Forecasting Commencing Enrolments Under Data Sparsity: A Zero-Shot Time Series Foundation Models Framework for Higher Education Planning

Pith reviewed 2026-05-16 02:29 UTC · model grok-4.3

The pith

Covariate-conditioned zero-shot time series models match classical methods for forecasting university enrolments with sparse data.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The paper establishes that zero-shot TSFMs conditioned on a leakage-safe covariate protocol that integrates feature-engineered Google Trends with the Institutional Operating Conditions Index achieve accuracy competitive with or better than classical statistical baselines in expanding-window backtests that respect real decision timing, thereby supplying usable enrolment forecasts without requiring bespoke model training at each institution.

What carries the argument

Zero-shot Time Series Foundation Models conditioned through a leakage-safe covariate protocol that combines Google Trends features with the Institutional Operating Conditions Index to detect environmental regime shifts.

If this is right

- University administrators can obtain enrolment forecasts without assembling long internal time series or training custom models.

- The same protocol supplies auditable forecasts under structural instability such as policy changes or economic shocks.

- Forecast quality varies with cohort type and the precise design of the covariates, so institutions must still validate the approach locally.

- The method reduces the barrier to using advanced time-series tools for operational planning in data-poor settings.

Where Pith is reading between the lines

- The protocol could transfer to other domains that forecast sparse event counts such as course registrations or campus facility usage.

- Institutions might embed the conditioned models inside existing planning dashboards to produce scenario-based enrolment ranges.

- The Institutional Operating Conditions Index itself may function as a reusable regime indicator for forecasting in adjacent sectors.

- Further tests on multi-year horizons or international datasets would clarify the limits of zero-shot performance under different sparsity levels.

Load-bearing premise

The Google Trends and Institutional Operating Conditions Index covariates reflect genuine environmental changes without any future data leaking into the forecast at the time of decision.

What would settle it

An expanding-window backtest on a fresh collection of institutions in which the zero-shot models produce materially higher forecast errors than the classical baselines across multiple cohorts would refute the claim of competitiveness.

