Recognition: unknown

On the Structure of Risk Contribution: A Leave-One-Out Decomposition into Inherent and Correlation Risk

Pith reviewed 2026-05-10 15:15 UTC · model grok-4.3

The pith

Standard risk contribution decomposes into an always-positive inherent volatility part and a correlation part that can hedge or amplify.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

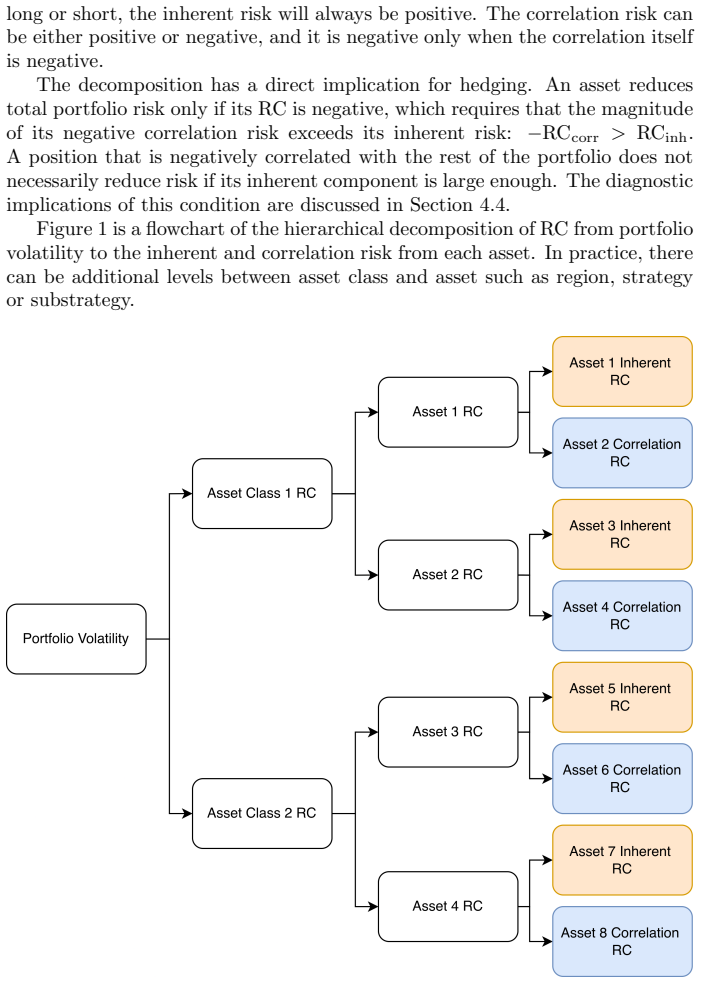

Using a leave-one-out representation, each position's risk contribution separates into an inherent risk term that reflects only its own volatility independent of the portfolio and a correlation risk term that captures its covariance with the remainder; the inherent term is always non-negative while the correlation term can be positive or negative, and the two parts together sum exactly to the standard risk contribution for every position.

What carries the argument

The leave-one-out decomposition of risk contribution, which isolates the position-specific volatility effect by comparing full-portfolio risk to risk without that position.

If this is right

- The inherent component remains positive for every position regardless of portfolio context.

- The correlation component reveals when a position functions as a hedge by moving against the rest of the holdings.

