Recognition: unknown

The Long-Only Minimum Variance Portfolio in a One-Factor Market: Theory and Asymptotics

Pith reviewed 2026-05-10 16:30 UTC · model grok-4.3

The pith

In a one-factor market the long-only minimum variance portfolio is supported exactly on assets whose betas exceed a positive threshold solving an integral equation.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

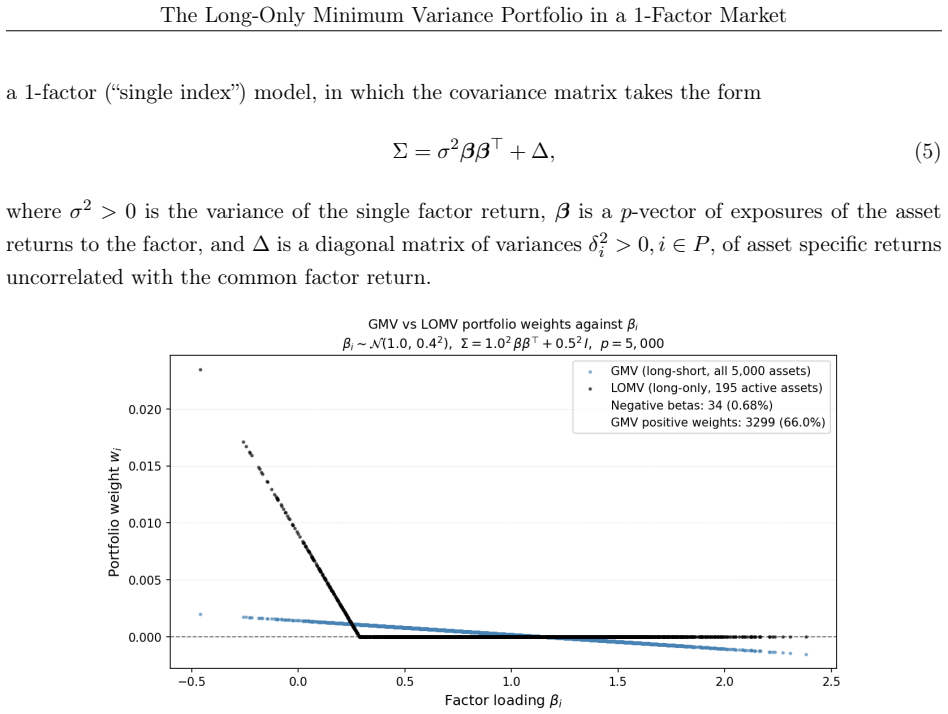

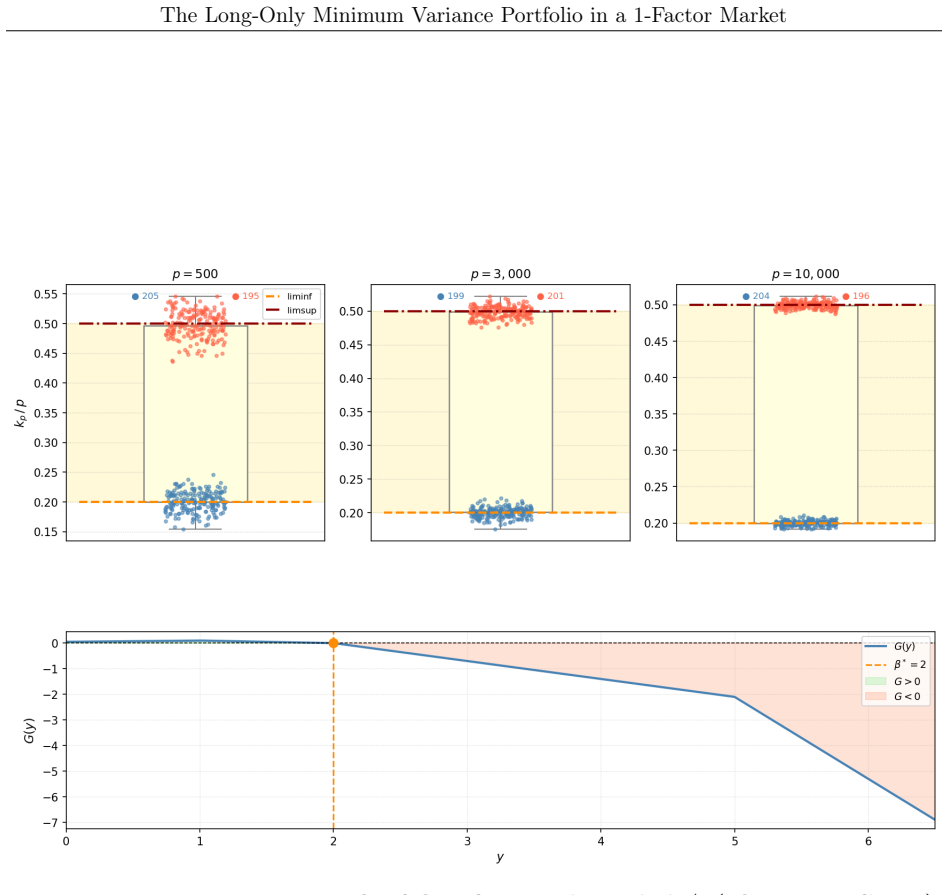

Under the one-factor covariance model the long-only minimum-variance portfolio is given explicitly once the active set is known; the active set itself is characterized by a threshold condition on the betas that can be computed from the factor loadings and the target. In the p → ∞ regime with betas drawn from cdf F the active ratio converges to F(β*), where β* ≥ 0 solves the integral equation determined by F. When F is continuous and F(0) = 0 the limit is zero; when F(0) is small the rate is O(F(0)^{1/3}) under mild moment and concentration assumptions.

What carries the argument

The explicit characterization of the active asset set, which selects assets whose betas lie above the threshold β* solving the integral equation fixed by the beta distribution F.

If this is right

- The portfolio can be constructed by first solving for the threshold β* and then assigning weights only to assets with betas strictly larger than β*.

- When every beta is positive the limiting active ratio is zero, so the portfolio becomes sparse in the high-dimensional limit.

- The same integral-equation threshold governs the mixed-sign case, resolving the extension left open by earlier work.

- The convergence rate O(F(0)^{1/3}) supplies a quantitative bound on how many negative-beta assets survive in the active set when their proportion is small.

Where Pith is reading between the lines

- The sparsity result suggests that, for equity universes whose betas are mostly positive, long-only minimum-variance portfolios will concentrate on a vanishing fraction of names as the universe grows.

- The explicit threshold rule could be used to derive approximate closed-form risk formulas for large portfolios even when the exact active set is not enumerated.

- One could test whether real-market active ratios track the predicted F(β*) by sorting stocks on estimated betas and comparing the empirical active fraction to the theoretical limit.

Load-bearing premise

The covariance matrix is exactly that of a one-factor model, the betas are drawn independently from a fixed distribution F, and the stated mild moment and concentration conditions hold.

What would settle it

A large-scale simulation or empirical check in which the realized fraction of positive-weight assets in the long-only minimum-variance portfolio fails to approach the predicted F(β*) for a known F would refute the high-dimensional convergence claim.

