Recognition: unknown

Strategic Pricing and Consumer Welfare under One-Sided Price Regulation

Pith reviewed 2026-05-10 04:54 UTC · model grok-4.3

The pith

One-sided price regulation that limits increases to one per day can prompt firms to set higher initial prices, weakly raising expected average prices.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under the one-sided regulation the firm prices strategically high in period one to preserve downward flexibility in period two. This produces weakly higher expected average prices than flexible monopoly pricing each period, with the increase becoming strict when future high demand is sufficiently likely and the demand gap is large; consumer surplus rises when expected prices remain unchanged and falls otherwise.

What carries the argument

Strategic high pricing in period one to retain the option of not raising price again in period two when demand is uncertain.

If this is right

- Expected average prices are at least as high as under flexible pricing and strictly higher when high future demand is sufficiently probable and the high-low gap is large.

- Consumer surplus rises precisely when expected prices stay the same and falls when expected prices strictly increase.

- The regulation leaves expected prices and consumer surplus unchanged when demand conditions do not trigger strategic first-period pricing.

- The welfare effect depends only on whether average prices change, with no separate direct benefit or cost from the regulation itself.

Where Pith is reading between the lines

- Regulators in other daily-priced markets could see similar strategic responses if they impose comparable one-increase limits.

- The size of the price and welfare effects can be calibrated directly from observable demand probabilities and state gaps in the target industry.

- Testing the mechanism requires tracking both initial prices and realized average prices around the policy change rather than average prices alone.

Load-bearing premise

The firm will deliberately set a high first-period price solely to keep the ability to avoid a second increase if low demand occurs, with demand states drawn from a known distribution and no other pricing constraints present.

What would settle it

Observe whether opening prices rise and average prices weakly increase after the regulation takes effect in fuel markets, particularly when high-demand probability and demand gaps match the model's conditions for a strict effect.

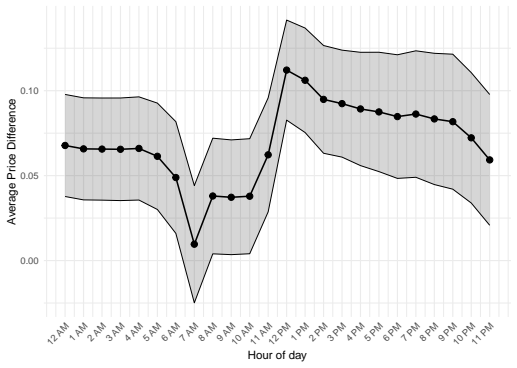

Figures

read the original abstract

Motivated by Germany's April 2026 fuel price regulation, in this note I study a two-period pricing problem with demand uncertainty and a rule that prohibits more than one price increase during the day. Under flexible pricing, the firm chooses the static monopoly price in each period. Under the regulation, by contrast, it may price strategically high in period 1 to preserve flexibility in period 2. I show that the regulation weakly raises expected average prices. The increase is strict when future high demand is sufficiently likely and the gap between high and low demand is large; otherwise, expected average prices are unchanged. Consumer surplus rises when expected prices do not, and decreases otherwise.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies a two-period monopoly pricing model with demand uncertainty (high or low state) under a one-sided regulation that prohibits more than one price increase per day. Under flexible pricing the firm sets the static monopoly price each period independently. Under the regulation the firm may set a high price in period 1 to retain the option to decrease in period 2 if low demand realizes. The central claim is that expected average prices are weakly higher under the regulation; the increase is strict when the probability of high demand is sufficiently large and the demand gap is large; otherwise prices are unchanged. Consumer surplus moves inversely with the price effect.

Significance. If the comparative-static result holds, the paper supplies a transparent example of how an asymmetric price-change constraint can induce preemptive high pricing that raises expected prices and can lower consumer surplus. The result is expressed directly in terms of the two free parameters (probability of high demand and size of the demand gap) without auxiliary fitted constants, and the welfare reversal is stated cleanly. This is policy-relevant for real-world one-sided regulations such as the German fuel-price rule cited in the motivation.

major comments (2)

- [main result / abstract claim] The abstract states that the firm 'may price strategically high in period 1 to preserve downward flexibility in period 2' and that this produces a weak (sometimes strict) rise in expected average prices. The manuscript must explicitly derive the firm's optimal period-1 price under the regulation, show the condition on the probability p and gap parameter under which the high price is chosen, and compute the resulting quantity-weighted expected price relative to the two independent static-monopoly prices. Without these steps the strict-increase claim cannot be verified.

