Recognition: no theorem link

The P behind Q: Empirical Evidence from Physical Drift in Put-Call Parity

Pith reviewed 2026-05-13 03:08 UTC · model grok-4.3

The pith

Physical drift enters the put-call parity carry gap through capital-cost channels in margin enforcement.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Put-call parity is an exact terminal-payoff identity, yet its market enforcement is path-dependent and capital-using. Extending the GBM implementation-risk term adds an (r μ τ) component to the standard (r σ √τ) path-risk component. With μ measured by a lagged rolling-OLS trend proxy that is not interpreted as an observed expected return, the extended specification improves both in-sample and leave-one-year-out fit to the annualized carry gap between option-implied and OIS-implied discounting, especially for SPX European index options. This pattern is consistent with drift-sensitive margin burden in parity enforcement rather than a failure of no-arbitrage.

What carries the argument

Drift-preserving extension of the GBM implementation-risk term that adds an (r μ τ) component to the standard (r σ √τ) path-risk component, with μ proxied by lagged rolling-OLS trend.

If this is right

- The drift term improves explanatory power for the carry gap in both in-sample estimation and leave-one-year-out validation.

- The fit gain is larger for SPX options than for RUT options.

- The evidence favors a margin-burden interpretation over a no-arbitrage violation.

- Parity deviations should be assessed with explicit allowance for physical drift when capital constraints bind.

Where Pith is reading between the lines

- Option pricing and risk models used by dealers may need to embed physical-measure drift when calibrating to capital-constrained markets.

- Analogous drift-sensitive capital costs could appear in other leveraged arbitrage trades such as futures basis or convertible arbitrage.

- Repeating the test on single-stock options or around earnings events would test whether the channel strengthens with higher effective leverage.

Load-bearing premise

The lagged rolling-OLS trend proxy for physical drift accurately captures the relevant capital-cost channel without contamination from the carry-gap data or from other omitted factors.

What would settle it

Finding no improvement or a deterioration in fit when the drift term is added, especially in leave-one-year-out validation on SPX options, would falsify the claim that physical drift contributes to the carry gap via margin costs.

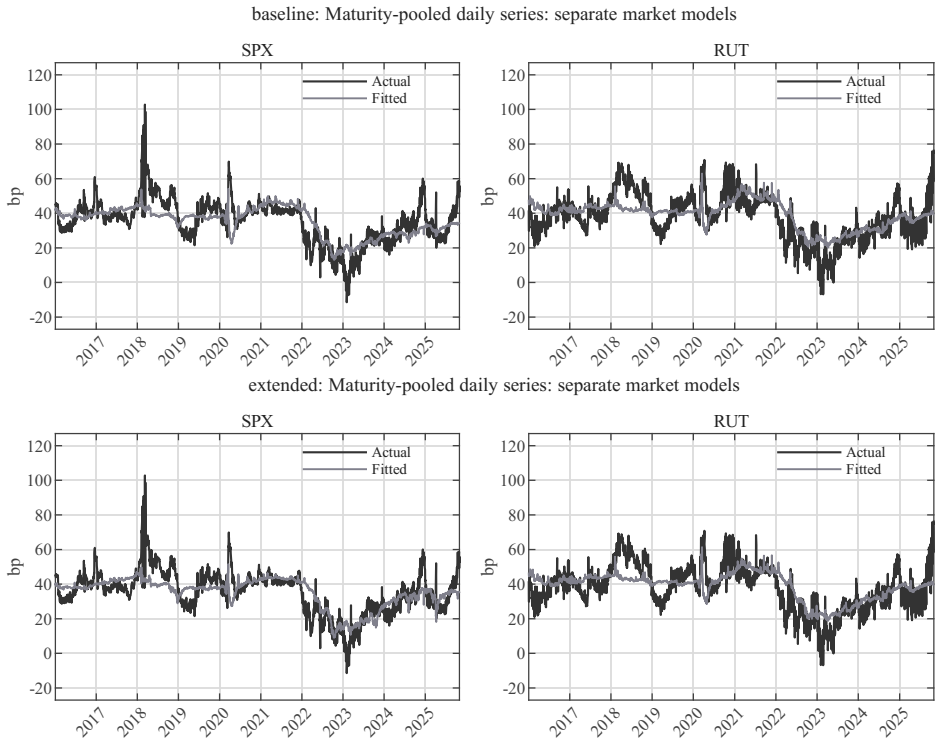

Figures

read the original abstract

Put-call parity is exact as a terminal-payoff identity, yet its market enforcement is path-dependent and capital-using. This paper examines whether physical-measure drift is reflected in the carry gap, defined as the annualized wedge between option-implied and OIS-implied discounting, using SPX and RUT European index options. I derive a drift-preserving extension of the GBM implementation-risk term that adds an (r\mu\tau) component to the standard (r\sigma\sqrt{\tau}) path-risk component. The drift input (\mu) is measured by a lagged rolling-OLS trend proxy and should not be interpreted as an observed expected return. Empirically, the drift term improves both in-sample and leave-one-year-out fit, especially for SPX, consistent with drift-sensitive margin burden in parity enforcement rather than a failure of no-arbitrage.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript claims that put-call parity enforcement for SPX and RUT European index options reflects physical-measure drift through capital costs. It derives a GBM-based extension to the implementation-risk term that augments the standard (r σ √τ) path-risk component with an additional (r μ τ) drift term. Using a lagged rolling-OLS trend proxy for μ (explicitly not to be read as an observed expected return), the paper reports that inclusion of the drift term improves both in-sample and leave-one-year-out fit to the carry gap (annualized wedge between option-implied and OIS-implied discounting), especially for SPX, and interprets this as evidence of drift-sensitive margin burden rather than a no-arbitrage violation.

