Recognition: 2 theorem links

· Lean TheoremOptimal Annuitization Time under a Mortality Shock

Pith reviewed 2026-05-10 16:39 UTC · model grok-4.3

The pith

Explicit closed-form solutions exist for the value function and optimal annuitization boundaries when retirement wealth faces a sudden permanent mortality shock.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

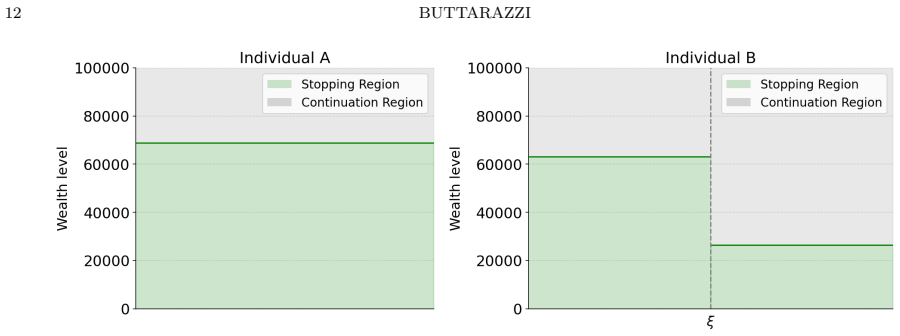

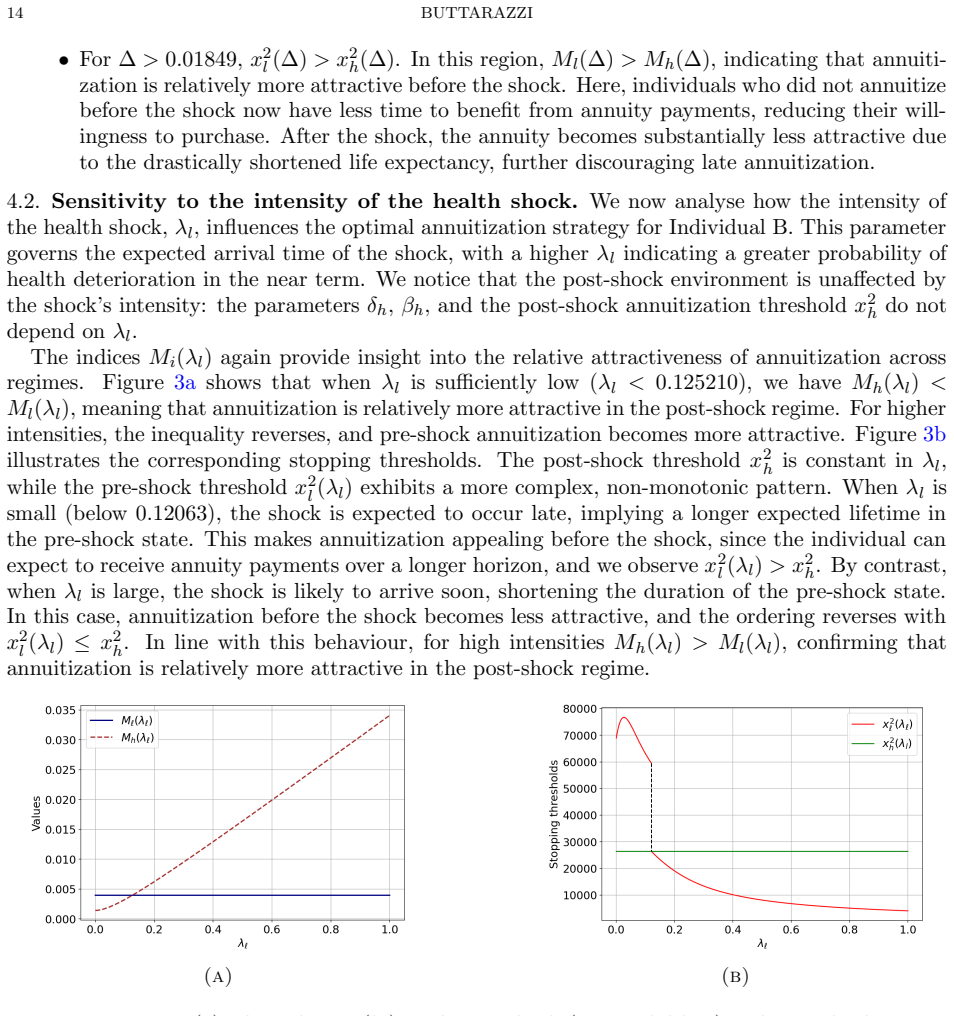

The paper derives explicit closed-form solutions for the value function and the associated optimal stopping boundaries in an optimal annuitization problem under a mortality shock. An individual's retirement wealth follows geometric Brownian motion and can be converted at any time into a life annuity. The mortality shock is a single permanent jump at an exponentially distributed time, so the problem reduces to optimal stopping across two health states with different mortality intensities. The resulting analytical expressions characterize both the value function in each state and the optimal annuitization thresholds, with the strategy governed by the relative attractiveness of the annuity, the

What carries the argument

The two-state optimal stopping framework with an exponential mortality shock time, where the value function satisfies ordinary differential equations in each health state subject to value-matching and smooth-pasting conditions at the free boundaries.

If this is right

- The optimal annuitization boundary in good health differs from the boundary in poor health because of the change in mortality intensity.

- Higher money's worth of the annuity pulls the optimal stopping boundary downward in both states.

- Stronger bequest motives raise the thresholds, delaying annuitization.

- The likelihood of the health shock alters the value of waiting in the initial health state relative to the constant-mortality benchmark.

- Explicit formulas allow immediate computation of the regions in which it is optimal to annuitize immediately versus continue investing.

Where Pith is reading between the lines

- The framework suggests that personalized annuity recommendations should incorporate an individual's estimated probability of future health shocks rather than using average mortality tables.

- Similar closed-form techniques could be applied to other irreversible choices under jump risk, such as the timing of long-term care insurance purchases.

- If health shocks are correlated across family members, the model implies that joint annuitization decisions would require an expanded state space.

