Mean-Variance Optimization in Ambiguous Financial Markets with Learning

Pith reviewed 2026-06-27 10:47 UTC · model grok-4.3

The pith

Ambiguity-averse investors using a decomposed mean-variance criterion optimally reduce holdings in risky assets when drifts are uncertain but learnable from a prior distribution.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

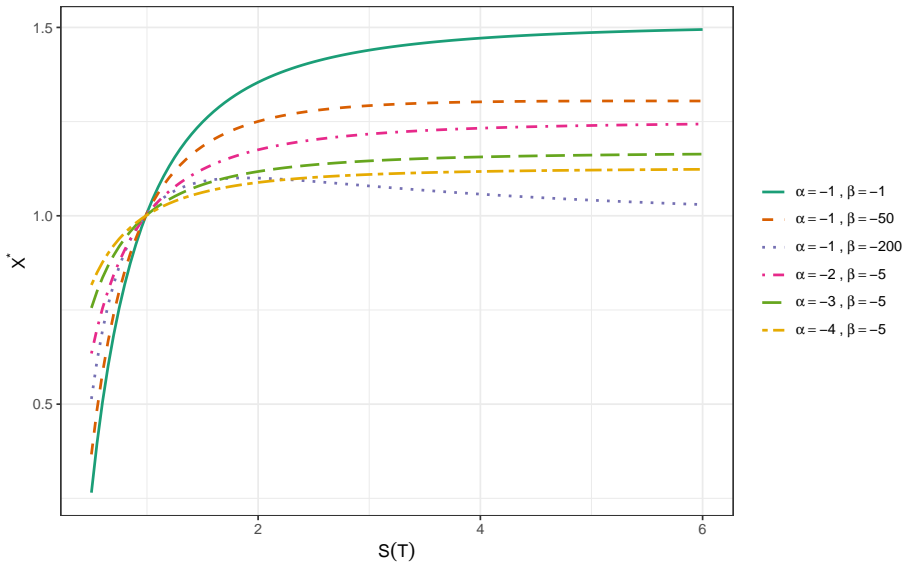

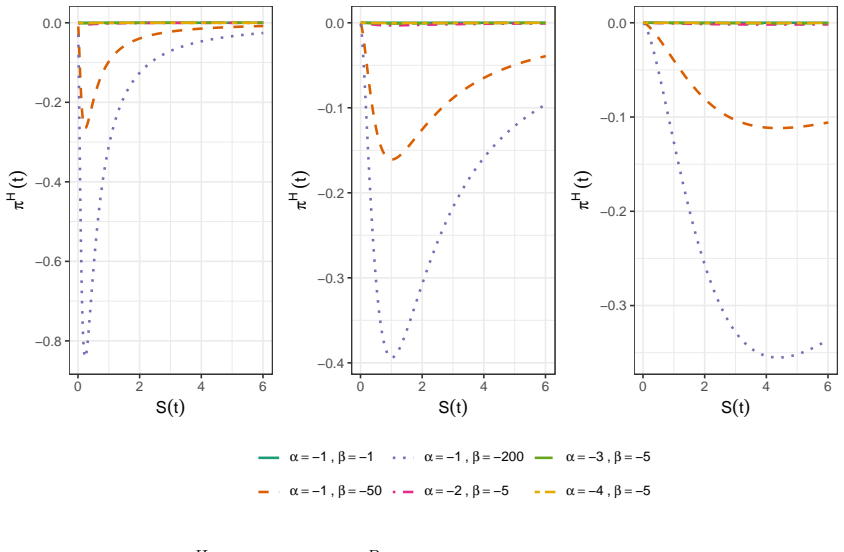

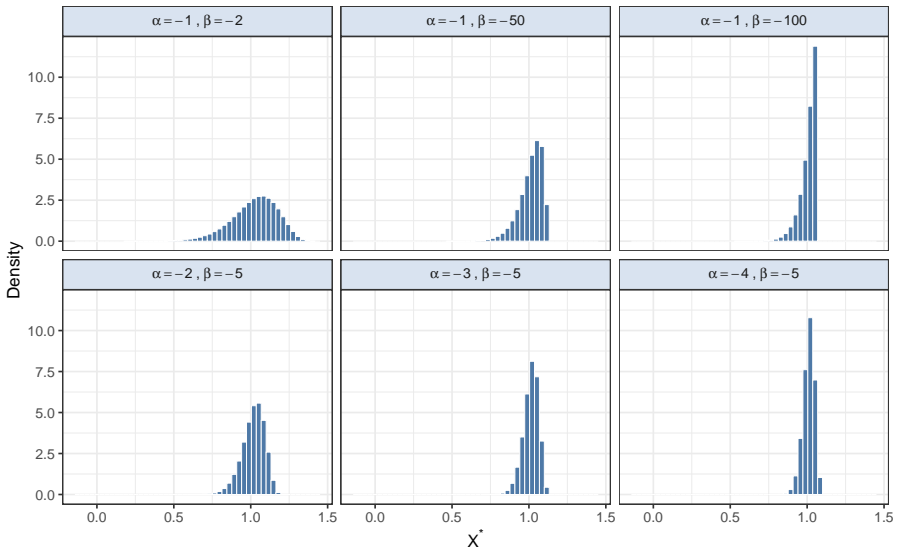

In a Black-Scholes market with unknown drifts endowed with a prior, an ambiguity-averse agent who maximizes the Maccheroni-style mean-variance criterion (in which variance is additively decomposed and each term receives its own penalty) obtains an optimal investment process that is adapted to the filtration generated by the asset prices and that updates beliefs continuously; this process allocates less wealth to risky assets than the corresponding ambiguity-neutral strategy, with the reduction increasing in the ambiguity-aversion parameter.

What carries the argument

The Maccheroni et al. 2013 mean-variance criterion that decomposes terminal-wealth variance into a market-risk component and a model-ambiguity component, each penalized at its own rate, together with Bayesian updating of the drift prior inside the dynamic optimization.

If this is right

- The optimal strategy is fully dynamic and updates continuously with new price observations.

- Comparative statics show that the reduction in risky-asset holdings scales directly with the ambiguity-aversion weight.

- The same framework produces explicit dependence of the strategy on the parameters of the drift prior.

- Numerical experiments confirm that the qualitative reduction holds across a range of market parameters.

Where Pith is reading between the lines

- The same learning-plus-ambiguity structure could be applied to other terminal-wealth criteria such as expected utility or shortfall risk.

- Regulators or portfolio platforms could embed the decomposed-variance objective to generate conservative dynamic allocations under parameter uncertainty.

- Empirical tests could compare the model's predicted allocation paths against observed behavior of funds that publicly disclose ambiguity-averse mandates.

Load-bearing premise

The specific decomposition and differential weighting of variance in the chosen mean-variance objective correctly represents the investor's separate attitudes toward market risk and model ambiguity.

What would settle it

A simulation or market dataset in which investors with higher ambiguity aversion (higher weight on the ambiguity component) do not exhibit smaller risky-asset positions than investors with lower ambiguity aversion, once learning and the prior are accounted for.

Figures

