Recognition: no theorem link

Learning Polyhedral Conformal Sets for Robust Optimization

Pith reviewed 2026-05-12 01:37 UTC · model grok-4.3

The pith

Decision-aware conformal sets learn polyhedral uncertainty regions optimized for robust optimization loss while retaining finite-sample coverage.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

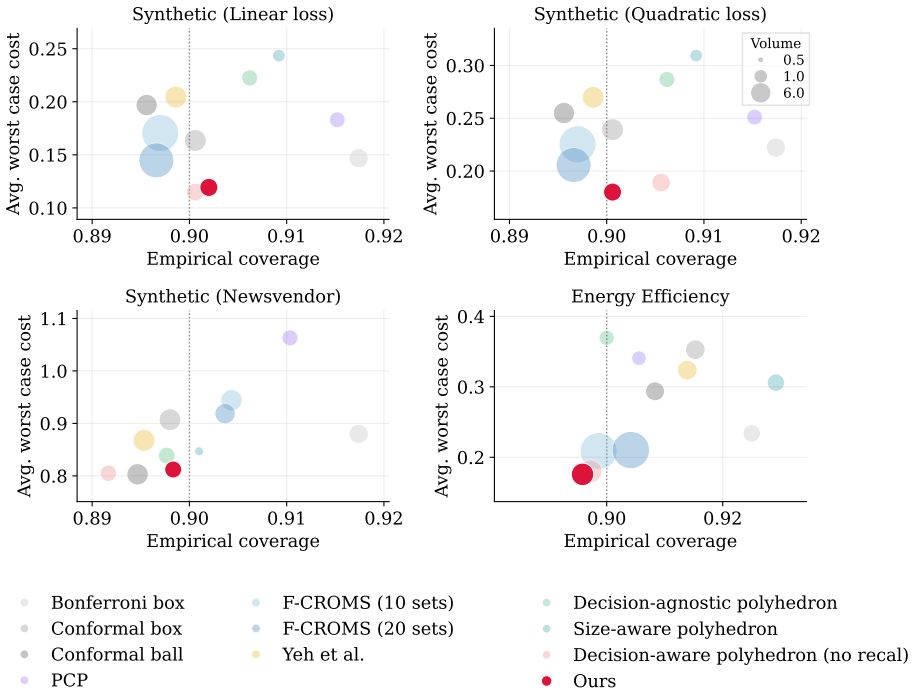

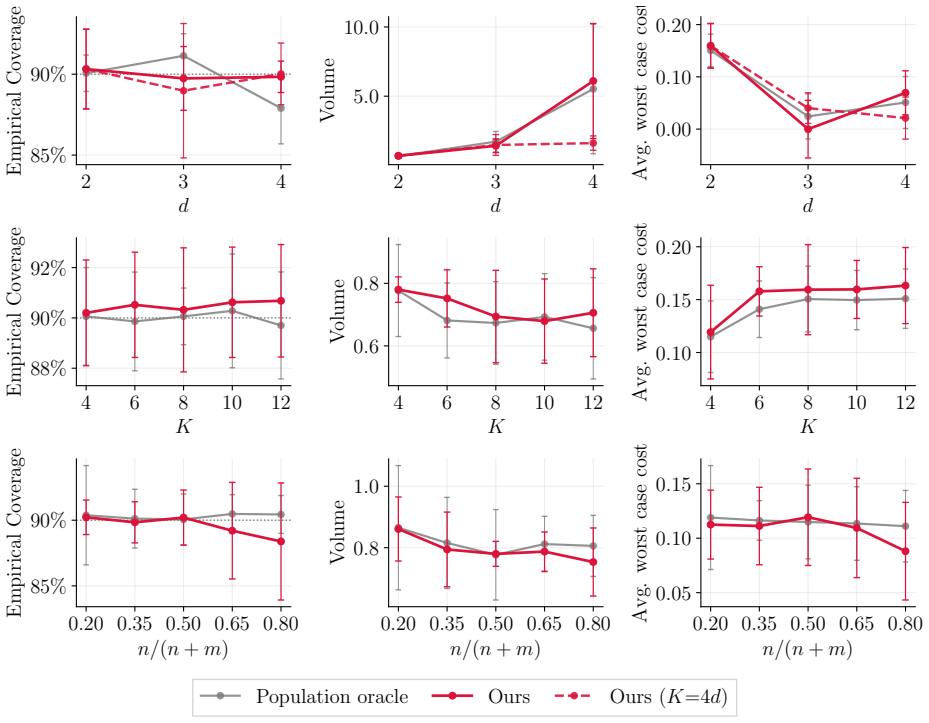

The authors show that polyhedral uncertainty sets can be parameterized by data-driven hyperplanes, their geometry learned by minimizing the robust loss they induce, and statistical validity restored through conformal calibration followed by re-calibration on an independent dataset; the resulting sets capture directional uncertainty aligned with the objective and deliver finite-sample coverage guarantees together with bounds on the sub-optimality gap to an oracle decision.

What carries the argument

Data-driven polyhedral uncertainty sets parameterized by hyperplanes and optimized to minimize the induced robust loss subject to conformal calibration and re-calibration.

If this is right

- The learned sets provide finite-sample coverage guarantees for the unknown true outcomes.

- They come with explicit upper bounds on the sub-optimality gap relative to the oracle robust solution.

- The sets remain computationally tractable inside standard robust optimization solvers.

- Uncertainty is represented anisotropically, stretching more in directions that matter most for the objective.

