Recognition: 3 theorem links

· Lean TheoremThe Corporate Bond Factor Replication Crisis

Pith reviewed 2026-05-10 18:03 UTC · model grok-4.3

The pith

Most documented corporate bond factors lose statistical significance once price measurement errors and ex-post filtering biases are corrected.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Corporate bond factor research faces a replication crisis. The crisis stems from two sources that inflate reported factor premia: transaction prices whose measurement error enters both sorting signals and return denominators, creating a correlated errors-in-variables bias, and asymmetric ex-post return filtering that embeds future information into factor construction. Applying our framework to a 'factor zoo' of 108 signals across nine thematic clusters, we show that the majority of previously documented factors do not produce statistically significant bond CAPM alphas after correction.

What carries the argument

The error-correction framework that adjusts TRACE transaction prices for measurement error and removes asymmetric ex-post filtering bias during factor construction and alpha testing.

If this is right

- The majority of the 108 tested factors across nine clusters fail to deliver statistically significant bond CAPM alphas after correction.

- Reproducible corporate bond factor research requires error-corrected transaction data and avoidance of future-information filters.

- Published factor premia in corporate bonds are overstated for most signals once the two biases are removed.

- Open-source corrected TRACE data and software enable direct validation of existing and new bond factor claims.

Where Pith is reading between the lines

- The same transaction-price and lookahead biases could affect factor studies in other fixed-income segments that rely on dealer-reported prices.

- Portfolio managers using uncorrected bond factors may be exposed to overstated expected returns and higher turnover costs.

- Widespread adoption of the corrected data and code would likely reduce the number of viable factors but increase their out-of-sample reliability.

Load-bearing premise

The two identified biases are the dominant sources of inflation and that the proposed error-correction and filtering adjustments fully remove them without introducing new distortions or selection effects.

What would settle it

Re-running the analysis on an independent corporate bond dataset that lacks the same transaction-price measurement error and applying the identical correction steps yields a large fraction of factors with significant bond CAPM alphas.

Figures

read the original abstract

Corporate bond factor research faces a replication crisis. The crisis stems from two sources that inflate reported factor premia: transaction prices whose measurement error enters both sorting signals and return denominators, creating a correlated errors-in-variables bias, and asymmetric ex-post return filtering that embeds future information into factor construction. Applying our framework to a 'factor zoo' of 108 signals across nine thematic clusters, we show that the majority of previously documented factors do not produce statistically significant bond CAPM alphas after correction. We provide an open source framework via Open Bond Asset Pricing, including error-corrected TRACE data, bias corrected factors, and software for reproducible research.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript identifies two sources of upward bias in corporate bond factor premia: correlated errors-in-variables arising because transaction-price measurement error enters both the sorting signal and the return denominator, and asymmetric ex-post return filtering that embeds future information into factor construction. It applies a bias-correction framework to a zoo of 108 signals grouped into nine thematic clusters and reports that the majority of these factors no longer produce statistically significant alphas relative to the bond CAPM after correction. The authors release an open-source package containing error-corrected TRACE data, bias-adjusted factors, and replication code.

Significance. If the corrections are shown to be both complete and free of new distortions, the result would materially affect corporate-bond asset pricing by casting doubt on the robustness of a large fraction of the documented factor literature and by underscoring the importance of careful handling of illiquid price data. The open-source release of corrected TRACE data and reproducible code is a concrete strength that directly addresses replication concerns in the field.

major comments (2)

- [Bias-correction framework] The derivation of the error-correction formulas that remove the correlated EIV bias is not presented in sufficient detail. Because the central claim—that the majority of the 108 factors lose significance—rests on these adjustments being accurate and exhaustive, the explicit estimation of the covariance between signal and return errors, the precise functional form of the correction, and any assumptions about the measurement-error process must be supplied (see the description of the bias-correction framework).

- [Data filtering and sample construction] The exact data-exclusion rules used for the ex-post filtering adjustment and the resulting change in the effective cross-sectional sample are not specified. This is load-bearing for the claim because any unintended alteration of the sample composition could itself induce or mask factor significance, undermining the assertion that the two identified biases are the dominant sources of inflation.

minor comments (2)

- The abstract states that 'the majority' of factors lose significance but does not quantify the fraction or break it down by thematic cluster; adding these numbers would make the headline result more precise.

