Recognition: 2 theorem links

· Lean TheoremOn the Possibility of Informationally Inefficient Markets Without Noise

Pith reviewed 2026-05-12 01:50 UTC · model grok-4.3

The pith

Non-exponential preferences cause only partial information revelation through prices even without noise traders.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

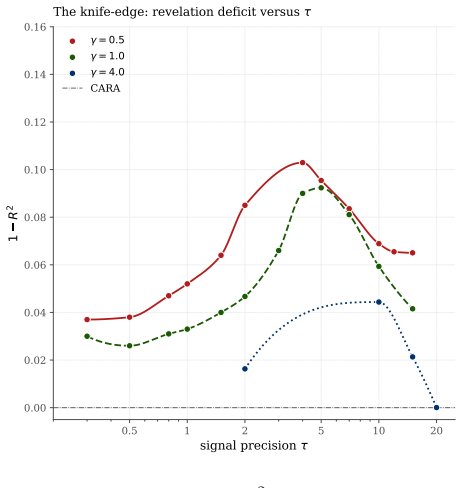

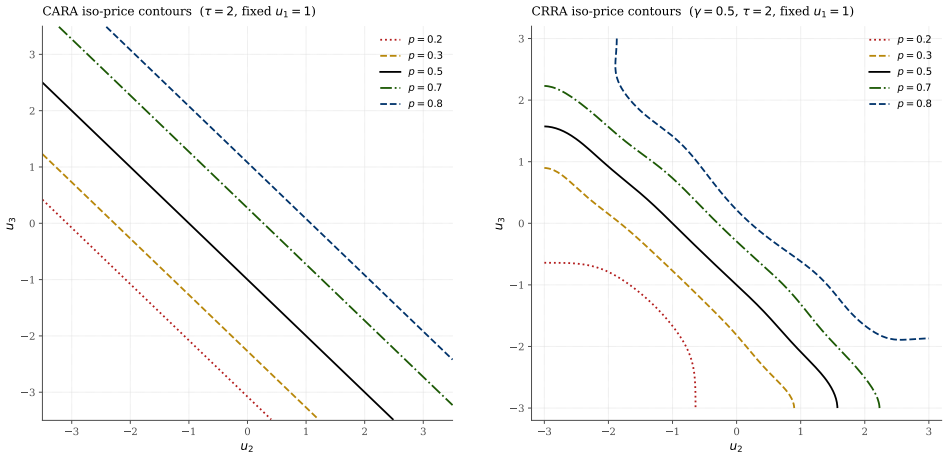

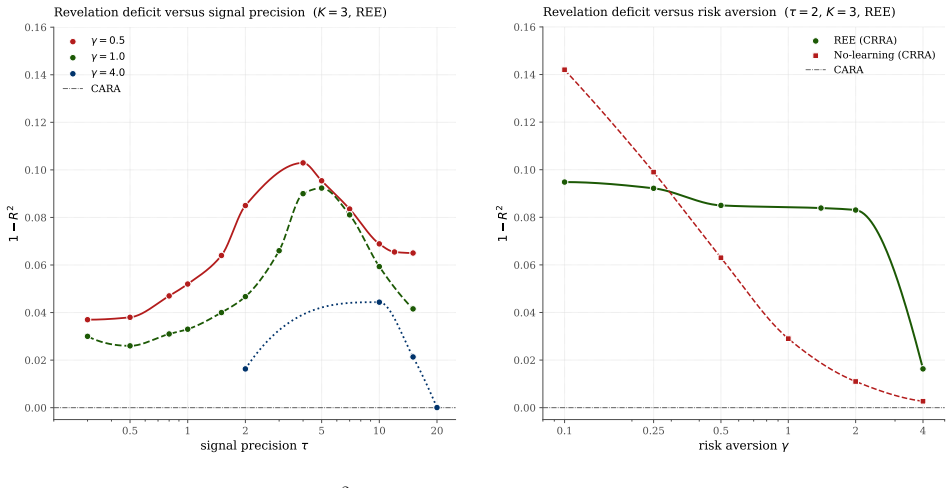

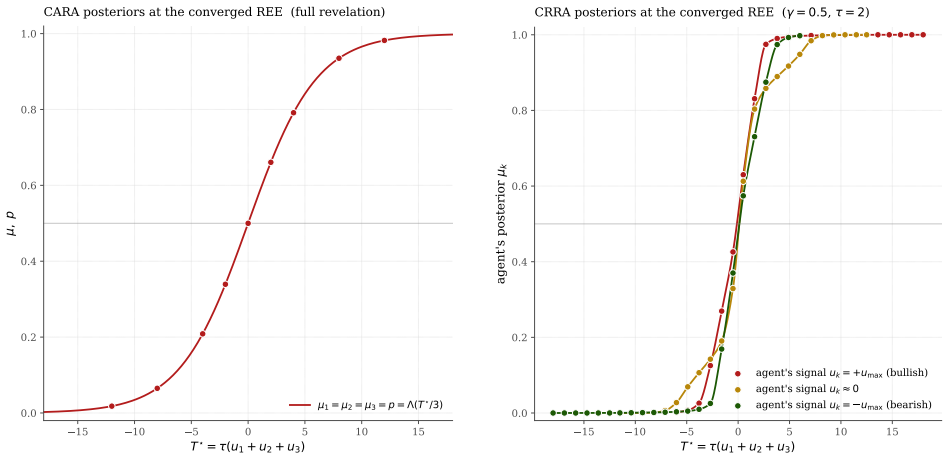

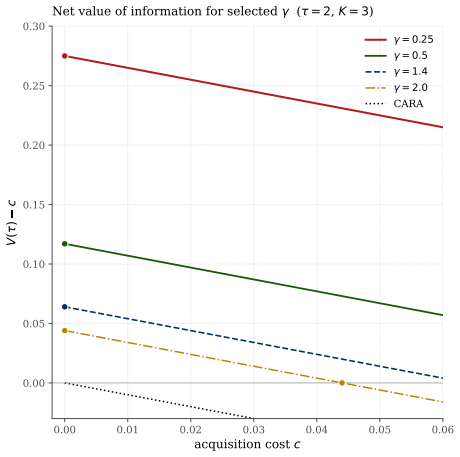

Under any non-exponential expected utility preference, including CRRA, the rational expectations equilibrium price only partially reveals the aggregate private information because market clearing aggregates signals differently from the Bayesian sufficient statistic; the resulting Jensen gap prevents full revelation. CARA is the unique preference class that produces linear demand in log-odds and therefore full revelation. The equilibrium is characterized by a contour integration fixed point, and numerical solutions for CRRA confirm that partial revelation, positive trade volume, and positive value of information all survive learning from prices.

What carries the argument

The mismatch between the space in which market clearing aggregates individual demands and the space of the Bayesian sufficient statistic for the asset payoff.

If this is right

- Information acquisition retains strictly positive value in equilibrium.

- Equilibrium trade volume stays positive with zero exogenous noise.

- Partial revelation continues to hold when agents update beliefs from the observed price.

- Only constant absolute risk aversion preferences produce fully revealing prices.

Where Pith is reading between the lines

- Preference heterogeneity by itself can sustain persistent information asymmetry in otherwise rational markets.

- Changes in effective risk aversion, for instance through regulation or contract design, could alter how much information prices convey.

- Empirical work could test whether cross-sectional variation in measured risk aversion predicts differences in price informativeness across assets.

Load-bearing premise

That market clearing aggregates signals in a space distinct enough from the Bayesian sufficient statistic to produce a material Jensen gap for non-CARA utilities.