read the original abstract

We consider a continuous time investment problem in a multi-asset Black-Scholes market with the following features: The assets' drifts are not known and constitute a source of model ambiguity. However, there is a prior distribution (knowledge) on the possible drifts. Our investor is ambiguity averse and wants to maximize a mean-variance criterion for the terminal wealth where ambiguity aversion is incorporated in a smooth way. We consider here the criterion introduced in Maccheroni et al. 2013 where the variance is decomposed and each part is weighted differently to account for different levels of market risk and model ambiguity aversion. We use a novel approach to find the optimal dynamic investment strategy within the class of all adapted strategies which allow for learning. We also present a number of numerical results which help to understand how the model parameters affect the optimal investment strategy. In general it turns out that ambiguity averse investors invest less in the risky assets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper considers a continuous-time multi-asset Black-Scholes market in which asset drifts are unknown but equipped with a prior distribution. An ambiguity-averse investor maximizes the mean-variance objective of Maccheroni et al. (2013), which decomposes terminal-wealth variance into components that are weighted separately to capture market risk versus model ambiguity. The authors derive the optimal dynamic investment strategy within the class of all adapted processes that permit learning from the prior, and they supply numerical illustrations showing that higher ambiguity aversion reduces holdings in the risky assets.

Significance. If the derivation is correct, the work supplies a concrete continuous-time example in which Bayesian learning and smooth ambiguity aversion are jointly optimized under a mean-variance criterion. The numerical results constitute a verifiable strength, allowing readers to inspect how the optimal strategy responds to changes in the prior, the ambiguity weights, and the investment horizon. The finding that ambiguity-averse agents reduce risky-asset exposure is consistent with the maintained objective and provides a falsifiable comparative static.

major comments (2)

- [Abstract and §3 (main derivation)] The central claim that a novel approach yields the optimal adapted strategy rests on solving the stochastic control problem after filtering the unknown drifts. No explicit statement of the resulting Hamilton-Jacobi-Bellman equation, the form of the candidate strategy, or the verification argument appears in the abstract or the visible summary; this derivation is load-bearing for both the optimality assertion and the comparative static on ambiguity aversion.