Figures

read the original abstract

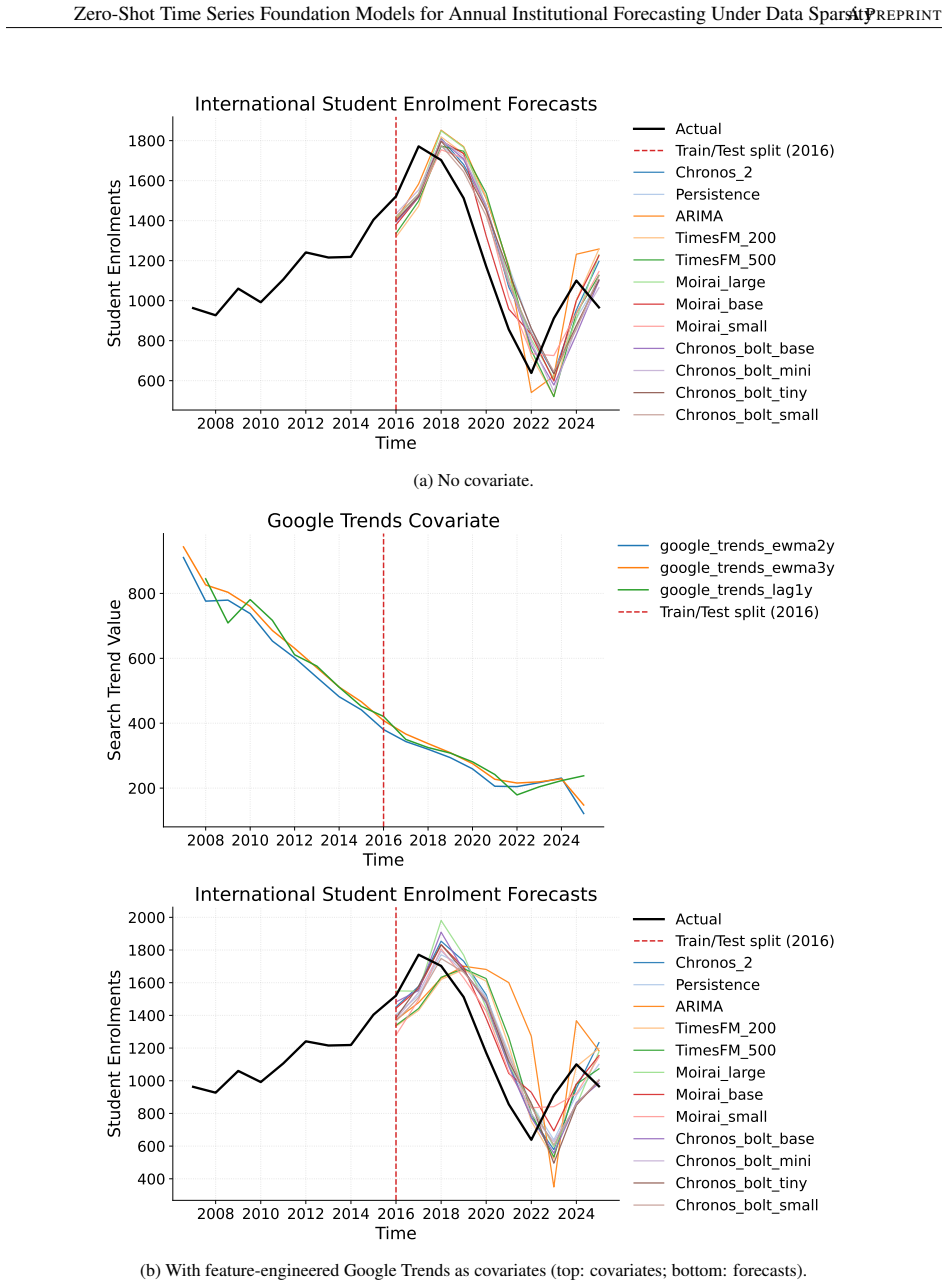

Effective resource allocation in higher education depends on reliable enrolment forecasts, yet institutional planners frequently face data series disrupted by structural shifts. This paper investigates whether zero-shot Time Series Foundation Models (TSFMs) can provide rigorous decision support for annual enrolment forecasting under severe data sparsity. We benchmark multiple TSFMs against classical operational baselines using an expanding-window backtest that mirrors decision-time constraints. To capture environmental shifts without look-ahead bias, we introduce a leakage-safe covariate protocol that integrates feature-engineered Google Trends with the Institutional Operating Conditions Index (IOCI), a transferable regime measure extracted from historical narrative evidence. Our evaluation demonstrates that covariate-conditioned TSFMs are competitive with classical methods and can improve accuracy without requiring bespoke institutional training. However, the operational benefits depend on cohort characteristics and covariate design. This study provides an auditable and transferable forecasting protocol for operational researchers and university administrators, helping institutions determine when context-aware forecasting adds practical value under limited data and structural instability.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that zero-shot Time Series Foundation Models (TSFMs) conditioned on a leakage-safe covariate protocol—combining feature-engineered Google Trends with the Institutional Operating Conditions Index (IOCI) derived from historical narratives—can deliver competitive annual enrolment forecasts for higher education under severe data sparsity. It supports this via an expanding-window backtest that mirrors decision-time constraints, showing accuracy gains over classical baselines without requiring bespoke institutional training, while noting that benefits vary by cohort and covariate design.

Significance. If the central claim holds after verification, the work offers practical value for operational researchers and university administrators by providing an auditable, transferable forecasting protocol that leverages foundation models in zero-shot settings. This addresses a real gap in higher-education planning where data series are short and disrupted by structural shifts, potentially improving resource allocation without extensive custom modeling.

major comments (2)

- [Abstract and Evaluation] Abstract and Evaluation section: The expanding-window backtest description does not explicitly document the precise lag structure for Google Trends and IOCI alignment to each forecast origin (e.g., truncation of Google Trends to the last date known at origin, enforcement of IOCI narrative extraction windows, and whether any smoothing or feature engineering uses post-origin data). This documentation is load-bearing for the no-look-ahead-bias claim and the reported accuracy improvements.

- [Covariate Protocol] Covariate Protocol subsection: The claim that the protocol 'captures environmental shifts without look-ahead bias' requires concrete verification steps (e.g., pseudocode or explicit rules for origin-aligned feature construction) because any inadvertent post-origin information would invalidate the competitiveness result relative to classical methods.

minor comments (2)

- [Abstract] Abstract: Specify the exact TSFMs and classical baselines compared, along with the performance metrics used (e.g., MAE, RMSE) to allow readers to assess the 'competitive' claim quantitatively.

- [Introduction] Notation: Define IOCI more formally on first use, including its construction from narrative evidence, to improve transferability for other institutions.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which correctly identify areas where additional methodological transparency is needed to fully substantiate our no-look-ahead-bias claims. We address each point below and will revise the manuscript to incorporate the requested documentation.

read point-by-point responses

-

Referee: [Abstract and Evaluation] Abstract and Evaluation section: The expanding-window backtest description does not explicitly document the precise lag structure for Google Trends and IOCI alignment to each forecast origin (e.g., truncation of Google Trends to the last date known at origin, enforcement of IOCI narrative extraction windows, and whether any smoothing or feature engineering uses post-origin data). This documentation is load-bearing for the no-look-ahead-bias claim and the reported accuracy improvements.

