Recognition: unknown

Market Composition and the Consumer Surplus-Profit Frontier in Monopoly Screening

Pith reviewed 2026-05-10 16:48 UTC · model grok-4.3

The pith

Varying the distribution of buyer valuations traces the entire Pareto frontier between consumer surplus and monopoly profit.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We characterize the consumer surplus-profit frontier across market compositions: as the weight on consumer surplus varies, the payoff pair induced by the optimal market composition traces the Pareto frontier. If profit receives at least as much weight as consumer surplus, the optimal market composition collapses to the top type. Otherwise, it exhibits no exclusion, no interior bunching, and a positive mass at the highest valuation. Under a mild curvature condition, the optimal market composition is unique. Greater weight on consumer surplus makes the market less top-heavy: the differentiated interior expands and the premium top segment shrinks.

What carries the argument

The market composition, i.e., the distribution of buyer valuations chosen upstream before the monopolist applies its optimal screening menu.

If this is right

- When profit is weighted at least as heavily as consumer surplus, the optimal market composition reduces to a single atom at the highest valuation.

- When consumer surplus receives more weight, the composition serves all types with no interior bunching and positive mass at the top.

- Increasing the weight on consumer surplus expands the differentiated interior segment and shrinks the premium top segment.

- Under the mild curvature condition the optimal composition is unique for each weighting.

Where Pith is reading between the lines

- Policymakers could achieve desired surplus-profit trade-offs by regulating buyer entry or information rather than directly controlling seller menus.

- The same composition logic may apply when intermediaries curate participant pools before downstream optimization occurs.

- The results suggest testing whether similar frontier-tracing properties hold when multiple sellers compete after the composition choice.

Load-bearing premise

The upstream actor can freely select any distribution of buyer valuations, and a mild curvature condition on that distribution ensures uniqueness of the optimum.

What would settle it

For a weighting that favors profit, observe whether the optimal distribution places mass only at the highest type; any spread to lower types, or any exclusion or interior bunching when consumer surplus is favored, would falsify the characterization.

Figures

read the original abstract

Economic institutions often influence market outcomes not by directly controlling sellers' menus, but by shaping the market composition sellers face. We study the welfare effects of this upstream choice in a monopoly screening model. An upstream actor chooses the distribution of buyer valuations, after which a monopolist screens optimally. We characterize the consumer surplus-profit frontier across market compositions: as the weight on consumer surplus varies, the payoff pair induced by the optimal market composition traces the Pareto frontier. If profit receives at least as much weight as consumer surplus, the optimal market composition collapses to the top type. Otherwise, it exhibits no exclusion, no interior bunching, and a positive mass at the highest valuation. Under a mild curvature condition, the optimal market composition is unique. Greater weight on consumer surplus makes the market less top-heavy: the differentiated interior expands and the premium top segment shrinks.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper examines an upstream design problem in a standard monopoly screening model with quasilinear preferences and single-dimensional types. An upstream actor selects the distribution of buyer valuations (the market composition), after which the monopolist solves its optimal screening problem. The central claim is that the consumer surplus-profit pairs induced by the optimal market compositions, as the relative weight on consumer surplus varies, trace the Pareto frontier of the feasible payoff set. When the weight on profit is at least as large as the weight on consumer surplus, the optimal composition is a singleton at the highest type. When consumer surplus receives positive weight, the optimal composition features no exclusion, no interior bunching, and a positive atom at the highest valuation. A mild curvature condition on the valuation distribution ensures uniqueness of the optimum. Greater weight on consumer surplus expands the differentiated interior segment and shrinks the top premium segment.

Significance. If the derivations hold, the paper delivers a clean, first-principles characterization of how freely choosing the type distribution allows the designer to achieve any point on the welfare frontier in a screening environment. This is a useful contribution to the market-design and mechanism-design literatures, as it shows that upstream composition choice can substitute for direct menu regulation. The results are derived without fitted parameters or self-referential equations, and the qualitative properties (collapse to top type, no exclusion or interior bunching) are consistent with virtual-value maximization once the designer controls the support and atoms. The explicit description of how the market becomes less top-heavy with higher consumer-surplus weight is a concrete, falsifiable prediction.

minor comments (3)

- [Main characterization result] The curvature condition is invoked only for uniqueness; the main text should state explicitly whether the qualitative properties (no exclusion, no interior bunching, atom at the top) continue to hold without it, or provide a counter-example when the condition fails.

- [Section 3] The proof that the induced payoffs trace the entire Pareto frontier (rather than a subset) should be highlighted with a short argument or reference to the convexity of the feasible set; this is load-bearing for the welfare interpretation but appears only sketched in the abstract.

- [Model and notation] Notation for the welfare weight (e.g., λ for the relative weight on consumer surplus) should be introduced once in the model section and used consistently; current usage mixes verbal descriptions with symbols in the results.

Simulated Author's Rebuttal

We thank the referee for the positive and accurate report. The referee's summary correctly captures the paper's central results on the consumer surplus-profit frontier under upstream market composition choice, and we appreciate the assessment that the characterization is clean and contributes to the market-design and mechanism-design literatures by showing how composition choice can substitute for direct menu regulation. We are pleased that the qualitative predictions are viewed as falsifiable and consistent with virtual-value maximization.

