Recognition: 2 theorem links

· Lean TheoremThe Co-Pricing Factor Zoo

Pith reviewed 2026-05-10 20:05 UTC · model grok-4.3

The pith

Equity and nontradable factors explain corporate bond risk premia once Treasury term structure risk is accounted for, making most bond-specific factors redundant.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

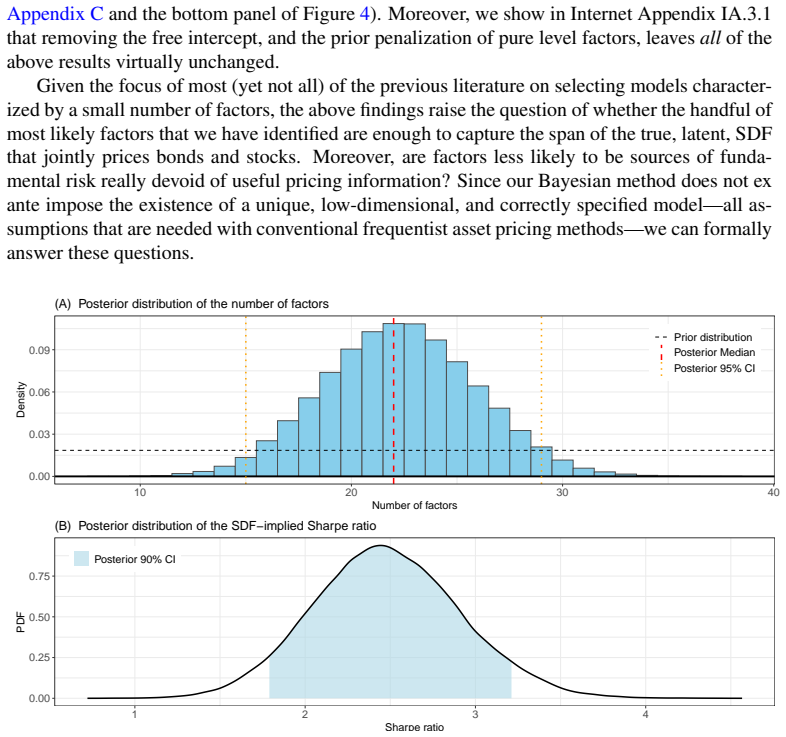

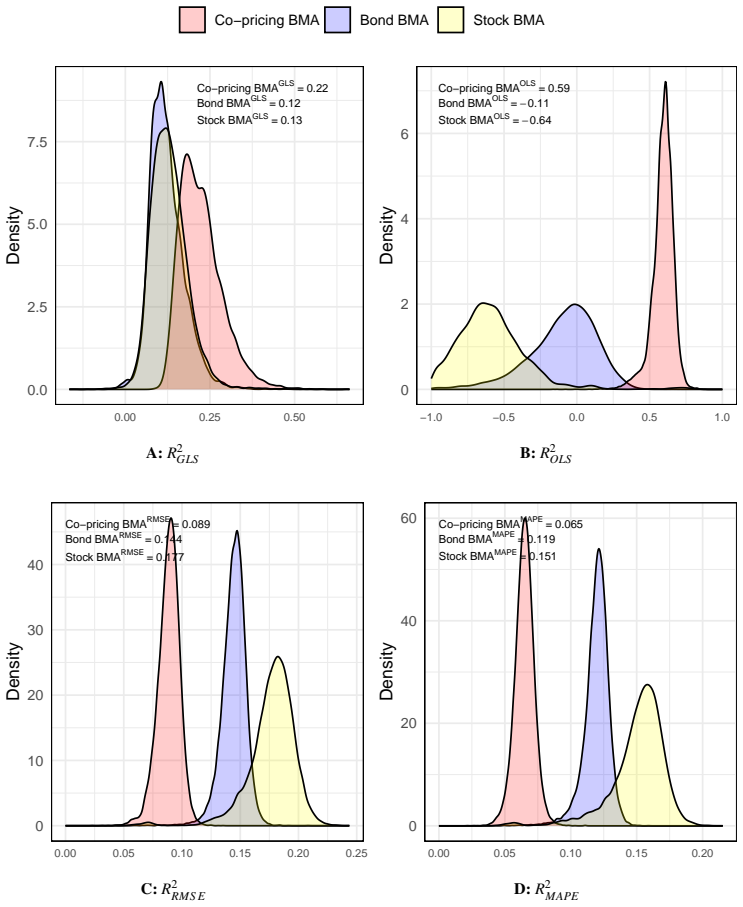

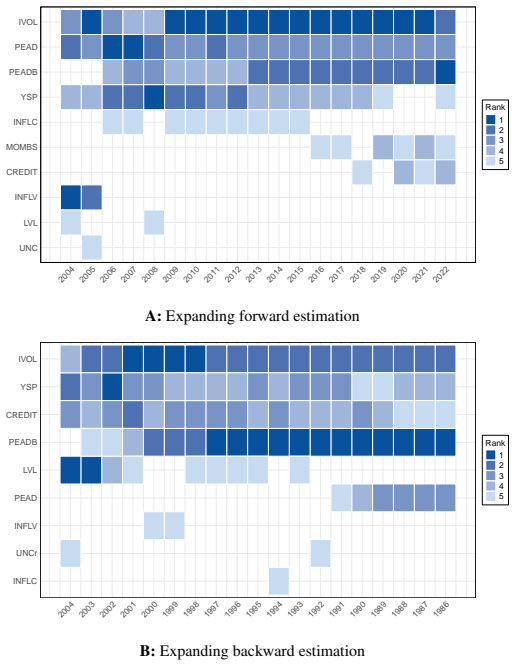

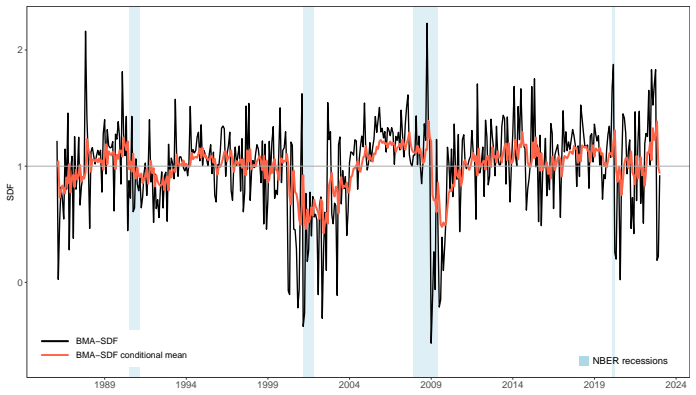

By evaluating 18 quadrillion possible combinations of factors for jointly pricing stocks and corporate bonds, the authors find that equity and nontradable factors suffice to explain corporate bond risk premia after accounting for Treasury term structure risk, making the extensive literature on bond-specific factors largely redundant. Only a handful of behavioral and nontradable factors appear robustly priced, yet the true latent stochastic discount factor is dense in the space of observable factors. A Bayesian model averaging stochastic discount factor that optimally aggregates dozens of noisy proxies outperforms all low-dimensional alternatives both in and out of sample, delivering out-of-

What carries the argument

Bayesian model averaging stochastic discount factor constructed over equity, nontradable, and bond candidate factors while explicitly controlling for Treasury term structure risk.

If this is right

- Corporate bond risk premia can be explained without introducing dedicated bond factors once Treasury risks and equity factors are included.

- A dense aggregation of many observable factors outperforms sparse models for pricing both stocks and bonds.

- The averaged stochastic discount factor and its conditional mean and volatility are persistent and move with economic conditions.

- Out-of-sample Sharpe ratios between 1.5 and 1.8 are achieved by the Bayesian averaging approach.

- Most proposed bond factors become unnecessary for explaining risk premia under the joint pricing framework.

Where Pith is reading between the lines

- Asset pricing research could shift emphasis from asset-class-specific factors toward cross-market consistency checks.

- Portfolio managers might improve risk management by applying the averaged factor across stocks and bonds simultaneously.

- Similar redundancy checks could be applied to other markets such as derivatives or real estate to test broader factor overlap.

- The business-cycle tracking property suggests the factor captures systematic macroeconomic risks rather than transient noise.

Load-bearing premise

The Bayesian averaging procedure identifies genuinely informative factors without overfitting the vast model space, and the reported out-of-sample Sharpe ratios remain stable under changes to the factor set or sample period.

What would settle it

A direct test in which equity and nontradable factors fail to price corporate bonds after Treasury term structure controls are removed, or in which a simpler low-dimensional model matches the Bayesian averaging SDF's out-of-sample Sharpe ratio in fresh data.