Authors: We agree that the current description of the expanding-window backtest is insufficiently detailed on lag structures and alignment. In the revised manuscript we will expand the Evaluation section with explicit rules and pseudocode for origin-aligned feature construction. Google Trends series will be truncated to the last date known at each forecast origin; IOCI narrative extraction will be restricted to historical windows ending at the origin; and all smoothing or feature engineering steps will be confirmed to use only pre-origin data. These additions will make the no-look-ahead-bias claim directly verifiable. revision: yes

-

Referee: [Covariate Protocol] Covariate Protocol subsection: The claim that the protocol 'captures environmental shifts without look-ahead bias' requires concrete verification steps (e.g., pseudocode or explicit rules for origin-aligned feature construction) because any inadvertent post-origin information would invalidate the competitiveness result relative to classical methods.

Authors: We concur that concrete verification steps are required. The revised Covariate Protocol subsection will include pseudocode together with step-by-step rules for origin-aligned construction. These will specify truncation of Google Trends to information available at the origin, restriction of IOCI extraction to pre-origin narratives, and explicit checks confirming that no post-origin data enters feature engineering. This documentation will directly support the validity of the reported competitiveness results. revision: yes

Circularity Check

No circularity: empirical benchmark protocol is self-contained

full rationale

The paper describes an expanding-window backtest and a leakage-safe covariate protocol (Google Trends + IOCI) for zero-shot TSFM evaluation. No equations, fitted parameters renamed as predictions, or self-citation chains appear in the provided text. The central claim rests on external benchmark comparisons whose inputs (historical enrolment series, narrative-derived IOCI) are independent of the reported accuracy numbers. This is the expected non-finding for an applied forecasting study.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption IOCI is a transferable regime measure extracted from historical narrative evidence that captures environmental shifts

invented entities (1)

-

Institutional Operating Conditions Index (IOCI)

no independent evidence

Reference graph

Works this paper leans on

-

[1]

I-Hong Kuo, Shi-Jinn Horng, Tzong-Wann Kao, Tsung-Lieh Lin, Cheng-Ling Lee, and Yi Pan. An improved method for forecasting enrollments based on fuzzy time series and particle swarm optimization.Expert Systems with Applications, 36(3, Part 2):6108–6117, 2009. ISSN 0957-4174. doi:10.1016/j.eswa.2008.07.043. URL https://www.sciencedirect.com/science/article/...

-

[2]

Yao-Lin Huang, Shi-Jinn Horng, Mingxing He, Pingzhi Fan, Tzong-Wann Kao, Muhammad Khurram Khan, Jui-Lin Lai, and I-Hong Kuo. A hybrid forecasting model for enrollments based on aggregated fuzzy time series and particle swarm optimization.Expert Systems with Applications, 38(7):8014–8023, 2011. ISSN 0957-

work page 2011

-

[3]

URL https://www.sciencedirect.com/science/article/pii/ S0957417410014909

doi:10.1016/j.eswa.2010.12.127. URL https://www.sciencedirect.com/science/article/pii/ S0957417410014909

-

[4]

Examining the relationship between institutional financial stress and stu- dent enrollment

Robert Kelchen and Holly Evans. Examining the relationship between institutional financial stress and stu- dent enrollment. Working Paper 24-05, Federal Reserve Bank of Philadelphia, July 2024. URL https: //robertkelchen.com/wp-content/uploads/2024/07/hcm_enrollment_jul24.pdf

work page 2024

-

[5]

Johns Hopkins University Press, Baltimore, MD, 2018

Nathan D Grawe.Demographics and the Demand for Higher Education. Johns Hopkins University Press, Baltimore, MD, 2018

work page 2018

-

[6]

Kelli A Bird. Predictive analytics in higher education: The promises and challenges of using machine learning to improve student success.AIR Professional File, (161):1–18, 2023. URL https://www.airweb.org/ docs/default-source/aha/apf-161-predictive-analytics-in-higher-education.pdf?sfvrsn= f31dcce4_1

work page 2023

-

[7]

K Willis and P Yang. Towards redefining strategic enrollment management: Response to emerging challenges of the 21st century.Journal of Advancing Education Practice, 5(2):45–58, 2024. URL https://openriver. winona.edu/jaep/vol5/iss2/7/

work page 2024

-

[8]

