0

Rule embedding cuts parameters for imbalance price forecasts

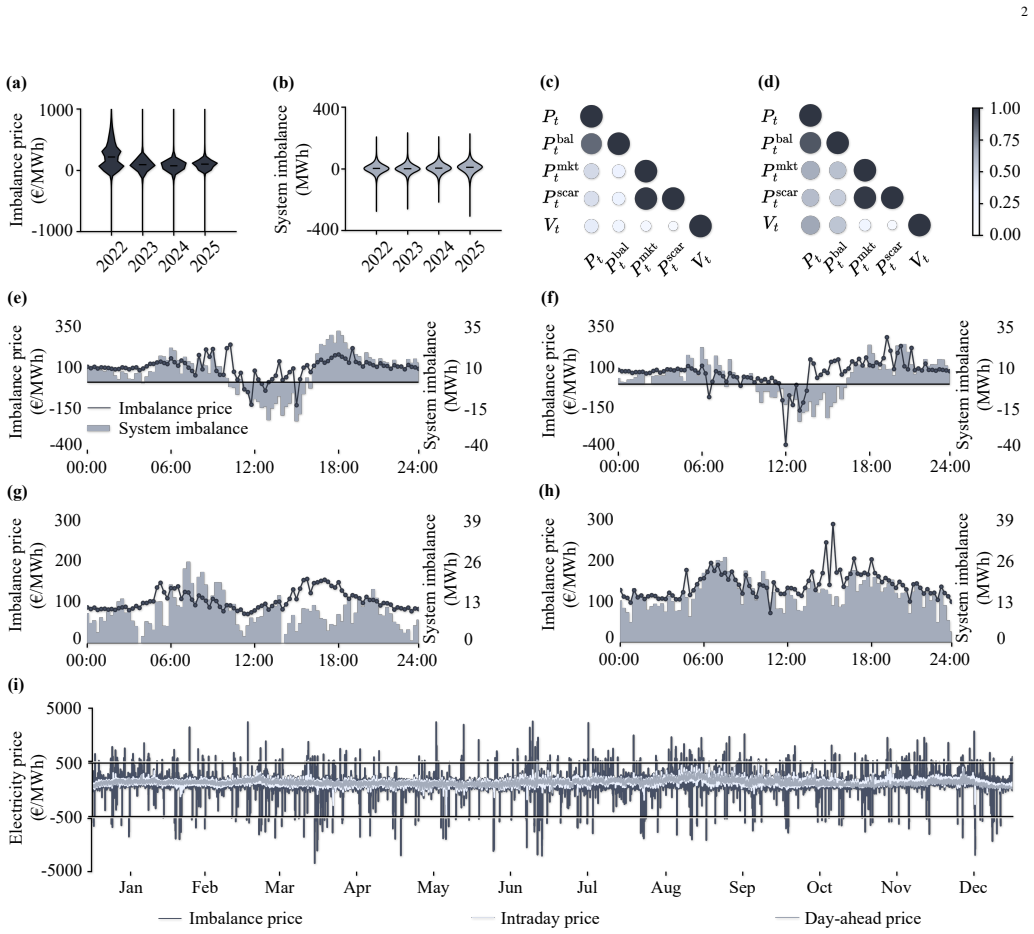

A Market-Rule-Informed Neural Network for Efficient Imbalance Electricity Price Forecasting

Hybrid neural model matches deep learning accuracy while using far fewer parameters and less training time in electricity balancing markets.

full image

full image

abstract click to expand

Accurate and efficient imbalance electricity price forecasting is critical for industrial energy trading systems, especially as battery assets and automated bidding pipelines increasingly participate in balancing markets. However, real-time forecasting is complicated by nonlinear market-rule-based price formation, heterogeneous input signals, and incomplete data availability caused by communication delays, publication lags, and measurement outages. This paper proposes a market-rule-informed neural forecasting framework that embeds imbalance price formation rules into the latent space of an expressive neural network. The proposed framework preserves raw signal information while exploiting transparent market-rule priors. We further analyze operational robustness by removing price-component information and characterize how forecasting performance scales with input length and forecasting horizon. Experimental results show that the proposed model achieves competitive forecasting performance with substantially fewer trainable parameters and shorter training time than generic deep learning baselines. Experimental results show that the proposed model achieves competitive forecasting performance with substantially fewer trainable parameters and shorter training time than generic deep learning baselines, demonstrating that market-rule priors and expressive neural networks should be jointly used for accurate and computationally sustainable forecasting in industrial energy trading applications. The implementation is publicly available at https://runyao-yu.github.io/MRINN/.