Generating EUPHEMIA-compatible bids for flexible demand under imperfect information

Pith reviewed 2026-06-25 22:14 UTC · model grok-4.3

The pith

A method for creating two EUPHEMIA-compatible bid formats shows that flexible demand performs differently depending on its operational constraints and market price volatility.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

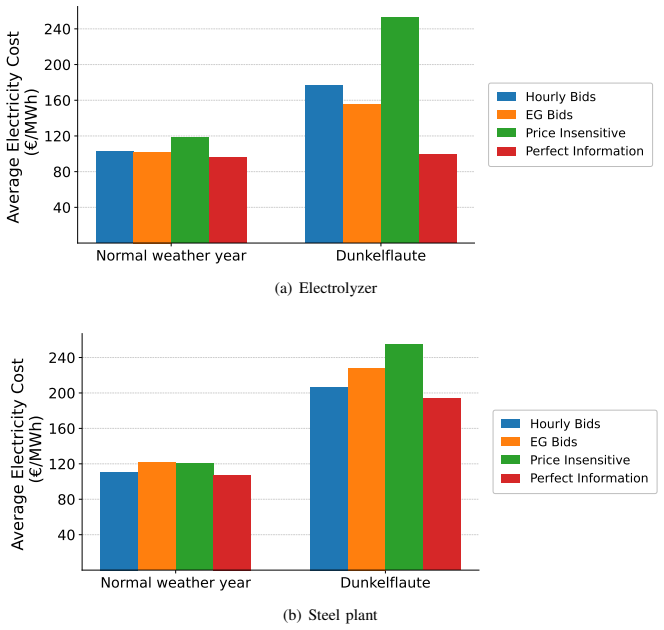

The method generates EUPHEMIA-compatible hourly bids and exclusive-group bids for flexible demand. Economic outcomes vary with operational characteristics: in volatile conditions, highly flexible systems benefit more from exclusive-group bids, while less flexible systems with stronger intertemporal constraints benefit from hourly bids.