What would settle it

A closed-form or numerical demonstration that the rational expectations price is a sufficient statistic for the full vector of private signals under CRRA preferences would falsify the partial-revelation claim.

Figures

read the original abstract

Noise traders can be dispensed with entirely. Partial revelation of information through prices arises under any non-exponential expected utility preference, including CRRA, without noise traders, random endowments, supply shocks, hedging motives, or behavioral biases. The model contains zero exogenous noise. The mechanism is a mismatch between the space in which market clearing aggregates signals and the Bayesian sufficient statistic. CARA demand is linear in log-odds, so prices aggregate in log-odds space and reveal the statistic exactly. Every other preference aggregates differently; the resulting Jensen gap makes revelation partial. I prove that CARA is the unique fully revealing preference class, characterize the rational expectations equilibrium via a contour integration fixed point, and verify that partial revelation survives learning from prices. The Grossman-Stiglitz paradox is resolved: information acquisition has positive value within the rational class. Numerical solution of the rational expectations fixed point at K = 3 confirms partial revelation, positive trade volume, and positive value of information across the full range of CRRA risk aversion, vanishing only in the CARA limit.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that partially revealing rational expectations equilibria (REE) can exist in markets with zero exogenous noise when agents have non-CARA vNM preferences (e.g., CRRA). Market clearing aggregates signals in a space that differs from the Bayesian sufficient statistic, producing a Jensen gap that prevents full revelation except for the CARA class, which is proved unique. The REE is characterized as the fixed point of a contour-integration operator on candidate price functions; partial revelation, positive trade volume, and positive value of information are verified numerically for CRRA at K=3 signals across risk-aversion values, with the result vanishing only in the CARA limit.