Wald,General Relativity, Chicago Univ

Bridget Terry Long.The Financial Crisis and College Enrollment: How Have Students and Their Families Responded?, pages 209–233. University of Chicago Press, January 2014. doi:10.7208/chicago/9780226201979.003.0007. URLhttp://www.nber.org/chapters/c12862

-

[9]

Thomas C. Sharkey, Steven Foster, Sudeep Hegde, Mary E. Kurz, and Emily L. Tucker. A categoriza- tion of observed uses of operational research models for fundamental surprise events: Observations from university operations during covid-19.Journal of the Operational Research Society, 76(2):254–266, 2025. doi:10.1080/01605682.2024.2346117. URLhttps://doi.or...

-

[10]

J M Mendez et al. Analyzing and forecasting enrolment patterns using time series models.International Journal of Advanced Computer Science, 12(1):102–115, 2025

work page 2025

-

[11]

The financial sustainability of higher educa- tion: Insights from policy in oecd countries, 2025

Organisation for Economic Co-operation and Development. The financial sustainability of higher educa- tion: Insights from policy in oecd countries, 2025. URL https://www.oecd.org/en/publications/ the-financial-sustainability-of-higher-education_f544ccfe-en.html . Published 24 November 2025

work page 2025

-

[12]

Education at a glance 2024: Oecd indi- cators, 2024

Organisation for Economic Co-operation and Development. Education at a glance 2024: Oecd indi- cators, 2024. URL https://www.oecd-ilibrary.org/education/education-at-a-glance-2024_ c00cad36-en. Published 10 September 2024

work page 2024

-

[13]

Elliot N. Maltz, Kenneth E. Murphy, and Michael L. Hand. Decision support for university enrollment man- agement: Implementation and experience.Decision Support Systems, 44(1):106–123, 2007. ISSN 0167-

work page 2007

-

[14]

URL https://www.sciencedirect.com/science/article/pii/ S016792360700053X

doi:10.1016/j.dss.2007.03.008. URL https://www.sciencedirect.com/science/article/pii/ S016792360700053X. 21 Zero-Shot Time Series Foundation Models for Annual Institutional Forecasting Under Data SparsityA PREPRINT

-

[15]

Xinshuai Li, Senlin Luo, Limin Pan, and Zhouting Wu. Adapt to small-scale and long-term time series forecasting with enhanced multidimensional correlation.Expert Systems with Applications, 238:122203, 2024. ISSN 0957-

work page 2024

-

[16]

URL https://www.sciencedirect.com/science/article/pii/ S0957417423027057

doi:10.1016/j.eswa.2023.122203. URL https://www.sciencedirect.com/science/article/pii/ S0957417423027057

-

[17]

Spyros Makridakis, Evangelos Spiliotis, and Vassilios Assimakopoulos. The m4 competition: 100,000 time series and 61 forecasting methods.International Journal of Forecasting, 36(1):54–74, 2020. ISSN 0169-

work page 2020

-

[18]

URL https://www.sciencedirect.com/science/article/ pii/S0169207019301128

doi:10.1016/j.ijforecast.2019.04.014. URL https://www.sciencedirect.com/science/article/ pii/S0169207019301128. M4 Competition

-

[19]

Christoph Bergmeir, Rob J. Hyndman, and Bonsoo Koo. A note on the validity of cross-validation for evaluating autoregressive time series prediction.Computational Statistics & Data Analysis, 120:70–83, 2018. ISSN 0167-

work page 2018

-

[20]

URL https://www.sciencedirect.com/science/article/pii/ S0167947317302384

doi:10.1016/j.csda.2017.11.003. URL https://www.sciencedirect.com/science/article/pii/ S0167947317302384

-

[21]

Daniel Bolaños-Martinez, Alberto Durán-López, Jose Luis Garrido, Blanca Delgado-Márquez, and Maria Bermudez-Edo. Sasd: Self-attention for small datasets—a case study in smart villages.Expert Systems with Applications, 271:126245, 2025. ISSN 0957-4174. doi:10.1016/j.eswa.2024.126245. URL https: //www.sciencedirect.com/science/article/pii/S0957417424031129

-

[22]

Abdul Fatir Ansari, Lorenzo Stella, Caner Turkmen, Xiyuan Zhang, Pedro Mercado, Huibin Shen, Oleksandr Shchur, Syama Syndar Rangapuram, Sebastian Pineda Arango, Shubham Kapoor, Jasper Zschiegner, Danielle C. Maddix, Michael W. Mahoney, Kari Torkkola, Andrew Gordon Wilson, Michael Bohlke-Schneider, and Yuyang Wang. Chronos: Learning the language of time se...