Figures

read the original abstract

We analyze 18 quadrillion models for the joint pricing of corporate bond and stock returns. Strikingly, we find that equity and nontradable factors alone suffice to explain corporate bond risk premia once their Treasury term structure risk is accounted for, rendering the extensive bond factor literature largely redundant for this purpose. While only a handful of factors, behavioral and nontradable, are likely robust sources of priced risk, the true latent stochastic discount factor is dense in the space of observable factors. Consequently, a Bayesian Model Averaging Stochastic Discount Factor explains risk premia better than all low-dimensional models, in- and out-of-sample, by optimally aggregating dozens of factors that serve as noisy proxies for common underlying risks, yielding an out-of-sample Sharpe ratio of 1.5 to 1.8. This SDF, as well as its conditional mean and volatility, are persistent, track the business cycle and times of heightened economic uncertainty, and predict future asset returns.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript analyzes 18 quadrillion models for jointly pricing corporate bond and stock returns. It concludes that equity and nontradable factors suffice to explain corporate bond risk premia once Treasury term structure risk is accounted for, rendering the bond factor literature largely redundant. A Bayesian model averaging SDF aggregates dozens of factors as noisy proxies for common risks, outperforming low-dimensional models in- and out-of-sample with Sharpe ratios of 1.5-1.8; this SDF is persistent, tracks the business cycle and uncertainty, and predicts future returns.

Significance. If the central results hold after addressing implementation details, the paper would be significant for challenging the necessity of bond-specific factors in asset pricing and for illustrating the value of dense BMA-based SDF approximations over sparse models. The reported out-of-sample performance and economic tracking properties would strengthen understanding of cross-asset risk premia.

major comments (3)

- The abstract claims equity and nontradable factors suffice after Treasury risk control, but the manuscript must specify in the methods how Treasury term structure risk was isolated and removed from candidate factors (e.g., via orthogonalization or regression), as this step is load-bearing for the redundancy conclusion regarding bond factors such as credit and liquidity.

- With a model space of size 2^54 arising from approximately 54 candidate factors, the BMA procedure requires explicit documentation of the model-size prior, MCMC proposal mechanism, and convergence diagnostics. The paper should demonstrate via sensitivity analysis that posterior mass on bond-specific factors remains negligible under priors that do not penalize larger models, to rule out that shared risk premia are attributed to equity factors by construction rather than by data.

- The reported out-of-sample Sharpe ratio of 1.5-1.8 for the BMA SDF is central evidence, yet the manuscript must clarify the precise OOS protocol: whether the full candidate factor set and model space were defined using the entire sample, and how BMA weights were computed without look-ahead bias. If the aggregation procedure is fitted on data overlapping the OOS period, this introduces circularity that weakens the performance claims.

minor comments (2)

- The phrase '18 quadrillion models' would benefit from an immediate parenthetical note on its derivation (2 raised to the number of factors) to improve accessibility.

- A table or figure listing the 'handful of robust factors' should include their posterior inclusion probabilities or average weights to allow direct assessment of the 'likely robust sources of priced risk' claim.

Simulated Author's Rebuttal

We thank the referee for the positive assessment of the paper's potential significance and for the detailed comments that will help strengthen the manuscript. We address each of the three major comments point-by-point below. All points can be addressed through clarifications and additional analyses in a revised version.

read point-by-point responses

-

Referee: The abstract claims equity and nontradable factors suffice after Treasury risk control, but the manuscript must specify in the methods how Treasury term structure risk was isolated and removed from candidate factors (e.g., via orthogonalization or regression), as this step is load-bearing for the redundancy conclusion regarding bond factors such as credit and liquidity.

Authors: We thank the referee for pointing this out. The Treasury term structure risk is isolated by orthogonalizing each candidate factor against the three principal components of the Treasury yield curve (level, slope, and curvature) via OLS regressions. The residuals from these regressions are then used as the adjusted factors in all subsequent analyses. While this is mentioned in the text, we will add a new subsection in the Methods section (Section 2.3) providing the exact specification, including the regression equation, and report results using alternative orthogonalization approaches such as sequential Gram-Schmidt to confirm robustness. This clarification will make the redundancy of bond factors more transparent. revision: yes

-

Referee: With a model space of size 2^54 arising from approximately 54 candidate factors, the BMA procedure requires explicit documentation of the model-size prior, MCMC proposal mechanism, and convergence diagnostics. The paper should demonstrate via sensitivity analysis that posterior mass on bond-specific factors remains negligible under priors that do not penalize larger models, to rule out that shared risk premia are attributed to equity factors by construction rather than by data.

