Recognition: unknown

Forecasting Oil Prices Across the Distribution: A Quantile VAR Approach

Pith reviewed 2026-05-10 13:42 UTC · model grok-4.3

The pith

A Quantile Bayesian VAR model improves real oil price forecasts at the median and especially in the left tail by capturing varying predictor effects across the distribution.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

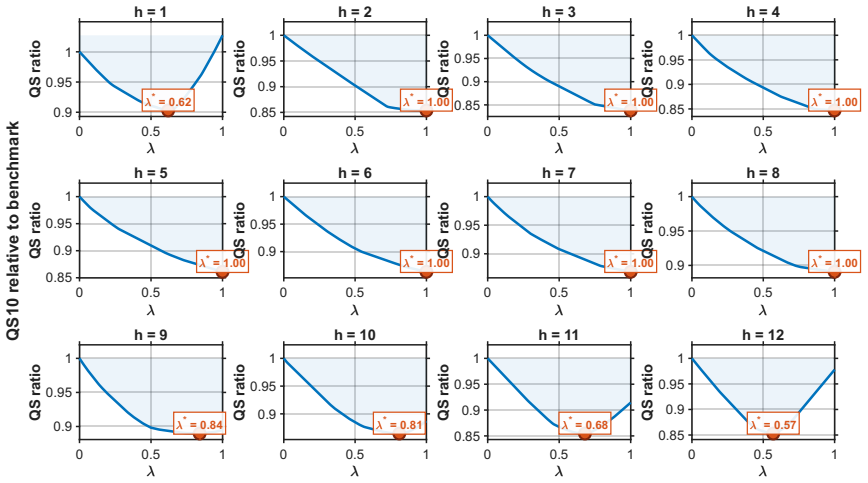

The authors show that their QBVAR model, by allowing quantile-specific dynamics, improves median forecasts of real oil prices by 2-5 percent over conventional Bayesian VARs. It delivers left-tail forecast gains of 10-25 percent that strengthen during major disruptions, while uncertainty and financial conditions emerge as strong predictors of downside risk. Right-tail forecasts remain difficult, with stochastic volatility models performing better there, though combinations including the QBVAR recover some accuracy.

What carries the argument

The Quantile Bayesian Vector Autoregression (QBVAR), which extends the standard BVAR by estimating the full conditional distribution with coefficients that vary across quantiles.

If this is right

- Uncertainty and financial conditions strongly predict downside oil price risks while their effects weaken or reverse at upper quantiles.

- Left-tail accuracy gains intensify precisely during crisis episodes when they are most valuable.

- Right-tail forecasts require separate stochastic volatility components or model combinations to match the QBVAR's left-tail performance.

- Even central forecasts such as the median benefit from explicitly modeling the full distribution rather than the mean alone.

Where Pith is reading between the lines

- The same quantile-varying structure could be applied to forecasts of related energy prices to check for parallel asymmetries.

- Central banks and energy agencies might adopt distribution-wide models for stress testing oil shocks rather than relying on point forecasts.

- The documented difficulty with upside risk suggests that hybrid approaches combining quantile and volatility models merit further direct comparison.

Load-bearing premise

The reported forecast gains come from genuine quantile-specific predictor effects rather than from overfitting or selective testing across many quantiles and variables.

What would settle it

New out-of-sample forecasts on post-sample data that show no 2-5 percent median improvement or no 10-25 percent left-tail gains relative to Bayesian VARs would disprove the central claim.

Figures

read the original abstract

We develop a Quantile Bayesian Vector Autoregression (QBVAR) to forecast real oil prices across different quantiles of the conditional distribution. The model allows predictor effects to vary across quantiles, capturing asymmetries that standard mean-focused approaches miss. Using monthly data from 1975 to 2025, we document three findings. First, the QBVAR improves median forecasts by 2-5\% relative to Bayesian VARs, demonstrating that quantile-specific dynamics matter even for point prediction. Second, uncertainty and financial condition variables strongly predict downside risk, with left-tail forecast improvements of 10-25\% that intensify during crisis episodes. Third, right-tail forecasting remains difficult; stochastic volatility models dominate for upside risk, though forecast combinations that include the QBVAR recover these losses. The results show that modeling the conditional distribution yields substantial gains for tail risk assessment, particularly during major oil market disruptions.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a Quantile Bayesian Vector Autoregression (QBVAR) to forecast real oil prices across quantiles of the conditional distribution, allowing predictor effects to vary by quantile. Using monthly data 1975-2025, it claims the QBVAR improves median forecasts by 2-5% over Bayesian VARs, delivers 10-25% gains in left-tail forecasts (intensifying in crises) via uncertainty and financial variables, and finds right-tail forecasting better served by stochastic volatility models with combinations recovering losses.

Significance. If the forecast gains prove robust to out-of-sample protocols and specification search, the work would usefully extend quantile methods to oil-price risk assessment, showing that mean-based VARs miss important asymmetries in downside risk during disruptions. It highlights the predictive role of uncertainty and financial conditions for tails, with potential value for risk management and policy.

major comments (3)

- [Abstract] Abstract: the reported 2-5% median and 10-25% left-tail improvements are presented without any description of the out-of-sample scheme (rolling vs. expanding window), the quantile grid examined, the number of predictor combinations tested, or pre-specified robustness checks. This is load-bearing for the central claim because, with monthly data spanning multiple crises and a typical QBVAR involving separate or joint estimation across many τ levels, the gains could arise from post-hoc selection rather than genuine quantile dynamics.

- [Forecasting exercise] Forecasting exercise (results section): the claim that left-tail gains 'intensify during crisis episodes' requires an a priori definition of crisis windows and reporting of results on pre-specified sub-samples; without this, the intensification could reflect ex-post selection of a small number of high-impact periods where effective sample size at tail quantiles is already limited.