Circularity Check

No significant circularity detected

full rationale

The paper's core characterization follows from direct optimization over market compositions in a standard monopoly screening setup with quasilinear preferences and single-dimensional types. The statement that weighted-optimal compositions trace the Pareto frontier of achievable (consumer surplus, profit) pairs is a direct consequence of the feasible-set definition under the upstream choice of distribution, not a reduction of one equation to another by construction. Qualitative properties such as collapse to the top type when profit weight dominates, absence of exclusion or interior bunching when consumer-surplus weight is positive, and positive mass at the highest valuation are obtained from virtual-value maximization once the designer can select any distribution (including atoms); the mild curvature condition is invoked only for uniqueness and does not underpin the main claims. No self-citations, fitted parameters renamed as predictions, or ansatzes imported from prior work appear in the derivation chain.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Buyers have single-dimensional private valuations drawn from a distribution chosen upstream; utilities are quasilinear; seller has zero marginal cost.

- domain assumption The upstream actor can select any probability distribution over buyer valuations before the monopolist optimizes.

Reference graph

Works this paper leans on

-

[1]

Finally, we have: Lemma 14.Fixk>1/2, and suppose Assumption 2 holds

This proves uniqueness of the optimal virtual value profile. Finally, we have: Lemma 14.Fixk>1/2, and suppose Assumption 2 holds. Letϕ ∗ ∈Φbe the unique maximizer of maxϕ∈Φ Jk(ϕ). ThenG ϕ∗ is the unique maximizer of the original problemmax G∈∆([0,1]) Wk(G). Proof.By Lemmas 1 and 2,G ϕ∗ is an optimizer of the original problem. We prove uniqueness. LetG∈∆([...

2015

-

[2]

Then Ge ⪰st G,G e ⪰icx G,W k(Ge)−C(G e)≥W k(G)−C(G)

LetG∈∆([0, 1]), and letG e be the regularized distribution from Lemma 1, with quantile Qe(u) = R(u) 1−u ,u∈[0, 1). Then Ge ⪰st G,G e ⪰icx G,W k(Ge)−C(G e)≥W k(G)−C(G)

-

[3]

Then G+ ⪰st G,G + ⪰icx G,W k(G+)−C(G +)≥W k(G)−C(G)

LetG∈Ωhave ironed virtual valueϕ, and letG + be the truncation from Lemma 2. Then G+ ⪰st G,G + ⪰icx G,W k(G+)−C(G +)≥W k(G)−C(G). Consequently, sup G∈∆([0,1]) {Wk(G)−C(G)}=sup ϕ∈Φ ˆJk(ϕ). Proof.For part (i), Lemma 1 givesW k(Ge)≥W k(G). Moreover, by construction ofG e, Qe(u) = R(u) 1−u ≥Q(u)∀u∈[0, 1), 67 becauseRmajorizes the raw revenue curve ofG. IfU∼Un...

2022

-

[4]

¯q(v) =0for allv<Q(0)

-

[5]

¯qis constant on every connected component of(Q(0), 1)\supp(G)

-

[6]

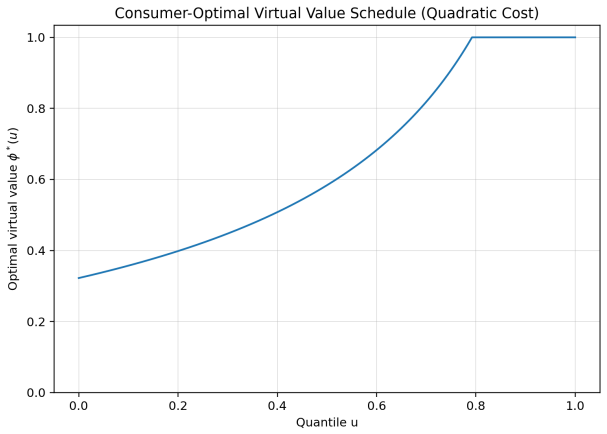

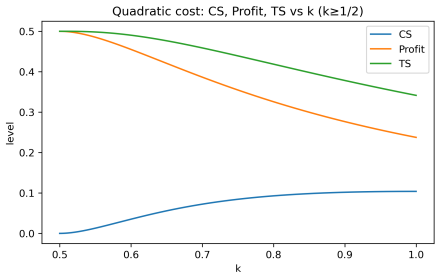

Supported Material for the Quadratic Cost Example

¯q(v) = ˜q(v)for everyv∈supp(G); 4.Π( ¯q, ¯t;G)≥Π( ˜q, ˜t;G)andTS( ¯q, ¯t;G) =TS( ˜q, ˜t;G). Consequently, in solving the seller’s problem it is without loss to restrict attention to mechanisms whose allocation rule is zero below the lower support point and constant on each support gap. Proof.By Fact 2, we may normalizeU(v ) =0. Letv 0 :=Q(0) =inf supp(G)...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.