A Declining CVaR Glidepath Framework for Target-Date Fund Design with an Application to the Chilean Pension System

Pith reviewed 2026-06-27 05:06 UTC · model grok-4.3

The pith

Target-date funds reach explicit return targets by drawing each period from portfolios that satisfy a regulator-specified declining CVaR glidepath.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The framework replaces conventional age-based asset-class caps with an explicit return target and a declining CVaR constraint; because the manager draws randomly from the feasible set each period, success probabilities are conservative averages rather than optimistic maxima, and the two figures of merit are the probability of meeting the target and the cumulative CVaR incurred over the accumulation phase.

What carries the argument

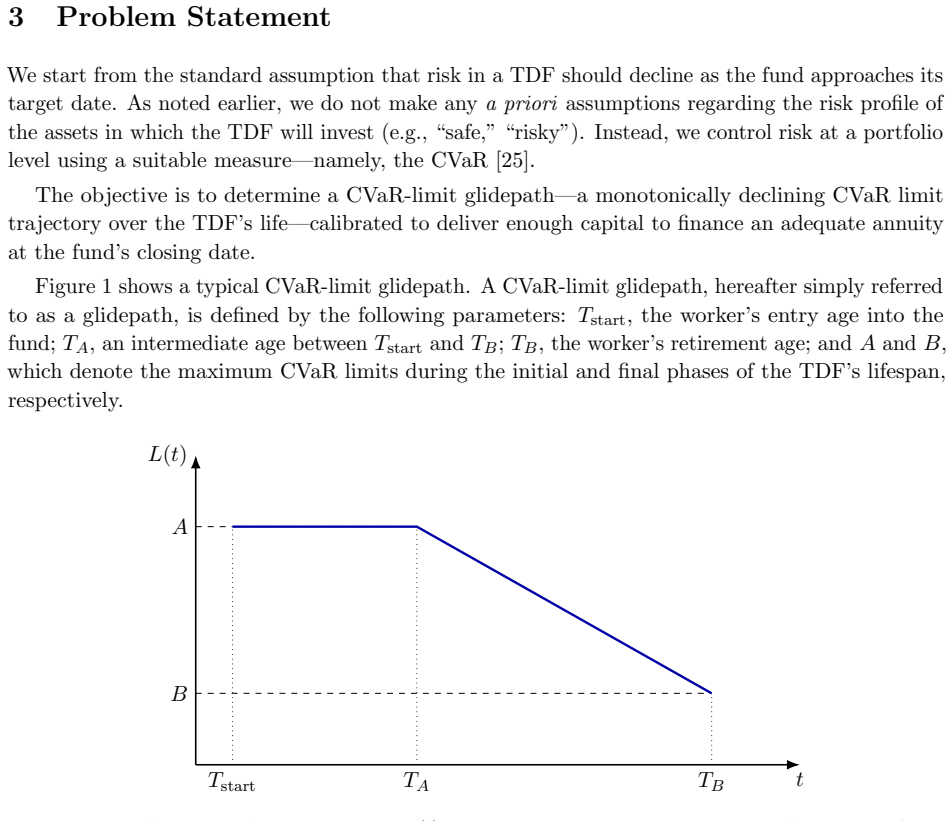

The declining CVaR glidepath, a schedule of maximum conditional value-at-risk levels that decreases with time and defines the set of admissible portfolios from which the manager samples each month.

If this is right

- Success probabilities are computed as averages over admissible allocations, producing a conservative performance metric for any given glidepath.

- The age at which the CVaR limit begins its decline is the single most influential design parameter.

- Contribution density below a critical level functions as a hard constraint that asset allocation cannot overcome.

- The same structure applies to any target-date fund built around an explicit return objective and multiple asset classes.

Where Pith is reading between the lines

- Regulators could use the framework to set glidepaths that remain robust even if managers do not optimize inside the constraint.

- The method can be recalibrated for other national pension systems simply by changing the exogenous inputs that determine the target return.

- Empirical tests could check whether actual manager choices within similar risk bounds match the random-draw model or cluster near the boundary that maximizes success.

- Policy attention may need to shift from glidepath tuning toward raising contribution density when that density falls below the identified threshold.

Load-bearing premise

The manager does not pick the portfolio inside the CVaR set that maximizes the chance of success; instead each allocation is drawn from the full admissible set.

What would settle it

Compare the average success rate predicted by sampling all CVaR-compliant portfolios against the realized success rate when a manager is observed choosing the single best portfolio inside the same constraint each month.

