Nonconvex High-Dimensional Time-Varying Coefficient Estimation for Noisy High-Frequency Observations with a Factor Structure

Pith reviewed 2026-05-24 04:44 UTC · model grok-4.3

The pith

The FATEN-LASSO estimator recovers integrated time-varying coefficients from noisy high-frequency data that exhibit a factor structure.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

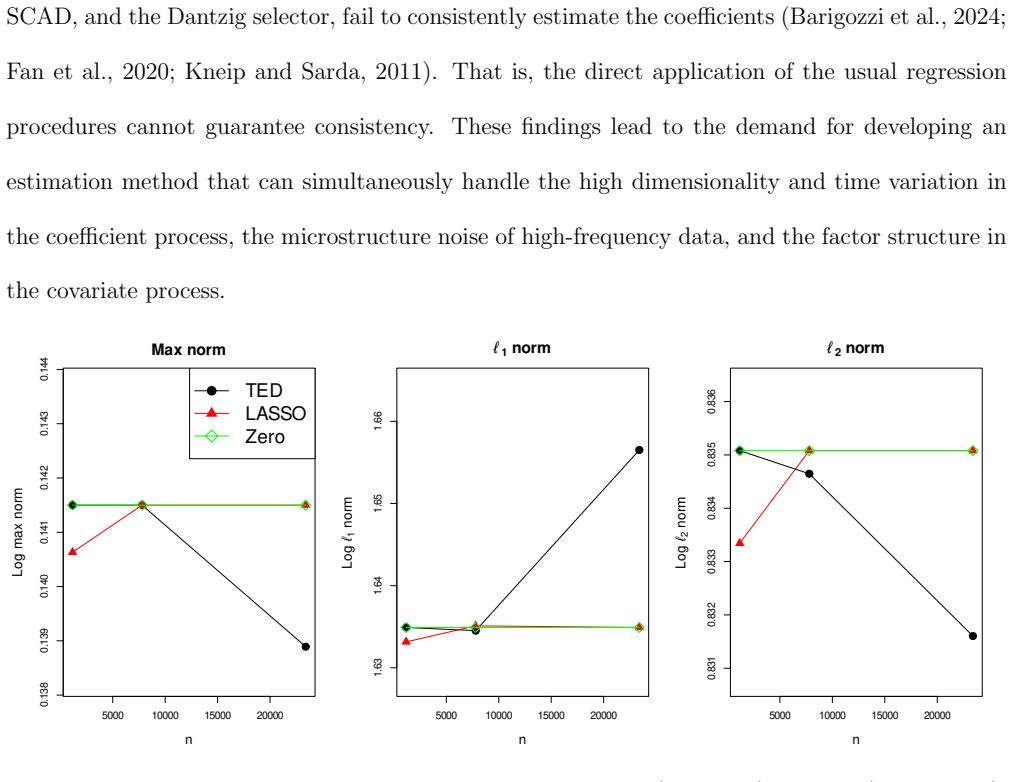

The paper proposes the Factor Adjusted Thresholded dEbiased Nonconvex LASSO (FATEN-LASSO) estimator. It first smooths the dependent and covariate processes to reduce noise, applies PCA to transform the strongly dependent covariates into a weakly dependent structure, performs nonconvex penalized regression for each local coefficient, debiases the resulting estimators to obtain integrated coefficient estimates, and finally thresholds the debiased integrated estimators to account for sparsity. The paper establishes concentration properties of the FATEN-LASSO estimator and discusses a nonconvex optimization algorithm for computing it.

What carries the argument

The FATEN-LASSO scheme, which integrates smoothing, PCA transformation, nonconvex penalized regression, debiasing of local coefficients, and thresholding of the integrated estimators.

If this is right

- Consistent estimation of both local and integrated time-varying coefficients becomes feasible under high dimensionality, noise, and factor dependence.

- The debiased and thresholded estimators satisfy concentration inequalities derived in the paper.

- A nonconvex optimization algorithm can be used to compute the local coefficient estimates.

- Thresholding after debiasing exploits sparsity to improve finite-sample performance of the integrated estimators.

Where Pith is reading between the lines

- The combination of PCA and nonconvex debiasing might be adapted to other high-frequency settings with latent factors, such as sensor networks or genomic time series.