work page 2024

-

[23]

A decoder-only foundation model for time-series forecasting

Abhimanyu Das, Weihao Kong, Rajat Sen, and Yichen Zhou. A decoder-only foundation model for time-series forecasting. InProceedings of the 41st International Conference on Machine Learning (ICML), volume 235 of Proceedings of Machine Learning Research, pages 9510–9529. PMLR, 2024. URL https://proceedings. mlr.press/v235/das24c.html

work page 2024

-

[24]

Unified training of universal time series forecasting transformers

Gerald Woo, Chenghao Liu, Akshat Kumar, Caiming Xiong, Silvio Savarese, and Doyen Sahoo. Unified training of universal time series forecasting transformers. InForty-first International Conference on Machine Learning, 2024

work page 2024

-

[25]

Hyunyoung Choi and Hal R. Varian. Predicting the present with google trends.Economic Record, 88(s1):2–9,

-

[26]

doi:10.1111/j.1475-4932.2012.00809.x

-

[27]

Luis Gruber and Gregor Kastner. Forecasting macroeconomic data with bayesian vars: Sparse or dense? it depends!International Journal of Forecasting, 41(4):1589–1619, 2025. ISSN 0169-2070. doi:https://doi.org/10.1016/j.ijforecast.2025.02.001. URL https://www.sciencedirect.com/science/ article/pii/S0169207025000081

-

[28]

Eichenauer, Ronald Indergand, Isabel Z

Vera Z. Eichenauer, Ronald Indergand, Isabel Z. MartÃnez, and Christoph Sax. Obtaining consistent time series from google trends.Economic Inquiry, 60(2):694–705, April 2022. doi:10.1111/ecin.13049. URL https://ideas.repec.org/a/bla/ecinqu/v60y2022i2p694-705.html

-

[29]

Justin Grimmer and Brandon M. Stewart. Text as data: The promise and pitfalls of automatic content analysis methods for political texts.Political Analysis, 21(3):267–297, 2013. doi:10.1093/pan/mps028

-

[30]

Baker, Nicholas Bloom, and Steven J

Scott R. Baker, Nicholas Bloom, and Steven J. Davis. Measuring economic policy uncertainty*.The Quarterly Journal of Economics, 131(4):1593–1636, 07 2016. ISSN 0033-5533. doi:10.1093/qje/qjw024. URL https: //doi.org/10.1093/qje/qjw024

-

[31]

William J. Webster. The cohort-survival ratio method in the projection of school attendance.The Journal of Experimental Education, 39(1):89–96, 1970. doi:10.1080/00220973.1970.11011238. URL https://doi.org/ 10.1080/00220973.1970.11011238

-

[32]

Giacomo Sbrana and Paolo Antonetti. Persistence modeling for sales prediction: A simple, self-contained approach.Journal of Business Research, 166:114103, 2023. ISSN 0148-2963. doi:10.1016/j.jbusres.2023.114103. URLhttps://www.sciencedirect.com/science/article/pii/S0148296323004617

-

[33]

S.L. Ho and M. Xie. The use of arima models for reliability forecasting and analysis.Computers & Industrial Engineering, 35(1):213–216, 1998. ISSN 0360-8352. doi:10.1016/S0360-8352(98)00066-7. URL https: //www.sciencedirect.com/science/article/pii/S0360835298000667

-

[34]

Yu Chen, Ran Li, and Linda Serra Hagedorn. Undergraduate international student enrollment forecasting model: An application of time series analysis.Journal of International Students, 9(1):242–261, Jan. 2019. doi:10.32674/jis.v9i1.266. URLhttps://ojed.org/jis/article/view/266. 22 Zero-Shot Time Series Foundation Models for Annual Institutional Forecasting ...

-

[35]

James H Stock and Mark W Watson. Macroeconomic forecasting using diffusion indexes.Journal of Business & Economic Statistics, 20(2):147–162, 2002. doi:10.1198/073500102317351921. URL https://doi.org/10. 1198/073500102317351921

-

[36]

Tianyu Shen, James Raymer, and Caroline Hendy. Forecasting school enrollments in the australian capital territory.Journal of the Royal Statistical Society Series A: Statistics in Society, 188(4):1107–1124, 10 2024. ISSN 0964-1998. doi:10.1093/jrsssa/qnae094. URLhttps://doi.org/10.1093/jrsssa/qnae094

-

[37]

