Recognition: unknown

Bond Market Making with a Hit-Ratio Target

Pith reviewed 2026-05-09 22:50 UTC · model grok-4.3

The pith

Dualizing a hit-ratio target keeps the optimal control problem for bond market making separable and yields explicit quote maps.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

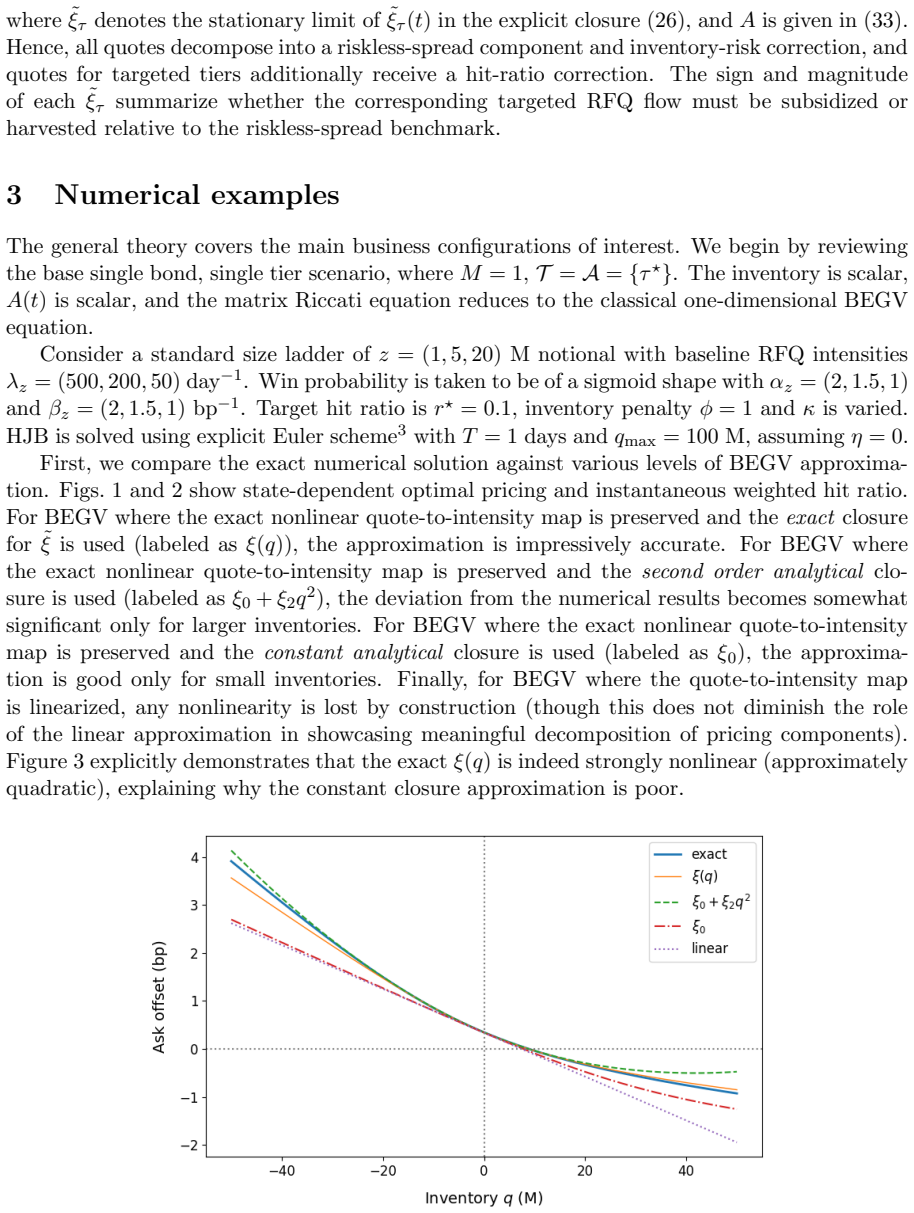

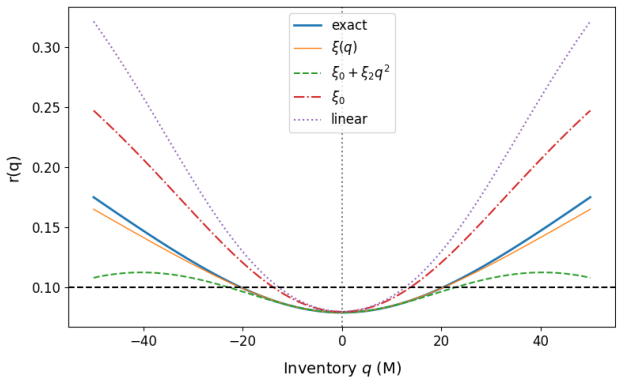

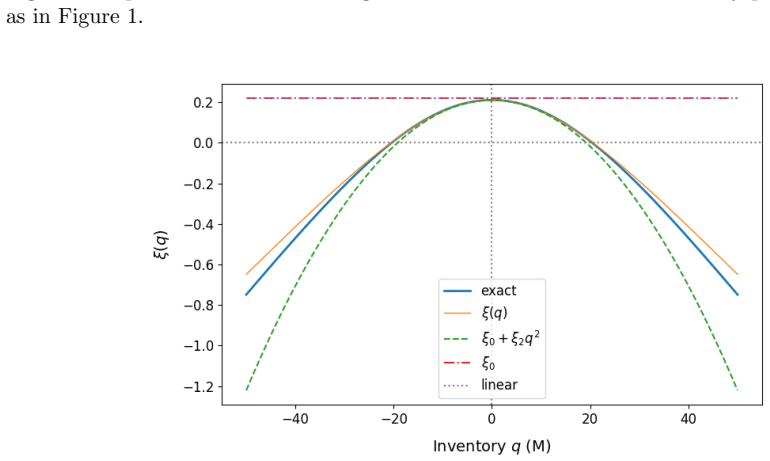

We study OTC bond market making on a size ladder with quadratic inventory penalty and a running target on the dealer's size-weighted hit ratio within a stochastic optimal control approach. We demonstrate that the corresponding reduced Hamilton-Jacobi-Bellman (HJB) equation remains separable by dualizing the hit ratio target term and provides the exact optimal controls through the inverse of the fill-probability function and the Hamiltonian derivative. We then focus on the quadratic approximation which yields a Riccati equation for the inventory curvature while retaining the exact quote map. In its linearized form, this approximation produces explicit quote decompositions into riskless spread

What carries the argument

The dualization of the hit-ratio target term in the reduced HJB equation, which maintains separability and recovers exact controls from the inverse fill-probability function together with the Hamiltonian derivative.

If this is right

- Quotes decompose explicitly into riskless spread, inventory-risk correction, and hit-ratio correction, allowing separate tuning of each component.

- The Riccati solution for inventory curvature supplies usable quote adjustments even when fill probabilities are nonlinear.

- The same separable structure extends immediately to multi-bond and multi-client-tier problems by restricting which targets and coverages are active.

- Linearized controls remain practical for small inventory deviations and can be recomputed quickly as market parameters shift.

Where Pith is reading between the lines

- The decomposition could be used to back out implied risk aversion and target weights from observed dealer quotes in live bond markets.

- The same dualization technique might apply to other running performance metrics such as volume targets or spread-capture goals in OTC control problems.

- Periodic re-solution of the Riccati equation would allow the maps to adapt to changing volatility or liquidity regimes without losing the closed-form quote structure.

Load-bearing premise

That dualizing the hit-ratio target term preserves optimality of the derived controls and that the quadratic inventory approximation remains accurate enough when fill probabilities are nonlinear.

What would settle it

Simulate paths under the derived quotes and check whether the realized size-weighted hit ratio converges to the chosen target while inventory risk stays bounded, then compare to the same simulation run without the dualized target term.