- Empirical checks on high-frequency financial returns with documented factor structures would test whether the theoretical concentration rates translate to observable accuracy.

- If the nonconvex penalty yields lower bias than convex alternatives after debiasing, similar two-stage procedures could be explored for other sparse time-varying models.

Load-bearing premise

After smoothing and PCA, the remaining noise in the transformed variables can be managed by nonconvex penalized regression without destroying consistency of the integrated coefficient estimators.

What would settle it

A simulation or real-data experiment in which the FATEN-LASSO estimator fails to attain the claimed concentration rates on data generated with known factors and non-negligible post-PCA noise would falsify the central claims.

Figures

read the original abstract

In this paper, we propose a novel high-dimensional time-varying coefficient estimator for noisy high-frequency observations with a factor structure. In high-frequency finance, we often observe that noises dominate the signal of underlying true processes and that covariates exhibit a factor structure due to their strong dependence. Thus, we cannot apply usual regression procedures to analyze high-frequency observations. To handle the noises, we first employ a smoothing method for the observed dependent and covariate processes. Then, to handle the strong dependence of the covariate processes, we apply Principal Component Analysis (PCA) and transform the highly correlated covariate structure into a weakly correlated structure. However, the variables from PCA still contain non-negligible noises. To manage these non-negligible noises and the high dimensionality, we propose a nonconvex penalized regression method for each local coefficient. This method produces consistent but biased local coefficient estimators. To estimate the integrated coefficients, we propose a debiasing scheme and obtain a debiased integrated coefficient estimator using debiased local coefficient estimators. Then, to further account for the sparsity structure of the coefficients, we apply a thresholding scheme to the debiased integrated coefficient estimator. We call this scheme the Factor Adjusted Thresholded dEbiased Nonconvex LASSO (FATEN-LASSO) estimator. Furthermore, this paper establishes the concentration properties of the FATEN-LASSO estimator and discusses a nonconvex optimization algorithm.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes the Factor Adjusted Thresholded dEbiased Nonconvex LASSO (FATEN-LASSO) estimator for high-dimensional time-varying coefficient models under noisy high-frequency observations with factor-structured covariates. The procedure first smooths the observed processes, applies PCA to produce weakly correlated covariates, fits nonconvex penalized regressions to obtain local coefficient estimates, applies a debiasing step to recover integrated coefficients, and finally thresholds for sparsity. The paper establishes concentration properties of the resulting estimator and discusses a nonconvex optimization algorithm.

Significance. If the consistency and concentration results hold under the stated conditions, the work addresses a practically important setting in high-frequency econometrics where standard regression methods are inapplicable due to noise dominance and strong covariate dependence. The combination of smoothing, PCA-based factor adjustment, nonconvex penalties, debiasing, and integrated-scale thresholding is a coherent methodological contribution, and the provision of concentration bounds constitutes a clear theoretical strength.

minor comments (2)

- [Abstract] Abstract: the claim that the PCA-transformed variables 'still contain non-negligible noises' is used to motivate the subsequent nonconvex step, but the abstract does not indicate the precise rate at which these residual noises must vanish relative to the smoothing bandwidth; a one-sentence clarification would improve readability.

- The nonconvex optimization algorithm is mentioned but its convergence analysis or practical implementation details (e.g., choice of initialization or stopping criteria) are not summarized; adding a short dedicated paragraph would help readers assess computational feasibility.

Simulated Author's Rebuttal

We thank the referee for the positive evaluation of our work on the FATEN-LASSO estimator and for recommending minor revision. The absence of specific major comments is noted.

Circularity Check

No significant circularity identified

full rationale

The derivation consists of a sequence of distinct, sequentially applied operations: smoothing the observed processes, PCA to adjust for factor structure, nonconvex penalized regression on the resulting covariates, debiasing of the local estimators, and thresholding for sparsity. None of these steps reduce by construction to re-expressing an input parameter or fitted quantity as the output (e.g., no local coefficient is defined in terms of the integrated coefficient it is later used to estimate). The concentration properties are derived from the composed procedure rather than from any self-referential definition or self-citation that would force the result. The central estimator is therefore not equivalent to its inputs by the paper's own equations.

