Recognition: unknown

Sharp adaptive nonparametric testing for constant volatility

Pith reviewed 2026-05-07 14:33 UTC · model grok-4.3

The pith

A test for constant volatility achieves minimax optimality and adaptivity by measuring deviations as a ratio to the L2 average.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

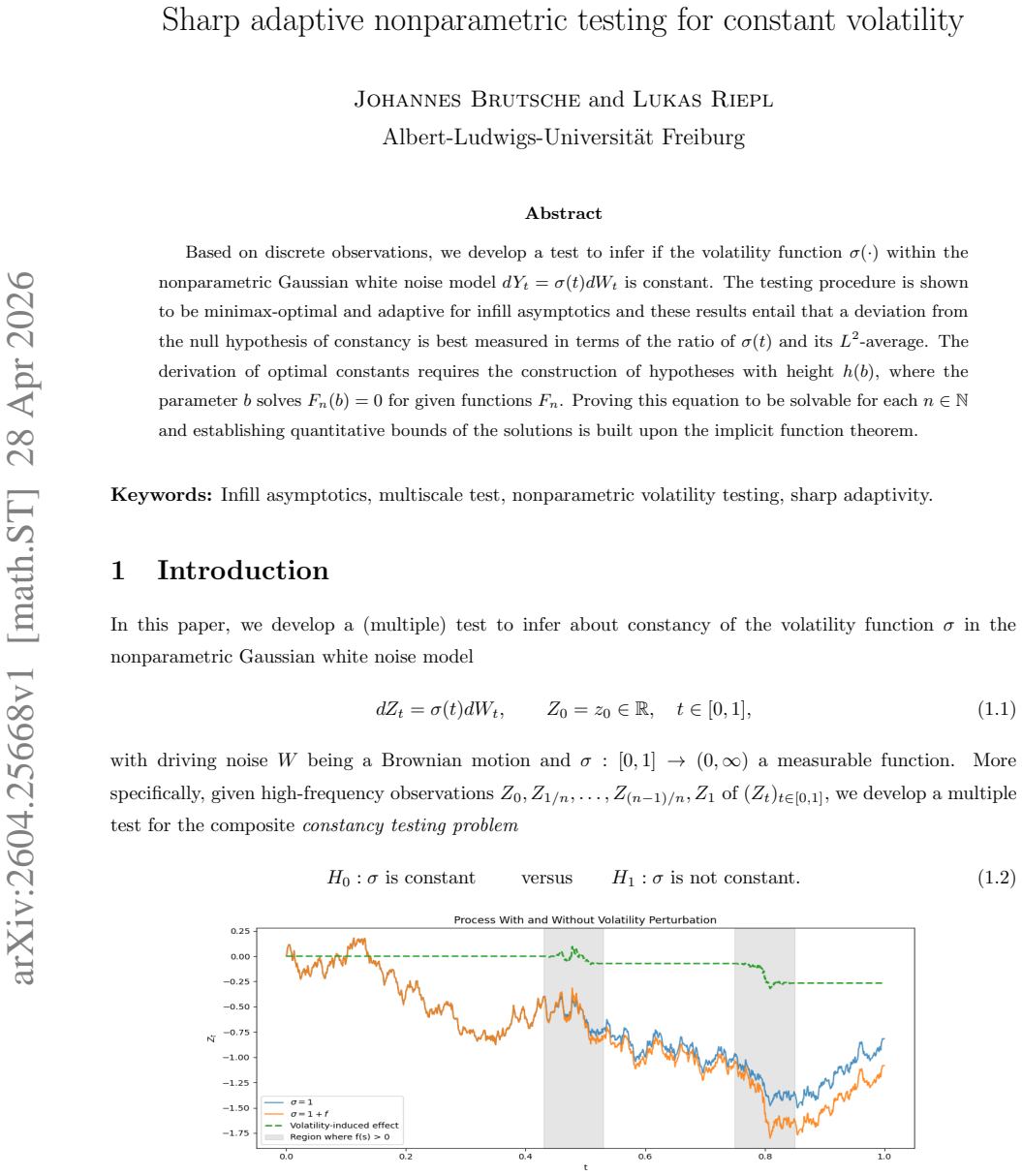

Based on discrete observations, we develop a test to infer if the volatility function σ(·) within the nonparametric Gaussian white noise model dY_t = σ(t)dW_t is constant. The testing procedure is shown to be minimax-optimal and adaptive for infill asymptotics and these results entail that a deviation from the null hypothesis of constancy is best measured in terms of the ratio of σ(t) and its L²-average. The derivation of optimal constants requires the construction of hypotheses with height h(b), where the parameter b solves F_n(b)=0 for given functions F_n. Proving this equation to be solvable for each n∈N and establishing quantitative bounds of the solutions is built upon the implicit

What carries the argument

The family of alternative hypotheses whose height h(b) is chosen so that the auxiliary equation F_n(b)=0 holds, with solvability and bounds for b established by the implicit function theorem for every n.