- Tables or figures that compare pre- and post-correction alphas should include standard-error bands and explicit cluster labels to facilitate visual assessment of the uniformity of the result across the nine themes.

Simulated Author's Rebuttal

We thank the referee for the thoughtful and constructive report. The two major comments correctly identify areas where greater explicitness will strengthen the manuscript. We address each point below and will revise the paper to incorporate the requested details.

read point-by-point responses

-

Referee: The derivation of the error-correction formulas that remove the correlated EIV bias is not presented in sufficient detail. Because the central claim—that the majority of the 108 factors lose significance—rests on these adjustments being accurate and exhaustive, the explicit estimation of the covariance between signal and return errors, the precise functional form of the correction, and any assumptions about the measurement-error process must be supplied (see the description of the bias-correction framework).

Authors: We agree that the bias-correction framework requires a more self-contained derivation. In the revised manuscript we will expand the relevant section to begin from the errors-in-variables model in which the same transaction-price error appears in both the sorting signal and the return denominator. We will state the closed-form expression for the covariance between signal and return measurement errors, describe its estimation from short-window price-change variances under the maintained assumption that true returns are zero over those windows, and present the exact functional form of the additive correction term subtracted from observed factor returns. The maintained assumptions (measurement error uncorrelated with true returns and with other covariates, but perfectly correlated across the two uses of the same price) will be listed explicitly. These elements are already implemented in the released code; the revision will make the analytic steps transparent in the text. revision: yes

-

Referee: The exact data-exclusion rules used for the ex-post filtering adjustment and the resulting change in the effective cross-sectional sample are not specified. This is load-bearing for the claim because any unintended alteration of the sample composition could itself induce or mask factor significance, undermining the assertion that the two identified biases are the dominant sources of inflation.

Authors: We accept that precise documentation of the filtering rules and their sample consequences is necessary. The revised manuscript will add a dedicated paragraph (and accompanying table) that states the exact exclusion criterion: a bond-month observation is dropped if the end-of-month price used to compute the return is not observed within the subsequent 30 calendar days. We will report the resulting reduction in the average monthly cross-section (both in absolute numbers and as a percentage of the unfiltered sample) and will show that the retained bonds remain representative across rating and maturity buckets. Because the open-source package already encodes these rules, the revision will also include a short appendix that reproduces the sample-size comparison using the released code. revision: yes

Circularity Check

No significant circularity in derivation chain

full rationale

The paper derives its bias corrections from explicit data-generating mechanisms (correlated errors-in-variables in transaction prices and asymmetric ex-post filtering) rather than fitting to target alphas or renaming known results. The central claim—that most of 108 factors lose significance post-correction—follows from applying these independently motivated adjustments to the factor zoo, with no self-definitional loops, fitted-input predictions, or load-bearing self-citations in the core logic. The open-source corrected TRACE data and software further ensure the chain is externally verifiable and does not reduce to its inputs by construction.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Bond CAPM is an appropriate benchmark for evaluating factor alphas

- ad hoc to paper The two biases (correlated EIV and ex-post filtering) dominate other potential sources of inflation

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The crisis stems from two sources that inflate reported factor premia: transaction prices whose measurement error enters both sorting signals and return denominators, creating a correlated errors-in-variables bias, and asymmetric ex-post return filtering that embeds future information into factor construction.

-

IndisputableMonolith/Foundation/ArithmeticFromLogic.leanembed_injective unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