What carries the argument

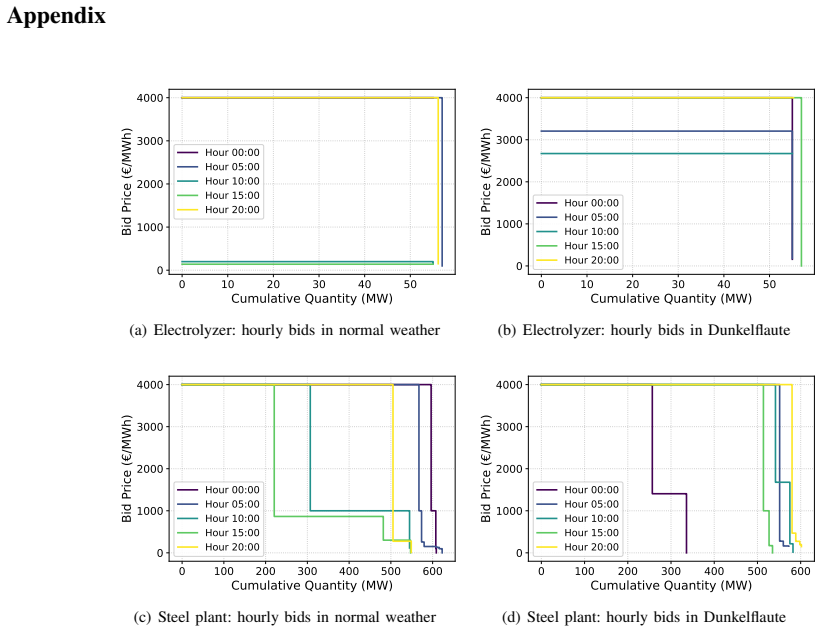

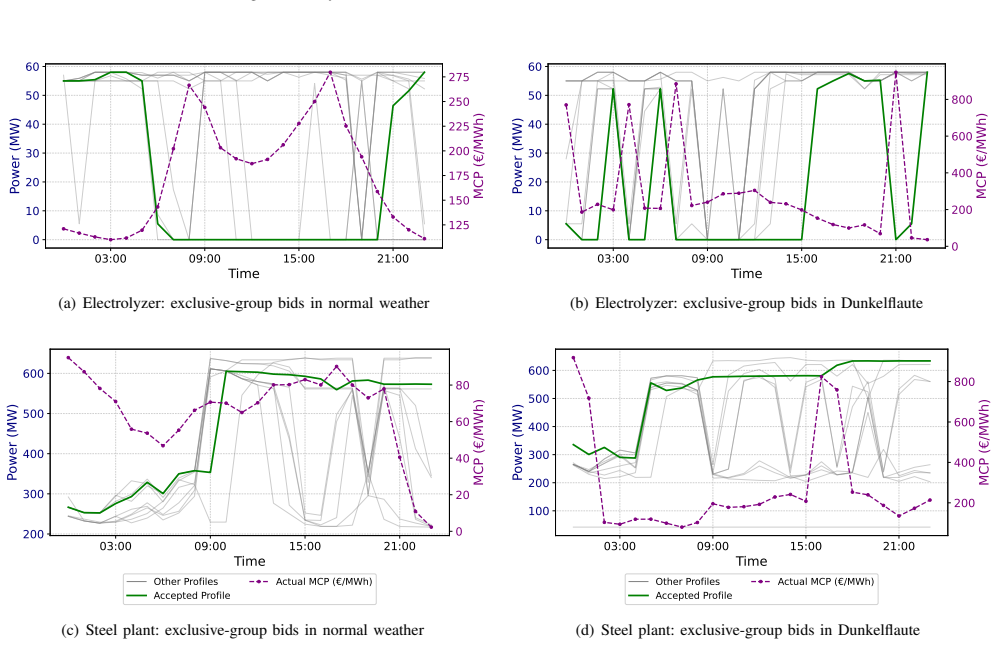

The two bid formats: hourly bids via price-quantity pairs for marginal price responsiveness and exclusive-group bids via mutually exclusive operational schedules submitted at opportunity cost.

If this is right

- Under volatile market conditions, highly flexible systems achieve better economic outcomes with exclusive-group bids.

- Less flexible systems with stronger intertemporal constraints perform better with hourly bids.

- The relative advantage of each format depends on the specific operational characteristics of the load.

- Both formats allow flexible demand to participate in the day-ahead market while addressing risk from imperfect price information.

Where Pith is reading between the lines

- The pattern could be checked on other loads such as data centers or cold storage to test whether flexibility level remains the dominant factor.

- Market rules that make exclusive-group bids easier to submit might increase participation by highly adaptable industrial users.

- If risk is quantified through explicit probability distributions rather than the current approach, the performance gap between the formats might narrow or reverse.

- Wider use of the better-matching format could reduce the need for real-time balancing actions caused by inflexible day-ahead positions.

Load-bearing premise

The two bid formats are assumed to adequately represent flexibility under imperfect information, and the electrolyzer and steel plant cases allow general conclusions about economic performance.

What would settle it

Running the steel plant's actual historical load data through both bid formats over a multi-week period of recorded high price volatility and comparing the resulting procurement costs would show whether one format consistently outperforms the other.

Figures

read the original abstract

Electricity procurement constitutes a significant share of operational costs for large electricity consumers, and thus exposure to extreme prices poses a substantial financial risk. This paper proposes a method to generate EUPHEMIA-compatible bids for flexible demand to enable their participation in the European day-ahead electricity market while minimizing risks. Two strategies are considered, resulting in two bid formats: hourly bids (HBs), representing flexibility via marginal price responsiveness through price-quantity pairs, and exclusive-group bids (EBs), representing flexibility via mutually exclusive operational schedules submitted at opportunity cost. Our method is evaluated on a hypothetical electrolyzer system and a real-world steel plant under different market conditions. Results show that the economic performance of each strategy depends on the operational characteristics of the load and market conditions. Under volatile market conditions, highly flexible systems achieve better economic outcomes with EBs, while less flexible systems with stronger intertemporal constraints perform better with HBs.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a method to generate EUPHEMIA-compatible bids for flexible electricity demand under imperfect information, comparing two formats: hourly bids (HBs) that use price-quantity pairs to represent marginal price responsiveness, and exclusive-group bids (EBs) that submit mutually exclusive operational schedules at opportunity cost. The method is evaluated on a hypothetical electrolyzer and a real steel plant across different market conditions, with the central claim that economic performance depends on load flexibility and volatility—EBs outperform for highly flexible systems under volatile prices, while HBs perform better for loads with stronger intertemporal constraints.

