Recognition: unknown

A Counterfactual Diagnostic Framework for Explaining KS Deterioration in Credit Risk Model Validation

Pith reviewed 2026-05-10 14:56 UTC · model grok-4.3

The pith

A counterfactual framework sequentially attributes declines in the KS statistic to sampling variability, portfolio changes, covariate shifts, or model drift.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

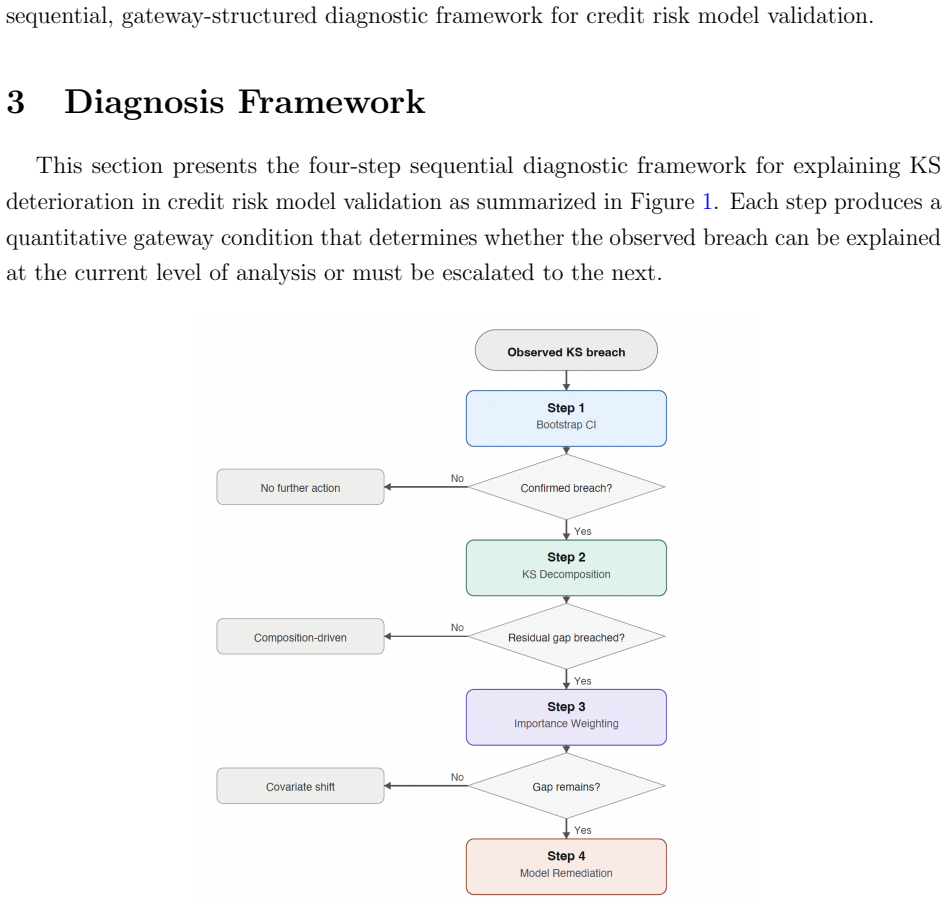

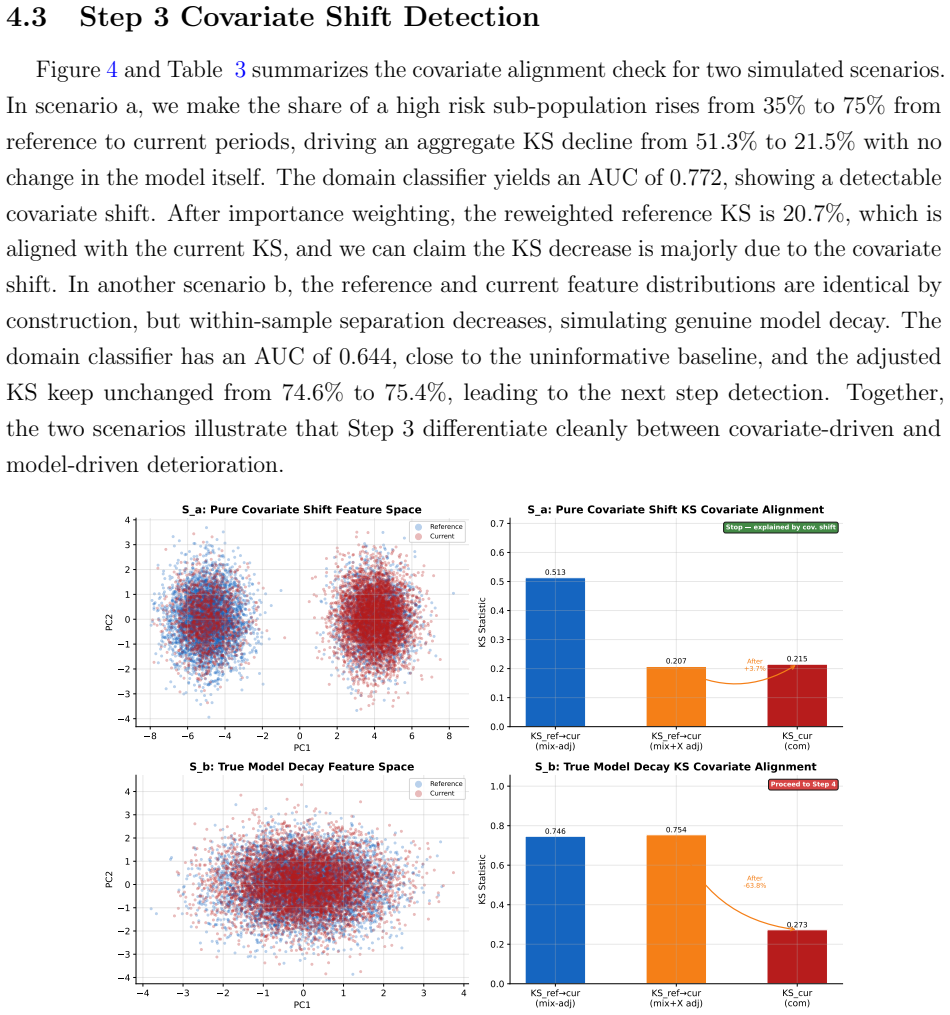

The framework uses sequential counterfactual attribution with gateway conditions to decompose an observed decline in the KS statistic into contributions from sampling variability, portfolio composition change, covariate shift, and residual deterioration consistent with model drift. Simulation results indicate that this yields more interpretable and governance-relevant explanations than relying solely on threshold breaches.

What carries the argument

The sequential decomposition process with explicit gateway conditions that escalates analysis from sampling variability through portfolio composition and covariate shift to residual model drift.

Load-bearing premise

The four potential causes of KS decline can be separated into distinct, non-overlapping categories using the sequential checks and gateway conditions.

What would settle it

Observing a case where the framework attributes the KS decline to model drift, but subsequent analysis shows it was actually due to an unaccounted covariate shift or portfolio change.

Figures

read the original abstract

The Kolmogorov-Smirnov (KS) statistic is widely used in credit risk model monitoring and validation to assess discriminatory power. In practice, a material decline in KS often triggers governance review and requires validation teams to identify the breach source and the potential business risk. However, such diagnosis is frequently conducted on an ad hoc basis, relying on the judgment of individual validators rather than a standardized analytical framework. This paper proposes a counterfactual diagnostic framework for explaining KS deterioration in credit risk model validation. The framework sequentially attributes observed KS decline to sampling variability, portfolio composition change, covariate shift, and residual deterioration consistent with model drift, with explicit gateway conditions governing escalation at each stage. Simulation experiments demonstrate that the proposed approach provides more interpretable and governance-relevant explanations than threshold-based review alone, and contributes to more consistent, transparent, and defensible performance-breach assessment in credit risk model validation.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a counterfactual diagnostic framework for explaining declines in the Kolmogorov-Smirnov (KS) statistic in credit risk model validation. It sequentially attributes the observed KS deterioration to sampling variability, portfolio composition change, covariate shift, and residual model drift using explicit gateway conditions for escalation. Simulation experiments are presented to demonstrate that this approach yields more interpretable and governance-relevant explanations than threshold-based review alone.