Figures

read the original abstract

We propose a framework for designing Target-Date Funds (TDFs) around an explicit return objective while controlling risk directly at the portfolio level through a declining Conditional Value-at-Risk (CVaR) constraint. In this approach, the regulator or sponsor specifies a CVaR glidepath that gives the portfolio manager enough flexibility to reach a target return with a reasonably high probability. The target return is determined exogenously from pension-design inputs such as retirement age, contribution rate, working years, life expectancy, and replacement-rate goals. This differs from conventional TDF design, where age-dependent asset-class limits are set without an explicit link to a required return. A key feature of the method is that it does not assume the manager selects an optimal portfolio each period. Instead, each month the manager draws an allocation from the set of portfolios satisfying the CVaR constraint. This yields a conservative evaluation of each glidepath: success probabilities are averages over admissible allocations, rather than best-case outcomes. We introduce two figures of merit: the probability of meeting the target return and the cumulative risk assumed over the life of the TDF. As a proof of concept, we apply the framework to Chile's 2025 pension reform using nine Chilean and global asset classes and a 40-year accumulation horizon. The results show that the transition age at which risk starts to decline is the most consequential design parameter, and that contribution density acts as a hard constraint: below a critical threshold, portfolio design alone cannot compensate for structurally low contributions. The framework is general and can be applied to any TDF designed around an explicit return objective.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a framework for Target-Date Fund (TDF) design that specifies an exogenous target return (derived from pension parameters such as retirement age, contribution rate, and replacement-rate goals) and enforces it via a declining CVaR glidepath constraint at the portfolio level. Unlike conventional age-based asset-class limits, the approach lets the regulator set the CVaR path; each period the manager draws an allocation from the feasible set rather than optimizing inside it, yielding conservative success probabilities that are averages over admissible portfolios. The framework is applied as a proof of concept to Chile’s 2025 pension reform using nine asset classes over a 40-year horizon, with results indicating that the transition age at which the CVaR begins to decline is the most consequential parameter and that contribution density functions as a hard constraint below which portfolio design cannot compensate.

Significance. If the numerical results hold under the stated conservative evaluation, the framework supplies a direct, regulator-specified link between risk limits and required returns that is absent from standard TDF glidepaths; the Chilean application illustrates how design parameters interact with structural constraints such as contribution density, offering a template that could be adapted to other systems with explicit replacement-rate targets.

major comments (2)

- [Abstract and framework description] The central claim—that a declining CVaR glidepath supplies the manager with enough flexibility to reach the target return with reasonably high probability—is evaluated exclusively under random draws from the admissible set rather than any optimization within that set. This choice directly determines the reported success probabilities and the conclusion that transition age is most consequential; if the admissible set contains portfolios with materially different conditional expected returns, the gap between average and best-case outcomes becomes load-bearing for whether the flexibility claim is demonstrated.

- [Abstract] No mathematical formulation, definition of the CVaR constraint, or description of the admissible-set sampling procedure appears in the provided abstract or high-level description, making it impossible to verify whether the reported transition-age and contribution-density results follow from the stated method or from auxiliary modeling choices.

minor comments (1)

- [Application section] Clarify whether the nine asset classes are treated as fixed or rebalanced monthly and whether any transaction-cost or liquidity constraints are imposed inside the CVaR set.

Simulated Author's Rebuttal

We thank the referee for the constructive comments. We respond point-by-point to the major comments below, maintaining the conservative evaluation approach as a deliberate feature of the framework.

read point-by-point responses

-

Referee: [Abstract and framework description] The central claim—that a declining CVaR glidepath supplies the manager with enough flexibility to reach the target return with reasonably high probability—is evaluated exclusively under random draws from the admissible set rather than any optimization within that set. This choice directly determines the reported success probabilities and the conclusion that transition age is most consequential; if the admissible set contains portfolios with materially different conditional expected returns, the gap between average and best-case outcomes becomes load-bearing for whether the flexibility claim is demonstrated.

Authors: The manuscript explicitly adopts random draws from the admissible set to generate conservative (average-case) success probabilities rather than best-case outcomes under optimization; this is stated in the abstract and Section 3 as a core methodological choice. The declining CVaR glidepath is shown to deliver reasonable success rates even under this conservative sampling, which we regard as the appropriate benchmark for a regulator-specified framework. The transition-age result follows directly from this evaluation. We can add a brief sensitivity discussion contrasting average versus optimized outcomes if requested. revision: partial

-

Referee: [Abstract] No mathematical formulation, definition of the CVaR constraint, or description of the admissible-set sampling procedure appears in the provided abstract or high-level description, making it impossible to verify whether the reported transition-age and contribution-density results follow from the stated method or from auxiliary modeling choices.