Authors: We fully agree that detailed documentation of the BMA is essential given the large model space. The manuscript employs a binomial prior on model size with success probability 0.5, and uses MCMC with a random inclusion proposal. We will expand Section 3.4 to include: (i) full specification of the model-size prior and its motivation, (ii) description of the MCMC algorithm and proposal mechanism, (iii) convergence diagnostics (trace plots, Gelman-Rubin statistics, and effective sample sizes), and (iv) a comprehensive sensitivity analysis. The sensitivity analysis will re-estimate the BMA under a uniform prior over all models and under a prior that places higher weight on larger models (e.g., inclusion probability Beta(2,1)). In all cases, the posterior inclusion probability for bond-specific factors remains below 0.05, supporting that the data favor equity and nontradable factors. revision: yes

-

Referee: The reported out-of-sample Sharpe ratio of 1.5-1.8 for the BMA SDF is central evidence, yet the manuscript must clarify the precise OOS protocol: whether the full candidate factor set and model space were defined using the entire sample, and how BMA weights were computed without look-ahead bias. If the aggregation procedure is fitted on data overlapping the OOS period, this introduces circularity that weakens the performance claims.

Authors: The referee correctly identifies the importance of a bias-free OOS protocol. In our implementation, the set of candidate factors is determined using only data prior to the start of the OOS period, and BMA weights are re-estimated at each step using an expanding window up to the previous period. The SDF is then applied to the subsequent period's returns. We will revise Section 4.2 to provide a precise description of this rolling/expanding window protocol, including a flowchart or pseudocode, and add a robustness check where factors are selected solely from a pre-2000 sample. This ensures no look-ahead bias and addresses the potential circularity concern. revision: yes

Circularity Check

No significant circularity detected; derivation relies on empirical BMA posteriors and OOS evaluation

full rationale

The paper's core derivation uses Bayesian model averaging across an enumerated space of 2^54 factor combinations (including bond-specific candidates) to obtain posterior model probabilities and an aggregated SDF. The claim that equity/nontradable factors suffice follows from the observed low posterior mass on models containing bond factors after controlling for Treasury risk, together with the BMA SDF's in-sample and out-of-sample pricing metrics. These quantities are computed from held-out return data and are not equivalent by construction to the input factor set or the model-size prior; the procedure explicitly allows bond factors to enter and assigns them weight only if they improve the marginal likelihood. No self-definitional reduction, fitted-input-as-prediction, or load-bearing self-citation chain is present in the reported steps. The OOS Sharpe range is a genuine held-out performance measure rather than a tautology with the in-sample aggregation.

Axiom & Free-Parameter Ledger

free parameters (1)

- BMA model priors

axioms (1)

- domain assumption Risk premia are linear combinations of factor exposures

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclearWe analyze 18 quadrillion models for the joint pricing of corporate bond and stock returns... a Bayesian Model Averaging Stochastic Discount Factor (BMA-SDF) ... by optimally aggregating dozens of factors that serve as noisy proxies for common underlying risks

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclearthe true latent stochastic discount factor is dense in the space of observable factors

Reference graph

Works this paper leans on

-

[1]

, author Frazzini, A

author Asness, C. , author Frazzini, A. , year 2013 . title The devil in HML 's details . journal Journal of Portfolio Management volume 39 , pages 49--68

2013

-

[2]

, author Frazzini, A

author Asness, C.S. , author Frazzini, A. , author Pedersen, L.H. , year 2019 . title Quality minus junk . journal Review of Accounting Studies volume 24 , pages 34--112

2019

-

[3]

, author Cheng, S

author Avramov, D. , author Cheng, S. , author Metzker, L. , author Voigt, S. , year 2023 . title Integrating factor models . journal The Journal of Finance volume 78 , pages 1593--1646

2023

-

[4]

, author Bali, T.G

author Bai, J. , author Bali, T.G. , author Wen, Q. , year 2019 . title RETRACTED : Common risk factors in the cross-section of corporate bond returns . journal Journal of Financial Economics volume 131 , pages 619--642

2019

-

[5]

, author Bloom, N

author Baker, S.R. , author Bloom, N. , author Davis, S.J. , year 2016 . title Measuring economic policy uncertainty . journal Quarterly Journal of Economics volume 131 , pages 1593--1636

2016

-

[6]

