Recognition: unknown

Distributionally Robust Insurance under Bregman-Wasserstein Divergence

Pith reviewed 2026-05-07 05:56 UTC · model grok-4.3

The pith

Bregman-Wasserstein balls around a benchmark loss distribution produce closed-form optimal insurance indemnities.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

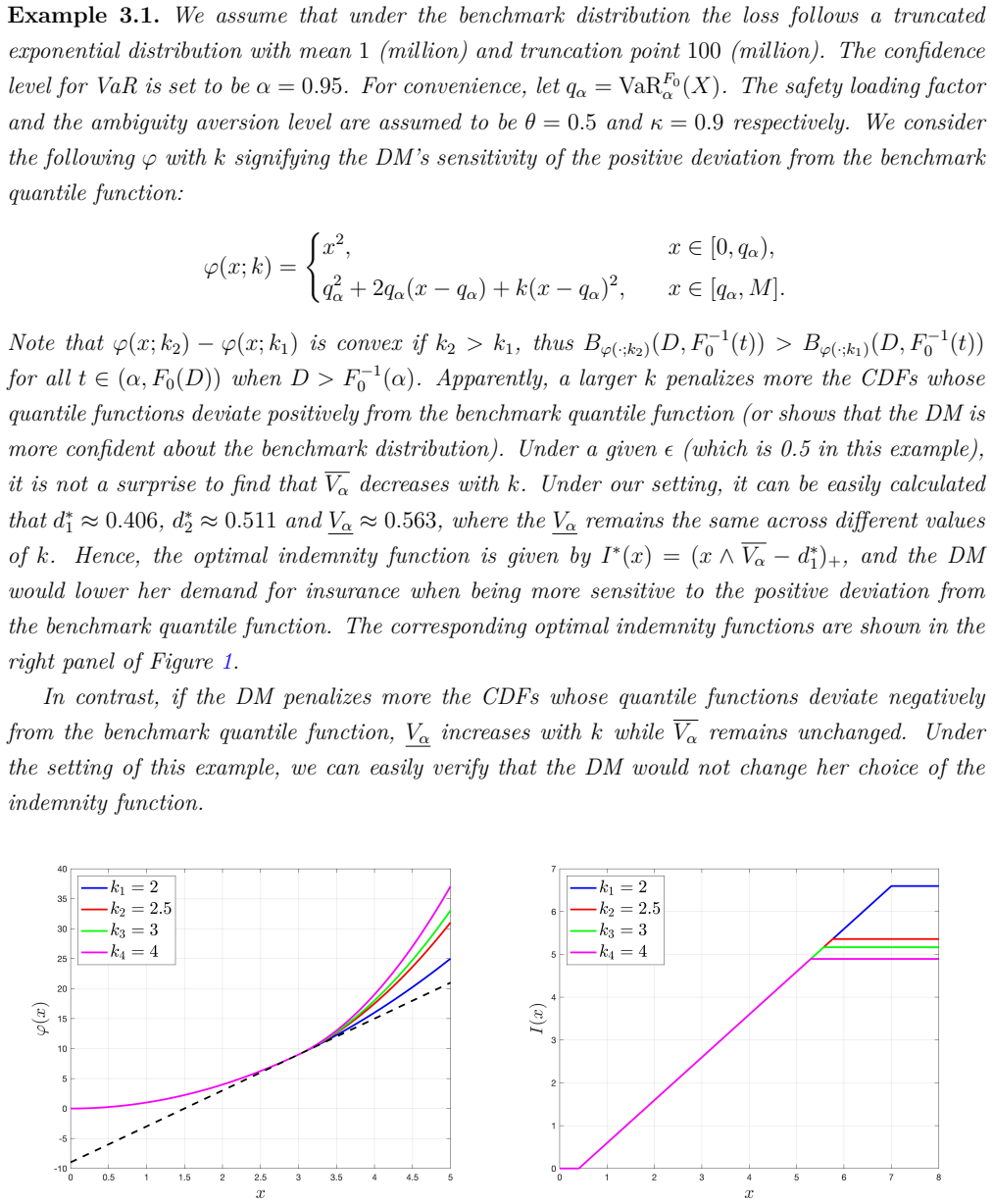

In the first problem, the policyholder maximizes an alpha-maxmin criterion involving Value-at-Risk over the BW ball, yielding a closed-form optimal indemnity. In the second, the policyholder minimizes the worst-case value of a convex distortion risk measure subject to a VaR constraint, again with explicit solutions for indemnity and worst-case law obtained by Lagrangian and modification techniques. The paper demonstrates analytically and numerically that the asymmetry parameter of the BW divergence alters the optimal indemnity structure compared to symmetric cases.

What carries the argument

Bregman-Wasserstein divergence ball, which defines the ambiguity set of loss distributions with asymmetric penalization of deviations from a benchmark, combined with Lagrangian methods and modification arguments to obtain closed-form indemnity functions.

If this is right

- The optimal indemnity provides explicit coverage levels that vary with loss size and the asymmetry parameter.

- The worst-case distribution is also obtained in closed form, identifying the loss scenarios that drive the contract design.