Marco Caserta and Luca D’Angelo. Intermittent demand forecasting for spare parts with little historical informa- tion.Journal of the Operational Research Society, 76(2):294–309, 2025. doi:10.1080/01605682.2024.2349734. URLhttps://doi.org/10.1080/01605682.2024.2349734

-

[38]

Wanli Xie, Chong Liu, and Wen-Ze Wu. A novel fractional grey system model with non-singular exponen- tial kernel for forecasting enrollments.Expert Systems with Applications, 219:119652, 2023. ISSN 0957-

work page 2023

-

[39]

URL https://www.sciencedirect.com/science/article/pii/ S0957417423001537

doi:10.1016/j.eswa.2023.119652. URL https://www.sciencedirect.com/science/article/pii/ S0957417423001537

-

[40]

Andrew Barr and Sarah E. Turner. Out of work and into school: Labor market policies and college enrollment during the great recession.Journal of Public Economics, 127:63–73, 2015. doi:10.1016/j.jpubeco.2015.04.002

-

[41]

Nikos Askitas and Klaus F. Zimmermann. Google econometrics and unemployment forecasting. RatSWD Research Notes 41, German Council for Social and Economic Data (RatSWD), June 2009. URL https: //ssrn.com/abstract=1480251. Available at SSRN

work page 2009

-

[42]

Adam Hale Shapiro, Moritz Sudhof, and Daniel J. Wilson. Measuring news sentiment.Journal of Econo- metrics, 228(2):221–243, 2022. ISSN 0304-4076. doi:10.1016/j.jeconom.2020.07.053. URL https://www. sciencedirect.com/science/article/pii/S0304407620303535

-

[43]

C. Ilin et al. Public mobility data enables covid-19 forecasting and management at local and global scales. Scientific Reports, 11:13531, 2021. doi:10.1038/s41598-021-92866-z

-

[44]

Hush, Tushar Ojha, and Terry Babbitt

Ahmad Slim, Don R. Hush, Tushar Ojha, and Terry Babbitt. Predicting student enrollment based on student and college characteristics. InEducational Data Mining, 2018. URL https://api.semanticscholar.org/ CorpusID:52173545

work page 2018

-

[45]

Konstantinos Nikolopoulos, Akrivi Litsa, Fotios Petropoulos, Vasileios Bougioukos, and Marwan Khammash. Relative performance of methods for forecasting special events.Journal of Business Research, 68(8):1785–1791,

-

[46]

doi:https://doi.org/10.1016/j.jbusres.2015.03.037

ISSN 0148-2963. doi:https://doi.org/10.1016/j.jbusres.2015.03.037. URL https://www.sciencedirect. com/science/article/pii/S0148296315001551. Special Issue on Simple Versus Complex Forecasting

-

[47]

Zheqi Wang, Jonathan Crook, and Galina Andreeva. Improving the accuracy of credit scoring models using an innovative bayesian informative prior specification method.Journal of the Operational Research Society, 76(2): 229–253, 2025. doi:10.1080/01605682.2024.2339510. URL https://doi.org/10.1080/01605682.2024. 2339510

-

[48]

Özgür Arik, Nicolas Loeff, and Tomas Pfister

Bryan Lim, S. Özgür Arik, Nicolas Loeff, and Tomas Pfister. Temporal fusion transformers for inter- pretable multi-horizon time series forecasting.International Journal of Forecasting, 37(4):1748–1764, 2021. doi:10.1016/j.ijforecast.2021.03.012

-

[49]

Robert Goodell Brown.Statistical Forecasting for Inventory Control. McGraw-Hill, New York, 1959

work page 1959

-

[50]

Maximilian Christ, Nils Braun, Julius Neuffer, and Andreas W. Kempa-Liehr. Time series feature extraction on basis of scalable hypothesis tests (tsfresh – a python package).Neurocomputing, 307:72–77, 2018. ISSN 0925-

work page 2018

-

[51]

URL https://www.sciencedirect.com/science/article/ pii/S0925231218304843

doi:10.1016/j.neucom.2018.03.067. URL https://www.sciencedirect.com/science/article/ pii/S0925231218304843

-

[52]

Andrew Halterman and Katherine A. Keith. Codebook llms: Evaluating llms as measurement tools for political science concepts.Political Analysis, page 1–17, September 2025. ISSN 1476-4989. doi:10.1017/pan.2025.10017. URLhttp://dx.doi.org/10.1017/pan.2025.10017

-

[53]

Shujie Wu, Yao Zhang, YiWei Yang, Zhen Li, GuangYu Yu, Long Chen, Jianwei Xu, and Aziguli Wulamu. Lgtime: Leveraging llms with feature-aware processing and multi-granularity fusion for zero-shot time series forecasting. Expert Systems with Applications, 297:129483, 2026. ISSN 0957-4174. doi:10.1016/j.eswa.2025.129483. URL https://www.sciencedirect.com/sci...