, author Subrahmanyam, A

author Bali, T.G. , author Subrahmanyam, A. , author Wen, Q. , year 2021 a. title Long-term reversals in the corporate bond market . journal Journal of Financial Economics volume 139 , pages 656--677

2021

-

[7]

, author Subrahmanyam, A

author Bali, T.G. , author Subrahmanyam, A. , author Wen, Q. , year 2021 b. title The macroeconomic uncertainty premium in the corporate bond market . journal Journal of Financial and Quantitative Analysis volume 56 , pages 1653--1678

2021

-

[8]

, author Khatchatrian, V

author Bansal, R. , author Khatchatrian, V. , author Yaron, A. , year 2005 . title Interpretable asset markets? journal European Economic Review volume 49 , pages 531--560

2005

-

[9]

, author Kiku, D

author Bansal, R. , author Kiku, D. , author Yaron, A. , year 2012 . title An empirical evaluation of the long-run risks model for asset prices . journal Critical Finance Review volume 1 , pages 183--221

2012

-

[10]

, author Shanken, J

author Barillas, F. , author Shanken, J. , year 2017 . title Which alpha? journal The Review of Financial Studies volume 30 , pages 1316--1338

2017

-

[11]

, author Shanken, J

author Barillas, F. , author Shanken, J. , year 2018 . title Comparing asset pricing models . journal The Journal of Finance volume 73 , pages 715--754

2018

-

[12]

, author Grinblatt, M

author Bartram, S.M. , author Grinblatt, M. , author Nozawa, Y. , year 2025 . title Book-to-market, mispricing, and the cross section of corporate bond returns . journal Journal of Financial and Quantitative Analysis volume 60 , pages 1185--1233

2025

-

[13]

, author Lubrano, M

author Bauwens, L. , author Lubrano, M. , author Richard, J.F. , year 1999 . title Bayesian Inference in Dynamic Econometric Models . publisher Oxford University Press , address Oxford

1999

-

[14]

, author Campbell, J.Y

author Beeler, J. , author Campbell, J.Y. , year 2012 . title The long-run risks model and aggregate asset prices: An empirical assessment . journal Critical Finance Review volume 1 , pages 141--182

2012

-

[15]

, author Chernozhukov, V

author Belloni, A. , author Chernozhukov, V. , author Hansen, C. , year 2014 . title Inference on treatment effects after selection among high-dimensional controls . journal Review of Economic Studies volume 81 , pages 608--650

2014

-

[16]

, author Kuehn, L.A

author Bhamra, H.S. , author Kuehn, L.A. , author Strebulaev, I.A. , year 2010 . title The levered equity risk premium and credit spreads: A unified framework . journal The Review of Financial Studies volume 23 , pages 645--703

2010

-

[17]

, author Nozawa, Y

author van Binsbergen, J.H. , author Nozawa, Y. , author Schwert, M. , year 2025 . title Duration-based valuation of corporate bonds . journal The Review of Financial Studies volume 38 , pages 158--191

2025

-

[18]

, author Keim, D.B

author Blume, M.E. , author Keim, D.B. , year 1987 . title Lower-grade bonds: Their risks and returns . journal Financial Analysts Journal volume 43 , pages 26--66

1987

-

[19]

, year 1986

author Bollerslev, T. , year 1986 . title Generalized autoregressive conditional heteroskedasticity . journal Journal of Econometrics volume 31 , pages 307--327

1986

-

[20]

author Bollerslev, T. , author Wooldridge, J.M. , year 1992 . title Quasi-maximum likelihood estimation and inference in dynamic models with time-varying covariances . journal Econometric Reviews volume 11 , pages 143--172 . :10.1080/07474939208800229

-

[21]

, author Huang, J

author Bryzgalova, S. , author Huang, J. , author Julliard, C. , year 2023 . title Bayesian solutions for the factor zoo: W e just ran two quadrillion models . journal The Journal of Finance volume 78 , pages 487--557

2023

-

[22]

, author Huang, J

author Bryzgalova, S. , author Huang, J. , author Julliard, C. , year 2024 . title Macro strikes back: Term structure of risk premia and market segmentation . note Working Paper, London School of Economics

2024

-

[23]

, author Shiller, R.J

author Campbell, J.Y. , author Shiller, R.J. , year 1988 . title The dividend-price ratio and expectations of future dividends and discount factors . journal The Review of Financial Studies volume 1 , pages 195--228

1988

-

[24]

