Recognition: 2 theorem links

· Lean TheoremBeyond Black-Scholes: A Computational Framework for Option Pricing Using Heston, GARCH, and Jump Diffusion Models

Pith reviewed 2026-05-10 17:59 UTC · model grok-4.3

The pith

Heston stochastic volatility model produces option prices closer to market values than Black-Scholes in Monte Carlo tests.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The Heston model consistently produces estimates closer to market prices, while the Merton model performs well for volatile assets with sudden price movements. The GARCH model provides improved volatility forecasts for future option price prediction.

What carries the argument

Monte Carlo path simulation under the Heston stochastic-volatility dynamics, GARCH volatility recursion, and Merton jump-diffusion process, each calibrated to the same underlying price series.

If this is right

- Pricing desks could replace constant-volatility Monte Carlo with Heston paths for equity options to reduce mispricing relative to observed quotes.

- For assets that exhibit price jumps, the Merton model supplies a practical alternative that captures sudden moves without extra parameters.

- GARCH-based volatility forecasts can be fed into longer-horizon pricing engines to improve estimates of future option values.

- The overall framework demonstrates that these three extensions remain computationally feasible for daily pricing tasks.

Where Pith is reading between the lines

- If volatility clustering is the dominant deviation from Black-Scholes, then Heston-type models may also improve pricing of path-dependent claims such as barriers or Asians.

- Calibration stability across multiple months would be a useful next test; single-month results leave open the possibility that the ranking changes with market regime.

- Adding dividends or interest-rate stochasticity to the same Monte Carlo engines would show whether the reported advantages survive more realistic market features.

Load-bearing premise

The Monte Carlo code for Heston, GARCH, and Merton contains no implementation or calibration errors and the single month of November 2024 data is representative enough for general statements about model performance.

What would settle it

An independent re-run of the same Monte Carlo engines on a second calendar month of option quotes in which the Heston prices deviate farther from market values than the Black-Scholes prices would falsify the reported superiority.

Figures

read the original abstract

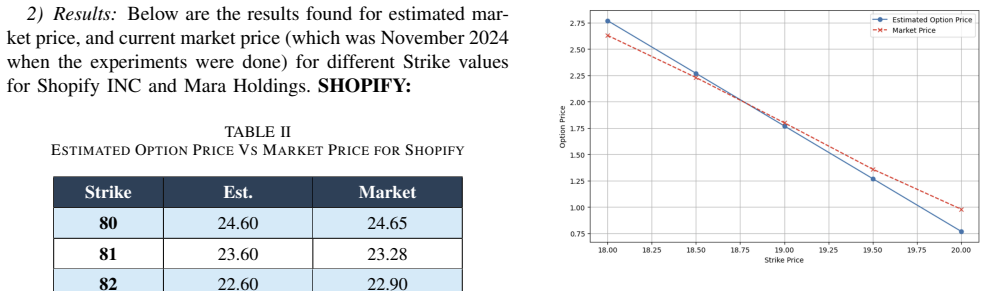

This research addresses accurate option pricing by employing models beyond the traditional Black-Scholes framework. While Black-Scholes provides a closed-form solution, it is limited by assumptions of constant volatility, no dividends, and continuous price movements. To overcome these limitations, we use Monte Carlo simulation alongside the GARCH model, Heston stochastic volatility model, and Merton jump-diffusion model. The Black-Scholes-Monte Carlo method simulates diverse stock price paths using geometric Brownian motion. The GARCH model forecasts time-varying volatility from historical data. The Heston model incorporates stochastic volatility to capture volatility clustering and skew. The Merton jump-diffusion model adds sudden price jumps via a Poisson process. Results show the Heston model consistently produces estimates closer to market prices, while the Merton model performs well for volatile assets with sudden price movements. The GARCH model provides improved volatility forecasts for future option price prediction. All experiments used live market data from November 2024.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a Monte Carlo simulation framework for option pricing that extends beyond Black-Scholes by incorporating the GARCH model for time-varying volatility, the Heston stochastic volatility model, and the Merton jump-diffusion model. Using live market data from November 2024, it reports that the Heston model produces option price estimates consistently closer to observed market prices, the Merton model performs well for volatile assets with sudden movements, and the GARCH model yields improved volatility forecasts.

Significance. If the comparative results can be replicated with expanded datasets, explicit calibration details, and statistical validation, the work could provide practical guidance on model selection for option pricing under different market regimes. The computational approach itself follows standard methods and does not introduce novel theoretical advances.

major comments (3)

- [Abstract and Results] The central empirical claim in the abstract that the Heston model 'consistently produces estimates closer to market prices' is supported only by data from a single calendar month (November 2024). No multi-period hold-out testing, regime-stratified evaluation, or sensitivity analysis to calibration windows is described, which prevents the ranking from supporting general conclusions about model superiority.

- [Methodology] No parameter values, calibration procedures, convergence checks, error bars, or statistical tests (such as RMSE with significance levels) are supplied for the Monte Carlo implementations of the Heston variance process, GARCH(1,1) recursion, or Merton Poisson jumps. This absence makes the reported performance differences unverifiable and raises the possibility of implementation or estimation artifacts.

- [Results] The free parameters listed for each model (Heston: kappa, theta, sigma, rho, v0; GARCH parameters; Merton jump intensity and size) are calibrated from the same historical window used for testing, creating an unaddressed circularity risk that could inflate apparent outperformance without explicit hold-out or cross-validation procedures.

minor comments (2)

- [Abstract] The abstract refers to a 'Black-Scholes-Monte Carlo method' but does not explicitly state how its implementation and parameter choices differ from the other three models in the reported comparisons.