- [model setup] The regulation is described as prohibiting 'more than one price increase during the day.' The model must clarify whether downward adjustments are unrestricted and whether an initial price is set before period 1. If the firm can always decrease after an initial low price, the strategic incentive to start high may not bind for all parameter values; the paper should state the precise timing and feasible price paths that make the one-increase limit non-trivial.

minor comments (1)

- The abstract refers to 'expected average prices' without specifying whether the average is quantity-weighted or time-weighted; a short clarifying sentence would remove ambiguity.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive suggestions. The comments identify areas where greater explicitness will strengthen the paper. We address each major comment below and will revise the manuscript to incorporate the requested derivations and clarifications.

read point-by-point responses

-

Referee: [main result / abstract claim] The abstract states that the firm 'may price strategically high in period 1 to preserve downward flexibility in period 2' and that this produces a weak (sometimes strict) rise in expected average prices. The manuscript must explicitly derive the firm's optimal period-1 price under the regulation, show the condition on the probability p and gap parameter under which the high price is chosen, and compute the resulting quantity-weighted expected price relative to the two independent static-monopoly prices. Without these steps the strict-increase claim cannot be verified.

Authors: We agree that the steps underlying the main result should be derived explicitly. In the revised manuscript we will add a new subsection that first states the firm's period-2 problem under each realized demand state. We then derive the firm's optimal period-1 price by comparing expected profits from choosing the high versus low static-monopoly price in period 1, taking into account the subsequent optimal adjustment in period 2. We will state the precise threshold condition on the probability p of high demand and the demand-gap parameter under which the high price is strictly preferred. Finally, we will compute the quantity-weighted expected average price under the regulated strategy and show that it is weakly higher than the flexible-pricing benchmark (the average of the two independent static prices), with the inequality strict precisely when p is sufficiently large and the demand gap is large. These derivations will be presented in full so that the claims can be verified directly. revision: yes

-

Referee: [model setup] The regulation is described as prohibiting 'more than one price increase during the day.' The model must clarify whether downward adjustments are unrestricted and whether an initial price is set before period 1. If the firm can always decrease after an initial low price, the strategic incentive to start high may not bind for all parameter values; the paper should state the precise timing and feasible price paths that make the one-increase limit non-trivial.

Authors: We thank the referee for noting the need for a more precise model description. In the revision we will expand the model-setup section to state the timing explicitly: the firm selects the period-1 price before the demand state is realized; the state is then observed at the start of period 2, after which the firm may adjust the price for period 2. Downward adjustments are unrestricted. The one-sided regulation prohibits any price increase, so the feasible price paths are (high, high), (high, low), and (low, low); the path (low, high) is infeasible. This formulation makes the constraint non-trivial and generates the strategic incentive to begin with the high price precisely when the probability of high demand is large and the demand gap is large, as the firm then values the option to decrease if low demand realizes. We will also note that the wording 'more than one price increase' in the original draft is intended to capture the one-sided nature of the rule and will be revised for clarity. revision: yes

Circularity Check

No significant circularity; derivation is self-contained

full rationale

The paper sets up a two-period monopoly pricing model with binary demand states drawn from a known distribution and a regulatory constraint allowing at most one price increase. It compares the firm's optimal strategy under unconstrained static monopoly pricing each period against the constrained case, where the firm may select a high period-1 price to retain downward flexibility. The claimed weak (or strict) rise in expected average prices and the corresponding consumer-surplus effects are obtained by solving the firm's profit-maximization problem under each regime and comparing the resulting expected values. These comparisons are direct consequences of the model's assumptions and the definition of the regulatory rule; they do not rely on external fitted parameters, self-citations, or any reduction of the conclusion to its own inputs by construction. The parameter regions for strict increase are ordinary comparative-statics statements within the model, not tautologies.

Axiom & Free-Parameter Ledger

free parameters (2)

- probability of high demand

- gap between high and low demand

axioms (2)

- domain assumption Firm is a static monopoly pricer in each period absent the regulatory constraint

- domain assumption Demand states are drawn independently across periods from a known two-point distribution

Reference graph

Works this paper leans on

-

[1]

Measures against high petrol prices , year =

-

[2]

Christoph Siemroth , title =. 2026 , month = mar, note =. 2603.18920 , archivePrefix=

-

[3]

International Journal of Industrial Organization , year =

Martin Obradovits , title =. International Journal of Industrial Organization , year =

-

[4]

The Effects of Gasoline Price Regulations: Experimental Evidence , institution =

Justus Haucap and Hans Christian M. The Effects of Gasoline Price Regulations: Experimental Evidence , institution =. 2012 , number =

2012

-

[5]

Energy Economics , year =

Maike Becker and Gregor Pfeifer and Karsten Schweikert , title =. Energy Economics , year =

-

[6]

International Journal of Industrial Organization , year =

Patrick Andreoli-Versbach and Jens-Uwe Franck , title =. International Journal of Industrial Organization , year =

-

[7]

Noel , title =

Michael D. Noel , title =. The Review of Economics and Statistics , year =

-

[8]

Finance Research Letters , year =

Angerer, Martin , title =. Finance Research Letters , year =

-

[9]

2018 , number =

Fasoula, Evangelia , title =. 2018 , number =

2018

-

[10]

Germany's fuel-price relief has backfired on motorists , year =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.