Significance. If the fixed-point characterization and uniqueness proof hold, the result supplies a preference-based mechanism for informational inefficiency and resolves the Grossman-Stiglitz paradox without invoking noise traders, random endowments, or behavioral biases. The contour-integration approach and numerical confirmation for CRRA utilities would constitute a technically novel contribution to the theory of REE.

major comments (2)

- The existence and stability of the contour-integration fixed point for non-CARA utilities is load-bearing for the central claim of partial revelation under any non-exponential preference. The abstract asserts analytic characterization and that the fixed point lies strictly inside the non-revealing set, yet supplies only a numerical solution at K=3; without an analytic proof of existence (e.g., via contractivity of the operator or verification that the required analytic continuation exists for general K and risk-aversion parameters), the result may fail to generalize and the partial-revelation conclusion collapses.

- The uniqueness proof that CARA is the only fully revealing class rests on showing that only linear aggregation in log-odds space coincides with the Bayesian sufficient statistic. The manuscript must explicitly rule out other non-CARA utilities for which the demand aggregation happens to produce a zero Jensen gap (or for which the contour-integral operator admits the fully revealing map as a fixed point), as this would constitute a counterexample to the claimed uniqueness.

minor comments (2)

- The abstract states that partial revelation 'survives learning from prices,' but the precise updating rule and the sense in which the fixed point remains stable under iterative learning should be stated more explicitly.

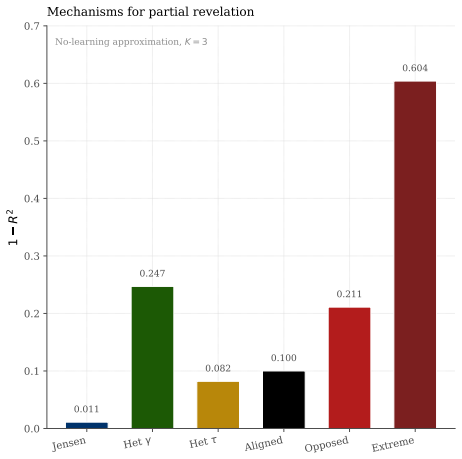

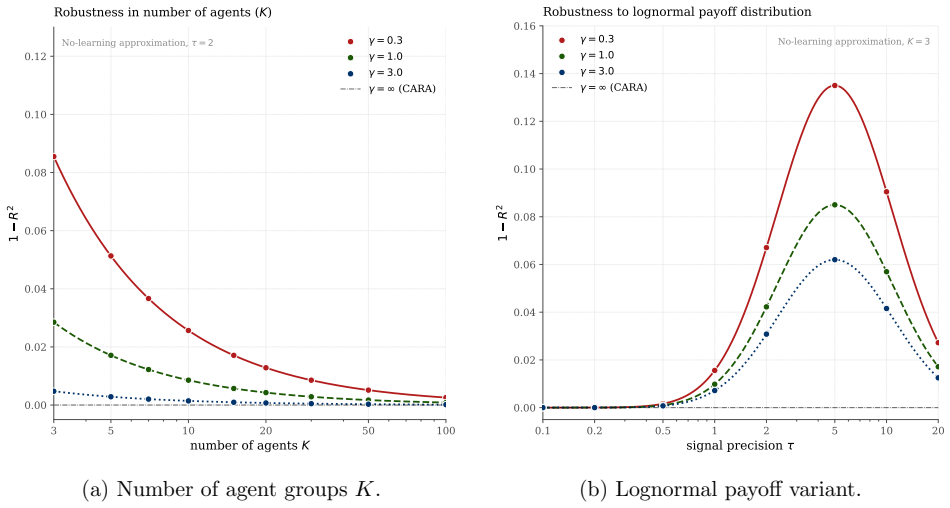

- Numerical results are reported only for K=3; a brief table or figure showing sensitivity to higher K (or to the CRRA coefficient) would strengthen the verification without altering the main argument.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on our manuscript. We address each major comment point by point below. We agree that additional analytic support for the fixed-point characterization would strengthen the paper and will revise accordingly, while maintaining that the existing numerical evidence and uniqueness argument are robust for the cases considered.

read point-by-point responses

-

Referee: The existence and stability of the contour-integration fixed point for non-CARA utilities is load-bearing for the central claim of partial revelation under any non-exponential preference. The abstract asserts analytic characterization and that the fixed point lies strictly inside the non-revealing set, yet supplies only a numerical solution at K=3; without an analytic proof of existence (e.g., via contractivity of the operator or verification that the required analytic continuation exists for general K and risk-aversion parameters), the result may fail to generalize and the partial-revelation conclusion collapses.