- [§2 (criterion definition)] The paper adopts the specific variance decomposition and weighting scheme of Maccheroni et al. (2013) as the objective without reporting a sensitivity analysis with respect to the relative weights on the two variance components. Because the comparative static “ambiguity averse investors invest less” is obtained directly from these weights, the result is not robust to alternative parameterizations of the criterion.

minor comments (2)

- [§2] Notation for the filtered drift process and the innovation process should be introduced once and used consistently; several passages reuse symbols for the prior mean and the posterior mean without explicit redefinition.

- [Numerical results] The numerical section would benefit from an explicit statement of the discretization scheme and the number of Monte-Carlo paths used to generate the reported investment proportions.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive suggestions. We address each major comment below and indicate the revisions we are prepared to make.

read point-by-point responses

-

Referee: [Abstract and §3 (main derivation)] The central claim that a novel approach yields the optimal adapted strategy rests on solving the stochastic control problem after filtering the unknown drifts. No explicit statement of the resulting Hamilton-Jacobi-Bellman equation, the form of the candidate strategy, or the verification argument appears in the abstract or the visible summary; this derivation is load-bearing for both the optimality assertion and the comparative static on ambiguity aversion.

Authors: Section 3 contains the complete filtered stochastic control problem, the associated Hamilton-Jacobi-Bellman equation, the candidate optimal strategy expressed in terms of the filtered drift and the ambiguity weights, and the verification argument establishing optimality within the class of adapted processes. The abstract is intentionally concise and therefore omits these technical elements. We are willing to expand the abstract by one or two sentences that explicitly reference the filtered HJB equation and verification step. revision: partial

-

Referee: [§2 (criterion definition)] The paper adopts the specific variance decomposition and weighting scheme of Maccheroni et al. (2013) as the objective without reporting a sensitivity analysis with respect to the relative weights on the two variance components. Because the comparative static “ambiguity averse investors invest less” is obtained directly from these weights, the result is not robust to alternative parameterizations of the criterion.

Authors: The analysis is performed for the exact Maccheroni et al. (2013) criterion with its two distinct variance weights. The comparative static follows directly from the first-order condition with respect to those weights. We agree that readers may wish to see how the holdings change when the relative weight on the ambiguity component is varied; we will therefore add a short numerical sensitivity table (or figure) that recomputes the optimal strategy for a range of weight ratios while keeping all other parameters fixed. revision: yes

Circularity Check

Derivation self-contained given external objective

full rationale

The paper takes the decomposed mean-variance criterion of Maccheroni et al. (2013) as given, then solves the resulting stochastic control problem after filtering unknown drifts to obtain adapted strategies. No step reduces by construction to a fitted parameter, self-citation, or redefinition of the inputs; the comparative statics on ambiguity aversion are obtained from the optimization itself. The external criterion supplies independent content, and no load-bearing uniqueness theorem or ansatz is imported from the authors' prior work.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Black-Scholes dynamics for asset prices

- domain assumption Existence of a prior distribution on the vector of drifts

Reference graph

Works this paper leans on

-

[1]

1985 , publisher=

Integral equations , author=. 1985 , publisher=

1985

-

[2]

arXiv preprint arXiv:2412.16175 , doi=

Mean--Variance Portfolio Selection by Continuous-Time Reinforcement Learning: Algorithms, Regret Analysis, and Empirical Study , author=. arXiv preprint arXiv:2412.16175 , doi=

-

[3]

1989 , publisher=

Linear integral equations , author=. 1989 , publisher=

1989

-

[4]

, title =

Dunford, Nelson and Schwartz, Jacob T. , title =. 1963 , address =

1963

-

[5]

2006 , publisher=

Order structure and topological methods in nonlinear partial differential equations , author=. 2006 , publisher=

2006

-

[6]

Applied Mathematics Letters , volume=

Eigenvalues of rank-one updated matrices with some applications , author=. Applied Mathematics Letters , volume=. 2007 , publisher=

2007

-

[7]

Alpha as. Econometrica , author =. 2013 , keywords =. doi:10.3982/ECTA9678 , abstract =

-

[8]

and Zhao, X

Karatzas, I. and Zhao, X. , editor =. Bayesian. Option. 2001 , doi =

2001

-

[9]

European Journal of Operational Research , author =

Optimal investment in ambiguous financial markets with learning , volume =. European Journal of Operational Research , author =. 2024 , pages =. doi:10.1016/j.ejor.2024.01.022 , abstract =

-

[10]