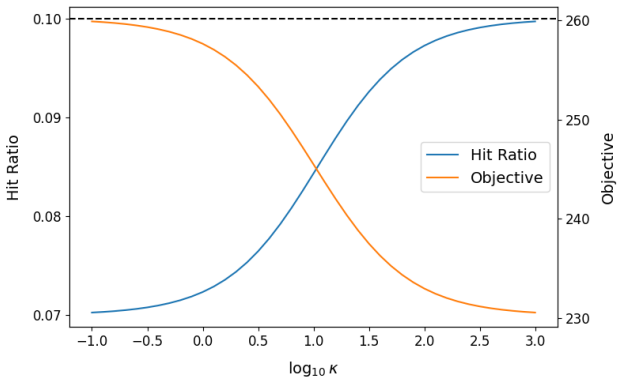

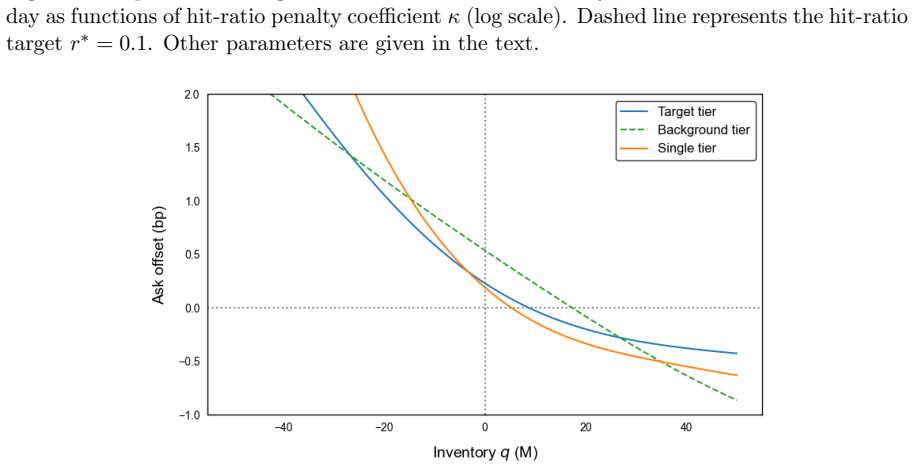

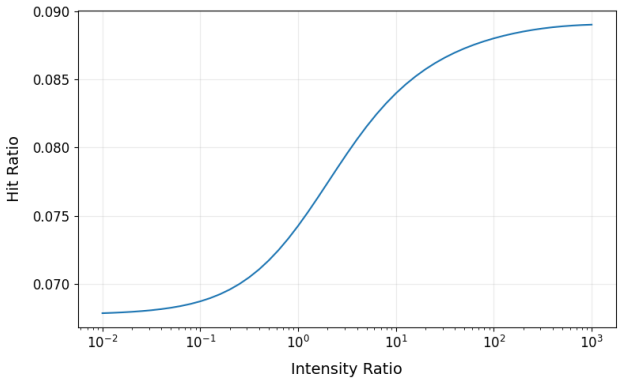

Figures

read the original abstract

We study OTC bond market making on a size ladder with quadratic inventory penalty and a running target on the dealer's size-weighted hit ratio within a stochastic optimal control approach. We demonstrate that the corresponding reduced Hamilton-Jacobi-Bellman (HJB) equation remains separable by dualizing the hit ratio target term and provides the exact optimal controls through the inverse of the fill-probability function and the Hamiltonian derivative. We then focus on the quadratic approximation \'a la Bergault et al., which yields a Riccati equation for the inventory curvature while retaining the exact quote map. In its linearized form, this approximation produces explicit quote decompositions into riskless spread, inventory-risk correction, and hit-ratio correction. The formulation is general and applies to multi-bond, multi-client-tier scenarios, with special cases obtained by restricting the targeted tiers, their bond coverage, and their associated targets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a stochastic optimal control framework for OTC bond market making on a size ladder, incorporating quadratic inventory penalties and a running size-weighted hit-ratio target. It shows that dualizing the hit-ratio target term keeps the reduced HJB equation separable, yielding exact optimal controls via the inverse fill-probability function and the Hamiltonian derivative. A quadratic approximation à la Bergault et al. produces a Riccati equation for inventory curvature while retaining the exact quote map; linearization then gives explicit quote decompositions into riskless spread, inventory-risk correction, and hit-ratio correction. The formulation is general and extends to multi-bond, multi-client-tier scenarios by restricting targeted tiers and bonds.

Significance. If the dualization is rigorously justified, this provides a parameter-light (only hit-ratio target level and inventory risk aversion as free parameters) and tractable extension of existing quadratic market-making models that directly incorporates a practical dealer objective. The explicit controls, Riccati solution, and quote decompositions, together with the multi-asset generality, represent a clear strength for both theoretical and applied work in bond market making. The approach avoids circularity by treating the target as exogenous and builds on standard stochastic-control assumptions without unsupported reductions.

major comments (2)

- [Abstract and §3 (reduced HJB derivation)] The abstract and the derivation of the reduced HJB (presumably §3) assert that dualizing the hit-ratio target term renders the equation separable and supplies exact optimal controls through the inverse fill-probability and Hamiltonian derivative. The manuscript must explicitly introduce the dual variable, derive the optimality conditions, and verify that the resulting controls satisfy the original (non-dualized) HJB without introducing hidden constraints or altering the admissible control set.

- [§4 (quadratic approximation and Riccati equation)] §4 (quadratic approximation): the claim that the quadratic approximation around zero inventory remains accurate enough to produce usable quote maps when fill probabilities are nonlinear is load-bearing for the practical utility of the Riccati solution and linearized decompositions. No error bounds, numerical comparisons against the full nonlinear problem, or sensitivity analysis with respect to the curvature of the fill-probability function are provided.

minor comments (2)

- [§2 (model setup)] The notation for the size ladder, client tiers, and associated hit-ratio targets would be clarified by adding a summary table in §2 listing the relevant parameters, coverage, and target values for each tier.