Axiom & Free-Parameter Ledger

free parameters (2)

- nonconvex penalty parameter

- threshold level

axioms (2)

- domain assumption Noises dominate the signal of underlying true processes and covariates exhibit a factor structure due to strong dependence.

- domain assumption After PCA the transformed variables still contain non-negligible noises that require nonconvex penalization and debiasing.

Reference graph

Works this paper leans on

-

[1]

Agarwal, A., Negahban, S., and Wainwright, M. J. (2012). Fast global convergence of gradient methods for high-dimensional statistical recovery. The Annals of Statistics , 40(5):2452–2482. A¨ ıt-Sahalia, Y., Fan, J., and Xiu, D. (2010). High-frequency covariance estimates with noisy and asynchronous financial data. Journal of the American Statistical Assoc...

work page 2012

-

[2]

A¨ ıt-Sahalia, Y., Kalnina, I., and Xiu, D. (2020). High-frequency factor models and regressions. Journal of Econometrics , 216(1):86–105. A¨ ıt-Sahalia, Y. and Xiu, D. (2017). Using principal component analysis to estimate a high dimen- sional factor model with high-frequency data. Journal of Econometrics , 201(2):384–399. 35 A¨ ıt-Sahalia, Y. and Xiu, D...

work page 2020

-

[3]

G., Cakici, N., and Whitelaw, R

Bali, T. G., Cakici, N., and Whitelaw, R. F. (2011). Maxing out: Stocks as lotteries and the cross-section of expected returns. Journal of Financial Economics , 99(2):427–446. Banz, R. W. (1981). The relationship between return and market value of common stocks. Journal of Financial Economics , 9(1):3–18. Barbee Jr, W. C., Mukherji, S., and Raines, G. A. ...

work page 2011

-

[4]

Barndorff-Nielsen, O. E., Hansen, P. R., Lunde, A., and Shephard, N. (2011). Multivariate realised kernels: consistent positive semi-definite estimators of the covariation of equity prices with noise and non-synchronous trading. Journal of Econometrics , 162(2):149–169. Barndorff-Nielsen, O. E. and Shephard, N. (2004). Econometric analysis of realized cov...

-

[5]

Cooper, M. J., Gulen, H., and Schill, M. J. (2008). Asset growth and the cross-section of stock returns. the Journal of Finance , 63(4):1609–1651. Dai, C., Lu, K., and Xiu, D. (2019). Knowing factors or factor loadings, or neither? evaluating esti- mators of large covariance matrices with noisy and asynchronous data. Journal of Econometrics, 208(1):43–79....

-

[6]

Loh, P.-L. and Wainwright, M. J. (2012). High-dimensional regression with noisy and missing data: Provable guarantees with nonconvexity. The Annals of Statistics , 40(3):1637–1664. Loughran, T. and Wellman, J. W. (2011). New evidence on the relation between the enterprise multiple and average stock returns. Journal of Financial and Quantitative Analysis ,...

work page 2012

-

[7]

Lyandres, E., Sun, L., and Zhang, L. (2008). The new issues puzzle: Testing the investment-based explanation. The Review of Financial Studies , 21(6):2825–2855. McLean, R. D. and Pontiff, J. (2016). Does academic research destroy stock return predictability? The Journal of Finance , 71(1):5–32. 42 Miller, M. H. and Scholes, M. S. (1982). Dividends and tax...

-

[8]

and the momentum factor (Carhart, 1997), we first obtained the monthly portfolio constituents among the stocks traded on the NYSE, NASDAQ, and AMEX. Specifically, we obtained MKT as the return of a value-weighted portfolio 48 5000 10000 15000 20000 -1.0 -0.5 0.0 0.5 1.0 Max norm n Log max norm FATEN-LASSO FATEC-LASSO TEN-LASSO TEC-LASSO 5000 10000 15000 2...

work page 1997

-

[9]

We used the same factor symbols as those in Jensen et al. (2023). Group Symbol Description CitationValue at me Assets-to-market Fama and French (1992)beme Book-to-market equity Rosenberg et al. (1985)bevmev Book-to-market enterprise value Penman et al. (2007)chcsho12m Net stock issues Pontiff and Woodgate (2008)debtme Debt-to-market Bhandari (1988)div12mm...