Mathematical Methods of Operations Research , author =

Markov decision processes with risk-sensitive criteria: An overview , volume =. Mathematical Methods of Operations Research , author =. 2024 , pages =. doi:10.1007/s00186-024-00857-0 , abstract =

-

[11]

European Journal of Operational Research , author =

Mean–variance approximations to expected utility , volume =. European Journal of Operational Research , author =. 2014 , pages =. doi:10.1016/j.ejor.2012.08.023 , abstract =

-

[12]

SIAM Journal on Control and Optimization , author =

Mean‐. SIAM Journal on Control and Optimization , author =. 2007 , pages =. doi:10.1137/050641132 , abstract =

-

[13]

European Journal of Operational Research , author =

The surprising robustness of dynamic. European Journal of Operational Research , author =. 2021 , pages =. doi:10.1016/j.ejor.2020.07.021 , abstract =

-

[14]

Computational Management Science , author =

Mean-variance versus expected utility in dynamic investment analysis , volume =. Computational Management Science , author =. 2011 , pages =. doi:10.1007/s10287-009-0106-7 , abstract =

-

[15]

Applied Mathematics & Optimization , author =

Continuous-. Applied Mathematics & Optimization , author =. 2000 , pages =. doi:10.1007/s002450010003 , abstract =

-

[16]

IEEE Transactions on Automatic Control , author =

Time-. IEEE Transactions on Automatic Control , author =. 2025 , keywords =. doi:10.1109/TAC.2024.3420413 , number =

-

[17]

Mean–. Automatica , author =. 2025 , pages =. doi:10.1016/j.automatica.2025.112142 , abstract =

-

[18]

European Journal of Operational Research , author =

Continuous time mean variance asset allocation:. European Journal of Operational Research , author =. 2011 , pages =. doi:10.1016/j.ejor.2010.09.038 , abstract =

-

[19]

European Journal of Operational Research , author =

On the equivalence of quadratic optimization problems commonly used in portfolio theory , volume =. European Journal of Operational Research , author =. 2013 , pages =. doi:10.1016/j.ejor.2013.03.002 , abstract =

-

[20]

Journal of Economic Dynamics and Control , author =

A geometric approach to multiperiod mean variance optimization of assets and liabilities , volume =. Journal of Economic Dynamics and Control , author =. 2004 , pages =. doi:10.1016/S0165-1889(03)00067-8 , abstract =

-

[21]

Quantitative Finance , volume=

Mean--variance portfolio selection under partial information with drift uncertainty , author=. Quantitative Finance , volume=. 2021 , doi=

2021

-

[22]

, author=

On general minimax theorems. , author=. Pacific J. Math. , number=

-

[23]

The Review of Financial Studies , volume=

Portfolio selection with parameter and model uncertainty: A multi-prior approach , author=. The Review of Financial Studies , volume=. 2007 , doi=

2007

-

[24]

Risk, ambiguity, and the

Ellsberg, Daniel , journal=. Risk, ambiguity, and the. 1961 , doi=

1961

-

[25]

On mean-variance portfolio selection under a hidden

Elliott, Robert J and Siu, Tak Kuen and Badescu, Alex , journal=. On mean-variance portfolio selection under a hidden. 2010 , doi=

2010

-

[26]

Ismail, Amine and Pham, Huy. Robust. Mathematical Finance , volume=. 2019 , doi=

2019

-

[27]

Mathematics and Financial Economics , volume=

Optimal mean-variance portfolio selection , author=. Mathematics and Financial Economics , volume=. 2017 , doi=

2017

-

[28]

2024 , address =

Zhang, Yuanyuan , title =. 2024 , address =

2024

-

[29]

European Journal of Operational Research , volume=

Optimal investment in ambiguous financial markets with learning , author=. European Journal of Operational Research , volume=. 2024 , publisher=

2024

-

[30]

Economic Modelling , volume=

Continuous-time mean--variance portfolio selection with only risky assets , author=. Economic Modelling , volume=. 2014 , publisher=

2014

-

[31]

Optimal portfolios:

Korn, Ralf , year=. Optimal portfolios:

-

[32]

SIAM Journal on Control and Optimization , volume=

Markowitz's mean-variance portfolio selection with regime switching: A continuous-time model , author=. SIAM Journal on Control and Optimization , volume=. 2003 , doi=

2003

-

[33]

Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics , volume=

Markowitz's portfolio optimization in an incomplete market , author=. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics , volume=. 2006 , doi=

2006

-

[34]

SIAM Journal on Control and Optimization , volume=

Dynamic mean-variance portfolio selection with no-shorting constraints , author=. SIAM Journal on Control and Optimization , volume=. 2002 , doi=