Authors: The abstract is intentionally concise. The full manuscript defines the CVaR constraint mathematically in Section 2, specifies the admissible-set construction, and details the sampling procedure in Section 3; all reported results are generated from this formulation. To address the concern about verifiability from the abstract alone, we will expand the abstract with a short clause summarizing the CVaR definition and sampling approach. revision: yes

Circularity Check

No circularity: exogenous target return and explicit conservative random-draw policy are independent of reported outcomes.

full rationale

The paper defines the target return from external pension-design inputs (retirement age, contribution rate, etc.) and evaluates glidepaths by averaging success probabilities over random draws from the CVaR-admissible set rather than optimization. This choice is stated upfront as conservative and does not reduce the reported probabilities or figures of merit to a fitted parameter or self-referential quantity. No self-citations, uniqueness theorems, or ansatzes are invoked to justify the central construction. The derivation chain therefore remains self-contained against the paper's own stated assumptions and data.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Target-date funds continue their rapid rise

Mahi Roy. Target-date funds continue their rapid rise. Morningstar, March 2026. URL https://www.morningstar.com/funds/target-date-funds-continue-their-rapid-rise . Published March 11, 2026

2026

-

[2]

Parker, Antoinette Schoar, and Yang Sun

Jonathan A. Parker, Antoinette Schoar, and Yang Sun. Retail financial innovation and stock market dynamics: The case of Target Date Funds.The Journal of Finance, 78(5):2673–2723,

-

[3]

doi: 10.1111/jofi.13258

-

[4]

Vanguard Target Retirement 2070 Fund investment profile

Vanguard. Vanguard Target Retirement 2070 Fund investment profile. Investment profile, March 2026. URL https://workplace.vanguard.com/assets/corp/fund_communications /pdf_publish/us-products/investment-profiles/V009.pdf. Data as of March 31, 2026

2070

-

[5]

Vanguard Target Retirement 2025 Fund investment profile

Vanguard. Vanguard Target Retirement 2025 Fund investment profile. Investment profile, March 2026. URL https://workplace.vanguard.com/assets/corp/fund_communications /pdf_publish/us-products/investment-profiles/0304.pdf. Data as of March 31, 2026

2025

-

[6]

Paul A. Samuelson. Lifetime portfolio selection by dynamic stochastic programming.The Review of Economics and Statistics, 51(3):239–246, 1969. doi: 10.2307/1926559. URL https://www.jstor.org/stable/1926559

-

[7]

Robert C. Merton. Lifetime portfolio selection under uncertainty: The continuous-time case. The Review of Economics and Statistics, 51(3):247–257, 1969. doi: 10.2307/1926560. URL https://www.jstor.org/stable/1926560

-

[8]

Merton, and William F

Zvi Bodie, Robert C. Merton, and William F. Samuelson. Labor supply flexibility and portfolio choice in a life cycle model.Journal of Economic Dynamics and Control, 16(3–4):427–449,

-

[9]

doi: 10.1016/0165-1889(92)90044-F

-

[10]

Francisco J. Gomes, Laurence J. Kotlikoff, and Luis M. Viceira. Optimal life-cycle investing with flexible labor supply: A welfare analysis of life-cycle funds.American Economic Review, 98(2):297–303, 2008. doi: 10.1257/aer.98.2.297

-

[11]

Jo˜ ao F. Cocco, Francisco J. Gomes, and Pascal J. Maenhout. Consumption and portfolio choice over the life cycle.The Review of Financial Studies, 18(2):491–533, 2005. doi: 10.1093/rfs/hh i017

-

[12]

Ley 21.735: Crea un nuevo sistema mixto de pensiones y un seguro social en el pilar contributivo

Biblioteca del Congreso Nacional de Chile. Ley 21.735: Crea un nuevo sistema mixto de pensiones y un seguro social en el pilar contributivo. Ley Chile, March 2025. URL https: //www.leychile.cl/navegar?idNorma=1212060. Published March 26, 2025

2025

-

[13]

Superintendencia de pensiones adjudica a mercer consulting el diseno de los nuevos fondos generacionales

Subsecretaria de Prevision Social. Superintendencia de pensiones adjudica a mercer consulting el diseno de los nuevos fondos generacionales. Press release, August 2025. URL https: //previsionsocial.gob.cl/superintendencia-de-pensiones-adjudica-a-mercer-con sulting-el-diseno-de-los-nuevos-fondos-generacionales-carteras-de-referenci a-y-medidas-de-desempeno...