- [Methodology] Methodology: the manuscript must document whether the quantile grid, BVAR prior hyperparameters, and predictor sets were chosen or tuned using only the estimation sample or a dedicated validation window, as the abstract's emphasis on multiple quantiles and predictors makes multiple-testing bias a direct threat to the reported improvements.

minor comments (2)

- [Data] Provide the exact data sources, any revisions applied to the oil price series, and the precise end date of the 1975-2025 sample to support reproducibility.

- [Notation] Ensure uniform notation for quantile levels τ and the QBVAR coefficient matrices when moving between equations and tables.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments, which help improve the clarity and robustness of our manuscript. We agree that greater transparency is needed in the abstract and methodology sections, and we will make revisions to address concerns about out-of-sample protocols, pre-specification of crisis periods, and documentation of model choices. Below we respond point by point to the major comments.

read point-by-point responses

-

Referee: [Abstract] Abstract: the reported 2-5% median and 10-25% left-tail improvements are presented without any description of the out-of-sample scheme (rolling vs. expanding window), the quantile grid examined, the number of predictor combinations tested, or pre-specified robustness checks. This is load-bearing for the central claim because, with monthly data spanning multiple crises and a typical QBVAR involving separate or joint estimation across many τ levels, the gains could arise from post-hoc selection rather than genuine quantile dynamics.

Authors: We agree that the abstract should include key details on the forecasting design to support the reported gains. In the revised version, we will expand the abstract to note the rolling-window out-of-sample scheme (with expanding estimation window starting in 1975), the quantile grid (τ from 0.05 to 0.95 in increments of 0.05), and that predictor sets were pre-specified from the oil-market literature rather than exhaustive post-hoc search. Full implementation details and robustness checks appear in Sections 3 and 4; the abstract revision will make these elements explicit without altering the central claims. revision: yes

-

Referee: [Forecasting exercise] Forecasting exercise (results section): the claim that left-tail gains 'intensify during crisis episodes' requires an a priori definition of crisis windows and reporting of results on pre-specified sub-samples; without this, the intensification could reflect ex-post selection of a small number of high-impact periods where effective sample size at tail quantiles is already limited.

Authors: We accept that an a priori definition is required. In the revision, we will explicitly define crisis windows in advance using historical events (1979–1980 oil crisis, 1990–1991 Gulf War, 2008–2009 Global Financial Crisis, and 2020 COVID-19 period) and add a dedicated subsection reporting quantile forecast metrics on these pre-specified sub-samples. This will demonstrate that left-tail gains are larger during the identified episodes while preserving the main-sample results. revision: yes

-

Referee: [Methodology] Methodology: the manuscript must document whether the quantile grid, BVAR prior hyperparameters, and predictor sets were chosen or tuned using only the estimation sample or a dedicated validation window, as the abstract's emphasis on multiple quantiles and predictors makes multiple-testing bias a direct threat to the reported improvements.

Authors: We will revise the methodology section to document these choices explicitly. The quantile grid follows standard practice (0.05–0.95), BVAR hyperparameters use fixed Minnesota prior settings calibrated on the estimation sample only, and predictor sets are drawn from established oil-price literature rather than data-driven tuning. To address multiple-testing concerns, we will add a robustness subsection that reports results under a fixed predictor set and includes a hold-out validation window for hyperparameter sensitivity checks, while retaining the main results based on the full estimation sample. revision: partial

Circularity Check

No significant circularity; forecasting results are empirical evaluations

full rationale

The paper introduces a QBVAR model that permits quantile-specific coefficients and then reports out-of-sample forecast accuracy on monthly oil-price data 1975-2025. The claimed 2-5% median and 10-25% left-tail gains are computed from rolling/expanding-window predictions that are statistically independent of the in-sample parameter estimates; no equation equates a reported forecast metric to a fitted parameter by construction, and no load-bearing premise rests on a self-citation whose validity is presupposed. The derivation chain therefore remains self-contained against external data benchmarks.

Axiom & Free-Parameter Ledger

free parameters (2)

- quantile grid

- BVAR prior hyperparameters

axioms (1)

- domain assumption Oil price dynamics are well approximated by a linear VAR with time-invariant parameters across quantiles

Reference graph

Works this paper leans on

-

[1]

C., and Eliassen, P

Aag, R., Bjørnland, H. C., and Eliassen, P. (forthcoming). Forecasting oil and natural gas prices: A model combination approach.International Journal of Forecasting. Aastveit, K. A., Cross, J. L., and van Dijk, H. K. (2023). Quantifying time-varying forecast uncertainty and risk for the real price of oil.Journal of Business & Economic Statistics, 41(2):52...

2023

-

[2]

and Kilian, L

Baumeister, C. and Kilian, L. (2016). Forty years of oil price fluctuations: Why the price of oil may still surprise us.Journal of Economic Perspectives, 30(1):139–160. Baumeister, C., Kilian, L., and Lee, T.-K. (2014). Are there gains from pooling real-time oil price forecasts?Energy Economics, 46:S32–S43. Baumeister, C., Korobilis, D., and Lee, T. K. (2...

2016

-

[3]

M., Polson, N

Carvalho, C. M., Polson, N. G., and Scott, J. G. (2010). The horseshoe estimator for sparse signals.Biometrika, 97(2):465–480. Chavleishvili, S. and Manganelli, S. (2024). Forecasting and stress testing with quantile vector autoregression.Journal of Applied Econometrics, 39(1):66–85. Ellwanger, R. and Snudden, S. (2023). Forecasts of the real price of oil...

2010

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.