Load-bearing premise

The observations are generated exactly from the Gaussian white noise model dY_t = σ(t) dW_t and the equation F_n(b)=0 admits a solution for every finite sample size n.

What would settle it

A Monte Carlo experiment in which the empirical power of the test lies strictly below the minimax boundary predicted by the solved value of b for alternatives scaled by the ratio σ(t) over its L2 average would refute the optimality claim.

Figures

read the original abstract

Based on discrete observations, we develop a test to infer if the volatility function $\sigma(\cdot)$ within the nonparametric Gaussian white noise model $dY_t = \sigma(t)dW_t$ is constant. The testing procedure is shown to be minimax-optimal and adaptive for infill asymptotics and these results entail that a deviation from the null hypothesis of constancy is best measured in terms of the ratio of $\sigma(t)$ and its $L^2$-average. The derivation of optimal constants requires the construction of hypotheses with height $h(b)$, where the parameter $b$ solves $F_n(b)=0$ for given functions $F_n$. Proving this equation to be solvable for each $n\in\mathbb{N}$ and establishing quantitative bounds of the solutions is built upon the implicit function theorem.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops a test for the null hypothesis that the volatility function σ(·) is constant in the nonparametric Gaussian white noise model dY_t = σ(t)dW_t observed at discrete times. It establishes minimax optimality and adaptivity of the procedure under infill asymptotics, showing that deviations from constancy are optimally detected via the ratio of σ(t) to its L²-average. The optimality constants are derived by constructing least-favorable alternatives using solutions b to F_n(b)=0, with existence and bounds justified by the implicit function theorem.

Significance. If the optimality and adaptation claims hold with the stated sharp constants, the work would advance nonparametric testing for stochastic volatility by providing adaptive procedures and a novel ratio-based characterization of the separation rate. The technical construction via the implicit function theorem for hypothesis generation is a potential strength if the uniform bounds are rigorously verified.

major comments (2)

- [Abstract] Abstract: The claim that existence for every n and quantitative bounds on solutions to F_n(b)=0 are obtained from the implicit function theorem requires explicit verification that |∂F_n/∂b| ≥ c > 0 uniformly in n near the root. The standard IFT guarantees only local existence and does not automatically supply the uniform-in-n control needed to justify the sharp minimax constants for the ratio-based separation in the infill regime.

- [Derivation of optimal constants] Derivation of optimal constants (via hypothesis construction with height h(b)): The minimax optimality and adaptation results rest on solvability of F_n(b)=0 for each n. Without a separate monotonicity argument or uniform derivative bound, the least-favorable alternatives may not yield the claimed sharp constants, undermining the central assertion that deviation is best measured by the ratio of σ(t) and its L²-average.

minor comments (1)

- [Model and setup] Clarify the precise statement of the infill asymptotic regime and the discrete observation scheme in the model definition to ensure consistency with the testing procedure.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments. The points raised about the application of the implicit function theorem and the justification of sharp constants are substantive and we address them directly below, indicating the revisions we will undertake.

read point-by-point responses

-

Referee: [Abstract] Abstract: The claim that existence for every n and quantitative bounds on solutions to F_n(b)=0 are obtained from the implicit function theorem requires explicit verification that |∂F_n/∂b| ≥ c > 0 uniformly in n near the root. The standard IFT guarantees only local existence and does not automatically supply the uniform-in-n control needed to justify the sharp minimax constants for the ratio-based separation in the infill regime.

Authors: We agree that the standard implicit function theorem yields only local existence for each fixed n and that uniform-in-n control on the derivative is required to justify the sharp constants under infill asymptotics. In the manuscript the IFT is applied pointwise in n, with uniformity expected to follow from uniform convergence of F_n to a limiting F with F'(b*) bounded away from zero together with the explicit form of F_n. To make this rigorous we will insert a new lemma establishing the uniform lower bound |∂F_n/∂b| ≥ c > 0 for all sufficiently large n and b in a neighborhood of the root, using the explicit expression for F_n and standard domination arguments. This addition will supply the missing quantitative control without changing the main results. revision: yes

-

Referee: [Derivation of optimal constants] Derivation of optimal constants (via hypothesis construction with height h(b)): The minimax optimality and adaptation results rest on solvability of F_n(b)=0 for each n. Without a separate monotonicity argument or uniform derivative bound, the least-favorable alternatives may not yield the claimed sharp constants, undermining the central assertion that deviation is best measured by the ratio of σ(t) and its L²-average.