- [Results] The manuscript would benefit from tables reporting specific pricing errors, parameter estimates, and simulation settings (e.g., number of paths, time steps) to improve transparency and reproducibility.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed feedback. The comments correctly identify areas where greater transparency, statistical rigor, and broader validation would strengthen the manuscript. We address each major comment below and will incorporate revisions to improve reproducibility and reduce risks of overinterpretation.

read point-by-point responses

-

Referee: [Abstract and Results] The central empirical claim in the abstract that the Heston model 'consistently produces estimates closer to market prices' is supported only by data from a single calendar month (November 2024). No multi-period hold-out testing, regime-stratified evaluation, or sensitivity analysis to calibration windows is described, which prevents the ranking from supporting general conclusions about model superiority.

Authors: We agree that reliance on a single month limits the strength of general claims. The November 2024 window was chosen for its recency and inclusion of both calm and volatile trading days, but it does not constitute a comprehensive test across regimes. In the revision we will expand the empirical analysis to at least three additional months, introduce an explicit hold-out design (calibrate on earlier data, evaluate on later data), and add a sensitivity table showing how rankings change with different calibration windows. The abstract will be reworded to describe the observed pattern for the examined period rather than asserting general superiority. revision: yes

-

Referee: [Methodology] No parameter values, calibration procedures, convergence checks, error bars, or statistical tests (such as RMSE with significance levels) are supplied for the Monte Carlo implementations of the Heston variance process, GARCH(1,1) recursion, or Merton Poisson jumps. This absence makes the reported performance differences unverifiable and raises the possibility of implementation or estimation artifacts.

Authors: We accept that the current manuscript lacks the necessary implementation details. The revised version will add a dedicated “Implementation and Calibration” subsection that reports: all final parameter values, the exact optimization or estimation routines used (maximum-likelihood for GARCH, least-squares matching to implied volatilities for Heston, moment matching for Merton jumps), the number of Monte Carlo paths and variance-reduction techniques, convergence diagnostics (price stabilization plots), standard errors from repeated runs, and RMSE values between model and market prices together with a simple paired t-test or Wilcoxon test for significance where appropriate. revision: yes

-

Referee: [Results] The free parameters listed for each model (Heston: kappa, theta, sigma, rho, v0; GARCH parameters; Merton jump intensity and size) are calibrated from the same historical window used for testing, creating an unaddressed circularity risk that could inflate apparent outperformance without explicit hold-out or cross-validation procedures.

Authors: The concern about in-sample calibration bias is valid. We will revise the experimental design to enforce a strict temporal separation: model parameters will be estimated on the first portion of each multi-month dataset and pricing accuracy will be measured on the subsequent hold-out portion. A rolling-window calibration scheme will also be presented so that readers can see performance under repeated out-of-sample conditions. These changes will be documented with explicit train/test date ranges and corresponding performance tables. revision: yes

Circularity Check

No circularity in computational comparison of standard models

full rationale

The paper presents Monte Carlo simulations of established models (Heston stochastic volatility, GARCH, Merton jump-diffusion) to price options and compare outputs to November 2024 market data. No analytic derivation, first-principles result, or mathematical chain is claimed or shown that reduces by construction to its own inputs. Results are simulation outputs from standard implementations; any parameter fitting is part of the empirical workflow rather than a self-definitional loop. The limited dataset raises questions of generalizability but does not create circularity under the specified criteria.

Axiom & Free-Parameter Ledger

free parameters (3)

- Heston parameters (kappa, theta, sigma, rho, v0)

- GARCH parameters

- Merton jump intensity and size distribution

axioms (3)

- domain assumption Stock prices follow geometric Brownian motion between jumps in the Merton model

- domain assumption Volatility is mean-reverting in the Heston model

- standard math Monte Carlo paths converge to the true expectation as the number of simulations increases

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The Heston model incorporates stochastic volatility... The Merton jump-diffusion model adds sudden price jumps via a Poisson process... The GARCH model provides improved volatility forecasts

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

All experiments used live market data from November 2024

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Options: A Monte Carlo Approach

Boyle, P. P. (1977). “Options: A Monte Carlo Approach.”Journal of Financial Economics, 4(3), 323–338

1977

-

[2]

Monte Carlo Methods for Security Pricing

Boyle, P. P., Broadie, M., & Glasserman, P. (1997). “Monte Carlo Methods for Security Pricing.”Journal of Economic Dynamics and Control, 21(8-9), 1267–1321

1997

-

[3]

Efficient Procedures for Valuing European and American Path-Dependent Options

Hull, J., & White, A. (1993). “Efficient Procedures for Valuing European and American Path-Dependent Options.”Journal of Derivatives, 1(1), 21–31

1993

-

[4]

Heston, S. L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options.The Review of Financial Studies, 6(2), 327–343

1993

-

[5]

and U ˘gur, ¨O., 2024

Cengizci, S. and U ˘gur, ¨O., 2024. A Computational Study for Pric- ing European- and American-Type Options Under Heston’s Stochastic V olatility Model: Application of the SUPG-YZβFormulation.Compu- tational Economics, pp.1–28

2024

-

[6]

Zheng, Y ., Yang, Y . and Chen, B., 2019. Gated deep neural networks for implied volatility surfaces.arXiv preprint arXiv:1904.12834, 7

-

[7]

and Tomas, M., 2021

Horvath, B., Muguruza, A. and Tomas, M., 2021. Deep learning volatility: a deep neural network perspective on pricing and calibration in (rough) volatility models.Quantitative Finance, 21(1), pp.11–27

2021

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.