Load-bearing premise

The mortality shock is modeled as a single permanent jump occurring at an exponentially distributed time, with the annuitization decision treated as an optimal stopping problem across exactly two health states.

What would settle it

Empirical records of when individuals actually annuitize after experiencing a documented sudden health decline, compared against the model's predicted boundaries for given annuity money's worth, investment volatility, and bequest strength, would falsify the claim if the observed timings deviate systematically.

Figures

read the original abstract

In this paper, we derive explicit closed-form solutions for the value function and the associated optimal stopping boundaries in an optimal annuitization problem under a mortality shock. We consider an individual whose retirement wealth is invested in a financial fund following the dynamics of a geometric Brownian motion and has the option at any time to irreversibly convert their wealth into a life annuity. The individual faces a sudden, permanent health deterioration occurring at a random, exponentially distributed time, and the annuitization decision is modelled as an optimal stopping problem across two health states. Our analytical expressions characterise both the value function and the optimal timing of annuitization. The results provide clear economic intuition: the optimal strategy is governed by the critical interplay between the relative attractiveness of the annuity (money's worth), the financial returns from the investment fund, and bequest motives across different health states. A numerical analysis compares the optimal annuitization strategy of an individual facing a health shock against a benchmark case with constant mortality, highlighting how the likelihood and severity of a health shock significantly alter optimal annuitization behaviour.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. This paper models the optimal timing of annuitization for an individual with wealth invested in a geometric Brownian motion fund, facing a sudden permanent health deterioration (mortality shock) occurring at an exponentially distributed time. The annuitization decision is formulated as an optimal stopping problem across two health states (pre- and post-shock), and the authors derive explicit closed-form solutions for the value functions and associated optimal stopping boundaries, along with numerical comparisons to a constant-mortality benchmark.

