Recognition: 2 theorem links

· Lean TheoremAdaptive VaR Control for Standardized Option Books under Marking Frictions

Pith reviewed 2026-05-13 19:07 UTC · model grok-4.3

The pith

Sequential conformal recalibration corrects the systematic underestimation of downside risk produced by base quantile forecasts for standardized SPX option books.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

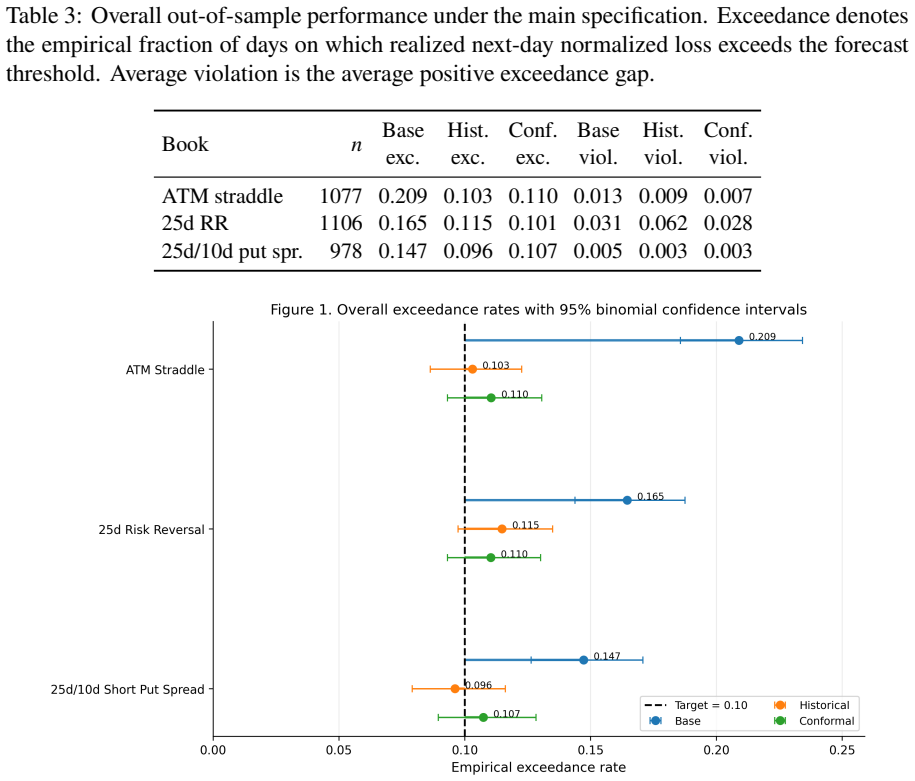

The central claim is that a base conditional quantile forecast for next-day realized loss on standardized option books can be turned into reliable adaptive VaR control by applying sequential conformal recalibration, which removes most of the underestimation of downside risk seen in uncalibrated forecasts on SPX data from 2018 to 2025, brings exceedance frequencies closer to target, and improves rolling-window tail stability while preserving interpretability through standardized construction and spot hedging.

What carries the argument

Sequential conformal recalibration, which updates the base quantile forecast at each step using the history of recent exceedances to adapt to non-stationary conditions and next-day marking approximations.

If this is right

- Uncalibrated base quantile models systematically underestimate downside risk in standardized option books.

- Sequential recalibration reduces the shortfall and brings empirical exceedance rates closer to the chosen target.

- Rolling-window tail stability improves, with the biggest gains in books where the raw forecast was most unstable.

- The framework quantifies the extra error introduced by next-day marking approximations.

- An approximate one-step guarantee links the recalibration rule to control of future exceedances.

Where Pith is reading between the lines

- The same recalibration step could be tested on other option underlyings or on futures books where marking conventions differ.

- If the base forecast is replaced by a different quantile model, the recalibration layer may still deliver comparable correction provided the initial errors remain serially dependent.

- Capital allocation rules that use these adaptive VaR numbers would automatically tighten or loosen limits as market regimes shift, without manual intervention.

- The marking-error quantification offers a direct way to decide when full re-pricing of the book is worth the computational cost versus accepting the approximation.