Authors: The referee is correct that both the uniform derivative bound and, where necessary, a monotonicity argument are needed to guarantee that the solutions b_n produce well-defined least-favorable alternatives with the claimed sharp constants. We will add the uniform derivative bound as described in the response to the first comment and, if a monotonicity statement is not already explicit, include a short argument showing that F_n is strictly monotone in a neighborhood of the root (again using the explicit form of F_n). These clarifications will confirm that the ratio-based separation rate is indeed optimal and that the adaptation results hold with the stated constants. revision: yes

Circularity Check

No significant circularity; derivation applies external IFT to constructed hypotheses

full rationale

The paper defines hypotheses via height h(b) where b solves the newly introduced equation F_n(b)=0, then invokes the implicit function theorem (an external result) to prove solvability for each n and obtain quantitative bounds. This construction feeds into the minimax optimality and adaptation arguments for infill asymptotics, but does not reduce the final claims to a self-definition, a fitted parameter renamed as prediction, or a self-citation chain. The central result that deviations are best measured by the ratio of σ(t) to its L²-average follows from the asymptotic analysis of these alternatives and remains independent of the result itself. No load-bearing self-citations or ansatzes are present in the provided text.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Observations follow the nonparametric Gaussian white noise model dY_t = σ(t) dW_t

- domain assumption Infill asymptotics govern the discrete observation scheme

Reference graph

Works this paper leans on

-

[1]

Change-point inference on volatility in noisy I t\^o semimartingales

Markus Bibinger and Mehmet Madensoy. Change-point inference on volatility in noisy I t\^o semimartingales. Stochastic Process. Appl., 129 0 (12): 0 4878--4925, 2019. ISSN 0304-4149,1879-209X. doi:10.1016/j.spa.2018.12.013. URL https://doi.org/10.1016/j.spa.2018.12.013

-

[2]

Nonparametric change-point analysis of volatility

Markus Bibinger, Moritz Jirak, and Mathias Vetter. Nonparametric change-point analysis of volatility. Ann. Statist., 45 0 (4): 0 1542--1578, 2017. ISSN 0090-5364,2168-8966. doi:10.1214/16-AOS1499. URL https://doi.org/10.1214/16-AOS1499

-

[3]

Sharp adaptive and pathwise stable similarity testing for scalar ergodic diffusions

Johannes Brutsche and Angelika Rohde. Sharp adaptive and pathwise stable similarity testing for scalar ergodic diffusions. Ann. Statist., 52 0 (3): 0 1127--1151, 2024. ISSN 0090-5364,2168-8966. doi:10.1214/24-aos2386. URL https://doi.org/10.1214/24-aos2386

-

[4]

A. C. Davison. Statistical models, volume 11 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 2003. ISBN 0-521-77339-3. doi:10.1017/CBO9780511815850. URL https://doi.org/10.1017/CBO9780511815850

-

[5]

Holger Dette and Mark Podolskij. Testing the parametric form of the volatility in continuous time diffusion models---a stochastic process approach. J. Econometrics, 143 0 (1): 0 56--73, 2008. ISSN 0304-4076,1872-6895. doi:10.1016/j.jeconom.2007.08.002. URL https://doi.org/10.1016/j.jeconom.2007.08.002

-

[6]

On a test for a parametric form of volatility in continuous time financial models

Holger Dette, von Lieres, and Carsten Wilkau. On a test for a parametric form of volatility in continuous time financial models. Finance Stoch., 7 0 (3): 0 363--384, 2003. ISSN 0949-2984,1432-1122. doi:10.1007/s007800200087. URL https://doi.org/10.1007/s007800200087

-

[7]

Holger Dette, Mark Podolskij, and Mathias Vetter. Estimation of integrated volatility in continuous-time financial models with applications to goodness-of-fit testing. Scand. J. Statist., 33 0 (2): 0 259--278, 2006. ISSN 0303-6898,1467-9469. doi:10.1111/j.1467-9469.2006.00479.x. URL https://doi.org/10.1111/j.1467-9469.2006.00479.x