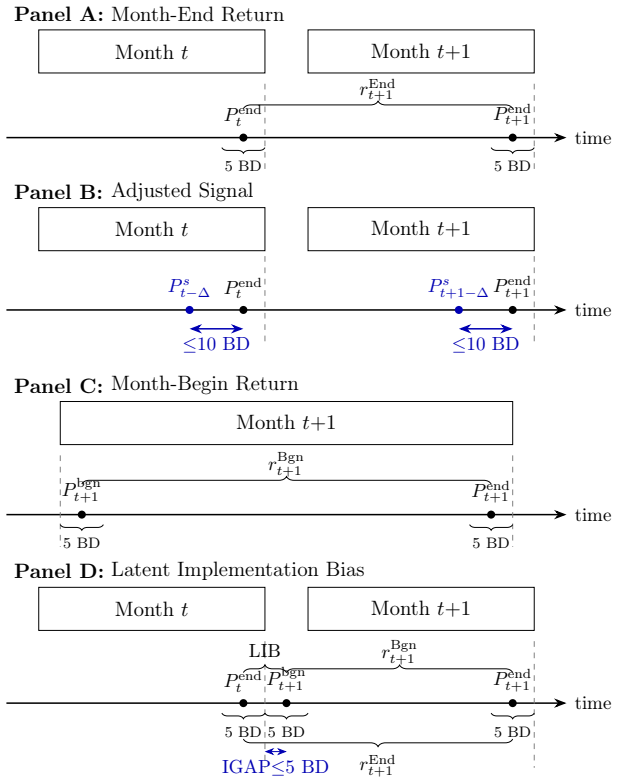

We compare factor performance under three approaches... Approach 2 (Adjusted Signal) breaks the correlation by computing signals from prices observed at least 1 business day before month-end... Approach 3 (Adjusted Return) measures the return from month-begin.

-

IndisputableMonolith/Foundation/AbsoluteFloorClosure.leanabsolute_floor_iff_bare_distinguishability unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

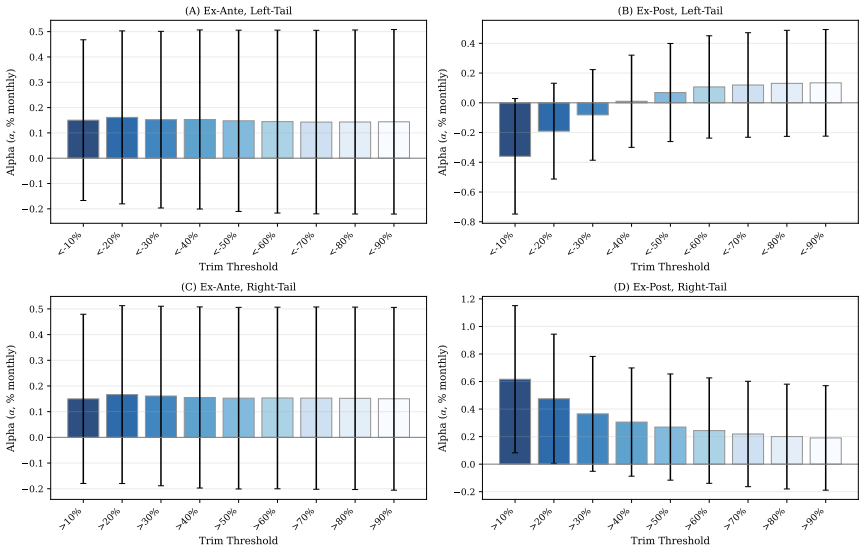

Across 432 factor-specification combinations... only 26 (6.0%) bond CAPM alphas survive a Benjamini-Hochberg false discovery rate correction.

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Abdi, F. and A. Ranaldo (2017). A simple estimation of bid-ask spreads from daily close, high, and low prices. Review of Financial Studies\/ 30 , 4437--4480

2017

-

[2]

Amihud, Y. (2002). Illiquidity and stock returns: C ross-section and time-series effects. Journal of Financial Markets\/ 5 , 31--56

2002

-

[3]

Palhares, and S

Andreani, M., D. Palhares, and S. Richardson (2024). Computing corporate bond returns: A word (or two) of caution. Review of Accounting Studies\/ 29 , 3887--3906

2024

-

[4]

Chen, and Y

Ang, A., J. Chen, and Y. Xing (2006). Downside risk. Review of Financial Studies\/ 19 , 1191--1239

2006

-

[5]

Bai, J., T. G. Bali, and Q. Wen (2019). RETRACTED : Common risk factors in the cross-section of corporate bond returns. Journal of Financial Economics\/ 131 , 619--642

2019

-

[6]