Authors: We appreciate the referee's emphasis on this foundational aspect. The manuscript analytically characterizes the REE as the fixed point of the contour-integration operator and establishes partial revelation numerically for K=3 across CRRA risk-aversion values. We agree that a general analytic proof of existence and stability (including contractivity or analytic continuation for arbitrary K) is not supplied and would be valuable. In revision, we will add a dedicated subsection analyzing the operator's mapping properties on suitable function spaces, provide conditions under which contractivity holds for non-CARA utilities, and explicitly bound the scope of the K=3 numerical verification while noting that generalization remains an open direction. revision: partial

-

Referee: The uniqueness proof that CARA is the only fully revealing class rests on showing that only linear aggregation in log-odds space coincides with the Bayesian sufficient statistic. The manuscript must explicitly rule out other non-CARA utilities for which the demand aggregation happens to produce a zero Jensen gap (or for which the contour-integral operator admits the fully revealing map as a fixed point), as this would constitute a counterexample to the claimed uniqueness.

Authors: We agree that the uniqueness result benefits from explicit exclusion of potential counterexamples. The proof shows that full revelation requires the market-clearing aggregation to recover the Bayesian sufficient statistic exactly, which occurs if and only if individual demands are linear in log-odds—a property that holds solely for the CARA class. For non-CARA utilities the resulting nonlinearity generates a nonzero Jensen gap. In the revision we will strengthen the uniqueness theorem with an additional lemma that directly rules out other vNM preference classes capable of producing a zero gap or admitting the fully revealing price as a fixed point of the contour operator, by deriving the necessary functional form of demand from the zero-gap condition. revision: yes

Circularity Check

No circularity; derivation follows from model primitives and fixed-point characterization

full rationale

The paper establishes that CARA utility yields linear demand in log-odds space, so market clearing aggregates exactly to the Bayesian sufficient statistic, while non-CARA preferences (including CRRA) induce a Jensen gap due to nonlinear aggregation. It proves uniqueness of the CARA class for full revelation and characterizes the REE as the fixed point of a contour-integral operator derived directly from the market-clearing condition and demand functions. The K=3 numerical solution verifies existence and partial revelation for CRRA but does not constitute the source of the claim; the result is obtained by solving the model's own equations rather than by fitting parameters or renaming inputs. No self-citations appear load-bearing, and no step reduces the central partial-revelation result to a pre-defined quantity by construction.

Axiom & Free-Parameter Ledger

free parameters (1)

- CRRA risk aversion coefficient

axioms (2)

- domain assumption Traders maximize expected utility of wealth

- domain assumption Rational expectations equilibrium exists and is characterized by a fixed-point condition

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel echoesTheorem 1 (CARA uniqueness for log-odds-linear demand). ... Suppose the optimal demand admits ... x⋆(μ,p,W)=[logitμ−logitp]/α(p,W). Then U is CARA ... U(W)=a−b exp(−α0 W)

-

IndisputableMonolith/Cost.leanJcost_pos_of_ne_one / convexity properties echoesthe probability average of a logistic transform is not the logistic transform of the average ... Jensen gap ... is the size of the revelation failure

Reference graph

Works this paper leans on

-

[1]

Information aggregation with asymmetric asset payoffs

Elias Albagli, Christian Hellwig, and Aleh Tsyvinski. Information aggregation with asymmetric asset payoffs. Journal of Finance, 79 0 (4): 0 2715--2758, 2024

work page 2024

-

[2]

Beauty contests and iterated expectations in asset markets

Franklin Allen, Stephen Morris, and Hyun Song Shin. Beauty contests and iterated expectations in asset markets. Review of Financial Studies, 19 0 (3): 0 719--752, 2006

work page 2006

-

[3]

Rational panics and stock market crashes

Gadi Barlevy and Pietro Veronesi. Rational panics and stock market crashes. Journal of Economic Theory, 110 0 (2): 0 234--263, 2003

work page 2003

-

[4]

Insiders, outsiders, and market breakdowns

Utpal Bhattacharya and Matthew Spiegel. Insiders, outsiders, and market breakdowns. Review of Financial Studies, 4 0 (2): 0 255--282, 1991

work page 1991

-

[5]

