. Review of Economic Studies, 70(2), 281--315

2003

-

[19]

The role of factoring for financing small and medium enterprises

Klapper, L.\ (2006). The role of factoring for financing small and medium enterprises. Journal of Banking and Finance, 30(11), 3111--3130

2006

-

[20]

Trade credit contracts

Klapper, L., L.\ Laeven, and R.\ Rajan (2012). Trade credit contracts. Review of Financial Studies, 25(3), 838--867

2012

-

[21]

Mechanism design with financially constrained agents and costly verification

Li, Y.\ (2021). Mechanism design with financially constrained agents and costly verification. Theoretical Economics, 16(3), 1139--1194

2021

-

[22]

Using cost observation to regulate firms

Laffont, J.-J.\ and J.\ Tirole (1986). Using cost observation to regulate firms. Journal of Political Economy, 94(3), 614--641

1986

-

[23]

Optimal equity auctions with heterogeneous bidders

Liu, T.\ (2016). Optimal equity auctions with heterogeneous bidders. Journal of Economic Theory, 166, 94--123

2016

-

[24]

Optimal equity auctions with two-dimensional types

Liu, T.\ and D.\ Bernhardt (2019). Optimal equity auctions with two-dimensional types. Journal of Economic Theory, 184, 104913

2019

-

[25]

Multidimensional mechanism design: Revenue maximization and the multiple-good monopoly

Manelli, A.\ M.\ and D.\ R.\ Vincent (2007). Multidimensional mechanism design: Revenue maximization and the multiple-good monopoly. Journal of Economic Theory, 137(1), 153--185

2007

-

[26]

Envelope theorems for arbitrary choice sets

Milgrom, P.\ and I.\ Segal (2002). Envelope theorems for arbitrary choice sets. Econometrica, 70(2), 583--601

2002

-

[27]

Monopoly and product quality

Mussa, M.\ and S.\ Rosen (1978). Monopoly and product quality. Journal of Economic Theory, 18(2), 301--317

1978

-

[28]

Corporate financing and investment decisions when firms have information that investors do not have

Myers, S.\ C.\ and N.\ S.\ Majluf (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187--221

1984

-

[29]

Optimal auction design

Myerson, R.\ B.\ (1981). Optimal auction design. Mathematics of Operations Research, 6(1), 58--73

1981

-

[30]

Optimal design of securities under asymmetric information

Nachman, D.\ C.\ and T.\ H.\ Noe (1994). Optimal design of securities under asymmetric information. Review of Financial Studies, 7(1), 1--44

1994

-

[31]

Evidence on the determinants of credit terms used in interfirm trade

Ng, C.\ K., J.\ K.\ Smith, and R.\ L.\ Smith (1999). Evidence on the determinants of credit terms used in interfirm trade. Journal of Finance, 54(3), 1109--1129

1999

-

[32]

Trade credit: Theories and evidence

Petersen, M.\ A.\ and R.\ G.\ Rajan (1997). Trade credit: Theories and evidence. Review of Financial Studies, 10(3), 661--691

1997

-

[33]

The dark side of internal capital markets: Divisional rent-seeking and inefficient investment

Scharfstein, D.\ S.\ and J.\ C.\ Stein (2000). The dark side of internal capital markets: Divisional rent-seeking and inefficient investment. Journal of Finance, 55(6), 2537--2564

2000

-

[34]

Internal capital markets and the competition for corporate resources

Stein, J.\ C.\ (1997). Internal capital markets and the competition for corporate resources. Journal of Finance, 52(1), 111--133

1997

-

[35]

Credit rationing in markets with imperfect information

Stiglitz, J.\ E.\ and A.\ Weiss (1981). Credit rationing in markets with imperfect information. American Economic Review, 71(3), 393--410

1981

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.