Where Pith is reading between the lines

- The same parameterization and calibration logic could be applied to other set families beyond polyhedra if the induced robust loss remains tractable.

- In inventory or portfolio problems the method would directly trade off stock-out risk against holding cost instead of using uniform safety margins.

- The approach suggests a general template for making any uncertainty-quantification technique decision-aware by inserting a loss-minimization step before calibration.

Load-bearing premise

The re-calibration step on an independent dataset restores the coverage guarantees after the data-dependent selection of the sets via optimization.

What would settle it

A numerical check in which the empirical coverage on fresh data falls below the nominal level even after the prescribed re-calibration step, or the realized sub-optimality gap exceeds the derived bound.

Figures

read the original abstract

Robust optimization (RO) provides a principled framework for decision-making under uncertainty, but its performance critically depends on the choice of the uncertainty set. While large sets ensure reliability, they often lead to overly conservative decisions, whereas small sets risk excluding the true outcome. Recent data-driven approaches, particularly conformal prediction, offer finite-sample validity guarantees but remain largely task-agnostic, ignoring the downstream decision structure. In this paper, we propose a decision-aware conformal framework that learns uncertainty sets tailored to robust optimization objectives. Our approach parameterizes a flexible family of polyhedral sets via data-driven hyperplanes and learns their geometry by directly minimizing the induced robust loss, while preserving statistical validity through conformal calibration. To correct for data-dependent selection, we incorporate a re-calibration step on an independent dataset to restore coverage. The resulting sets capture directional and anisotropic uncertainty aligned with the decision objective while remaining computationally tractable. We provide finite-sample coverage guarantees and bounds on the sub-optimality gap to an oracle decision. This work bridges the gap between statistical validity and decision optimality, providing a principled framework for data-driven robust optimization.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a decision-aware conformal framework for robust optimization that learns polyhedral uncertainty sets by optimizing data-driven hyperplanes to minimize the induced robust loss, followed by a re-calibration step on an independent dataset to restore finite-sample coverage guarantees, and derives bounds on the sub-optimality gap relative to an oracle decision.

Significance. If the finite-sample coverage guarantees hold, the work meaningfully advances data-driven robust optimization by aligning uncertainty sets with the downstream decision objective rather than using task-agnostic sets, which could reduce conservatism while preserving reliability. Credit is given for providing explicit finite-sample coverage guarantees and sub-optimality bounds, which supply a clear theoretical contribution.

major comments (1)

- [Re-calibration step and Theorem on coverage] The re-calibration procedure (described after the optimization step in the abstract and detailed in the construction of the sets): the claim that an independent dataset restores exact finite-sample coverage after data-dependent selection of the polyhedral sets via minimization of the robust loss is load-bearing for the central coverage guarantee and the derived sub-optimality bounds. The standard exchangeability argument for split conformal prediction does not automatically apply because the hyperplane coefficients (and thus the set geometry) are fitted on the first dataset, which can induce dependence that affects the calibration scores on the second dataset. A rigorous proof or explicit condition under which exchangeability is preserved is needed.

minor comments (2)

- [Section 3] The parameterization of the polyhedral sets via hyperplanes could be clarified with an explicit equation showing how the coefficients enter the robust loss objective.

- [Figures] Figure captions should explicitly state whether the visualized sets are before or after re-calibration to aid interpretation.

Simulated Author's Rebuttal

We thank the referee for the careful review and for identifying the need to clarify the coverage argument. We address the major comment point by point below.

read point-by-point responses

-

Referee: [Re-calibration step and Theorem on coverage] The re-calibration procedure (described after the optimization step in the abstract and detailed in the construction of the sets): the claim that an independent dataset restores exact finite-sample coverage after data-dependent selection of the polyhedral sets via minimization of the robust loss is load-bearing for the central coverage guarantee and the derived sub-optimality bounds. The standard exchangeability argument for split conformal prediction does not automatically apply because the hyperplane coefficients (and thus the set geometry) are fitted on the first dataset, which can induce dependence that affects the calibration scores on the second dataset. A rigorous proof or explicit condition under which exchangeability is preserved is needed.

Authors: The standard split-conformal argument does apply once the sets are fixed. The first dataset is used solely to optimize the hyperplane coefficients, after which the resulting polyhedral set is held fixed. The second (independent) dataset is then used only to compute nonconformity scores with respect to this fixed set. Because the calibration points and any future test point are i.i.d. and independent of the first dataset, their scores are exchangeable conditionally on the realized set. This is exactly the split-conformal setting, so the quantile threshold yields exact finite-sample coverage conditionally on the learned set (and therefore unconditionally). We will add a short remark in Section 3.2 explicitly stating this conditional exchangeability and noting that the sub-optimality bounds inherit the same guarantee. revision: partial

Circularity Check

No significant circularity detected in derivation chain

full rationale

The paper learns polyhedral sets by minimizing a robust loss on one dataset, then applies conformal calibration and re-calibration on an independent held-out dataset to obtain finite-sample coverage. The coverage guarantee and sub-optimality bounds are derived from standard split-conformal arguments applied after the re-calibration step, rather than being equivalent to the optimization objective by construction. No self-definitional equations, fitted parameters renamed as predictions, load-bearing self-citations, or ansatz smuggling appear in the abstract or described framework. The derivation remains self-contained against external conformal validity results.

Axiom & Free-Parameter Ledger

free parameters (1)

- hyperplane coefficients

axioms (2)

- domain assumption Data points are exchangeable for conformal prediction to hold

- ad hoc to paper The re-calibration on independent data restores exact coverage

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.