Recognition: unknown

The Financialization of Proof-of-Stake: Asymptotic Centralization under Exogenous Risk Premiums

Pith reviewed 2026-05-07 13:49 UTC · model grok-4.3

The pith

External risk premiums force Proof-of-Stake networks into complete institutional capture as internal staking yields collapse to zero.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

In this heterogeneous macroeconomic model, investors optimize between staking and external variance-dominated investments while consumers balance yields against liquidity needs via quasi-linear utility. The resulting cubic polynomial defines a unique equilibrium in which external risk premiums produce exponential compounding of investor wealth, massive capital inflows, and the collapse of the protocol's internal staking yield to zero. Consequently, consumer wealth becomes strictly upper-bounded, forcing consumers to exit staking entirely and hold all assets in liquid form to satisfy transactional constraints, resulting in complete institutional capture of the PoS consensus layer.

What carries the argument

The heterogeneous continuum of rational actors divided into investors and consumers, whose portfolio and liquidity optimizations are coupled through a cubic polynomial that determines the unique macroeconomic equilibrium.

Load-bearing premise

That investors will always direct capital to external investments whenever those offer higher risk premiums than staking, and that consumer behavior follows a quasi-linear utility that produces a unique equilibrium.

What would settle it

Observation of a large-scale PoS network in which the staking yield remains positive and retail (non-institutional) participants continue to hold a substantial fraction of staked tokens over time.