- [Notation and §3] The Hamiltonian and its derivative appear in the control expressions; a single, early definition of these objects (including any dependence on the dual variable) would improve readability of the exact-control formulas.

Simulated Author's Rebuttal

We thank the referee for the constructive review and the recommendation for minor revision. We address each major comment below and will revise the manuscript accordingly to strengthen the exposition and validation.

read point-by-point responses

-

Referee: [Abstract and §3 (reduced HJB derivation)] The abstract and the derivation of the reduced HJB (presumably §3) assert that dualizing the hit-ratio target term renders the equation separable and supplies exact optimal controls through the inverse of the fill-probability and Hamiltonian derivative. The manuscript must explicitly introduce the dual variable, derive the optimality conditions, and verify that the resulting controls satisfy the original (non-dualized) HJB without introducing hidden constraints or altering the admissible control set.

Authors: We agree that the current derivation in §3 would benefit from greater explicitness regarding the dualization step. In the revised manuscript we will introduce the dual variable λ explicitly at the start of §3, derive the first-order optimality conditions from the dualized HJB, and add a short verification subsection demonstrating that the resulting controls satisfy the original (non-dualized) HJB. The verification will confirm that the dualization is a standard Lagrange-multiplier treatment of the running constraint and does not alter the admissible control set or introduce hidden restrictions. revision: yes

-

Referee: [§4 (quadratic approximation and Riccati equation)] §4 (quadratic approximation): the claim that the quadratic approximation around zero inventory remains accurate enough to produce usable quote maps when fill probabilities are nonlinear is load-bearing for the practical utility of the Riccati solution and linearized decompositions. No error bounds, numerical comparisons against the full nonlinear problem, or sensitivity analysis with respect to the curvature of the fill-probability function are provided.

Authors: We acknowledge that the practical utility of the quadratic approximation would be strengthened by additional validation. While the approximation follows the standard small-inventory expansion of Bergault et al. and is motivated by the typical operating regime of bond dealers, we will add a new subsection to §4 containing numerical comparisons of the quadratic quote maps against the full nonlinear HJB solution for representative nonlinear fill-probability functions (logistic and power-law). The subsection will report relative errors in the optimal quotes and include a brief sensitivity analysis with respect to the curvature parameter of the fill probability. Analytic error bounds remain elusive because of the nonlinearity, but the numerical evidence will quantify the approximation's accuracy in the relevant inventory range. revision: yes

Circularity Check

No significant circularity; derivation is self-contained

full rationale

The paper's core derivation begins from a standard stochastic optimal control formulation of OTC bond market making with quadratic inventory penalty and an exogenous hit-ratio target. Dualization of the target term is introduced to restore separability of the reduced HJB equation, after which optimal controls are recovered exactly via the inverse fill-probability function and the Hamiltonian derivative. The subsequent quadratic approximation follows the external Bergault et al. framework to produce a Riccati equation for inventory curvature while preserving the exact quote map. All steps rely on established control-theoretic techniques and cited prior work rather than self-definitional reductions, fitted inputs renamed as predictions, or load-bearing self-citations. The hit-ratio target enters as an independent parameter, and the resulting explicit quote decompositions (riskless spread, inventory correction, hit-ratio correction) are direct algebraic consequences of the stated assumptions without circular closure.

Axiom & Free-Parameter Ledger

free parameters (2)

- hit-ratio target level

- inventory risk aversion coefficient

axioms (2)

- domain assumption The mid-price follows a diffusion and fill events are independent of inventory state except through the chosen quotes.

- domain assumption The fill-probability function is strictly decreasing and invertible.

Reference graph

Works this paper leans on

-

[1]

Avellaneda and S

M. Avellaneda and S. Stoikov, High-frequency trading in a limit order book,Quant. Fi- nance, 2008,8, 217–224

2008

-

[2]

Barzykin, P

A. Barzykin, P. Bergault, and O. Gu´ eant, Algorithmic market making in dealer markets with hedging and market impact,Math. Finance, 33(1):41–79, 2023

2023

-

[3]

A. Barzykin, Win-score promotion gates in aggregator-routed RFQ markets: A two-tier stochastic control model,arXiv:2603.10569, 2026

-

[4]

Bergault and O

P. Bergault and O. Gu´ eant, Size matters for OTC market makers: General results and dimensionality reduction techniques,Math. Finance, 31(1):279–322, 2021. 12

