Recognition: no theorem link

Timing, Entry, and Revenue in Clock-Based Platform Markets

Pith reviewed 2026-05-15 06:12 UTC · model grok-4.3

The pith

In platform markets with waiting costs, the descending clock dominates posted prices only in specific regions defined by earnings and timing gaps on each side.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

When time-to-contract is payoff-relevant and entry responds to waiting costs, the descending clock's ranking against posted-price benchmarks is settled by side-specific earnings gaps and timing gaps, producing a bidirectional four-case dominance classification; the clock cannot win unconditionally if it charges no more per trade and contracts no faster than the benchmark.

What carries the argument

The bidirectional four-case classification that maps earnings gap and timing gap primitives into dominance regions for the descending clock versus posted-price formats.

If this is right

- When the clock holds a local advantage, endogenous entry increases market thickness and platform revenue on that side.

- Cross-side complementarity converts a one-sided edge into joint dominance for the platform.

- No single format ranks highest for all combinations of waiting costs and gaps.

- Revenue gains from better format choice can be quantified by converting entry and volume effects via a conditional revenue theorem.

- The switching boundary in calibrated models lies near p0 over average value of one, matching empirical ride-hailing ranges.

Where Pith is reading between the lines

- Platforms could estimate the six reduced-form objects nonparametrically to decide between clock and posted-price mechanisms in practice.

- If waiting costs were zero or entry fixed, the classification would collapse and revenue equivalence would hold.

- The approach suggests examining how dispatch speed affects matching in on-demand labor markets beyond ride-hailing.

Load-bearing premise

Both sides of the market have endogenous participation that responds to the waiting costs created by the trading format.

What would settle it

Finding a market where the descending clock charges no higher per trade and contracts no faster than posted prices yet still attracts more entry or higher platform revenue.

Figures

read the original abstract

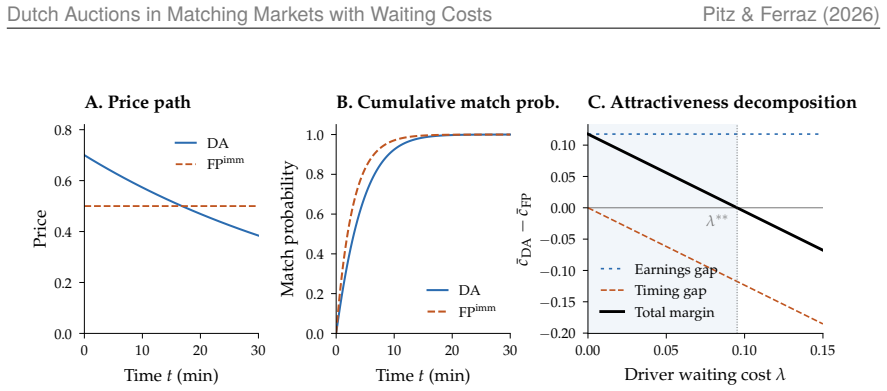

On platforms where time-to-contract is itself payoff-relevant--Aalsmeer's flower auctions, ride-hailing dispatch, on-demand-labor matching--the textbook revenue equivalence between Dutch and first-price formats holds the trading outcome fixed. Once participation is endogenous and both sides bear waiting costs, the trading format directly shapes who enters, market thickness, volume, and platform revenue. The platform's ranking of the descending clock against immediate and batched posted-price benchmarks is decided by two estimable primitives on each side of the market: an earnings gap and a timing gap. A bidirectional four-case classification identifies when the descending clock dominates at every level of waiting costs, only above a floor, only below a ceiling, or not at all; the last case is unconditional -- when the descending clock charges no more per trade and contracts no faster than the posted-price benchmark, it cannot win. No format admits a universal ranking. The local verdict propagates through endogenous entry, and cross-side complementarity amplifies shared local advantages into joint dominance. A conditional revenue theorem converts entry and volume gains into a platform-revenue ranking. In calibrated parameterizations the revenue-ranking switching boundary lies near $p_0/\bar v\approx 1$, inside the empirical range for ride-hailing platforms. A measurement protocol provides explicit nonparametric estimators for the six reduced-form objects and a test statistic for the dominance condition, and a Lean~4 formalization audits the algebraic and order-theoretic content. In markets where goods or services cannot wait, the speed of the trading mechanism is a primitive of market design.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models platform markets (e.g., ride-hailing, flower auctions) in which time-to-contract is payoff-relevant. With endogenous entry on both sides and format-dependent waiting costs, the ranking of a descending clock versus posted-price benchmarks is governed by two estimable primitives per side—an earnings gap and a timing gap—yielding a bidirectional four-case classification of dominance regions. An unconditional result states that the clock cannot dominate when it charges no more per trade and contracts no faster. The framework supplies a conditional revenue theorem, calibrated illustrations with a switching boundary near p0/v̄ ≈ 1, a nonparametric measurement protocol for the six reduced-form objects, and a Lean 4 formalization of the algebraic and order-theoretic content.