Figures

read the original abstract

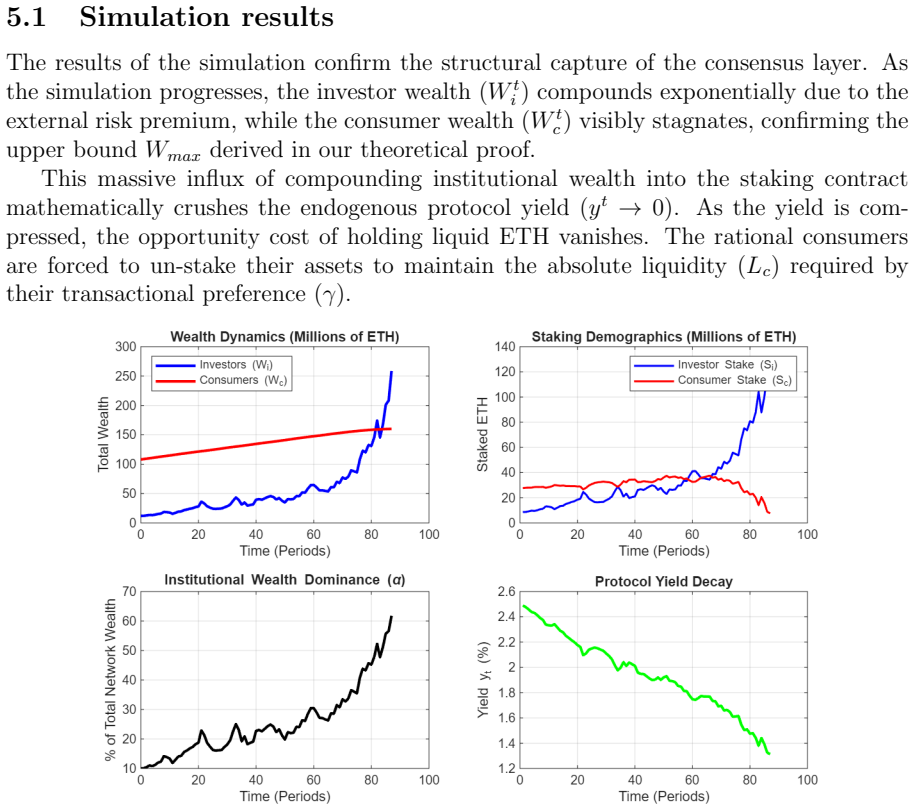

This paper introduces a heterogeneous macroeconomic model of a Proof-of-Stake (PoS) network to analyze the long-term centralizing effects of external traditional finance (TradFi) yields. We model a continuum of rational actors divided into two distinct classes: investors, who optimize portfolios between staking and external variance-dominated investments, and consumers, who balance staking yields against the transactional utility of holding liquid assets. By employing a quasi-linear utility function to model consumer behavior, we derive a cubic polynomial that strictly defines the unique macroeconomic equilibrium of the coupled network. The model demonstrates that, at scale, external macroeconomic factors force the complete institutional capture of the PoS consensus layer. Because investors have access to external risk premiums, their wealth compounds exponentially, leading to massive capital inflows that crush the protocol's internal staking yield to effectively zero. We show that as the yield is crushed, consumer wealth becomes strictly upper-bounded. Ultimately, consumers are forced to cease staking entirely and hold all remaining wealth in liquid form to satisfy their transactional constraints.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a heterogeneous-agent macroeconomic model for Proof-of-Stake blockchain networks, distinguishing between investors who allocate between staking and external variance-dominated assets and consumers who use quasi-linear utility to trade off staking yields against liquidity needs. From the equilibrium conditions, a cubic polynomial is derived that is asserted to uniquely pin down the macroeconomic equilibrium. The central result is that exogenous TradFi risk premiums drive exponential wealth growth for investors, causing massive inflows that drive the internal staking yield asymptotically to zero, forcing consumers to exit staking and hold only liquid assets.

Significance. If the model's derivations are correct and the uniqueness of the equilibrium root is rigorously established, the result would provide a formal mechanism by which external financial markets can induce centralization in PoS systems, with the yield collapse and consumer exit as falsifiable predictions. This could inform discussions on PoS incentive design and the interplay between DeFi and TradFi. The use of a continuum of agents and quasi-linear utility is a standard approach that allows closed-form analysis.

major comments (2)

- [Abstract] Abstract: the claim that the cubic polynomial 'strictly defines the unique macroeconomic equilibrium' is load-bearing for the asymptotic centralization result, yet no derivation of the cubic or proof of uniqueness is supplied. A general cubic admits up to three real roots; the manuscript must show (via sign changes, derivative analysis, or exhaustive root counting) that exactly one root lies in the admissible interval for aggregate staking fraction (0,1) for all exogenous risk-premium values. Absent this, multiple equilibria remain possible and the forced yield-to-zero outcome is not guaranteed.

- [Abstract] Abstract and equilibrium section: the assertion that investor wealth compounds exponentially, crushing internal yield to zero and strictly upper-bounding consumer wealth, requires explicit steps linking the portfolio-optimization first-order conditions to the cubic root. It is unclear whether this collapse is an independent prediction or follows tautologically from the chosen functional forms (quasi-linear consumer utility and variance-dominated external assets); a robustness check with alternative utility specifications or numerical root tabulation for varying risk premiums would be needed to support the institutional-capture conclusion.

minor comments (1)

- The abstract would benefit from a one-sentence statement of the key modeling assumptions (continuum of agents, specific external-asset variance process) to allow readers to assess the scope of the uniqueness claim without reading the full derivation.

Simulated Author's Rebuttal

We thank the referee for the thorough and constructive report. The comments highlight important gaps in the presentation of the equilibrium derivation and uniqueness proof, as well as the need for clearer linkage to the centralization result. We address each point below and commit to revisions that strengthen the manuscript without altering its core claims.

read point-by-point responses

-

Referee: [Abstract] Abstract: the claim that the cubic polynomial 'strictly defines the unique macroeconomic equilibrium' is load-bearing for the asymptotic centralization result, yet no derivation of the cubic or proof of uniqueness is supplied. A general cubic admits up to three real roots; the manuscript must show (via sign changes, derivative analysis, or exhaustive root counting) that exactly one root lies in the admissible interval for aggregate staking fraction (0,1) for all exogenous risk-premium values. Absent this, multiple equilibria remain possible and the forced yield-to-zero outcome is not guaranteed.

Authors: We agree that an explicit derivation and uniqueness proof are required for the claim to be rigorous. The cubic is obtained by substituting the investors' optimal staking share (from mean-variance optimization) and the consumers' optimal liquid-asset demand (from quasi-linear utility) into the market-clearing condition for total staked capital; the resulting equation in the aggregate staking fraction s is cubic. In the revised manuscript we will add a dedicated subsection (and appendix) that (i) derives the cubic coefficients step-by-step from the first-order conditions, (ii) shows that the cubic's derivative is strictly negative over (0,1) for all admissible risk-premium values (hence at most one root), and (iii) uses Descartes' rule of signs together with boundary evaluation to confirm exactly one root lies in (0,1). Numerical root tabulations for a grid of risk-premium values will also be included to illustrate uniqueness. revision: yes

-

Referee: [Abstract] Abstract and equilibrium section: the assertion that investor wealth compounds exponentially, crushing internal yield to zero and strictly upper-bounding consumer wealth, requires explicit steps linking the portfolio-optimization first-order conditions to the cubic root. It is unclear whether this collapse is an independent prediction or follows tautologically from the chosen functional forms (quasi-linear consumer utility and variance-dominated external assets); a robustness check with alternative utility specifications or numerical root tabulation for varying risk premiums would be needed to support the institutional-capture conclusion.