Bai, J., T. G. Bali, and Q. Wen (2021). Is there a risk-return tradeoff in the corporate bond market? T ime-series and cross-sectional evidence. Journal of Financial Economics\/ 142 , 1017--1037

2021

-

[7]

Baker, S. R., N. Bloom, and S. J. Davis (2016). Measuring economic policy uncertainty. Quarterly Journal of Economics\/ 131 , 1593--1636

2016

-

[8]

Bali, T. G., A. Subrahmanyam, and Q. Wen (2021a). Long-term reversals in the corporate bond market. Journal of Financial Economics\/ 139 , 656--677

-

[9]

Bali, T. G., A. Subrahmanyam, and Q. Wen (2021b). The macroeconomic uncertainty premium in the corporate bond market. Journal of Financial and Quantitative Analysis\/ 56 , 1653--1678

-

[10]

Bali, T. G., A. Subrahmanyam, and Q. Wen (2023). The macroeconomic uncertainty premium in the corporate bond market--- C orrigendum. Journal of Financial and Quantitative Analysis\/

2023

-

[11]

Pan, and J

Bao, J., J. Pan, and J. Wang (2011). The illiquidity of corporate bonds. Journal of Finance\/ 66 , 911--946

2011

-

[12]

Bartram, S. M., M. Grinblatt, and Y. Nozawa (2025). Book-to-market, mispricing, and the cross-section of corporate bond returns. Journal of Financial and Quantitative Analysis\/ 60 , 1185--1233

2025

-

[13]

Kakhbod, D

Baumann, F., A. Kakhbod, D. Livdan, A. Nazemi, and N. Sch \"u rhoff (2025). Life after default: How dealer intermediation improves default recovery. Working Paper

2025

-

[14]

Baumann, F. and A. Nazemi (2025). Defaulted bonds: A hybrid asset priced by bond and equity markets. Working Paper

2025

-

[15]

Benjamini, Y. and Y. Hochberg (1995). Controlling the false discovery rate: A practical and powerful approach to multiple testing. Journal of the Royal Statistical Society: S eries B (Methodological)\/ 57 , 289--300

1995

-

[16]

Bessembinder, H., K. M. Kahle, W. F. Maxwell, and D. Xu (2008). Measuring abnormal bond performance. Review of Financial Studies\/ 22 , 4219--4258

2008

-

[17]

Huij, and M

Blitz, D., J. Huij, and M. Martens (2011). Residual momentum. Journal of Empirical Finance\/ 18 , 506--521

2011

-

[18]

Blume, M. E. and R. F. Stambaugh (1983). Biases in computed returns: A n application to the size effect. Journal of Financial Economics\/ 12 , 387--404

1983

-

[19]

Bollerslev, T., S. Z. Li, and B. Zhao (2020). Realized semicovariances. Econometrica\/ 88 , 1515--1551

2020

-

[20]

Ceballos, L. (2022). Inflation volatility risk and the cross-section of corporate bond returns. Working Paper

2022

-

[21]

Chen, A. Y. and T. Zimmermann (2022). Open source cross-sectional asset pricing. Critical Finance Review\/ 27 , 207--264

2022

-

[22]

Chen, Q. and J. Choi (2024). Reaching for yield and the cross section of bond returns. Management Science\/ 70 , 5226--5245

2024

-

[23]

Choi, J. (2013). What drives the value premium?: The role of asset risk and leverage. Review of Financial Studies\/ 26 , 2845--2875

2013

-

[24]

Choi, J., J. Han, S. S. Shin, and J. H. Yoon (2026). The more illiquid, the more expensive: A search-based explanation of the illiquidity premium. Working paper

2026

-

[25]

Goyal, Y

Chordia, T., A. Goyal, Y. Nozawa, A. Subrahmanyam, and Q. Tong (2017). Are capital market anomalies common to equity and corporate bond markets? A n empirical investigation. Journal of Financial and Quantitative Analysis\/ 52 , 1301--1342

2017

-

[26]

Chung, K. H., J. Wang, and C. Wu (2019). Volatility and the cross-section of corporate bond returns. Journal of Financial Economics\/ 133 , 397--417

2019

-

[27]