2025

-

[14]

Martin and Joshua Rafsky

Craig C. Martin and Joshua Rafsky. The pension protection act of 2006: An overview of sweeping changes in the law governing retirement plans.The John Marshall Law Review, 40 (3):843–866, 2007. URLhttps://repository.law.uic.edu/lawreview/vol40/iss3/5/. 24

2006

-

[15]

Department of Labor

U.S. Department of Labor. Default investment alternatives under participant directed individual account plans. Final rule, 72 Fed. Reg. 60452, October 2007. URL https://www.dol.gov/ne wsroom/releases/ebsa/ebsa20071023. Codified at 29 CFR 2550.404c-5

2007

-

[16]

Robert J. Shiller. Life-cycle portfolios as government policy.The Economists’ Voice, 2(1), 2005. doi: 10.2202/1553-3832.1095

-

[17]

Wade D. Pfau and Michael Kitces. Reducing retirement risk with a rising equity glide-path. Journal of Financial Planning, 27(1):38–45, 2014. URL https://www.financialplanningass ociation.org/article/journal/JAN14-reducing-retirement-risk-rising-equity-gli de-path. Earlier SSRN version: 10.2139/ssrn.2324930

-

[18]

Javier Estrada. The glidepath illusion: An international perspective.Journal of Portfolio Management, 40(4):52–64, 2014. doi: 10.3905/jpm.2014.40.4.052

-

[19]

The retirement glidepath: An international perspective.Journal of Investing, 25 (2):28–54, 2016

Javier Estrada. The retirement glidepath: An international perspective.Journal of Investing, 25 (2):28–54, 2016. doi: 10.3905/joi.2016.25.2.028. URL https://ssrn.com/abstract=2557256

-

[20]

Elton, Martin J

Edwin J. Elton, Martin J. Gruber, Andr´ e de Souza, and Christopher R. Blake. Target Date Funds: Characteristics and performance.The Review of Asset Pricing Studies, 5(2):254–272,

-

[21]

doi: 10.1093/rapstu/rav004

-

[22]

Heterogeneity in target date funds: Strategic risk- taking or risk matching?The Review of Financial Studies, 32(1):300–337, 2019

Pierluigi Balduzzi and Jonathan Reuter. Heterogeneity in target date funds: Strategic risk- taking or risk matching?The Review of Financial Studies, 32(1):300–337, 2019. doi: 10.1093/ rfs/hhy054

2019

-

[23]

Pagnoncelli, and Arturo Cifuentes

Hans Schlechter, Bernardo K. Pagnoncelli, and Arturo Cifuentes. Pension funds in Mexico and Chile: A risk-reward comparison. SSRN Working Paper, 2019. URL https://ssrn.com/abs tract=3359920

2019

-

[24]

Pagnoncelli, Shirley Redroban, and Arturo Cifuentes

Bernardo K. Pagnoncelli, Shirley Redroban, and Arturo Cifuentes. A useful (but painful) risk- management lesson from the Chilean pension system.The Journal of Retirement, 11(1):74–83,

-

[25]

doi: 10.3905/jor.2023.1.135. URL https://clapesuc.cl/investigacion/paper-a-u seful-but-painful-risk-management-lesson-from-the-chilean-pension-system

-

[26]

Romain Perchet, Mehdi-Vincent Hacini, Thomas Heckel, and Koye Somefun. Practical and robust glide path design for multi-asset Target Date Funds.The Journal of Retirement, 13(3): 66–80, October 2025. doi: 10.3905/jor.2025.1.196. URL https://doi.org/10.3905/jor.20 25.1.196

-

[27]

Are target date funds dinosaurs? Failure to adapt can lead to extinction

Peter A. Forsyth, Yuying Li, and Kenneth R. Vetzal. Are Target Date Funds dinosaurs? failure to adapt can lead to extinction.arXiv preprint arXiv:1705.00543, 2017. doi: 10.48550/arXiv.1 705.00543. URLhttps://arxiv.org/abs/1705.00543

work page internal anchor Pith review Pith/arXiv arXiv doi:10.48550/arxiv.1 2017

-

[28]

