Recognition: unknown

Measuring the risk or reducing it, that is the question: is risk measurement necessary for risk reduction?

Pith reviewed 2026-05-07 07:31 UTC · model grok-4.3

The pith

Significant portfolio risk reduction is possible by ordering and cutting exposure to the riskiest scenarios identified through a full-spectrum analysis of the return matrix, without needing traditional risk measurement or minimization.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

A generalization of the numerical rank and condition number that uses the full eigenvalue spectrum of the return matrix directly ranks a finite set of risky scenarios; lowering portfolio exposures to the highest-ranked scenarios produces measurable out-of-sample risk reduction relative to standard risk-minimizing benchmarks, while preserving mean returns and the Sharpe ratio.

What carries the argument

Generalization of numerical rank and condition number of the return matrix that incorporates the entire eigenvalue spectrum instead of only the smallest eigenvalue.

If this is right

- Portfolios built by minimizing conventional risk measures exhibit lower out-of-sample return variability after the proposed exposure adjustments.

- Average portfolio returns and Sharpe ratios remain essentially unchanged under the exposure-reduction strategy.

- Because the adjustments are selective and limited, transaction costs stay manageable while risk is lowered.

- Risk reduction is achieved by acting on an ordering of scenarios rather than by solving an explicit risk-minimization optimization problem.

Where Pith is reading between the lines

- The approach could be tested on high-frequency or intraday return matrices to see whether the same ordering still produces stable out-of-sample gains.

- If the spectrum-based ranking proves robust, it might serve as a lightweight alternative to full covariance estimation in large-scale asset-allocation problems.

- The method's reliance on identifying extreme scenarios suggests a natural link to stress-testing frameworks used in regulatory capital calculations.

Load-bearing premise

The full-spectrum ordering correctly identifies which scenarios are riskiest in a way that actually produces lower out-of-sample return variability when exposures to those scenarios are reduced.

What would settle it

In repeated out-of-sample tests, the variability of portfolio returns after reducing exposures according to the proposed ordering is not lower than the variability obtained from portfolios that minimize standard risk measures.

Figures

read the original abstract

In this research, starting from a widely accepted definition of risk, we support the idea that risk reduction is a more realistic objective than risk minimization, which represents a theoretical utopia. Furthermore, significant risk reduction can be achieved without relying on risk measurement and risk minimization. To this end, we propose a generalization of the numerical rank and the condition number of a matrix, specifically the return matrix in this application. This generalization considers the entire matrix spectrum instead of focusing only on the smallest eigenvalue, as the condition number does. The approach directly provides an order among a finite number of risky scenarios. Risk reduction is obtained by identifying the riskiest scenarios and reducing investment exposures corresponding to them. The validity of this theoretical proposal is supported by a comprehensive experiment performed on real data. The capacity of the proposed approach to effectively reduce risk is proven by measuring the variability of out-of-sample returns for benchmark portfolios-constructed by minimizing standard risk measures-compared to the strategy of reducing exposure in high-risk scenarios. Finally, preventing large losses with limited active management-thereby controlling the impact of transaction costs-not only reduces risk but also preserves the average return and, consequently, the portfolio's Sharpe ratio.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

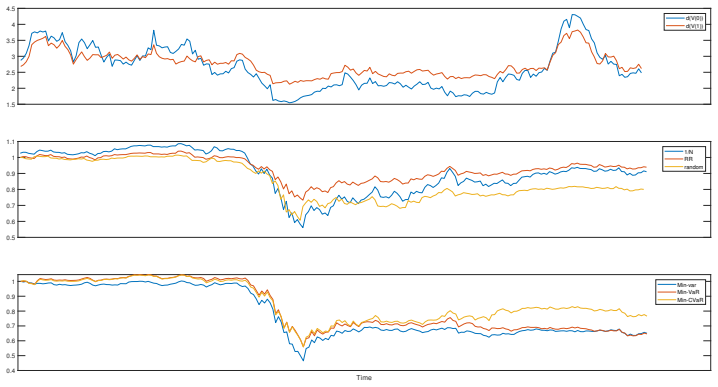

Summary. The paper claims that risk reduction is a more realistic goal than risk minimization in portfolio management. It proposes a generalization of the numerical rank and condition number of the return matrix that incorporates the full matrix spectrum (rather than only the smallest eigenvalue) to directly rank a finite set of risky scenarios by riskiness. Risk reduction is then achieved by selectively reducing investment exposures to the highest-ranked scenarios. The approach is asserted to operate without explicit risk measurement or minimization. Validity is supported by a real-data experiment showing that the resulting portfolios exhibit lower out-of-sample return variability than benchmark portfolios constructed by minimizing standard risk measures, while preserving average returns and Sharpe ratios with limited active management.