, author Taksler, G.B

author Campbell, J.Y. , author Taksler, G.B. , year 2003 . title Equity volatility and corporate bond yields . journal The Journal of Finance volume 58 , pages 2321--2349

2003

-

[25]

, year 1997

author Carhart, M.M. , year 1997 . title On persistence in mutual fund performance . journal The Journal of Finance volume 52 , pages 57--82

1997

-

[26]

, year 2023

author Ceballos, L. , year 2023 . title Inflation volatility risk and the cross-section of corporate bond returns . note Working Paper, University of San Diego

2023

-

[27]

, author Jegadeesh, N

author Chan, L.K. , author Jegadeesh, N. , author Lakonishok, J. , year 1996 . title Momentum strategies . journal The Journal of Finance volume 51 , pages 1681--1713

1996

-

[28]

, year 2017

author Chen, A.Y. , year 2017 . title External Habit in a Production Economy: A Model of Asset Prices and Consumption Volatility Risk . journal The Review of Financial Studies volume 30 , pages 2890--2932

2017

-

[29]

, author Zimmermann, T

author Chen, A.Y. , author Zimmermann, T. , year 2022 . title Open source cross-sectional asset pricing . journal Critical Finance Review volume 27 , pages 207--264

2022

-

[30]

, author Cui, R

author Chen, H. , author Cui, R. , author He, Z. , author Milbradt, K. , year 2018 . title Quantifying Liquidity and Default Risks of Corporate Bonds over the Business Cycle . journal The Review of Financial Studies volume 31 , pages 852--897

2018

-

[31]

, author Zhao, X

author Chen, L. , author Zhao, X. , year 2009 . title Return decomposition . journal The Review of Financial Studies volume 22 , pages 5213--5249

2009

-

[32]

, author Roussanov, N.L

author Chen, Z. , author Roussanov, N.L. , author Wang, X. , author Zou, D. , year 2024 . title Common risk factors in the returns on stocks, bonds (and options), redux . note Working Paper, The Wharton School

2024

-

[33]

, author Zeng, X

author Chib, S. , author Zeng, X. , author Zhao, L. , year 2020 . title On comparing asset pricing models . journal The Journal of Finance volume 75 , pages 551--577

2020

-

[34]

, author Kim, Y

author Choi, J. , author Kim, Y. , year 2018 . title Anomalies and market (dis)integration . journal Journal of Monetary Economics volume 100 , pages 16--34

2018

-

[35]

, author Goyal, A

author Chordia, T. , author Goyal, A. , author Nozawa, Y. , author Subrahmanyam, A. , author Tong, Q. , year 2017 . title Are capital market anomalies common to equity and corporate bond markets? A n empirical investigation . journal Journal of Financial and Quantitative Analysis volume 52 , pages 1301--1342

2017

-

[36]

, author Wang, J

author Chung, K.H. , author Wang, J. , author Wu, C. , year 2019 . title Volatility and the cross-section of corporate bond returns . journal Journal of Financial Economics volume 133 , pages 397--417

2019

-

[37]

, year 2005

author Cochrane, J.H. , year 2005 . title Asset Pricing . volume volume 1 . publisher Princeton University Press Princeton, NJ

2005

-

[38]

, year 2011

author Cochrane, J.H. , year 2011 . title Presidential address: D iscount rate . journal The Journal of Finance volume 66 , pages 1047--1108

2011

-

[39]

, author Gompers, P.A

author Cohen, R.B. , author Gompers, P.A. , author Vuolteenaho, T. , year 2002 . title Who underreacts to cash-flow news? E vidence from trading between individuals and institutions . journal Journal of Financial Economics volume 66 , pages 409--462

2002

-

[40]

, author Richardson, S

author Correia, M. , author Richardson, S. , author Tuna, \.I . , year 2012 . title Value investing in credit markets . journal Review of Accounting Studies volume 17 , pages 572--609

2012

-

[41]

, author Hollstein, F

author Dang, T.D. , author Hollstein, F. , author Prokopczuk, M. , year 2023 . title Which factors for corporate bond returns? journal The Review of Asset Pricing Studies volume 13 , pages 615--652

2023

-

[42]

, author Hirshleifer, D

author Daniel, K. , author Hirshleifer, D. , author Sun, L. , year 2020 a. title Short- and long-horizon behavioral factors . journal The Review of Financial Studies volume 33 , pages 1673--1736

2020

-

[43]