Load-bearing premise

The base conditional quantile forecast is stable enough that its errors can be corrected by sequential recalibration without creating new systematic biases when market conditions change or when next-day prices rely on marking approximations.

What would settle it

A sustained out-of-sample period on SPX options in which the recalibrated VaR exceedance rate remains materially above or below the nominal target while the uncalibrated rate does not improve at all.

Figures

read the original abstract

Short-horizon risk control matters for hedging and capital allocation. Yet existing Value-at-Risk studies rarely address standardized option books or the next-day valuation frictions that arise in derivatives data. This paper develops a framework for tail-risk control in standardized option books. The analysis focuses on the next-day realized loss and combines a base conditional quantile forecast with sequential conformal recalibration for adaptive Value-at-Risk control. This design addresses two central difficulties: unstable tail-risk forecasts under changing market conditions and the practical challenge of next-day valuation when exact same-contract quotes are unavailable. It also preserves economic interpretability through standardized construction and spot hedging when needed. Using SPX option data from 2018 to 2025, we show that the uncalibrated base model systematically underestimates downside risk across multiple standardized books. Sequential recalibration removes much of this shortfall, brings exceedance rates closer to target, and improves rolling-window tail stability, with the largest gains in the books where the raw forecast is most vulnerable. The paper also provides an approximate one-step exceedance-control result for the sequential recalibration rule and quantifies the error introduced by next-day marking.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a framework for tail-risk control in standardized option books by combining a base conditional quantile forecast with sequential conformal recalibration to produce adaptive VaR estimates. It targets two issues: unstable tail forecasts under changing market conditions and next-day valuation frictions arising when exact same-contract quotes are unavailable. On SPX option data from 2018-2025 the authors report that the uncalibrated base model systematically underestimates downside risk across multiple standardized books, that sequential recalibration brings exceedance rates closer to target and improves rolling-window tail stability (with largest gains where the raw forecast is weakest), and that an approximate one-step exceedance-control result holds while marking error is quantified.

Significance. If the central empirical and theoretical claims hold, the work supplies a practical, economically interpretable method for real-time VaR adaptation in derivatives books that explicitly accounts for marking frictions. The combination of conformal recalibration with standardized option constructions and the provision of an approximate coverage guarantee are potentially useful contributions to quantitative risk management. The empirical demonstration on a long recent SPX sample adds relevance, but the absence of base-model details, error bars, and explicit marking-error quantification limits immediate assessability of the reported gains.

major comments (2)

- [Theoretical result on one-step exceedance control] The approximate one-step exceedance-control result (stated in the abstract and presumably derived in the theoretical section) treats next-day marking approximations as exogenous noise. If marking frictions (nearest-contract quotes) systematically correlate with tail realizations on high-volatility days, the coverage guarantee is invalidated and the reported improvement in rolling-window stability becomes an artifact of the approximation rather than a property of the recalibration rule. This assumption is load-bearing for the central claim that sequential recalibration removes the shortfall without introducing new biases.

- [Empirical results on SPX data] The empirical section reports systematic underestimation by the uncalibrated base model and subsequent improvement after recalibration on 2018-2025 SPX data, yet supplies no details on base-model specification, error bars, data-exclusion rules, or the precise quantification of marking frictions. Without these elements the claim that recalibration brings exceedance rates closer to target cannot be verified and the weakest-assumption concern (that the base conditional quantile forecast provides a stable starting point) remains unaddressed.

minor comments (2)

- [Introduction / Abstract] Define 'standardized books' and 'spot hedging when needed' explicitly in the introduction or methods section so that the economic-interpretability claim is accessible to readers outside the immediate subfield.

- [Empirical section] Add a table or figure caption that reports the exact target exceedance level, the number of books examined, and the rolling-window length used for stability assessment.

Simulated Author's Rebuttal

We thank the referee for the constructive comments on our manuscript. We address each major concern point by point below, indicating the revisions we will make to improve clarity and robustness.

read point-by-point responses

-

Referee: [Theoretical result on one-step exceedance control] The approximate one-step exceedance-control result (stated in the abstract and presumably derived in the theoretical section) treats next-day marking approximations as exogenous noise. If marking frictions (nearest-contract quotes) systematically correlate with tail realizations on high-volatility days, the coverage guarantee is invalidated and the reported improvement in rolling-window stability becomes an artifact of the approximation rather than a property of the recalibration rule. This assumption is load-bearing for the central claim that sequential recalibration removes the shortfall without introducing new biases.