Significance. If the empirical results are robust, the work could offer a practical alternative to traditional mean-variance or spectral-risk optimization by providing a direct ordering of scenarios from the return matrix spectrum. The full-spectrum generalization is a potentially useful technical extension of classical matrix condition numbers. However, the central philosophical claim—that meaningful risk reduction occurs without risk measurement—is weakened because the proposed ordering is itself derived from eigenvalue/singular-value information that quantifies return variability and linear dependence, information already exploited by variance, PCA, and condition-number-based risk measures. The experiment's value hinges on whether the out-of-sample improvements are statistically and economically meaningful beyond what simpler de-risking heuristics achieve.

major comments (3)

- [Abstract / Proposed generalization] Abstract and the section describing the proposed generalization: the claim that the method achieves risk reduction 'without relying on risk measurement' is not substantiated. The generalized numerical rank/condition number is constructed directly from the spectrum of the return matrix; this spectrum encodes precisely the magnitude and structure of return variability that standard risk measures (variance, covariance eigenvalues, condition number) extract. The distinction therefore appears definitional rather than operational, and the paper does not demonstrate that an equivalent ordering could be obtained without any spectral or variability information.

- [Empirical validation] The real-data experiment section: the abstract states that out-of-sample variability is lower than for benchmarks minimizing standard risk measures, yet no quantitative results (e.g., percentage reductions in volatility or VaR, number of assets/scenarios, out-of-sample window lengths, or statistical tests) are provided in the summary description. Without these details, it is impossible to assess whether the reported improvement is load-bearing for the claim or could be explained by data selection, transaction-cost assumptions, or the limited-active-management constraint alone.

- [Empirical validation] The weakest assumption identified in the reader's note is not addressed: the paper must show that the full-spectrum ordering identifies genuinely riskier scenarios in a way that produces out-of-sample improvement beyond what would be obtained by any non-spectral heuristic (e.g., simple volatility ranking or random de-risking). No such falsification test or ablation is described.

minor comments (2)

- [Abstract] The abstract refers to 'a comprehensive experiment performed on real data' without naming the data source, asset universe, or sample period; these details should be stated explicitly even in the abstract for reproducibility.

- [Method] Notation for the generalized rank and condition number should be introduced with a clear mathematical definition (e.g., an explicit formula involving the full set of singular values) rather than a verbal description.

Simulated Author's Rebuttal

We thank the referee for the insightful comments and the recommendation for major revision. We address each of the major comments point by point below, offering clarifications and committing to revisions that strengthen the presentation of our results without altering the core contributions.

read point-by-point responses

-

Referee: [Abstract / Proposed generalization] Abstract and the section describing the proposed generalization: the claim that the method achieves risk reduction 'without relying on risk measurement' is not substantiated. The generalized numerical rank/condition number is constructed directly from the spectrum of the return matrix; this spectrum encodes precisely the magnitude and structure of return variability that standard risk measures (variance, covariance eigenvalues, condition number) extract. The distinction therefore appears definitional rather than operational, and the paper does not demonstrate that an equivalent ordering could be obtained without any spectral or variability information.

Authors: We appreciate this observation and agree that the spectrum inherently captures aspects of return variability. However, our approach differs operationally from traditional risk measurement in that it does not compute or optimize a scalar risk measure for the portfolio (such as variance or expected shortfall). Instead, the generalized condition number provides a direct ranking of scenarios based on their contribution to the matrix's spectral properties, enabling exposure reduction without formulating or solving a risk-minimization problem. This distinction is both philosophical—risk reduction via scenario de-emphasis rather than global optimization—and practical, as it avoids the need for estimating a full risk model for the adjusted portfolio. To clarify this, we will revise the abstract and the relevant methodological section to explicitly state that the method avoids explicit risk measurement and minimization of the portfolio, while acknowledging the use of spectral information for ranking. We will also include a brief comparison table or discussion highlighting differences from PCA-based or eigenvalue-only methods. revision: partial

-

Referee: [Empirical validation] The real-data experiment section: the abstract states that out-of-sample variability is lower than for benchmarks minimizing standard risk measures, yet no quantitative results (e.g., percentage reductions in volatility or VaR, number of assets/scenarios, out-of-sample window lengths, or statistical tests) are provided in the summary description. Without these details, it is impossible to assess whether the reported improvement is load-bearing for the claim or could be explained by data selection, transaction-cost assumptions, or the limited-active-management constraint alone.

