The fused asset flow model: stability, bifurcation, and contagion in multi-asset markets with heterogeneous investors

Pith reviewed 2026-06-29 09:51 UTC · model grok-4.3

The pith

In a fused multi-asset model with trend and value investors, the fundamental equilibrium loses stability through a supercritical Hopf bifurcation and produces persistent limit cycles.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

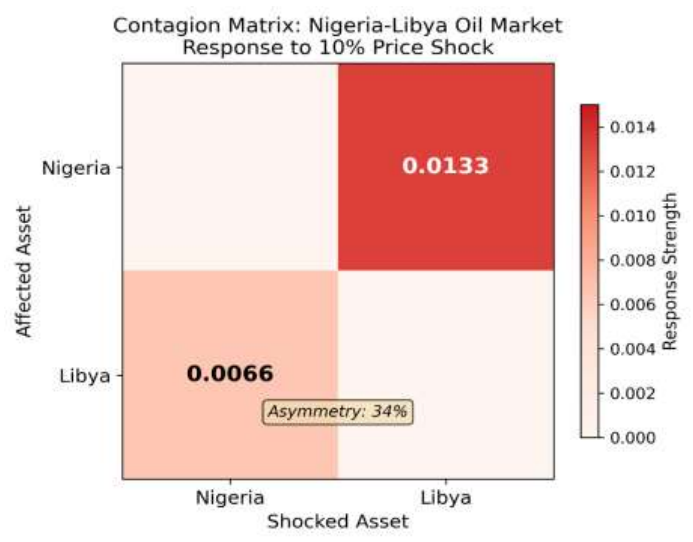

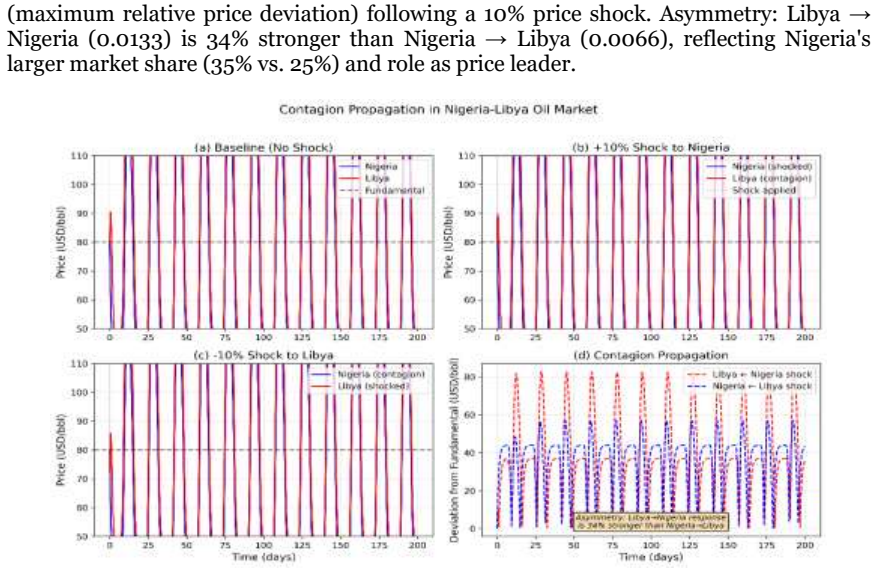

The fused asset-flow model is a system of ordinary differential equations for prices, cash holdings, share holdings, and sentiment variables across multiple assets and investor groups. The equilibrium set forms a manifold parameterized by the distribution of cash among groups; the fundamental equilibrium lies on this manifold. Linearization around that point yields a characteristic equation whose roots cross the imaginary axis transversely under explicit parameter conditions, producing a supercritical Hopf bifurcation. The resulting limit cycles reproduce the equilibrium manifolds, bifurcation thresholds, and asymmetric contagion signatures of the three benchmark models.

What carries the argument

The system of ODEs with asymmetric cross-asset coupling in buying decisions; linear stability analysis of the fundamental equilibrium on the cash-distribution manifold that detects the supercritical Hopf bifurcation.

If this is right

- The equilibrium manifold remains stable for wide ranges of cash distribution but loses stability at explicit thresholds on trend and value parameters.