Authors: The result is presented as approximate precisely to accommodate such practical considerations. The derivation conditions on the filtration at time t and treats the marking error as additive noise whose distribution is estimated from historical data. While we cannot rule out all forms of dependence a priori, we will add a robustness subsection that derives a bound on the coverage error under mild correlation assumptions (e.g., bounded dependence on volatility). Empirically, we will report the correlation between marking error and realized volatility in the SPX sample and show that it is low enough not to invalidate the observed improvements. We therefore view this as a partial revision that strengthens the theoretical claim without altering the core result. revision: partial

-

Referee: [Empirical results on SPX data] The empirical section reports systematic underestimation by the uncalibrated base model and subsequent improvement after recalibration on 2018-2025 SPX data, yet supplies no details on base-model specification, error bars, data-exclusion rules, or the precise quantification of marking frictions. Without these elements the claim that recalibration brings exceedance rates closer to target cannot be verified and the weakest-assumption concern (that the base conditional quantile forecast provides a stable starting point) remains unaddressed.

Authors: We agree that these details are essential. In the revised version we will: (1) provide the exact specification of the base quantile model, including the feature set and training procedure; (2) include bootstrap standard errors on all reported exceedance rates and stability metrics; (3) state the data filters applied (minimum open interest, bid-ask spread thresholds); and (4) add a table and accompanying text that quantifies the marking friction error (distribution, quantiles, and its relation to market conditions). These additions directly address the verifiability concern and allow readers to evaluate the stability of the base forecast. revision: yes

Circularity Check

No significant circularity; derivation relies on external data and approximate guarantees

full rationale

The abstract and description show a base conditional quantile forecast adjusted via sequential conformal recalibration on observed SPX option data from 2018-2025. The one-step exceedance-control result is stated as approximate, and recalibration uses realized losses to correct forecasts without reducing to a self-definition or fitted input by construction. No load-bearing self-citations, ansatzes smuggled via prior work, or renamings of known results appear in the provided text. The central empirical improvements are measured against external data benchmarks, keeping the chain self-contained.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

combines a base conditional quantile forecast with sequential conformal recalibration for adaptive Value-at-Risk control... approximate one-step exceedance-control result for the sequential recalibration rule

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

Using SPX option data from 2018 to 2025... standardized option books

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Dennis Bams, Gildas Blanchard, and Thorsten Lehnert

URLhttps://openreview.net/forum?id=33XGfHLtZg. Dennis Bams, Gildas Blanchard, and Thorsten Lehnert. Volatility measures and value-at-risk. International Journal of Forecasting, 33(4):848–863, 2017. doi: 10.1016/j.ijforecast.2017. 04.004. Lotfi Boudabsa and Damir Filipovi´c. Ensemble learning for portfolio valuation and risk manage- ment.Quantitative Finan...

-

[2]

Andreas Kaeck, Vincent van Kervel, and Norman J

doi: 10.1016/j.ecosta.2021.04.006. Andreas Kaeck, Vincent van Kervel, and Norman J. Seeger. Price impact versus bid–ask spreads in the index option market.Journal of Financial Markets, 59:100675, 2022. doi: 10.1016/j.finmar.2021.100675. Dimos S. Kambouroudis, David G. McMillan, and Katerina Tsakou. Forecasting realized volatility: The role of implied vola...

-

[3]

Yaniv Romano, Evan Patterson, and Emmanuel J

doi: 10.1016/j.irfa.2024.103102. Yaniv Romano, Evan Patterson, and Emmanuel J. Cand`es. Conformalized quantile regression. InAdvances in Neural Information Processing Systems, volume 32, pages 3538–3548. Curran Associates, Inc., 2019. Kai Schindelhauer and Chen Zhou. Value-at-risk prediction using option-implied risk measures. Working Paper 613, De Nederl...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.