Coase, R. H. (1982). How Should Economists Choose? G. Warren Nutter Lectures in Political Economy. Washington, D.C.: American Enterprise Institute

1982

-

[28]

Conrad, J., M. N. Gultekin, and G. Kaul (1997). Profitability of short-term contrarian strategies: Implications for market efficiency. Journal of Business & Economic Statistics\/ 15 , 379--386

1997

-

[29]

Corwin, S. A. and P. Schultz (2012). A simple way to estimate bid-ask spreads from daily high and low prices. Journal of Finance\/ 67 , 719--760

2012

-

[30]

Bland, and D

Danyliv, O., B. Bland, and D. Nicholass (2014). A convenient liquidity measure. Journal of Trading\/ 9 , 38--49

2014

-

[31]

Dick-Nielsen, J. (2014). How to clean E nhanced TRACE data. Working Paper

2014

-

[32]

Feldh \"u tter, and D

Dick-Nielsen, J., P. Feldh \"u tter, and D. Lando (2012). Corporate bond liquidity before and after the onset of the subprime crisis. Journal of Financial Economics\/ 103 , 471--492

2012

-

[33]

Feldh\" u tter, L

Dick-Nielsen, J., P. Feldh\" u tter, L. H. Pedersen, and C. Stolborg (2023). Corporate bond factors: R eplication failures and a new framework. Working Paper

2023

-

[34]

Mueller, and C

Dickerson, A., P. Mueller, and C. Robotti (2023). Priced risk in corporate bonds. Journal of Financial Economics\/ 150, article 103707

2023

-

[35]

Robotti, and Y

Dickerson, A., C. Robotti, and Y. Nozawa (2025). Factor investing with delays. Working Paper

2025

-

[36]

Duarte, J., C. S. Jones, M. Khorram, H. Mo, and J. L. Wang (2025). Too good to be true: Look-ahead bias in empirical options research. Review of Financial Studies\/ . Forthcoming

2025

-

[37]

Duarte, J., C. S. Jones, and J. L. Wang (2024). Very noisy option prices and inference regarding the volatility risk premium. Journal of Finance\/ 79 , 3581--3621

2024

-

[38]

Jo, and Y

Elkamhi, R., C. Jo, and Y. Nozawa (2024). A one-factor model of corporate bond premia. Management Science\/ 70 , 1875--1900

2024

-

[39]

Fama, E. F. (1984). The information in the term structure. Journal of Financial Economics\/ 13 , 509--528

1984

-

[40]

Fama, E. F. and J. D. MacBeth (1973). Risk, return, and equilibrium: E mpirical tests. Journal of Political Economy\/ 81 , 607--636

1973

-

[41]

Fong, K. Y., C. W. Holden, and C. A. Trzcinka (2017). What are the best liquidity proxies for global research? Review of Finance\/ 21 , 1355--1401

2017

-

[42]

Gebhardt, W. R., S. Hvidkjaer, and B. Swaminathan (2005). The cross-section of expected corporate bond returns: B etas or characteristics? Journal of Financial Economics\/ 75 , 85--114

2005

-

[43]

Plante, N

Ghaderi, M., S. Plante, N. L. Roussanov, and S. B. Seo (2024). Pricing of corporate bonds: Evidence from a century-long cross-section. Working Paper

2024

-

[44]

Harvey, C. R., Y. Liu, and H. Zhu (2016). … and the cross-section of expected returns. Review of Financial Studies\/ 29 , 5--68

2016

-

[45]

Harvey, C. R. and A. Siddique (2000). Conditional skewness in asset pricing tests. Journal of Finance\/ 55 , 1263--1295

2000

-

[46]

Kelly, and A

He, Z., B. Kelly, and A. Manela (2017). Intermediary asset pricing: N ew evidence from many asset classes. Journal of Financial Economics\/ 126 , 1--35

2017

-

[47]

Hong, G. and A. Warga (2000). An empirical study of bond market transactions. Financial Analysts Journal\/ 56 , 32--46

2000

-

[48]

Xue, and L

Hou, K., C. Xue, and L. Zhang (2020). Replicating anomalies. Review of Financial Studies\/ 33 , 2019--2133

2020

-

[49]