Significance. The derivation of explicit closed-form solutions for the pre- and post-shock value functions (via the linear second-order ODEs generated by the GBM operator plus the jump-intensity term) and the explicit algebraic system for the free boundaries is a clear technical strength, as is the provision of economic intuition on the interplay between annuity money's worth, investment returns, bequest motives, and shock parameters. If the derivations hold, the results and numerical analysis contribute to the literature by showing how the likelihood and severity of health shocks alter optimal annuitization behavior relative to constant-mortality cases.

minor comments (2)

- [Abstract] Abstract: the statement that 'explicit closed-form solutions' are derived would benefit from a brief qualifier noting that these arise from solving the regime-specific linear ODEs and enforcing value-matching/smooth-pasting conditions at the free boundaries.

- [Numerical Analysis] Numerical analysis section: the parameter values chosen for the GBM drift/volatility, force of mortality in each state, money's worth, and bequest coefficient should be tabulated or explicitly listed to facilitate replication and interpretation of the reported strategy differences.

Simulated Author's Rebuttal

We thank the referee for the careful reading of our manuscript and for the positive recommendation of minor revision. The referee's summary correctly identifies the core modeling framework, the derivation of closed-form value functions and free boundaries, and the numerical comparison to the constant-mortality benchmark. We are pleased that the technical contribution and economic intuition are viewed as strengths.

Circularity Check

No significant circularity: standard optimal stopping derivation on two-state Markov model

full rationale

The paper sets up a two-state optimal stopping problem with wealth following GBM and mortality shock as an exponential jump. Pre- and post-shock value functions are defined via the infinitesimal generator (second-order linear ODEs with constant coefficients plus jump intensity term), solved in closed form as linear combinations of power solutions plus particular solution. Optimal boundaries are then fixed by the standard value-matching and smooth-pasting conditions, producing an algebraic system solved explicitly in the parameters. This chain is self-contained mathematical derivation from the stated SDE and payoff structure; no fitted inputs are relabeled as predictions, no self-citations are load-bearing for the closed forms, and no ansatz or uniqueness result is smuggled in. The result is independent of any external fitted quantities or prior author work.

Axiom & Free-Parameter Ledger

free parameters (4)

- money's worth of the annuity

- drift and volatility of the geometric Brownian motion

- force of mortality in each health state

- bequest motive coefficient

axioms (3)

- domain assumption Wealth process follows geometric Brownian motion

- domain assumption Mortality shock arrival time is exponentially distributed and permanent

- standard math Optimal stopping theory applies directly to the two-regime value function

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclearThe problem is solved backwards... explicit solutions of the form A x^gamma + B x^delta plus particular solution... free boundaries fixed by value-matching and smooth-pasting

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclearV(x, μ_l) = sup ... e^{-r_l τ} δ_l (X_τ − K) + integral terms with λ_l V(X_t, μ_h)

Reference graph

Works this paper leans on

-

[1]

Agarwal and D

R.P. Agarwal and D. O’Regan.Ordinary and partial differential equations: with special functions, Fourier series, and boundary value problems. Springer Science & Business Media, 2008

2008

-

[2]

M. Buttarazzi, T. De Angelis, and G. Stabile. Optimal annuitization with stochastic mortality: Piecewise deter- ministic mortality force.arXiv preprint arXiv:2509.13091, 2025

-

[3]

Buttarazzi and G

M. Buttarazzi and G. Stabile. The market value of optimal annuitization and bequest motives. InMathematical and Statistical Methods for Actuarial Sciences and Finance, pages 67–73. Springer, 2024

2024

-

[4]

Duffie, J

D. Duffie, J. Pan, and K. Singleton. Transform analysis and asset pricing for affine jump-diffusions.Econometrica, 68(6):1343–1376, 2000. M. Buttarazzi: School of Management and Economics, Dept. ESOMAS, University of Torino, Corso Unione Sovietica, 218 Bis, 10134, Torino, Italy. Email address:matteo.buttarazzi@unito.it

2000

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.