Significance. If the underlying stochastic optimization, imperfect-information model, and risk functional are correctly specified and the numerical results hold under standard validation, the work would offer a practical contribution to demand-response participation in European day-ahead markets by showing how bid format choice interacts with operational constraints and price uncertainty.

major comments (2)

- [Abstract, §3] Abstract and §3 (method description): No equations, scenario-generation procedure, or risk measure (e.g., expected cost, CVaR) are supplied for mapping the imperfect-information distribution into bid parameters; without this, the reported ranking of EBs versus HBs cannot be reproduced or assessed for robustness.

- [§4] §4 (case studies): The electrolyzer and steel-plant evaluations report comparative economic outcomes but supply neither the data sources for price scenarios, the precise intertemporal constraints, nor any statistical validation (confidence intervals, sensitivity checks); this leaves the claim that “performance depends on operational characteristics” unsupported by verifiable evidence.

minor comments (1)

- [§2] Notation for opportunity cost in EBs and the definition of “volatility” in market conditions should be introduced explicitly before the numerical results.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which identify key gaps in reproducibility. We agree that additional methodological and empirical details are required and will revise the manuscript accordingly to address both major comments.

read point-by-point responses

-

Referee: [Abstract, §3] Abstract and §3 (method description): No equations, scenario-generation procedure, or risk measure (e.g., expected cost, CVaR) are supplied for mapping the imperfect-information distribution into bid parameters; without this, the reported ranking of EBs versus HBs cannot be reproduced or assessed for robustness.

Authors: We agree that the current description of the method in §3 lacks the explicit equations, scenario-generation procedure, and risk measure needed for full reproducibility. In the revised manuscript we will insert the stochastic optimization formulation, the procedure used to generate price scenarios from the imperfect-information distribution, and the specific risk functional (expected cost or CVaR) that maps scenarios into the bid parameters for both hourly bids and exclusive-group bids. These additions will allow independent verification of the ranking between the two formats. revision: yes

-

Referee: [§4] §4 (case studies): The electrolyzer and steel-plant evaluations report comparative economic outcomes but supply neither the data sources for price scenarios, the precise intertemporal constraints, nor any statistical validation (confidence intervals, sensitivity checks); this leaves the claim that “performance depends on operational characteristics” unsupported by verifiable evidence.

Authors: We acknowledge that §4 currently omits the data sources for the price scenarios, the exact intertemporal constraints applied to each load, and statistical validation. In the revision we will add the sources of the price data, list the precise operational constraints for the electrolyzer and steel plant, and include sensitivity checks or confidence intervals supporting the dependence of performance on flexibility and volatility. Some real-plant data may be summarized for confidentiality reasons, but the key parameters and validation steps will be provided. revision: partial

Circularity Check

No circularity; derivation is self-contained via explicit bid construction and case evaluation

full rationale

The paper proposes two explicit bid formats (hourly bids via price-quantity pairs and exclusive-group bids via mutually exclusive schedules) and evaluates their economic outcomes on defined load cases under stated market conditions. No step reduces a claimed prediction to a fitted input by construction, no self-citation chain bears the central result, and no ansatz or uniqueness theorem is imported to force the outcome. The reported performance rankings follow directly from applying the defined strategies to the electrolyzer and steel-plant instances, making the chain independent of its own outputs.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption EUPHEMIA accepts hourly bids via price-quantity pairs and exclusive-group bids with opportunity costs.

- domain assumption Operational characteristics of the electrolyzer and steel plant represent relevant classes of flexible demand.