-

[54]

Jonathan Mellon, Jack Bailey, Ralph Scott, James Breckwoldt, Marta Miori, and Phillip Schmedeman. Do ais know what the most important issue is? using language models to code open-text social survey responses at scale.Research & Politics, 11(1):20531680241231468, 2024. doi:10.1177/20531680241231468. URL https://doi.org/10.1177/20531680241231468. 23 Zero-Sh...

-

[55]

From text to quantified insights: A large-scale llm analysis of central bank communication, 2025

Thiago Christiano Silva, Kei Moriya, and Romain M Veyrune. From text to quantified insights: A large-scale llm analysis of central bank communication, 2025. URL https://www.elibrary.imf.org/view/journals/ 001/2025/109/001.2025.issue-109-en.xml

work page 2025

-

[56]

Shubham Atreja, Joshua Ashkinaze, Lingyao Li, Julia Mendelsohn, and Libby Hemphill. What’s in a prompt?: A large-scale experiment to assess the impact of prompt design on the compliance and accuracy of llm-generated text annotations.Proceedings of the International AAAI Conference on Web and Social Media, 19:122–145, June

-

[57]

ISSN 2162-3449. doi:10.1609/icwsm.v19i1.35807. URL http://dx.doi.org/10.1609/icwsm.v19i1. 35807

-

[58]

Miranda-Belmonte, Victor Muñiz-Sánchez, and Francisco Corona

Hairo U. Miranda-Belmonte, Victor Muñiz-Sánchez, and Francisco Corona. Word embeddings for topic modeling: An application to the estimation of the economic policy uncertainty index.Expert Systems with Applications, 211: 118499, 2023. ISSN 0957-4174. doi:10.1016/j.eswa.2022.118499. URL https://www.sciencedirect.com/ science/article/pii/S0957417422015822

-

[59]

Foundation models for time series: A survey, 2025

Siva Rama Krishna Kottapalli, Karthik Hubli, Sandeep Chandrashekhara, Garima Jain, Sunayana Hubli, Gayathri Botla, and Ramesh Doddaiah. Foundation models for time series: A survey, 2025. URLhttps://arxiv.org/ abs/2504.04011

-

[60]

Jittarin Jetwiriyanon, Teo Susnjak, and Surangika Ranathunga. Generalisation bounds of zero-shot economic forecasting using time series foundation models.Machine Learning and Knowledge Extraction, 7(4), 2025. ISSN 2504-4990. doi:10.3390/make7040135. URLhttps://www.mdpi.com/2504-4990/7/4/135

-

[61]

Cheng Feng, Long Huang, and Denis Krompass. General time transformer: an encoder-only foundation model for zero-shot multivariate time series forecasting. InProceedings of the 33rd ACM International Conference on Information and Knowledge Management, CIKM ’24, page 3757–3761, New York, NY , USA, 2024. Association for Computing Machinery. ISBN 979840070436...

- [62]

-

[63]

Banglore Vijay Kumar Vishwas and Sri Ram Macharla.TimesFM: Time Series Forecasting Using Decoder-Only Foundation Model, pages 195–210. Apress, Berkeley, CA, 2025. ISBN 979-8-8688-1276-7. doi:10.1007/979-8- 8688-1276-7_8

-

[64]

Chronos-2: From Univariate to Universal Forecasting

Abdul Fatir Ansari, Oleksandr Shchur, Jaris Küken, Andreas Auer, Boran Han, Pedro Mercado, Syama Sundar Rangapuram, Huibin Shen, Lorenzo Stella, Xiyuan Zhang, Mononito Goswami, Shubham Kapoor, Danielle C. Maddix, Pablo Guerron, Tony Hu, Junming Yin, Nick Erickson, Prateek Mutalik Desai, Hao Wang, Huzefa Rangwala, George Karypis, Yuyang Wang, and Michael B...

work page internal anchor Pith review Pith/arXiv arXiv 2025

-

[65]

Wolff, Shenghao Yang, Kari Torkkola, and Michael W

Malcolm L. Wolff, Shenghao Yang, Kari Torkkola, and Michael W. Mahoney. Using pre-trained llms for multivariate time series forecasting, 2025. URLhttps://arxiv.org/abs/2501.06386

-

[66]

Units: A unified multi-task time series model

Shanghua Gao, Teddy Koker, Owen Queen, Thomas Hartvigsen, Theodoros Tsiligkaridis, and Marinka Zitnik. Units: A unified multi-task time series model. In A. Globerson, L. Mackey, D. Belgrave, A. Fan, U. Paquet, J. Tomczak, and C. Zhang, editors,Advances in Neural Information Processing Systems, volume 37, pages 140589– 140631. Curran Associates, Inc., 2024...