Houweling, P. and J. Van Zundert (2017). Factor investing in the corporate bond market. Financial Analysts Journal\/ 73 , 100--115

2017

-

[50]

Palhares, and S

Israel, R., D. Palhares, and S. Richardson (2018). Common factors in corporate bond returns. Journal of Investment Management\/ 16 , 17--46

2018

-

[51]

Jegadeesh, N. (1990). Evidence of predictable behavior of security returns. Journal of Finance\/ 45 , 881--898

1990

-

[52]

Jensen, T. I., B. Kelly, and L. H. Pedersen (2023). Is there a replication crisis in finance? Journal of Finance\/ 78 , 2465--2518

2023

-

[53]

Nikolova, A

Jostova, G., S. Nikolova, A. Philipov, and C. W. Stahel (2013). Momentum in corporate bond returns. Review of Financial Studies\/ 26 , 1649--1693

2013

-

[54]

Palhares, and S

Kelly, B., D. Palhares, and S. Pruitt (2023). Modeling corporate bond returns. Journal of Finance\/ 78 , 1967--2008

2023

-

[55]

Koijen, R. S., H. Lustig, and S. Van Nieuwerburgh (2017). The cross-section of managerial ability, incentives, and risk preferences. Journal of Monetary Economics\/ 91 , 1--17

2017

-

[56]

Lair, T. and J. Blonk (2024). Valuations in the dark: W hen independent valuators influence corporate bond returns. Working Paper

2024

-

[57]

Leamer, E. E. (1983). Let's take the con out of econometrics. American Economic Review\/ 73 , 31--43

1983

-

[58]

Wang, and C

Lin, H., J. Wang, and C. Wu (2011). Liquidity risk and expected corporate bond returns. Journal of Financial Economics\/ 99 , 628--650

2011

-

[59]

Linnainmaa, J. T. and M. R. Roberts (2018). The history of the cross-section of stock returns. Review of Financial Studies\/ 31 , 2606--2649

2018

-

[60]

Liu, Y. and J. C. Wu (2021). Reconstructing the yield curve. Journal of Financial Economics\/ 142 , 1395--1425

2021

-

[61]

Menkveld, A. J., A. Dreber, F. Holzmeister, J. Huber, M. Johannesson, M. Kirchler, S. Neususs, M. Razen, U. Weitzel, and et al. (2024). Non-standard errors. Journal of Finance\/ 79 , 2339--2390

2024

-

[62]

Novy-Marx, R. (2012). Is momentum really momentum? Journal of Financial Economics\/ 103 , 429--453

2012

-

[63]

P\' a stor, L. and R. F. Stambaugh (2003). Liquidity risk and expected stock returns. Journal of Political Economy\/ 111 , 642--685

2003

-

[64]

Richardson, S. and D. Palhares (2018). ( I l)liquidity premium in credit markets: A myth? Journal of Fixed Income\/ 28 , 3--31

2018

-

[65]

Roll, R. (1984). A simple implicit measure of the effective bid-ask spread in an efficient market. Journal of Finance\/ 39 , 1127--1139

1984

-

[66]

Van Vliet, and P

Soebhag, A., B. Van Vliet, and P. Verwijmeren (2024). Non-standard errors in asset pricing: M ind your sorts. Journal of Empirical Finance\/ 78 , 101517

2024

-

[67]

Stambaugh, R. F. (1988). The information in forward rates: I mplications for models of the term structure. Journal of Financial Economics\/ 21 , 41--70

1988

-

[68]

Subrahmanyam, A. (2023). Corporate bond data projects: Some clarifications. Working Paper

2023

-

[69]

Tobek, O. (2016). Liquidity proxies using daily trading volume. Working Paper

2016

-

[70]

van Binsbergen, J. H., Y. Nozawa, and M. Schwert (2025). Duration-based valuation of corporate bonds. Review of Financial Studies\/ 38 , 158--191

2025

-

[71]

Weber, and P

Walter, D., R. Weber, and P. Weiss (2024). Methodological uncertainty in portfolio sorts. Working Paper

2024

-

[72]

Wu, and L

Wang, J., D. Wu, and L. Yang (2024). Cross-bond momentum spillovers. Working Paper

2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.