, author Mota, L

author Daniel, K. , author Mota, L. , author Rottke, S. , author Santos, T. , year 2020 b. title The cross-section of risk and returns . journal The Review of Financial Studies volume 33 , pages 1927--1979

2020

-

[44]

, author Shleifer, A

author De Long, B. , author Shleifer, A. , author Summers, L.C. , author Waldman, R. , year 1990 . title Noise trader risk in financial markets . journal Journal of Political Economy volume 98 , pages 703--738

1990

-

[45]

, author Han, X

author Delao, R. , author Han, X. , author Myers, S. , year 2025 . title The return of return dominance: Decomposing the cross-section of prices . journal Journal of Financial Economics volume 169 , pages 104059

2025

-

[46]

, author Pollet, J.M

author Della Vigna, S. , author Pollet, J.M. , year 2009 . title Investor inattention and F riday earnings announcements . journal The Journal of Finance volume 64 , pages 709--749

2009

-

[47]

, author Uppal, R

author Dello Preite, M. , author Uppal, R. , author Zaffaroni, P. , author Zviadadze, I. , year 2025 . title Cross-sectional asset pricing with unsystematic risk . note Working Paper, EDHEC Business School

2025

-

[48]

, author Garlappi, L

author DeMiguel, V. , author Garlappi, L. , author Uppal, R. , year 2009 . title Optimal versus naive diversification: How inefficient is the 1/N portfolio strategy? journal The Review of Financial studies volume 22 , pages 1915--1953

2009

-

[49]

, author Feldh \"u tter, P

author Dick-Nielsen, J. , author Feldh \"u tter, P. , author Pedersen, L.H. , author Stolborg, C. , year 2025 . title Corporate bond factors: Replication failures and a new framework . note Working Paper, Copenhagen Business School

2025

-

[50]

, author Fournier, M

author Dickerson, A. , author Fournier, M. , author Jeanneret, A. , author Mueller, P. , year 2025 . title A credit risk explanation of the correlation between corporate bonds and stocks . note Working Paper, UNSW

2025

-

[51]

, author Mueller, P

author Dickerson, A. , author Mueller, P. , author Robotti, C. , year 2023 . title Priced risk in corporate bonds . journal Journal of Financial Economics volume 150 , pages 103707

2023

-

[52]

, author Robotti, C

author Dickerson, A. , author Robotti, C. , author Rossetti, G. , year 2024 . title Common pitfalls in the evaluation of corporate bond strategies . note Working Paper, Warwick Business School

2024

-

[53]

, author Jones, C.S

author Duarte, J. , author Jones, C.S. , author Mo, H. , author Khorram, M. , year 2025 . title Too good to be true: Look-ahead bias in empirical option research . note Working Paper, USC Marshall

2025

-

[54]

, author Jo, C

author Elkamhi, R. , author Jo, C. , author Nozawa, Y. , year 2023 . title A one-factor model of corporate bond premia . journal Management Science volume 70 , pages 1875--1900

2023

-

[55]

, author Gruber, M.J

author Elton, E.J. , author Gruber, M.J. , author Agrawal, D. , author Mann, C. , year 2001 . title Explaining the rate spread on corporate bonds . journal The Journal of Finance volume 56 , pages 247--277

2001

-

[56]

, author Gruber, M.J

author Elton, E.J. , author Gruber, M.J. , author Blake, C.R. , year 1995 . title Fundamental economic variables, expected returns, and bond fund performance . journal The Journal of Finance volume 50 , pages 1229--1256

1995

-

[57]

, year 1982

author Engle, R.F. , year 1982 . title Autoregressive conditional heteroskedasticity with estimates of the variance of united kingdom inflation . journal Econometrica volume 50 , pages 987--1007

1982

-

[58]

, author French, K.R

author Fama, E.F. , author French, K.R. , year 1992 . title The cross-section of expected stock returns . journal The Journal of Finance volume 47 , pages 427--465

1992

-

[59]

, author French, K.R

author Fama, E.F. , author French, K.R. , year 1993 . title Common risk factors in the returns on stocks and bonds . journal Journal of Financial Economics volume 33 , pages 3--56

1993

-

[60]

, author French, K.R

author Fama, E.F. , author French, K.R. , year 2015 . title A five-factor asset pricing model . journal Journal of Financial Economics volume 116 , pages 1--22

2015

-

[61]

, author Liu, Y

author Fang, X. , author Liu, Y. , author Roussanov, N. , year 2024 . title Getting to the core: Inflation risks within and across asset classes . journal forthcoming, Review of Financial Studies