Fernando Su´ arez, Jos´ e Manuel Pe˜ na, and Omar Larr´ e. Target-Date Funds: A state-of-the-art review with policy applications to Chile’s pension reform.arXiv preprint arXiv:2504.17713,

-

[29]

URLhttps://arxiv.org/abs/2504.17713

doi: 10.48550/arXiv.2504.17713. URLhttps://arxiv.org/abs/2504.17713

-

[30]

Optimization of conditional value-at-risk,

R. Tyrrell Rockafellar and Stanislav Uryasev. Optimization of Conditional Value-at-Risk. Journal of Risk, 2(3):21–41, 2000. doi: 10.21314/JOR.2000.038. 25

-

[31]

Nelsen.An Introduction to Copulas

Roger B. Nelsen.An Introduction to Copulas. Springer, New York, 2 edition, 2006. doi: 10.1007/0-387-28678-0

-

[32]

Robert L. Smith. Efficient monte carlo procedures for generating points uniformly distributed over bounded regions.Operations Research, 32(6):1296–1308, 1984. doi: 10.1287/opre.32.6.1296

-

[33]

Indices de reajustabilidad: Unidad de fomento e indice de valor promedio

Banco Central de Chile. Indices de reajustabilidad: Unidad de fomento e indice de valor promedio. Methodological note, 2026. URL https://si3.bcentral.cl/estadisticas/Pri ncipal1/Metodologias/EMF/UF_IVP.pdf

2026

-

[34]

OECD Publishing, Paris,

OECD.Pensions at a Glance 2025: OECD and G20 Indicators. OECD Publishing, Paris,

2025

-

[35]

URLhttps://doi.org/10.1787/e40274c1-en

doi: 10.1787/e40274c1-en. URLhttps://doi.org/10.1787/e40274c1-en

-

[36]

Ficha estadistica previsional no

Superintendencia de Pensiones. Ficha estadistica previsional no. 141 – agosto 2024. Government statistical bulletin, August 2024. URL https://www.spensiones.cl/portal/institucion al/594/articles-16096_recurso_1.pdf. Includes contribution-density data as of May 2024 and new-affiliate data for 2023

2024

-

[37]

Decreto ley 3.500: Establece nuevo sistema de pensiones

Biblioteca del Congreso Nacional de Chile. Decreto ley 3.500: Establece nuevo sistema de pensiones. Ley Chile, November 1980. URL https://www.leychile.cl/navegar?idNorma= 7147

1980

-

[38]

Tablas de mortalidad cb-h-2020, mi-h-2020, rv-m-2020, b- m-2020 y mi-m-2020

Superintendencia de Pensiones. Tablas de mortalidad cb-h-2020, mi-h-2020, rv-m-2020, b- m-2020 y mi-m-2020. Compendio de Normas del Sistema de Pensiones, Libro III, Titulo X, Capitulo IX, 2023. URL https://www.spensiones.cl/portal/compendio/596/w3-propert yvalue-10624.html. Added by Norma de Caracter General No. 306, February 24, 2023

2020

-

[39]

Tasas de interes medias en las rentas vitalicias

Superintendencia de Pensiones. Tasas de interes medias en las rentas vitalicias. Statistical series, 2026. URLhttps://www.spensiones.cl/apps/tasas/tasasRentasVitalicias.php

2026

-

[40]

Seleccion de modalidad de pension: Sistema de consultas y ofertas de montos de pension (scomp), primer semestre 2025

Superintendencia de Pensiones. Seleccion de modalidad de pension: Sistema de consultas y ofertas de montos de pension (scomp), primer semestre 2025. Government statistical report,

2025

-

[41]

URL https://www.spensiones.gob.cl/portal/institucional/594/articles-166 79_recurso_1.pdf

-

[42]

Base de datos estadisticos: Tasas swap promedio camara, spc en uf 10 anos

Banco Central de Chile. Base de datos estadisticos: Tasas swap promedio camara, spc en uf 10 anos. Statistical series, 2026. URL https://si3.bcentral.cl/Siete/ES/Siete/Cuadro/CA P_TASA_INTERES/MN_TASA_INTERES_09/TI__TPM4/T31b?cbFechaDiaria=2018&cbFrecuen cia=DAILY&cbCalculo=NONE&cbFechaBase=. 26 APPENDIX A Uniform Sampling over the Feasible Set via the Hi...

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.