2002

-

[35]

Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics , volume=

Continuous-time mean-variance portfolio selection with bankruptcy prohibition , author=. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics , volume=. 2005 , doi=

2005

-

[36]

Management Science , volume=

Dynamic asset allocation in a mean-variance framework , author=. Management Science , volume=. 1998 , doi=

1998

-

[37]

The Review of Financial Studies , volume=

Dynamic mean-variance asset allocation , author=. The Review of Financial Studies , volume=. 2010 , doi=

2010

-

[38]

Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics , volume=

Mean--variance portfolio optimization with state-dependent risk aversion , author=. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics , volume=. 2014 , doi=

2014

-

[39]

Journal of Financial Economics , volume=

Asset pricing and ambiguity: Empirical evidence , author=. Journal of Financial Economics , volume=. 2018 , doi=

2018

-

[40]

Journal of Risk and Uncertainty , volume=

Estimating ambiguity preferences and perceptions in multiple prior models: Evidence from the field , author=. Journal of Risk and Uncertainty , volume=. 2015 , doi=

2015

-

[41]

The Review of Financial Studies , volume=

Ambiguity and nonparticipation: The role of regulation , author=. The Review of Financial Studies , volume=. 2009 , doi=

2009

-

[42]

SIAM Journal on Control and Optimization , volume=

Mean-variance portfolio selection for partially observed point processes , author=. SIAM Journal on Control and Optimization , volume=. 2020 , doi=

2020

-

[43]

European Financial Management , volume=

A generalisation of the mean-variance analysis , author=. European Financial Management , volume=. 2009 , doi=

2009

-

[44]

Mean-variance type controls involving a hidden

Yang, Zhixin and Yin, George and Zhang, Qing , journal=. Mean-variance type controls involving a hidden. 2015 , doi=

2015

-

[45]

Discrete and continuous dynamical systems

The optimal mean variance problem with inflation , author=. Discrete and continuous dynamical systems. Series B , volume=. 2016 , doi=

2016

-

[46]

Mathematics of Operations Research , volume=

Quadratic hedging and mean-variance portfolio selection with random parameters in an incomplete market , author=. Mathematics of Operations Research , volume=. 2004 , doi=

2004

-

[47]

arXiv preprint arXiv:2504.02987 , year=

Model ambiguity in risk sharing with monotone mean-variance , author=. arXiv preprint arXiv:2504.02987 , year=

-

[48]

Econometrica , volume=

A smooth model of decision making under ambiguity , author=. Econometrica , volume=. 2005 , doi=

2005

-

[49]

The Journal of Finance , volume =

Markowitz, Harry , title =. The Journal of Finance , volume =. doi:10.1111/j.1540-6261.1952.tb01525.x , year =

-

[50]

Decisions in Economics and Finance , year=

Pressacco, Flavio and Serafini, Paolo , title=. Decisions in Economics and Finance , year=

-

[51]

Review of Accounting and Finance , volume=

Economic properties of the risk sensitive criterion for portfolio management , author=. Review of Accounting and Finance , volume=. 2003 , doi=

2003

-

[52]

European Journal of Operational Research , volume=

Time-consistency of optimal investment under smooth ambiguity , author=. European Journal of Operational Research , volume=. 2021 , doi=

2021

-

[53]

doi:10.1137/140951758 , journal =

An Adaptive Shifted Power Method for Computing Generalized Tensor Eigenpairs , author =. doi:10.1137/140951758 , journal =

-

[54]

Nick Higham , title =

-

[55]

Kolda and Ali Pinar , eprint =

Chengbin Peng and Tamara G. Kolda and Ali Pinar , eprint =. Accelerating Community Detection by Using

-

[56]

and Zhang, Shanrong and Merritt, Matthew E

Woessner, Donald E. and Zhang, Shanrong and Merritt, Matthew E. and Sherry, A. Dean , title =. Magnetic Resonance in Medicine , doi =

-

[57]

Properties of Highly Clustered Networks , author =. 2003 , eid =. doi:10.1103/PhysRevE.68.026121 , journal =

-

[58]

Clawpack Software , author =

-

[59]

: A Document Preparation System

Leslie Lamport. : A Document Preparation System. 1986

1986

-

[60]

Frank Mittlebach and Michel Goossens , title =

-

[61]

and Van Loan, Charles F

Golub, Gene H. and Van Loan, Charles F. , title =

-

[62]

Paul Dawkins , title =

-

[63]

User's Guide for the

-

[64]

Michael Downes , title =

-

[65]

Christian Feuers\"anger , title =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.