Reference graph

Works this paper leans on

-

[1]

Available at SSRN 3517267 , year =

Fehmi Tanrisever and Masoud Shahmanzari and Burak Buke , title =. Available at SSRN 3517267 , year =

-

[2]

Industrial consumers' electricity market participation options: a case study of an industrial cooling process in Denmark , journal =

Nicolas Fatras and Zheng Ma and Bo N. Industrial consumers' electricity market participation options: a case study of an industrial cooling process in Denmark , journal =

-

[3]

IEEE Transactions on Smart Grid , year =

Zhiwei Xu and others , title =. IEEE Transactions on Smart Grid , year =. doi:10.1109/TSG.2021.3066801 , note =

-

[4]

IEEE Transactions on Sustainable Energy , year =

Tianyang Zhao and others , title =. IEEE Transactions on Sustainable Energy , year =. doi:10.1109/TSTE.2018.2884997 , note =

-

[5]

Advances in Applied Energy , volume =

Robert Herding and others , title =. Advances in Applied Energy , volume =. 2024 , doi =

2024

-

[6]

Kardakos and Christos K

Evaggelos G. Kardakos and Christos K. Simoglou and Anastasios G. Bakirtzis , title =. IEEE Transactions on Smart Grid , volume =

-

[7]

IEEE Transactions on Engineering Management , year =

Mansour Charwand and Mohsen Gitizadeh , title =. IEEE Transactions on Engineering Management , year =. doi:10.1109/TEM.2018.2864132 , note =

-

[8]

IEEE Transactions on Energy Markets, Policy and Regulation , year =

Makedon Karasavvidis and Dimitrios Papadaskalopoulos and Goran Strbac , title =. IEEE Transactions on Energy Markets, Policy and Regulation , year =

-

[9]

EUPHEMIA Public Description: Single Price Coupling Algorithm , year =

-

[10]

Applied Energy , volume =

Siwan Huang and others , title =. Applied Energy , volume =

-

[11]

Energy Reports , volume =

Tasarruf Bashir and others , title =. Energy Reports , volume =

-

[12]

2008 China International Conference on Electricity Distribution , publisher =

Quan Chen and others , title =. 2008 China International Conference on Electricity Distribution , publisher =. 2008 , pages =

2008

-

[13]

2011 16th International Conference on Intelligent System Applications to Power Systems , publisher =

Jean Sumaili and others , title =. 2011 16th International Conference on Intelligent System Applications to Power Systems , publisher =. 2011 , pages =

2011

-

[14]

A Robust Optimization Framework for Flexible Industrial Energy Scheduling: Application to a Cement Plant with Market Participation , year =

Sebasti. A Robust Optimization Framework for Flexible Industrial Energy Scheduling: Application to a Cement Plant with Market Participation , year =

-

[15]

Issam K. O. Jabari and others , title =. Proceedings of the 8th International Conference on Sustainable Information Engineering and Technology , year =

-

[16]

Kallabis , title =

T. Kallabis , title =

-

[17]

Optimal trading of flexible power consumption on the day-ahead market , booktitle =

Neele Leith. Optimal trading of flexible power consumption on the day-ahead market , booktitle =. 2021 , pages =

2021

-

[18]

Risk-Averse Optimal Bidding Strategy for Demand-Side Resource Aggregators in Day-Ahead Electricity Markets Under Uncertainty , year=

Xu, Zhiwei and Hu, Zechun and Song, Yonghua and Wang, Jianhui , journal=. Risk-Averse Optimal Bidding Strategy for Demand-Side Resource Aggregators in Day-Ahead Electricity Markets Under Uncertainty , year=

-

[19]

Strategic Bidding of Hybrid AC/DC Microgrid Embedded Energy Hubs: A Two-Stage Chance Constrained Stochastic Programming Approach , year=

Zhao, Tianyang and Pan, Xuewei and Yao, Shuhan and Ju, Chenchen and Li, Lei , journal=. Strategic Bidding of Hybrid AC/DC Microgrid Embedded Energy Hubs: A Two-Stage Chance Constrained Stochastic Programming Approach , year=

-

[20]

Risk-aware microgrid operation and participation in the day-ahead electricity market , journal =. 2024 , issn =. doi:https://doi.org/10.1016/j.adapen.2024.100180 , author =

-

[21]

and Simoglou, Christos K

Kardakos, Evaggelos G. and Simoglou, Christos K. and Bakirtzis, Anastasios G. , journal=. Optimal Offering Strategy of a Virtual Power Plant: A Stochastic Bi-Level Approach , year=

-

[22]

Machine learning and deep learning prediction models for time-series: a comparative analytical study for the use case of

Mishra, Bhupesh Kumar and Preniqi, Vjosa and Thakker, Dhavalkumar and Feigl, Erich , journal =. Machine learning and deep learning prediction models for time-series: a comparative analytical study for the use case of. 2024 , doi =

2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.