- Numerical illustrations with Tail Value-at-Risk confirm that stronger asymmetry changes coverage in the upper tail.

- The solutions allow direct computation of robust contracts without iterative numerical optimization.

Where Pith is reading between the lines

- The same Lagrangian-plus-modification technique could extend to multi-period insurance or reinsurance design under similar ambiguity.

- Regulators could adopt BW balls to set capital requirements that treat over- and under-estimation of losses differently.

- Empirical checks on historical loss data could test whether the predicted indemnity shapes improve out-of-sample performance.

- Hybrid ambiguity sets combining BW divergence with other divergences might yield further closed-form results.

Load-bearing premise

The set of possible loss distributions is exactly the Bregman-Wasserstein ball of a certain radius around a known benchmark distribution, and the policyholder uses either alpha-maxmin VaR preferences or minimizes a worst-case convex distortion risk measure subject to a VaR constraint.

What would settle it

Solve the optimization problem numerically for a concrete benchmark distribution and asymmetry parameter, then check whether the resulting indemnity function matches the paper's closed-form expression; systematic mismatch would disprove the derivation.

Figures

read the original abstract

This paper investigates two optimal insurance contracting problems under distributional uncertainty from the perspective of a potential policyholder, utilizing a Bregman-Wasserstein (BW) ball to characterize the ambiguity set of loss distributions. Unlike the $p$-Wasserstein distance, BW divergence enables asymmetric penalization of deviations from the benchmark distribution. The first problem examines an insurance demand model where the policyholder adopts an $\alpha$-maxmin preference with Value-at-Risk (VaR). We derive the optimal indemnity function in closed form and study, both analytically and numerically, how the asymmetry inherent in BW divergence influences the optimal indemnity structure. The second problem employs a robust optimization framework, where the policyholder aims to secure robust insurance indemnity by minimizing the worst-case convex distortion risk measure while adhering to a guaranteed VaR constraint. In this context, we provide explicit characterizations of both the optimal indemnity and the worst-case distribution in closed form through a combined approach using the Lagrangian method and modification arguments. To illustrate the practical implications of our theoretical findings, we include a concrete example based on Tail Value-at-Risk (TVaR).

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper examines two optimal insurance design problems under distributional ambiguity, where the ambiguity set is a Bregman-Wasserstein ball centered at a benchmark loss distribution. The first problem derives a closed-form optimal indemnity for an α-maxmin policyholder using Value-at-Risk. The second problem characterizes both the optimal indemnity and the worst-case distribution in closed form when minimizing a worst-case convex distortion risk measure subject to a guaranteed VaR constraint, via Lagrangian methods combined with modification arguments; a concrete TVaR example is provided to illustrate the results, along with analytical and numerical analysis of the effects of asymmetry in the BW divergence.

Significance. If the closed-form characterizations are rigorously justified, the work would extend the literature on distributionally robust insurance by replacing symmetric Wasserstein distances with the asymmetric Bregman-Wasserstein divergence, allowing more flexible modeling of ambiguity aversion. The explicit solutions and the study of asymmetry could provide practical insights for contract design and risk management under model uncertainty.

major comments (1)

- [Section on the robust optimization framework and Lagrangian application for the second problem] In the derivation of the second problem (minimizing the worst-case convex distortion risk measure subject to a VaR constraint inside the BW ball), the manuscript invokes the Lagrangian method and modification arguments to obtain explicit closed-form expressions for the optimal indemnity and worst-case distribution without stating or verifying the requisite constraint qualifications for strong duality. In the infinite-dimensional setting of probability measures equipped with BW divergence, the ambiguity set need not be weakly compact, the distortion risk measure need not be weakly lower-semicontinuous, and Slater-type interior-point conditions can fail when the benchmark distribution has atoms or when the VaR constraint binds; this leaves open whether the derived expressions solve the original primal problem or only a relaxed dual.

minor comments (2)

- [Numerical illustrations and TVaR example] The numerical study of asymmetry in the first problem and the TVaR example in the second problem would benefit from explicit reporting of the benchmark distribution parameters, the chosen BW divergence parameters, and any discretization or approximation scheme used to compute the worst-case distributions.

- [Preliminaries and problem formulation] Notation for the Bregman-Wasserstein divergence and the associated dual variables could be introduced more explicitly at the outset to improve readability when the Lagrangian is formed.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on our manuscript. The observation regarding the need for explicit constraint qualifications to justify strong duality in the second problem is well-taken. We address this point below and will revise the manuscript accordingly to strengthen the technical foundation.

read point-by-point responses

-

Referee: In the derivation of the second problem (minimizing the worst-case convex distortion risk measure subject to a VaR constraint inside the BW ball), the manuscript invokes the Lagrangian method and modification arguments to obtain explicit closed-form expressions for the optimal indemnity and worst-case distribution without stating or verifying the requisite constraint qualifications for strong duality. In the infinite-dimensional setting of probability measures equipped with BW divergence, the ambiguity set need not be weakly compact, the distortion risk measure need not be weakly lower-semicontinuous, and Slater-type interior-point conditions can fail when the benchmark distribution has atoms or when the VaR constraint binds; this leaves open whether the derived expressions solve the original primal problem or only a relaxed dual.