Authors: The exponential growth of investor wealth follows directly from their FOC: when the external risk premium is positive they optimally place a strictly positive share of wealth in the variance-dominated asset, producing a constant growth rate proportional to that premium. This growth enters the market-clearing condition and forces the equilibrium staking fraction s* (the relevant root of the cubic) toward 1, which in turn drives the internal yield to zero and caps consumer wealth. While the quasi-linear specification enables the closed-form cubic, the qualitative centralization mechanism is not an artifact; it arises because external returns dominate any bounded internal yield. In revision we will (i) insert the explicit algebraic steps connecting the investors' FOC to the cubic coefficients, (ii) add a short robustness subsection that solves the model numerically under log utility for consumers (via fixed-point iteration) and shows the same asymptotic consumer exit for high risk premiums, and (iii) include tables of s* and yields across a range of premiums. revision: yes

Circularity Check

No significant circularity; equilibrium derived from explicit model assumptions

full rationale

The paper constructs investor portfolio optimization and consumer quasi-linear utility from first principles, equates marginal conditions to obtain a cubic polynomial in the equilibrium staking fraction, and then performs asymptotic analysis on that root as external risk premiums or aggregate wealth scale. The claimed yield collapse to zero and institutional capture are mathematical consequences of solving the derived cubic under the stated parameter regime, not presupposed by the functional forms or by any self-citation. No load-bearing step reduces to a fitted input renamed as prediction, a self-definitional loop, or an imported uniqueness theorem; the derivation remains self-contained once the cubic is accepted as the equilibrium condition.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Borgese et al

E. Borgese et al. Studying the compounding effect: The role of proof-of-stake pa- rameters on wealth distribution. InCEUR Workshop Proceedings, volume 3460, 2023. 12

2023

-

[2]

Tokenomics: Dynamic adoption and valuation.The Review of Financial Studies, 2022

Lin William Cong, Zhiguo He, and Ke Tang. Tokenomics: Dynamic adoption and valuation.The Review of Financial Studies, 2022

2022

-

[3]

Economics of proof-of-stake payment systems

Giulia Fanti, Leonid Kogan, and Pramod Viswanath. Economics of proof-of-stake payment systems. Working Paper, 2019

2019

-

[4]

A macro finance model for proof-of-stake Ethereum

Urban Jermann. A macro finance model for proof-of-stake Ethereum. Working Paper, 2025

2025

-

[5]

Optimal issuance for proof-of-stake blockchains

Urban Jermann. Optimal issuance for proof-of-stake blockchains. Working Paper, University of Pennsylvania, 2025

2025

-

[6]

M. E. Kose, V. Rivera, and Fahad Saleh. Equilibrium staking levels in a proof-of- stake cryptocurrency. Working Paper, 2021

2021

-

[7]

Goose-2025 & eggs-2025 final report, 2026

Lido DAO. Goose-2025 & eggs-2025 final report, 2026. Accessed: 2026-04-26

2025

-

[8]

The merge - a deep dive with nansen, 2022

Nansen. The merge - a deep dive with nansen, 2022. Accessed: 2026-04-26

2022

-

[9]

Evolution of shares in a proof-of-stake cryptocurrency

Ioanid Ro¸ su and Fahad Saleh. Evolution of shares in a proof-of-stake cryptocurrency. Management Science, 67(11):6613–6632, 2021

2021

-

[10]

Transaction fee mechanism design

Tim Roughgarden. Transaction fee mechanism design. InProceedings of the 22nd ACM Conference on Economics and Computation, 2021

2021

-

[11]

Blockchain without waste: Proof-of-stake.The Review of Financial Studies, 34(3):1156–1190, 2021

Fahad Saleh. Blockchain without waste: Proof-of-stake.The Review of Financial Studies, 34(3):1156–1190, 2021. 13

2021

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.