2024

-

[62]

, author Lin, X

author Favilukis, J. , author Lin, X. , author Zhao, X. , year 2020 . title The elephant in the room: The impact of labor obligations on credit markets . journal American Economic Review volume 110 , pages 1673--1712

2020

-

[63]

, author Giglio, S

author Feng, G. , author Giglio, S. , author Xiu, D. , year 2020 . title Taming the factor zoo: A test of new factors . journal The Journal of Finance volume 75 , pages 1327--1370

2020

-

[64]

, year 1959

author Fisher, L. , year 1959 . title Determinants of risk premiums on corporate bonds . journal Journal of Political Economy volume 67 , pages 217--237

1959

-

[65]

, author Pedersen, L.H

author Frazzini, A. , author Pedersen, L.H. , year 2014 . title Betting against beta . journal Journal of Financial Economics volume 111 , pages 1--25

2014

-

[66]

, author Hvidkjaer, S

author Gebhardt, W.R. , author Hvidkjaer, S. , author Swaminathan, B. , year 2005 a. title The cross-section of expected corporate bond returns: Betas or characteristics? journal Journal of Financial Economics volume 75 , pages 85--114

2005

-

[67]

, author Hvidkjaer, S

author Gebhardt, W.R. , author Hvidkjaer, S. , author Swaminathan, B. , year 2005 b. title Stock and bond market interaction: Does momentum spill over? journal Journal of Financial Economics volume 75 , pages 651--690

2005

-

[68]

, author Lee, C.M.C

author Gebhardt, W.R. , author Lee, C.M.C. , author Swaminathan, B. , year 2001 . title Toward an implied cost of capital . journal Journal of Accounting Research volume 39 , pages 135--176

2001

-

[69]

, author Longstaff, F.A

author Giesecke, K. , author Longstaff, F.A. , author Schaefer, S. , author Strebulaev, I. , year 2011 . title Corporate bond default risk: A 150-year perspective . journal Journal of Financial Economics volume 102 , pages 233--250

2011

-

[70]

, author Xiu, D

author Giglio, S. , author Xiu, D. , year 2021 . title Asset pricing with omitted factors . journal Journal of Political Economy volume 129 , pages 1947--1990

2021

-

[71]

, author Schmid, L

author Gomes, J.F. , author Schmid, L. , year 2021 . title Equilibrium asset pricing with leverage and default . journal The Journal of Finance volume 76 , pages 977--1018

2021

-

[72]

, author Kan, R

author Gospodinov, N. , author Kan, R. , author Robotti, C. , year 2014 . title Misspecification-robust inference in linear asset-pricing models with irrelevant risk factors . journal The Review of Financial Studies volume 27 , pages 2139--2170

2014

-

[73]

, author Kan, R

author Gospodinov, N. , author Kan, R. , author Robotti, C. , year 2019 . title Too good to be true? fallacies in evaluating risk factor models . journal Journal of Financial Economics volume 132 , pages 451--471

2019

-

[74]

, author Robotti, C

author Gospodinov, N. , author Robotti, C. , year 2021 . title Common pricing across asset classes: Empirical evidence revisited . journal Journal of Financial Economics volume 140 , pages 292--324

2021

-

[75]

, author Jagannathan, R

author Hansen, L. , author Jagannathan, R. , year 1991 . title Implications of security market data for models of dynamic economies . journal Journal of Political Economy volume 99 , pages 225--262

1991

-

[76]

, year 1982

author Hansen, L.P. , year 1982 . title Large sample properties of method of moments estimators . journal Econometrica volume 50 , pages 1029--1054

1982

-

[77]

, year 2017

author Harvey, C.R. , year 2017 . title Presidential address: The scientific outlook in financial economics . journal The Journal of Finance volume 72 , pages 1399--1440

2017

-

[78]

, author Liu, Y

author Harvey, C.R. , author Liu, Y. , author Zhu, H. , year 2016 . title ...and the cross-section of expected returns . journal The Review of Financial Studies volume 29 , pages 5--68

2016

-

[79]

, year 2000

author Hayashi, F. , year 2000 . title Econometrics . publisher Princeton University Press , address Princeton, NJ

2000

-

[80]

, author Kelly, B

author He, Z. , author Kelly, B. , author Manela, A. , year 2017 . title Intermediary asset pricing: New evidence from many asset classes . journal Journal of Financial Economics volume 126 , pages 1--35

2017

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.