-

[67]

Ricardo Caetano, José Manuel Oliveira, and Patrícia Ramos. Transformer-based models for probabilistic time series forecasting with explanatory variables.Mathematics, 13(5), 2025. ISSN 2227-7390. doi:10.3390/math13050814. URLhttps://www.mdpi.com/2227-7390/13/5/814

-

[68]

Marcelo C. Medeiros and Henrique F. Pires. The proper use of google trends in forecasting models, 2021. URL https://arxiv.org/abs/2104.03065

-

[69]

David Kohns and Arnab Bhattacharjee. Nowcasting growth using google trends data: A bayesian struc- tural time series model.International Journal of Forecasting, 39(3):1384–1412, 2023. ISSN 0169-2070. doi:https://doi.org/10.1016/j.ijforecast.2022.05.002. URL https://www.sciencedirect.com/science/ article/pii/S0169207022000620

-

[70]

Restoring the forecasting power of google trends with statistical preprocessing, 2025

Candice Djorno, Mauricio Santillana, and Shihao Yang. Restoring the forecasting power of google trends with statistical preprocessing, 2025. URLhttps://arxiv.org/abs/2504.07032

-

[71]

Spyros Makridakis and Michèle Hibon. The m3-competition: Results, conclusions and implications.International Journal of Forecasting, 16(4):451–476, 2000. doi:10.1016/S0169-2070(00)00057-1. 24 Zero-Shot Time Series Foundation Models for Annual Institutional Forecasting Under Data SparsityA PREPRINT

-

[72]

James D. Hamilton.Time Series Analysis. Princeton University Press, 1994

work page 1994

-

[73]

Time series analysis: Forecasting and control, 5th edition , by george e

Granville Tunnicliffe Wilson. Time series analysis: Forecasting and control, 5th edition , by george e. p. box , gwilym m. jenkins , gregory c. reinsel and greta m. ljung , 2015 . published by john wiley and sons inc. , hoboken, n.Journal of Time Series Analysis, 37(5):709–711, September 2016. URL https://ideas.repec.org/a/ bla/jtsera/v37y2016i5p709-711.html

work page 2015

-

[74]

Peter Kennedy. Forecasting with dynamic regression models: Alan pankratz, 1991, (john wiley and sons, new york), isbn 0-471-61528-5, [uk pound]47.50.International Journal of Forecasting, 8(4):647–648, December 1992. URLhttps://ideas.repec.org/a/eee/intfor/v8y1992i4p647-648.html

work page 1991

-

[75]

Leonard J. Tashman. Out-of-sample tests of forecasting accuracy.International Journal of Forecasting, 16(4): 437–450, 2000. doi:10.1016/S0169-2070(00)00065-0

-

[76]

Greta M. Ljung and George E. P. Box. On a measure of a lack of fit in time series models.Biometrika, 65(2): 297–303, 1978. doi:10.1093/biomet/65.2.297

-

[77]

Another look at measures of forecast accuracy

Rob J. Hyndman and Anne B. Koehler. Another look at measures of forecast accuracy.International Journal of Forecasting, 22(4):679–688, 2006. ISSN 0169-2070. doi:10.1016/j.ijforecast.2006.03.001. URL https: //www.sciencedirect.com/science/article/pii/S0169207006000239

-

[78]

Cort J. Willmott and Kenji Matsuura. Advantages of the mean absolute error (mae) over the root mean square error (rmse) in assessing average model performance.Climate Research, 30(1):79–82, 2005. ISSN 0936577X, 16161572. URLhttp://www.jstor.org/stable/24869236

-

[79]

T. Chai and R. R. Draxler. Root mean square error (rmse) or mean absolute error (mae)? – arguments against avoiding rmse in the literature.Geoscientific Model Development, 7(3):1247–1250, 2014. doi:10.5194/gmd-7- 1247-2014. URLhttps://gmd.copernicus.org/articles/7/1247/2014/

-

[80]

Proper scoring rules for estimation and forecast evaluation

Kartik Waghmare and Johanna Ziegel. Proper scoring rules for estimation and forecast evaluation, 2025. URL https://arxiv.org/abs/2504.01781

work page internal anchor Pith review Pith/arXiv arXiv 2025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.