2021

-

[5]

Bergault, D

P. Bergault, D. Evangelista, O. Gu´ eant and D. Vieira, Closed-form approximations in multi-asset market making.Appl. Math. Finance, 2021,28, 101–142

2021

-

[6]

P. Bergault and O. Gu´ eant, Liquidity dynamics in RFQ markets and impact on pricing, arXiv:2309.04216, 2023

-

[7]

Bessembinder, S

H. Bessembinder, S. Jacobsen, W. Maxwell, and K. Venkataraman, Capital commitment and illiquidity in corporate bonds,J. Finance, 73(4):1615–1661, 2018

2018

-

[8]

Bessembinder, C

H. Bessembinder, C. Spatt, and K. Venkataraman, A survey of the microstructure of fixed-income markets,J. Financ. Quant. Anal., 55(1):1–45, 2020

2020

-

[9]

Cartea, S

´A. Cartea, S. Jaimungal, and J. Ricci, Buy low, sell high: A high frequency trading perspective,SIAM J. Financial Math., 5(1):415–444, 2014

2014

-

[10]

Cartea, S

´A. Cartea, S. Jaimungal, and J. Penalva,Algorithmic and High-Frequency Trading, Cam- bridge University Press, 2015

2015

-

[11]

Fermanian, O

J.-D. Fermanian, O. Gu´ eant, and J. Pu, The behavior of dealers and clients on the Eu- ropean corporate bond market: The case of Multi-Dealer-to-Client platforms,Mark. Mi- crostruct. Liq., 2(03n04):1750004, 2016

2016

-

[12]

M. A. Goldstein and E. S. Hotchkiss, Providing liquidity in an illiquid market: Dealer behavior in U.S. corporate bonds,J. Financ. Econ., 135(1):16–40, 2020

2020

-

[13]

Gu´ eant, C.-A

O. Gu´ eant, C.-A. Lehalle and J. Fernandez-Tapia, Dealing with the inventory risk: a solution to the market making problem.Math. Financ. Econ., 2013,7, 477–507

2013

-

[14]

Gu´ eant,The Financial Mathematics of Market Liquidity: From optimal execution to market making, Chapman and Hall/CRC: Boca Raton, FL, 2016

O. Gu´ eant,The Financial Mathematics of Market Liquidity: From optimal execution to market making, Chapman and Hall/CRC: Boca Raton, FL, 2016

2016

-

[15]

Gu´ eant and I

O. Gu´ eant and I. Manziuk, Deep reinforcement learning for market making in corporate bonds: Beating the curse of dimensionality,Appl. Math. Finance, 26(5):387–452, 2019

2019

-

[16]

Hendershott and A

T. Hendershott and A. Madhavan, Click or call? Auction versus search in the over-the- counter market,J. Finance, 70(1):419–447, 2015

2015

-

[17]

Jurkatis, A

S. Jurkatis, A. Schrimpf, K. Todorov, and N. Vause, Relationship discounts in corporate bond trading,BIS Working Papers, No. 1140, 2023

2023

-

[18]

Kargar, B

M. Kargar, B. Lester, S. Plante, and P.-O. Weill, Sequential search for corporate bonds, Federal Reserve Bank of Philadelphia Working Paper25-08, 2025

2025

-

[19]

Mar´ ın Mart´ ınez, S

P. Mar´ ın Mart´ ınez, S. Ardanza-Trevijano, and J. Sabio, Causal interventions in bond multi-dealer-to-client platforms,PLOS ONE, 21(1):e0341369, 2026

2026

-

[20]

O’Hara, Y

M. O’Hara, Y. Wang, and X. (Alex) Zhou, The execution quality of corporate bonds, J. Financ. Econ., 130(2):308–326, 2018

2018

-

[21]

O’Hara and X

M. O’Hara and X. (Alex) Zhou, The electronic evolution of corporate bond dealers,J. Fi- nanc. Econ., 140(2):368–390, 2021

2021

-

[22]

Oomen, Execution in an aggregator.Quant

R. Oomen, Execution in an aggregator.Quant. Finance, 2017,17, 383–404

2017

-

[23]

Wang, The limits of multi-dealer platforms,J

C. Wang, The limits of multi-dealer platforms,J. Financ. Econ., 149(3):434–450, 2023. 13 Appendix A Quadratic approximation for non-symmetric trade intensities In Section 2.3, we applied the BEGV framework to derive an approximation for the value func- tion and optimal dual variables under the assumption of symmetric trade intensities. In this section, we...

2023

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.