Authors: We appreciate the referee's identification of this important technical consideration. The modification arguments in Section 4 are used to directly construct and verify optimality of the candidate solutions by showing that any deviation would increase the objective, which is a standard technique in optimal insurance design to establish global optimality without relying solely on duality. However, we acknowledge that a fuller discussion of constraint qualifications is warranted in the infinite-dimensional setting. In the revised manuscript, we will add a dedicated remark (and, if space permits, a short appendix) specifying the conditions under which strong duality holds, including the assumption that the benchmark distribution is atomless. Under this condition, the BW ball is weakly compact and the distortion risk measure is weakly lower semicontinuous, ensuring no duality gap. We will also verify directly that the derived closed-form indemnity and worst-case distribution satisfy the primal problem by substitution into the original objective and constraint. For cases involving atoms or binding VaR constraints, we will explicitly note the limitation and state that the expressions provide optimal candidates that can be confirmed ex post. These additions will not alter the main results or closed-form characterizations but will address the duality concern rigorously. revision: yes

Circularity Check

No circularity; derivations self-contained via standard Lagrangian methods

full rationale

The paper formulates two explicit optimization problems (alpha-maxmin VaR and min worst-case convex distortion risk measure subject to VaR constraint) inside a Bregman-Wasserstein ball, then applies the Lagrangian method plus modification arguments to obtain closed-form optimal indemnity and worst-case distribution. These steps begin from the primal problems as stated and proceed via standard duality techniques without any reduction to self-referential definitions, fitted parameters presented as predictions, or load-bearing self-citations that presuppose the target closed forms. No self-definitional loops, ansatz smuggling, or renaming of known results occur in the derivation chain; the results follow directly from the problem setup and are therefore independent of the outputs.

Axiom & Free-Parameter Ledger

axioms (3)

- domain assumption Loss distributions lie in a Bregman-Wasserstein ball around a benchmark distribution

- domain assumption Policyholder uses alpha-maxmin preference with Value-at-Risk

- domain assumption Risk measure is a convex distortion risk measure with VaR constraint

Reference graph

Works this paper leans on

-

[1]

Albrecher, H., Teugels, J. L., & Beirlant, J. (2017). Reinsurance: Actuarial and Statistical Aspects . John Wiley & Sons. Arrow, K. J. (1974). Optimal insurance and generalized deductibles. Scandinavian Actuarial Journal, 1974(1), 1–42. Artzner, P., Delbaen, F., Eber, J.-M., & Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9(3), 203–22...

-

[2]

Wang, Q., Wang, R., & Wei, Y

Springer. Wang, Q., Wang, R., & Wei, Y. (2020). Distortion riskmetrics on general spaces. ASTIN Bulletin: The Journal of the IAA , 50(3), 827–851. Wang, W. & Zhang, Y. (2025). Preference robust insurance design. A vailable at SSRN 5367781. Xie, X., Liu, H., Mao, T., & Zhu, X. B. (2023). Distributionally robust reinsurance with expectile. ASTIN Bulletin: T...

2020

-

[3]

This completes the proof

26 An analogous argument applies to the interval (1, y]. This completes the proof. Now we are ready to prove Theorem 3.1. First, if ϵ > R 1 α Bφ(M, F −1 0 (t)) dt, we prove that M = sup F ∈B(F0,ϵ) VaRF α (X). Since X is bounded above by M , it implies sup F ∈B(F0,ϵ) VaRF α (X) M. We show that M is the supremum. Let δ1 2 (0, M F −1 0 (α)]. By the monotonic...

2020

-

[4]

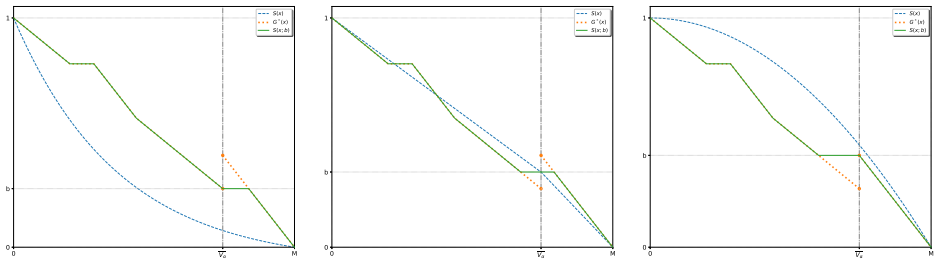

Intuitively, if there exists a b(β), such that S(x; b(β)) is pointwise closer to G∗(x) than S(x), then replacing S(x) by S(x; b(β)) improves the objective

over the relaxed admissible class G. Intuitively, if there exists a b(β), such that S(x; b(β)) is pointwise closer to G∗(x) than S(x), then replacing S(x) by S(x; b(β)) improves the objective. More precisely, it suffices to verify that for all x 2 [0, M] either S(x) S(x; b(β)) G∗(x) or S(x) S(x; b(β)) G∗(x). This property is immediate for x 2 [0, a1(β)) [ ...

1997

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.