- Supercritical Hopf bifurcations generate limit cycles whose periods match those observed in the single-asset and two-asset benchmark models.

- Contagion between assets is asymmetric: a cycle in one asset can drive or dampen cycles in the other depending on the sign of the cross-coupling terms.

- All physically relevant variables (prices, cash, shares, sentiment) remain positive and bounded for all time when initial conditions are positive.

Where Pith is reading between the lines

- The same bifurcation mechanism could be used to forecast the onset of oscillatory regimes in real multi-asset portfolios once the model parameters are fitted to observed price and volume data.

- Because the cash-distribution manifold is continuous, small shifts in wealth between investor groups can move the system across the Hopf threshold without any change in the underlying strategies.

- Extending the model to stochastic noise on the demand functions would likely turn the deterministic limit cycles into noisy oscillations whose power spectrum could be compared directly with empirical return series.

Load-bearing premise

The chosen functional forms for trend-following and value-based demand, together with the asymmetric cross-asset coupling, are assumed to guarantee positivity, boundedness, the equilibrium manifold, and the Hopf bifurcation without hidden inconsistencies or extra parameters.

What would settle it

A numerical integration of the full ODE system under the stated parameter values that produces no limit cycle after the predicted Hopf threshold, or a real-market time series of two assets showing no oscillatory contagion when the model parameters calibrated to those assets predict a cycle.

Figures

read the original abstract

This paper presents a unified multi-asset, multi-group asset-flow model that integrates three foundational frameworks from the behavioral finance literature. The model captures the dynamics of financial markets where multiple assets are traded by multiple investor groups, each with distinct trend-following (momentum) and value-based (fundamental) strategies. Unlike classical efficient market models, our framework explicitly incorporates the finiteness of cash and shares, asymmetric cross-asset coupling in buying decisions, and endogenous wealth redistribution across groups. We derive the complete system of ordinary differential equations governing price, cash, share, and sentiment dynamics, and establish the fundamental properties of positivity and boundedness for all physically relevant variables. The equilibrium set is characterized as a manifold parameterized by cash distribution, with the fundamental equilibrium as a special point. Through linear stability analysis, we identify conditions under which the fundamental equilibrium loses stability via a supercritical Hopf bifurcation, giving rise to persistent limit cycles. The model is validated against three benchmark papers: the single-asset multi-group model of DeSantis, Swigon, and Caginalp (2012); the two-asset single-group model of Bulut, Merdan, and Swigon (2019); and the two-asset two-group Nigeria-Libya oil market model of Cavani (2026). Our numerical simulations reproduce all key theoretical predictions, including equilibrium manifolds, Hopf bifurcation thresholds, limit cycle periods, and asymmetric contagion patterns.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents a unified multi-asset, multi-group asset-flow model integrating three prior frameworks. It derives an ODE system governing price, cash, share, and sentiment dynamics; establishes positivity and boundedness; characterizes the equilibrium set as a manifold parameterized by cash distribution (with the fundamental equilibrium as a special case); and claims that linear stability analysis identifies conditions for the fundamental equilibrium to lose stability via a supercritical Hopf bifurcation, producing persistent limit cycles. Numerical simulations are asserted to reproduce equilibrium manifolds, bifurcation thresholds, cycle periods, and asymmetric contagion, with validation against DeSantis-Swigon-Caginalp (2012), Bulut-Merdan-Swigon (2019), and Cavani (2026).

Significance. If the derivation, boundedness proofs, manifold characterization, and bifurcation analysis hold after correction, the work would supply a coherent dynamical-systems framework for multi-asset contagion and endogenous oscillations under heterogeneous trend-following and value-based strategies, extending the cited single-asset and single-group models while incorporating cash finiteness and asymmetric cross-asset coupling.

major comments (1)

- [Abstract] Abstract: the claim that 'linear stability analysis' identifies conditions for a 'supercritical Hopf bifurcation' cannot be supported by linearization alone. Linear analysis yields the crossing of a complex-conjugate pair through the imaginary axis (with the zero eigenvalue already present from the equilibrium manifold in the cash-distribution directions), but the distinction between super- and subcriticality requires the sign of the first Lyapunov coefficient computed from the quadratic and cubic terms of the vector field. The transverse dynamics on the manifold must be reduced before this coefficient can be evaluated; the manuscript therefore leaves the supercriticality assertion unverified.

minor comments (1)

- The numerical validation section should specify the integration scheme, step-size control, and tolerance criteria used to compute limit-cycle periods and bifurcation thresholds, as these details are required to assess reproducibility of the asserted agreement with the three benchmark models.