work page 2023

-

[10]

Table 5: Annual average in-sample and out-of-sample R2 for the FATEN-LASSO, FATEC-LASSO, TEN-LASSO, and TEC-LASSO estimators over the five assets. In-sampleR2 Estimator FATEN-LASSO FATEC-LASSO TEN-LASSO TEC-LASSO whole period 0.344 0.312 0.345 0.312 2013 0.322 0.318 0.324 0.320 2014 0.327 0.306 0.328 0.306 2015 0.322 0.256 0.325 0.256 2016 0.351 0.311 0.3...

work page 2013

-

[11]

, p}, define AU = {β ∈ Rp | ∥ β∥2 ≤ 1, supp (β) ⊂ U }

For any subset U ⊂ {1, . . . , p}, define AU = {β ∈ Rp | ∥ β∥2 ≤ 1, supp (β) ⊂ U } . By (A.57) and discretization argument in Lemma 15 (Loh and Wainwright, 2012), for any AU with |U | ≤ s, we have, with the probability at least 1 − 9s exp −c3n1/4 , sup β∈AU β⊤ n ϕk1k2 Ui + E X i ⊤ Ui + E X i − Σ0,u(i∆n) − nζ ϕk1 VX β ≤ λmin {Σ0,g (i∆n)} 216 . Note that Ks...

work page 2012

-

[12]

Thus, we have Pr (I) ≤ λmin {Σ0,g (i∆n)} 108 ≥ 1 − 6p−2−a

logp for large n, we have exp −c3n1/4 + s log 9p + 5p−2−a ≤ exp −c3n1/4 + c3n1/4/2 + 5p−2−a ≤ 6p−2−a. Thus, we have Pr (I) ≤ λmin {Σ0,g (i∆n)} 108 ≥ 1 − 6p−2−a. (A.66) Similarly, for the same s, we can show Pr (II ) + (III ) + (IV ) ≤ λmin {Σ0,g (i∆n)} 108 ≥ 1 − 6p−2−a. (A.67) From (A.55), (A.66), and (A.67), we have Pr ( sup θ∈Ks+r 1 θ⊤ ∇2Li(θ) − Σ0,g(i∆...

work page 2012

-

[13]

To obtain the upper bound for ∥cIβ − Iβ0∥max, we first investigate bΩi∆n. We have sup 0≤i≤n−k2 n ϕk1k2 bU⊤ i bUi − nζ ϕk1 bVX Ω0 (i∆n) − I max ≤ sup 0≤i≤n−k2 n ϕk1k2 bU⊤ i bUi − nζ ϕk1 bVX − Σ0,u (i∆n) max × sup 0≤i≤n−k2 ∥Ω0 (i∆n)∥1 . By the proofs of (A.42), we can show, with the probability at least 1 − p−2−a, sup 0≤i≤n−k2 n ϕk1k2 bU⊤ i bUi − nζ ϕk1 bVX...

work page 2024

-

[14]

92 Thus, it suffices to show the statement under {∥cIβ − Iβ0∥max ≤ hn/2}

By (3.13), there exists a constant Ch such that Pr n ∥cIβ − Iβ0∥max ≤ hn/2 o ≥ 1 − p−a. 92 Thus, it suffices to show the statement under {∥cIβ − Iβ0∥max ≤ hn/2}. Similar to the proofs of Theorem 1 (Kim et al., 2024), we can obtain ∥fIβ − Iβ0∥1 ≤ Cs phn. Also, (3.15) is obtained by (3.11). ■ A.9 Proof of Proposition 1 Proof of Proposition

work page 2024

-

[15]

By Proposition 5, we can show Proposition 1 similar to the proofs of Theorem 2 (Agarwal et al., 2012). ■ 93 A.10 Miscellaneous materials Algorithm 1 FATEN-LASSO estimation procedure Step 1 Estimate the factor loading matrix and smoothed latent factor variable: (bBi∆n ,bFi) = arg min B∈Rp×r,F∈R(k2 −k1 +1)×r ∥Xi − FB⊤∥2 F , subject to p−1B⊤B = Ir and F⊤F is...

work page 2012

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.