Figures

read the original abstract

We study the long-only minimum variance (LOMV) portfolio under a one-factor covariance model with asset betas of arbitrary sign. We provide an explicit solution in terms of the set of active (positive weight) assets, and provide an explicit and computable characterization of the active set. As a corollary we resolve an open question of \citet{qi2021} concerning the extension to mixed-sign betas. In the high-dimensional regime $p \to \infty$ where the betas are drawn from a distribution with cdf $F$, we prove that the proportion of active assets (the active ratio) in the LOMV portfolio converges in almost all cases to $F(\beta^{*})$, where $\beta^* \geq 0$ is the root of an explicit integral equation determined by $F$. This is a variation of a result first appearing in \citet{bernstein2025}. In particular, when $F$ is continuous and all betas are positive ($F(0)=0$), the active ratio converges to zero. When $F(0) >0$ is small, under mild moment conditions and concentration bounds we establish the convergence rate $F(\beta^*)=O(F(0)^{1/3})$ as $F(0) \to 0$.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies the long-only minimum-variance portfolio under an exact one-factor covariance model that permits betas of either sign. It supplies an explicit solution expressed via the active (positive-weight) asset set together with a computable characterization of that set, thereby resolving an open question of Qi et al. (2021) on the mixed-sign case. In the high-dimensional regime p→∞ with betas drawn i.i.d. from a fixed cdf F, the paper proves that the active ratio converges almost surely to F(β*), where β*≥0 solves an explicit integral equation determined by F; when F is continuous and F(0)=0 the limit is zero, while for small F(0)>0 a rate F(β*)=O(F(0)^{1/3}) is obtained under mild moment and concentration conditions.

Significance. If the derivations are correct, the work supplies a precise theoretical account of the sparsity induced by the long-only constraint in one-factor markets. The explicit active-set rule and the high-dimensional limit (including the rate result) extend earlier findings and furnish falsifiable predictions for large portfolios. These contributions are valuable for both the mathematical-finance literature on constrained optimization and for practical high-dimensional portfolio construction.

minor comments (3)

- The qualifier “in almost all cases” appearing in the abstract and high-dimensional theorem should be replaced by an explicit probability statement (e.g., “with probability 1 under the stated concentration hypotheses”) once the precise measure-theoretic setting is introduced.

- The integral equation satisfied by β* is described as “explicit and determined by F”; a short displayed equation in the introduction or the statement of the main limit theorem would improve immediate readability.

- The bibliography entries for qi2021 and bernstein2025 should be completed with full publication details (journal, volume, pages) if they are not already present.

Simulated Author's Rebuttal

We thank the referee for their positive assessment of the manuscript, accurate summary of our contributions, and recommendation for minor revision. The report correctly identifies the explicit active-set characterization and the high-dimensional asymptotic results for the long-only minimum-variance portfolio under the one-factor model with mixed-sign betas.

Circularity Check

No significant circularity identified

full rationale

The paper derives an explicit active-set characterization for the long-only minimum-variance quadratic program directly from the KKT stationarity and complementarity conditions applied to the exact one-factor covariance model. The high-dimensional limit is obtained by substituting the empirical measure of i.i.d. betas drawn from F into the resulting threshold rule and passing to the integral equation whose root β* yields the limiting active proportion F(β*). Both steps are self-contained consequences of the model assumptions, moment conditions, and concentration hypotheses; the integral equation is solved from F rather than fitted to data or defined in terms of the target quantity. The reference to bernstein2025 is noted as a related prior result but is not load-bearing for the present derivation, which independently resolves the mixed-sign extension of qi2021. No self-definitional, fitted-input, or self-citation reduction appears in the claimed chain.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Asset returns follow a one-factor model with covariance determined by betas of arbitrary sign.

- domain assumption In the p to infinity limit, betas are i.i.d. draws from a distribution F satisfying the listed continuity or moment conditions.

Reference graph

Works this paper leans on

-

[1]

SIAM, 2nd edition, 2023

Amir Beck.Introduction to Nonlinear Optimization: Theory, Algorithms, and Applications with Python and MATLAB. SIAM, 2nd edition, 2023. A. Bernstein and A. Shkolnik. Asymptotics of quadratic forms on a simplex. preprint, September 2025. M. J. Best and R. R. Grauer. Positively weighted minimum-variance portfolios and the structure of asset expected returns...

2023

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.