Simulated Author's Rebuttal

We thank the referee for the careful reading and for identifying the precise gap between linear analysis and the determination of bifurcation criticality. We address the single major comment below.

read point-by-point responses

-

Referee: [Abstract] Abstract: the claim that 'linear stability analysis' identifies conditions for a 'supercritical Hopf bifurcation' cannot be supported by linearization alone. Linear analysis yields the crossing of a complex-conjugate pair through the imaginary axis (with the zero eigenvalue already present from the equilibrium manifold in the cash-distribution directions), but the distinction between super- and subcriticality requires the sign of the first Lyapunov coefficient computed from the quadratic and cubic terms of the vector field. The transverse dynamics on the manifold must be reduced before this coefficient can be evaluated; the manuscript therefore leaves the supercriticality assertion unverified.

Authors: We agree with the referee that linearization alone establishes only the existence of a Hopf bifurcation (transverse to the equilibrium manifold) and does not determine its criticality. The manuscript's linear stability analysis correctly identifies the parameter values at which a complex-conjugate pair crosses the imaginary axis while the remaining eigenvalues associated with the cash-distribution manifold remain at zero. However, the claim of supercriticality in the abstract and main text rests on numerical evidence of attracting limit cycles rather than an explicit computation of the first Lyapunov coefficient. In the revised manuscript we will either (i) replace the word "supercritical" with "Hopf" throughout or (ii) perform the center-manifold reduction in the transverse directions and evaluate the Lyapunov coefficient analytically, thereby rigorously confirming the bifurcation type. We view this as a necessary clarification rather than a substantive change to the model's conclusions. revision: yes

Circularity Check

No significant circularity; derivation is self-contained

full rationale

The paper derives the fused multi-asset ODE system from the three cited frameworks, establishes positivity/boundedness and the equilibrium manifold directly from the equations, and applies linear stability analysis to locate Hopf conditions. The single self-citation (Cavani 2026) occurs only in the validation section for reproducing benchmark outputs and does not serve as load-bearing justification for the new model's derivation or bifurcation claims. No self-definitional reductions, fitted inputs renamed as predictions, or ansatzes imported via citation appear in the derivation chain. The central results rest on the paper's own equations and analysis rather than reducing to prior inputs by construction.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Awartani, B., Aktham, M., & Cherif, G. (2016). The connectedness between crude oil and financial markets: Evidence from implied volatility indices. Journal of Commodity Markets, 4(1), 56-69. Bouri, E., Gupta, R., & Roubaud, D. (2021). Investor sentiment and contagion in oil and commodity markets. Energy Economics, 98, 105234. Brock, W. A., & Hommes, C. H....

-

[2]

Springer‑Verlag. Kelley, A. (1967). The stable, center ‑stable, center, center ‑unstable, and unstable manifolds. Journal of Differential Equations, 3(4), 546–570. Khalil, H. K. (2002). Nonlinear Systems (3rd ed.). Prentice Hall. Kukačka, J., & Baruník, J. (2017). Estimation of financial agent ‑based models with simulated maximum likel ihood. Journal of E...

-

[3]

Trabelsi, N., Tiwari, A

Springer‑Verlag. Trabelsi, N., Tiwari, A. K., & Hammoudeh, S. (2022). Spillovers and directional predictability between international energy commodities and their implications for optimal portfolio and hedging. The North American Journal of Economics and Finance, 62, 101715. Wang, H. (2025). Decoding momentum spillover effects. Journal of Financial and Qu...

2022

-

[4]

https://doi.org/10.1017/S002210902500124X Westerhoff, F., et al. (2025). Boom –bust cycles and asset market participation waves: Momentum, value, risk, and herding. Journal of Evolutionary Economics , 35, 513–551. https://doi.org/10.1007/s00191-025-00919-6

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.