Significance. If the classification and revenue theorem hold, the paper supplies a useful, estimable framework for platform design in time-sensitive markets. The combination of endogenous-entry propagation, cross-side complementarity, a nonparametric measurement protocol, and machine-checked formalization constitutes a clear methodological contribution that could support both theoretical extensions and empirical tests.

major comments (2)

- [Equilibrium construction and four-case classification] The unconditional dominance result (descending clock cannot win when it charges no more and contracts no faster) is load-bearing for the four-case partition. The manuscript should supply the explicit equilibrium construction showing how this follows directly from the primitives without post-hoc restrictions on the waiting-cost distributions or entry functions.

- [Conditional revenue theorem] The conditional revenue theorem converts entry/volume gains into a platform-revenue ranking. The derivation relies on the interaction of the timing gap with cross-side complementarity; the manuscript should verify that the revenue ordering remains valid under the general (nonparametric) waiting-cost distributions used elsewhere rather than under auxiliary functional-form assumptions.

minor comments (3)

- [Measurement protocol] The abstract states that the measurement protocol supplies estimators for six reduced-form objects; the main text should list these objects explicitly with their nonparametric estimators and the associated test statistic for the dominance condition.

- [Calibrated parameterizations] In the calibrated parameterizations, the revenue-ranking switching boundary is reported near p0/v̄ ≈ 1. The text should clarify the exact functional forms and parameter values used for the waiting-cost distributions and entry costs in these illustrations.

- [Formalization] The Lean 4 formalization is a strength; the manuscript should include a short appendix or footnote mapping the formalized statements to the numbered propositions or theorems in the main text.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on the equilibrium construction and revenue theorem. We address each major comment below and will revise the manuscript to incorporate the requested clarifications.

read point-by-point responses

-

Referee: [Equilibrium construction and four-case classification] The unconditional dominance result (descending clock cannot win when it charges no more and contracts no faster) is load-bearing for the four-case partition. The manuscript should supply the explicit equilibrium construction showing how this follows directly from the primitives without post-hoc restrictions on the waiting-cost distributions or entry functions.

Authors: The equilibrium construction proceeds directly from the primitives (earnings gap, timing gap, general waiting-cost distributions, and entry functions) via threshold strategies on each side, with market clearing determining volumes. The unconditional dominance result follows immediately because, when the clock charges no more per trade and contracts no faster, the participation thresholds and resulting volumes are weakly lower than under posted prices for any waiting-cost distribution, implying weakly lower platform revenue. To make this fully explicit, the revised manuscript will add a dedicated subsection in Section 3 that derives the equilibrium strategies and the dominance result step-by-step from the primitives, without any auxiliary restrictions. This will be cross-referenced to the existing Lean 4 formalization of the order-theoretic content. revision: yes

-

Referee: [Conditional revenue theorem] The conditional revenue theorem converts entry/volume gains into a platform-revenue ranking. The derivation relies on the interaction of the timing gap with cross-side complementarity; the manuscript should verify that the revenue ordering remains valid under the general (nonparametric) waiting-cost distributions used elsewhere rather than under auxiliary functional-form assumptions.

Authors: The conditional revenue theorem is already derived under the general nonparametric waiting-cost distributions; the proof uses only monotonicity of entry with respect to the timing gap and cross-side complementarity, without imposing specific functional forms. The revenue ordering is preserved because volume gains from faster contracting translate directly into revenue gains via the earnings gap, independently of the shape of the waiting-cost distributions. To address the request explicitly, the revised version will add an appendix that re-derives the revenue ranking for arbitrary continuous waiting-cost distributions, confirming that the result holds distribution-free. revision: yes

Circularity Check

No significant circularity: derivation self-contained from primitives

full rationale

The central classification and unconditional dominance result are derived directly from the model's primitives (earnings gap and timing gap on each side) under endogenous participation and format-dependent waiting costs. These gaps are treated as estimable reduced-form objects with an explicit nonparametric measurement protocol; calibrations are presented only as illustrations, not as fitted predictions that define or force the ranking. The conditional revenue theorem follows algebraically from entry and volume propagation via cross-side complementarity. The Lean~4 formalization supplies independent machine-checked verification of the order-theoretic content, and no load-bearing step reduces to a self-citation, ansatz smuggled via prior work, or renaming of a known result. The framework is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Agents have quasi-linear preferences and rationally anticipate equilibrium payoffs when deciding entry.

- domain assumption Waiting costs are linear in time and borne symmetrically by both sides.

Reference graph

Works this paper leans on

-

[1]

doi: 10.1287/mnsc.2022.00096. Guillaume R. Fréchette, Alessandro Lizzeri, and Tobias Salz. Frictions and the city: Evidence from taxi rides.American Economic Review, 109(6):2170–2213, 2019. doi: 10.1257/aer.20160478. Barbara Petrongolo and Christopher A. Pissarides. Looking into the black box: A survey of the matching function.Journal of Economic Literatu...

-

[2]

doi: 10.1016/j.ecotra.2012.09.002. Gerard J. van den Berg, Jan C. van Ours, and Menno P. Pradhan. The declining price anomaly in Dutch rose auctions.American Economic Review, 91(4):1055–1062, 2001. doi: 10.1257/aer.91.4.1055. 25

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.