Significance. If the proposed decomposition can be shown to reliably isolate the contributing factors without significant confounding, the framework would address a practical need for standardized, transparent diagnosis of performance breaches in credit risk models. This could enhance consistency in validation processes. The emphasis on counterfactuals and simulations is a methodological strength that aligns with efforts to make model monitoring more rigorous.

major comments (2)

- Abstract: The abstract asserts that simulation experiments support the framework but supplies no details on experimental design, data generation, statistical tests, or sensitivity checks. This is load-bearing for the central claim that the approach provides more interpretable explanations, as it prevents assessment of whether attribution remains stable under joint perturbations of the factors.

- Sequential decomposition with gateway conditions: The central claim rests on the assumption that these conditions cleanly isolate sampling variability, portfolio composition change, covariate shift, and residual drift as distinct, non-overlapping contributors. However, composition shifts typically alter the joint distribution of covariates and interact with sampling noise. Without explicit identifiability conditions or bounds demonstrating that the chosen counterfactuals remove confounding, the residual category may absorb misattributed effects rather than isolate true model drift.

Simulated Author's Rebuttal

We thank the referee for their constructive and insightful comments, which highlight important aspects of clarity and methodological rigor in our proposed framework. We address each major comment below and outline the revisions we will make to the manuscript.

read point-by-point responses

-

Referee: Abstract: The abstract asserts that simulation experiments support the framework but supplies no details on experimental design, data generation, statistical tests, or sensitivity checks. This is load-bearing for the central claim that the approach provides more interpretable explanations, as it prevents assessment of whether attribution remains stable under joint perturbations of the factors.

Authors: We agree that the abstract should provide sufficient information to allow readers to evaluate the simulation-based support for the framework. In the revised manuscript, we will expand the abstract to include a concise description of the experimental design, including the data generation process (e.g., controlled perturbations of sampling, portfolio composition, and covariate distributions), the statistical tests employed for gateway conditions, and key sensitivity checks performed. This will strengthen the abstract without exceeding typical length constraints while directly addressing the concern about assessing stability under joint perturbations. revision: yes

-

Referee: Sequential decomposition with gateway conditions: The central claim rests on the assumption that these conditions cleanly isolate sampling variability, portfolio composition change, covariate shift, and residual drift as distinct, non-overlapping contributors. However, composition shifts typically alter the joint distribution of covariates and interact with sampling noise. Without explicit identifiability conditions or bounds demonstrating that the chosen counterfactuals remove confounding, the residual category may absorb misattributed effects rather than isolate true model drift.

Authors: This is a valid methodological concern. The framework employs a sequential structure with explicit gateway conditions (e.g., bootstrap-based tests for sampling variability, reweighting for composition shifts, and distribution matching for covariate shifts) to attribute effects in order and escalate only when prior factors are ruled out. While the design aims to minimize overlap by construction, we acknowledge that complete isolation is challenging in finite samples due to interactions between composition and covariate shifts. In the revision, we will add a dedicated subsection on identifiability assumptions, potential confounding pathways, and empirical bounds derived from the simulation results showing the frequency of correct attribution versus residual absorption. This will clarify the framework's scope and limitations without altering the core sequential logic. revision: yes

Circularity Check

No circularity: proposed diagnostic framework is independent of fitted inputs or self-citations

full rationale

The manuscript proposes a new sequential counterfactual diagnostic procedure for attributing KS statistic declines in credit risk models to four categories (sampling variability, portfolio composition change, covariate shift, residual model drift) under explicit gateway conditions. Attribution and validation occur via simulation experiments that compare interpretability against threshold-based review. No equations, parameter fits, or self-citations appear in the text that would reduce the central claims to re-expressions of the paper's own inputs by construction. The framework is presented as an external analytical tool rather than a renaming or re-derivation of prior results, making the derivation chain self-contained.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption KS statistic decline can be sequentially decomposed into sampling variability, portfolio composition change, covariate shift, and residual model drift without substantial overlap or misattribution.

Reference graph

Works this paper leans on

-

[1]

Oxford university press, 2007

Raymond Anderson.The credit scoring toolkit: theory and practice for retail credit risk management and decision automation. Oxford university press, 2007. Katarzyna Bijak and Lyn C Thomas. Does segmentation always improve model performance in credit scoring?Expert Systems with Applications, 39(3):2433–2442, 2012. Board of Governors of the Federal Reserve ...

2007

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.