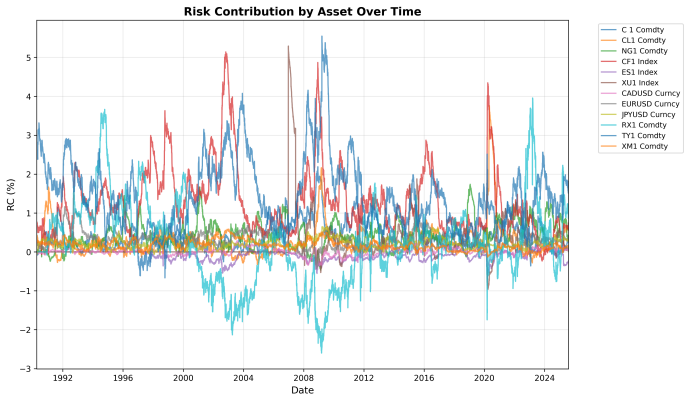

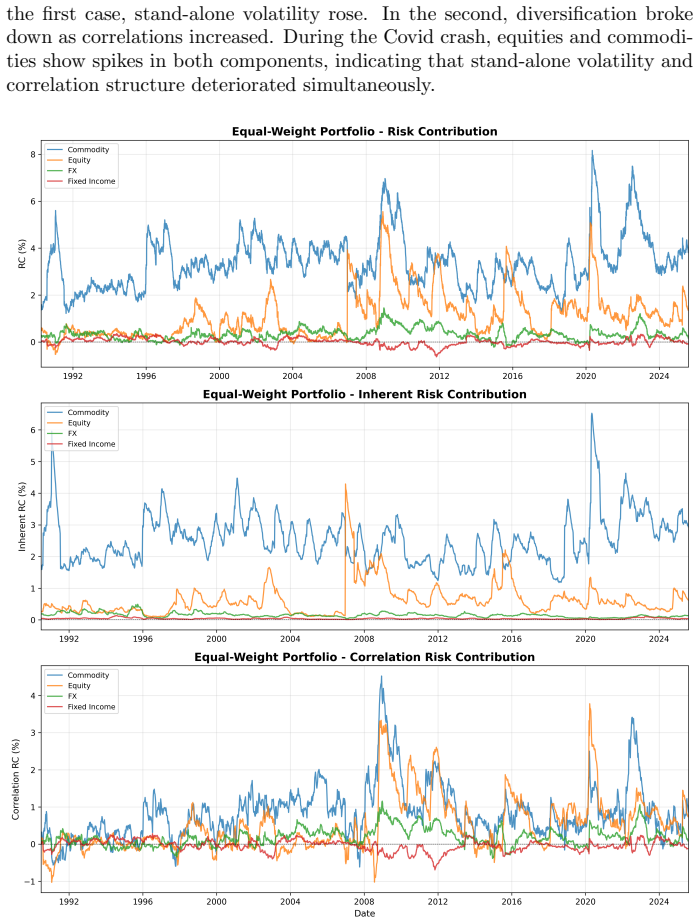

- Tracking the two components separately over time distinguishes volatility shocks from correlation shifts as drivers of portfolio risk changes.

- The split supplies diagnostics that distinguish isolated volatility from co-movement without losing the additive property of total risk.

Where Pith is reading between the lines

- Portfolio managers could monitor the ratio of inherent to correlation risk to decide when to reduce position size versus add offsetting holdings.

- Stress tests could apply shocks separately to the volatility and correlation components to isolate which change most affects total risk.

- The approach might extend naturally to other additive risk measures such as expected shortfall if a similar leave-one-out identity holds.

Load-bearing premise

The leave-one-out calculation isolates the standalone volatility term without needing any extra assumptions on return distributions or time-series properties beyond those already used in ordinary covariance-based risk contribution.

What would settle it

Apply the decomposition to a two-asset portfolio with known zero correlation between assets; if the correlation-risk terms fail to sum exactly to zero while the inherent-risk terms sum to the total portfolio risk, the claimed separation does not hold.

Figures

read the original abstract

This paper develops a decomposition of standard Risk Contribution (RC) into two economically interpretable components: inherent risk and correlation risk. Using a leave-one-out representation, each position's RC separates into a term reflecting its own volatility contribution independent of the portfolio and a term capturing its covariance with the remainder of the portfolio. The inherent component is always positive, arising from the intrinsic volatility of the position, while the correlation component may amplify or mitigate total portfolio risk depending on how the position moves relative to other holdings. Because the decomposition operates within standard RC, it preserves the property of strict additivity. This separation provides diagnostic insight not visible from aggregate risk contributions alone. It distinguishes whether a position contributes risk because it is volatile in isolation or because it is highly correlated with the rest of the portfolio, and it clarifies when a negatively correlated position functions as an effective hedge. Two approaches to time-series analysis are presented to track how inherent and correlation risk evolve across market regimes, revealing whether changes in portfolio risk during stress periods are driven by volatility shocks, correlation shifts, or both. Empirical illustrations suggest that the decomposition provides stable, transparent, and easily implementable risk diagnostics that can support portfolio risk reporting, stress testing, and performance attribution.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a leave-one-out decomposition of standard risk contribution (RC) into an inherent risk component (w_i² σ_i² / σ_p) reflecting a position's standalone volatility and a correlation risk component (w_i cov(R_i, R_{p-i}) / σ_p) capturing its interaction with the remainder of the portfolio. It claims the decomposition is an exact identity that preserves strict additivity of total RC, with the inherent component always non-negative, and extends the approach with two time-series methods to track component evolution across market regimes, illustrated by empirical examples.