-

[8]

David L. Donoho. Asymptotic minimax risk for sup-norm loss: solution via optimal recovery. Probab. Theory Related Fields, 99 0 (2): 0 145--170, 1994. ISSN 0178-8051,1432-2064. doi:10.1007/BF01199020. URL https://doi.org/10.1007/BF01199020

-

[9]

Lutz D\"umbgen and Vladimir G. Spokoiny. Multiscale testing of qualitative hypotheses. Ann. Statist., 29 0 (1): 0 124--152, 2001. ISSN 0090-5364,2168-8966. doi:10.1214/aos/996986504. URL https://doi.org/10.1214/aos/996986504

-

[10]

Lutz D\"umbgen and G\"unther Walther. Multiscale inference about a density, technical report. 2007. Available at: https://arxiv.org/abs/0706.3968v2

-

[11]

Lutz D\"umbgen and G\"unther Walther. Multiscale inference about a density. Ann. Statist., 36 0 (4): 0 1758--1785, 2008. ISSN 0090-5364,2168-8966. doi:10.1214/07-AOS521. URL https://doi.org/10.1214/07-AOS521

-

[12]

W. H\"ardle and E. Mammen. Comparing nonparametric versus parametric regression fits. Ann. Statist., 21 0 (4): 0 1926--1947, 1993. ISSN 0090-5364,2168-8966. doi:10.1214/aos/1176349403. URL https://doi.org/10.1214/aos/1176349403

-

[13]

URLhttps://link.springer.com/10.1007/978-3-030-61871-1

Olav Kallenberg. Foundations of modern probability, volume 99 of Probability Theory and Stochastic Modelling. Springer, Cham, third edition, 2021. ISBN 978-3-030-61871-1; 978-3-030-61870-4. doi:10.1007/978-3-030-61871-1. URL https://doi.org/10.1007/978-3-030-61871-1

-

[14]

Detection of a structural break in intraday volatility pattern

Piotr Kokoszka, Tim Kutta, Neda Mohammadi, Haonan Wang, and Shixuan Wang. Detection of a structural break in intraday volatility pattern. Stochastic Process. Appl., 176: 0 Paper No. 104426, 15, 2024. ISSN 0304-4149,1879-209X. doi:10.1016/j.spa.2024.104426. URL https://doi.org/10.1016/j.spa.2024.104426

-

[15]

B. Laurent and P. Massart. Adaptive estimation of a quadratic functional by model selection. Ann. Statist., 28 0 (5): 0 1302--1338, 2000. ISSN 0090-5364,2168-8966. doi:10.1214/aos/1015957395. URL https://doi.org/10.1214/aos/1015957395

-

[16]

Sergei L. Leonov. Remarks on extremal problems in nonparametric curve estimation. Statist. Probab. Lett., 43 0 (2): 0 169--178, 1999. ISSN 0167-7152,1879-2103. doi:10.1016/S0167-7152(98)00256-9. URL https://doi.org/10.1016/S0167-7152(98)00256-9

-

[17]

Adaptive goodness-of-fit tests based on signed ranks

Angelika Rohde. Adaptive goodness-of-fit tests based on signed ranks. Ann. Statist., 36 0 (3): 0 1346--1374, 2008. ISSN 0090-5364,2168-8966. doi:10.1214/009053607000000992. URL https://doi.org/10.1214/009053607000000992

-

[18]

Optimal calibration for multiple testing against local inhomogeneity in higher dimension

Angelika Rohde. Optimal calibration for multiple testing against local inhomogeneity in higher dimension. Probab. Theory Related Fields, 149 0 (3-4): 0 515--559, 2011. ISSN 0178-8051,1432-2064. doi:10.1007/s00440-010-0263-1. URL https://doi.org/10.1007/s00440-010-0263-1

-

[19]

Alexandre B. Tsybakov. Introduction to nonparametric estimation. Springer Series in Statistics. Springer, New York, 2009. ISBN 978-0-387-79051-0. doi:10.1007/b13794. URL https://doi.org/10.1007/b13794. Revised and extended from the 2004 French original, Translated by Vladimir Zaiats

-

[20]

A. W. van der Vaart and Jon A. Wellner. Weak convergence and empirical processes---with applications to statistics. Springer Series in Statistics. Springer, Cham, second edition, 2023. ISBN 978-3-031-29038-1; 978-3-031-29040-4. doi:10.1007/978-3-031-29040-4. URL https://doi.org/10.1007/978-3-031-29040-4

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.