Fischer Black. Noise. Journal of Finance, 41 0 (3): 0 529--543, 1986

work page 1986

-

[6]

On existence and uniqueness of equilibrium in a class of noisy rational expectations models

Bradyn Breon-Drish. On existence and uniqueness of equilibrium in a class of noisy rational expectations models. Review of Economic Studies, 82 0 (3): 0 868--921, 2015

work page 2015

-

[7]

Matthijs Breugem and Adrian Buss. Institutional investors and information acquisition: Implications for asset prices and informational efficiency. Working paper, Nyenrode Business University and INSEAD, 2019

work page 2019

-

[8]

Scott Condie and Jayant V. Ganguli. Ambiguity and rational expectations equilibria. The Review of Economic Studies, 78 0 (3): 0 821--845, 2011. doi:10.1093/restud/rdq032

-

[9]

Bradford De Long, Andrei Shleifer, Lawrence H

J. Bradford De Long, Andrei Shleifer, Lawrence H. Summers, and Robert J. Waldmann. Noise trader risk in financial markets. Journal of Political Economy, 98 0 (4): 0 703--738, 1990

work page 1990

-

[10]

Peter M. DeMarzo and Costis Skiadas. Aggregation, determinacy, and informational efficiency for a class of economies with asymmetric information. Journal of Economic Theory, 80 0 (1): 0 123--152, 1998

work page 1998

-

[11]

Douglas W. Diamond and Robert E. Verrecchia. Information aggregation in a noisy rational expectations economy. Journal of Financial Economics, 9 0 (3): 0 221--235, 1981

work page 1981

-

[12]

Lawrence R. Glosten and Paul R. Milgrom. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics, 14 0 (1): 0 71--100, 1985

work page 1985

-

[13]

Sanford J. Grossman and Joseph E. Stiglitz. On the impossibility of informationally efficient markets. American Economic Review, 70 0 (3): 0 393--408, 1980

work page 1980

-

[14]

Aviad Heifetz and Heracles M. Polemarchakis. Partial revelation with rational expectations. Journal of Economic Theory, 80 0 (1): 0 171--181, 1998. doi:10.1006/jeth.1998.2391

-

[15]

Martin F. Hellwig. On the aggregation of information in competitive markets. Journal of Economic Theory, 22 0 (3): 0 477--498, 1980

work page 1980

-

[16]

Kenneth Kasa, Todd B. Walker, and Charles H. Whiteman. Heterogeneous beliefs and tests of present value models. Review of Economic Studies, 81 0 (3): 0 1137--1163, 2014

work page 2014

-

[17]

Albert S. Kyle. Continuous auctions and insider trading. Econometrica, 53 0 (6): 0 1315--1335, 1985

work page 1985

-

[18]

Albert S. Kyle. Informed speculation with imperfect competition. Review of Economic Studies, 56 0 (3): 0 317--355, 1989

work page 1989

-

[19]

Asymmetric stock market volatility and the cyclical behavior of expected returns

Antonio Mele. Asymmetric stock market volatility and the cyclical behavior of expected returns. Journal of Financial Economics, 86 0 (2): 0 446--478, 2007

work page 2007

-

[20]

Information, trade and common knowledge

Paul Milgrom and Nancy Stokey. Information, trade and common knowledge. Journal of Economic Theory, 26 0 (1): 0 17--27, 1982

work page 1982

-

[21]

Wealth, information acquisition, and portfolio choice

Joel Peress. Wealth, information acquisition, and portfolio choice. Review of Financial Studies, 17 0 (3): 0 879--914, 2004

work page 2004

-

[22]

Informed speculation and hedging in a noncompetitive securities market

Matthew Spiegel and Avanidhar Subrahmanyam. Informed speculation and hedging in a noncompetitive securities market. Review of Financial Studies, 5 0 (2): 0 307--329, 1992

work page 1992

- [23]

-

[24]

Strategic supply function competition with private information

Xavier Vives. Strategic supply function competition with private information. Econometrica, 79 0 (6): 0 1919--1966, 2011

work page 1919

-

[25]

A model of intertemporal asset prices under asymmetric information

Jiang Wang. A model of intertemporal asset prices under asymmetric information. Review of Economic Studies, 60 0 (2): 0 249--282, 1993

work page 1993

-

[26]

A model of competitive stock trading volume

Jiang Wang. A model of competitive stock trading volume. Journal of Political Economy, 102 0 (1): 0 127--168, 1994

work page 1994

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.