Authors: We note that the referee's summary refers to the absence of quantitative results in the summary description, but the full manuscript's empirical validation section includes detailed quantitative results such as specific volatility reductions, dataset sizes, out-of-sample periods, and relevant statistical comparisons. To improve accessibility, we will revise the abstract to summarize key empirical findings, including the magnitude of out-of-sample variability reduction and the number of assets and scenarios used. We will also explicitly address assumptions like transaction costs and the limited active management in the revised text. revision: yes

-

Referee: [Empirical validation] The weakest assumption identified in the reader's note is not addressed: the paper must show that the full-spectrum ordering identifies genuinely riskier scenarios in a way that produces out-of-sample improvement beyond what would be obtained by any non-spectral heuristic (e.g., simple volatility ranking or random de-risking). No such falsification test or ablation is described.

Authors: We agree that demonstrating superiority over simpler heuristics strengthens the case for the full-spectrum approach. While the current benchmarks focus on standard risk-minimization techniques, which are more sophisticated than basic volatility ranking, we recognize the need for additional controls. In the revised manuscript, we will include an ablation study comparing our method against non-spectral heuristics, such as ranking scenarios by average individual asset volatility and random de-risking with the same number of adjustments. This will demonstrate that the improvement is not merely due to generic de-risking and provide the requested falsification test. revision: yes

Circularity Check

Central claim of risk reduction 'without measurement' reduces to definitional reclassification of the proposed spectral method

specific steps

-

self definitional

[Abstract]

"significant risk reduction can be achieved without relying on risk measurement and risk minimization. To this end, we propose a generalization of the numerical rank and the condition number of a matrix, specifically the return matrix in this application. This generalization considers the entire matrix spectrum instead of focusing only on the smallest eigenvalue, as the condition number does. The approach directly provides an order among a finite number of risky scenarios. Risk reduction is obtained by identifying the riskiest scenarios and reducing investment exposures corresponding to them."

The assertion that reduction occurs without measurement is supported by introducing a spectrum-based ordering of scenarios; since the spectrum directly encodes the magnitude and structure of return variability (the information standard risk measures extract), the 'without measurement' claim is true only by construction of reclassifying the proposed generalization as non-measurement while using it to decide which exposures to reduce.

full rationale

The paper's derivation begins from a definition of risk and asserts that reduction (not minimization) can be achieved without measurement, then immediately introduces a generalization of numerical rank/condition number on the return matrix that uses the full spectrum to rank and de-risk scenarios. This step is self-definitional: the mechanism for 'without measurement' is itself a direct spectral quantification of return variability and linear dependence, yet the claim holds only by defining the new generalization as outside the category of risk measurement. The subsequent real-data experiment compares out-of-sample variability against standard-risk-minimization benchmarks but does not test an ordering derived without any spectral information, leaving the central distinction definitional rather than independently derived. No equations, fitted parameters, or self-citations appear load-bearing in the provided text.

Axiom & Free-Parameter Ledger

axioms (1)

- standard math Standard properties of matrix eigenvalues, rank, and condition number from linear algebra

Reference graph

Works this paper leans on

-

[1]

David Allen, Colin Lizieri, and Stephen Satchell

URLhttps://www.imf.org/en/blogs/articles/2026/02/18/ stock-bond-diversification-offers-less-protection-from-market-selloffs. David Allen, Colin Lizieri, and Stephen Satchell. In defense of portfolio optimization: What if we can forecast?Financial Analysts Journal, 75(3):20–38,

2026

-

[2]

A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms

Victor DeMiguel, Lorenzo Garlappi, Francisco J Nogales, and Raman Uppal. A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms. Management science, 55(5):798–812, 2009a. Victor DeMiguel, Lorenzo Garlappi, and Raman Uppal. Optimal versus naive diversification: Howinefficientisthe1/nportfoliostrategy?The rev...

1915

-

[3]

Long-only equal risk contribution portfolios for cvar under discrete distributions.Quantitative Finance, 18(11):1927–1945,

Helmut Mausser and Oleksandr Romanko. Long-only equal risk contribution portfolios for cvar under discrete distributions.Quantitative Finance, 18(11):1927–1945,

1927

-

[4]

Financial protection against catastrophic risks: 2026 global assessment

OECD. Financial protection against catastrophic risks: 2026 global assessment. Report, Organ- isation for Economic Co-operation and Development,

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.