Significance. If the reported fit improvements prove robust, the work supplies a concrete, falsifiable channel linking physical drift to path-dependent capital costs in parity enforcement, offering a bridge between P- and Q-measure dynamics in a capital-constrained setting. The lagged proxy and leave-one-year-out validation are positive design choices that reduce direct data overlap. The result, if confirmed, could inform implementation-risk modeling and margin calculations for index options.

major comments (3)

- [Empirical results] Empirical results (fit improvement claims): the abstract and results section report that the drift term improves in-sample and LOO fit but supply no statistical significance tests, standard errors, p-values, or confidence intervals on the incremental R² or coefficient. This is load-bearing for the central claim because, without these, it is impossible to determine whether the reported gain exceeds what would be expected from adding any single extra regressor.

- [Data and proxy construction] Measurement and proxy construction (data section): μ is obtained from lagged rolling-OLS on price data and then inserted into the carry-gap regression. While the lag avoids contemporaneous overlap, the manuscript provides no auxiliary regressions, orthogonalization, or placebo tests against volatility clustering, autocorrelation, or liquidity factors that could independently widen the option-OIS wedge. This directly affects whether the fit gain can be attributed specifically to the capital-cost channel.

- [§3, theoretical derivation] §3 (theoretical derivation), Eq. for extended implementation risk: the addition of the (r μ τ) term is presented as a drift-preserving GBM extension, yet the paper does not show the explicit steps from the SDE to the capital-cost integral or verify that the linear term survives under realistic margin rules (e.g., variation-margin timing or collateral haircuts). Without this, the economic mapping from physical drift to margin burden remains an assumption rather than a derived result.

minor comments (2)

- [Data section] Clarify the exact formula used to annualize the carry gap and confirm that dividend yields and borrowing costs are consistently subtracted in both the option-implied and OIS legs.

- [Introduction / proxy definition] The parenthetical remark that μ 'should not be interpreted as an observed expected return' is helpful; repeat or expand this caveat when the proxy is first introduced in the main text.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments, which help clarify the empirical and theoretical foundations of our work. We respond to each major point below and outline revisions to address the concerns raised.

read point-by-point responses

-

Referee: [Empirical results] Empirical results (fit improvement claims): the abstract and results section report that the drift term improves in-sample and LOO fit but supply no statistical significance tests, standard errors, p-values, or confidence intervals on the incremental R² or coefficient. This is load-bearing for the central claim because, without these, it is impossible to determine whether the reported gain exceeds what would be expected from adding any single extra regressor.

Authors: We agree that formal statistical tests are necessary to evaluate the incremental explanatory power. In the revised manuscript we will report bootstrap standard errors, p-values, and confidence intervals for both the incremental R² and the drift coefficient in the in-sample and leave-one-year-out specifications. These will be obtained via block bootstrap to preserve time-series dependence, allowing direct assessment of whether the fit gains exceed those expected from an additional regressor. revision: yes

-

Referee: [Data and proxy construction] Measurement and proxy construction (data section): μ is obtained from lagged rolling-OLS on price data and then inserted into the carry-gap regression. While the lag avoids contemporaneous overlap, the manuscript provides no auxiliary regressions, orthogonalization, or placebo tests against volatility clustering, autocorrelation, or liquidity factors that could independently widen the option-OIS wedge. This directly affects whether the fit gain can be attributed specifically to the capital-cost channel.

Authors: We will add a dedicated robustness subsection that includes (i) correlations and auxiliary regressions of the lagged μ proxy against realized volatility, bid-ask spreads, and other liquidity measures; (ii) orthogonalization of μ with respect to volatility clustering via residualization; and (iii) placebo regressions that replace the trend proxy with simulated random walks or permuted series. These checks will help isolate whether the documented fit improvement is attributable to the drift channel rather than confounding factors. revision: yes

-

Referee: [§3, theoretical derivation] §3 (theoretical derivation), Eq. for extended implementation risk: the addition of the (r μ τ) term is presented as a drift-preserving GBM extension, yet the paper does not show the explicit steps from the SDE to the capital-cost integral or verify that the linear term survives under realistic margin rules (e.g., variation-margin timing or collateral haircuts). Without this, the economic mapping from physical drift to margin burden remains an assumption rather than a derived result.

Authors: We will expand Section 3 with the full derivation from the GBM SDE through the integrated capital-cost process, explicitly showing how the (r μ τ) term emerges under continuous margining. We will also add a discussion of discrete margin rules, noting that the linear drift term is an approximation that holds exactly only under continuous variation margin and zero haircuts; we will include a brief robustness analysis under stylized discrete-margin assumptions to clarify the scope of the mapping. revision: yes

Circularity Check

No significant circularity: GBM derivation and lagged proxy are independent of carry-gap measurement

full rationale

The paper derives the (r μ τ) extension from standard GBM dynamics applied to implementation risk and then inserts a pre-computed, lagged rolling-OLS trend estimate of μ obtained solely from underlying index price returns. The target variable (carry gap) is constructed from option prices versus OIS rates, a distinct data source. Because the proxy for μ is neither fitted to the carry-gap series nor defined in terms of it, the reported in-sample and LOO fit improvements are not forced by construction. No self-citation chain, ansatz smuggling, or renaming of known results is present in the provided text; the central claim therefore remains an independent empirical test.

Axiom & Free-Parameter Ledger

free parameters (1)

- mu (physical drift proxy)

axioms (2)

- domain assumption Put-call parity holds exactly as a terminal-payoff identity

- domain assumption The GBM implementation-risk term can be extended by a linear drift component while preserving its structure

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.