Significance. If the claims hold, the decomposition supplies a parameter-free, algebraically exact diagnostic that separates intrinsic volatility effects from correlation effects within the standard RC framework. This distinction is useful for risk reporting, identifying effective hedges, and attributing changes in portfolio risk to volatility shocks versus correlation shifts. The approach requires only second-moment assumptions already implicit in covariance-based RC and adds no free parameters or fitted quantities, strengthening its transparency and implementability for stress testing and attribution.

minor comments (3)

- [Abstract] The abstract states that the decomposition 'preserves the property of strict additivity' but does not point to the specific equation or section demonstrating that sum(inherent_i + correlation_i) = σ_p; adding this reference would clarify the claim for readers.

- [Section on time-series analysis] The two time-series approaches for tracking inherent and correlation risk across regimes are described at a high level; the manuscript should specify the exact rolling-window lengths, covariance estimation procedure (e.g., sample vs. shrinkage), and any stationarity or look-ahead bias checks.

- [Empirical section] Empirical illustrations are said to show 'stable, transparent' diagnostics, yet no quantitative summary statistics (e.g., average inherent vs. correlation shares per regime or changes in stress periods) are provided to allow readers to gauge effect sizes.

Simulated Author's Rebuttal

We thank the referee for the positive and accurate summary of our manuscript, as well as for the favorable assessment of its significance and the recommendation of minor revision. The referee correctly identifies the core contribution: an exact, parameter-free leave-one-out decomposition of standard risk contribution that isolates an always-non-negative inherent volatility term from a signed correlation term while preserving additivity.

Circularity Check

Decomposition is exact algebraic identity from standard RC definition

full rationale

The paper's core contribution is a leave-one-out rewriting of the standard risk contribution formula RC_i = w_i * (Σw)_i / σ_p. Expanding cov(R_i, R_p) = cov(R_i, R_i) + cov(R_i, R_{p-i}) directly yields the two terms w_i² σ_i² / σ_p (inherent) and w_i cov(R_i, R_{p-i}) / σ_p (correlation), which sum to RC_i by construction. This requires only the existence of second moments and the usual covariance-based marginal risk definition; no parameters are fitted, no external uniqueness theorem is invoked, and no self-citation chain supports the separation. The result is therefore a transparent re-expression rather than a derived prediction or fitted claim. No load-bearing step reduces to its own inputs beyond ordinary algebraic identity, so the derivation chain is self-contained.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Existence of a well-defined covariance matrix for asset returns that allows computation of risk contributions

invented entities (2)

-

Inherent risk component

no independent evidence

-

Correlation risk component

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Bredin, D., Conlon, T., & Pot` ı, V. (2015). Does gold glitter in the long-run? Gold as a hedge and safe haven across time and investment horizon. International Review of Financial Analysis,41, 320–328. https://doi. org/10.1016/j.irfa.2015.01.010 Chopra, V. K., & Ziemba, W. T. (1993). The Effect of Errors in Means, Vari- ances, and Covariances on Optimal ...

-

[2]

https://doi.org/10.3386/w8554 Grinold, R. C., & Kahn, R. N. (1999, November 16).Active Portfolio Manage- ment (PB). McGraw Hill Professional. Horasanl, M. (n.d.). Portfolio Selection by Using Time Varying Covariance Ma- trices.Journal of Economic and Social Research,9(2), 1–22. Ledoit, O., & Wolf, M. (2003). Improved estimation of the covariance matrix of...

-

[3]

We begin with the claim from eq

https://doi.org/10.1209/epl/i2002-00135-4 24 Appendices A iVol Non-additivity This appendix derives that the sum of the iVols is always greater than or equal to the portfolio volatility, which implies that iVol is not strictly additive. We begin with the claim from eq. (8) σp ≤ X a∈p iVol(a) Substituting in eq. (2) σp ≤ X a∈p σp − q σ2p +w 2aσ2a −2w acov(...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.