Recognition: unknown

The Revenue Effect of Demand Misspecification in Event Ticket Pricing

Pith reviewed 2026-05-10 11:48 UTC · model grok-4.3

The pith

Misspecifying the timing of event-ticket demand produces average revenue losses of 0.42 percent, with omissions of late demand costing the most.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

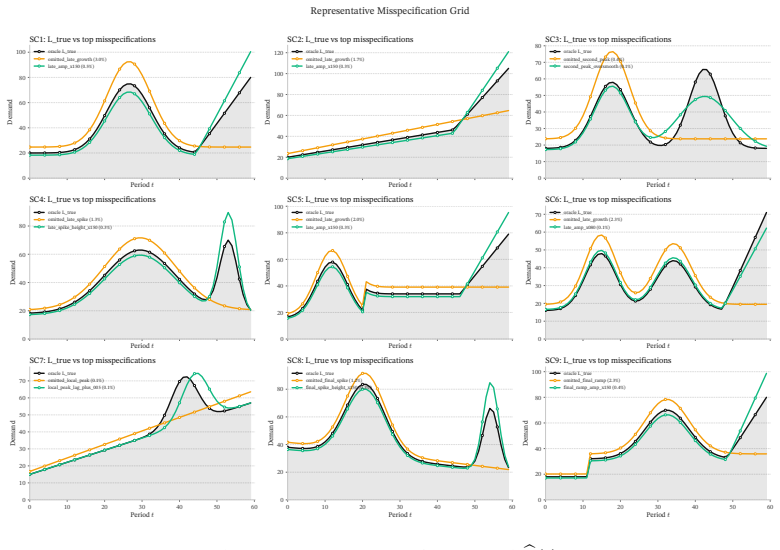

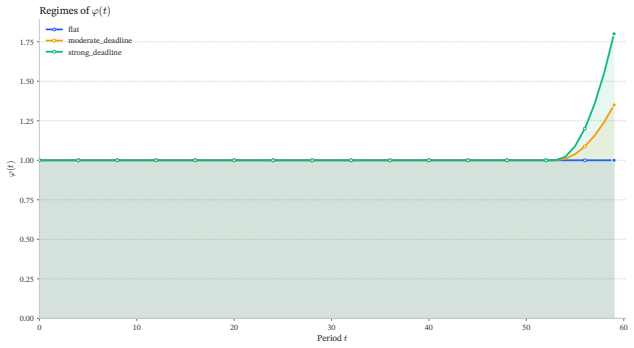

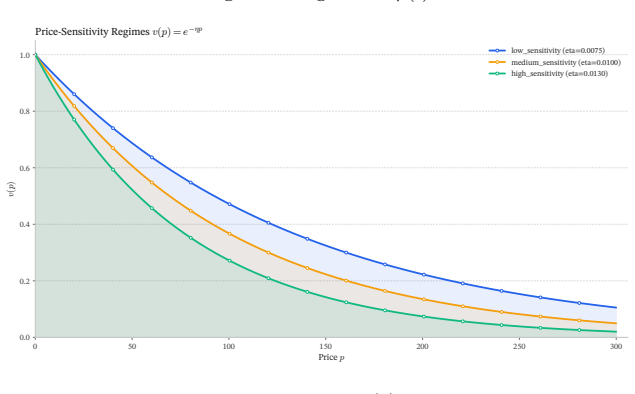

Within the model driven by total demand L(t), price response v(p) = e^{-ηp}, and time-dependent willingness-to-pay factor φ(t), a benchmark dynamic-programming policy evaluated across nine deterministic true-demand scenarios and a collection of feature-aware misspecifications of L(t) yields an aggregate relative revenue loss of 0.42 percent from misspecification, with the upper decile above 1 percent and the most expensive errors being omissions of late-demand components. The average effect remains modest yet non-negligible and intensifies under tight inventory and pronounced deadline effects.

What carries the argument

The dynamic-programming pricing policy evaluated by stochastic simulation under the demand intensity driven by L(t), v(p), and φ(t), using a ratio-of-means relative-loss metric across feature-aware misspecifications of the temporal demand profile.

If this is right

- Accurate recovery of the full temporal shape of L(t) improves revenue in limited-inventory dynamic pricing.

- Errors that drop late-arriving demand produce larger revenue shortfalls than other misspecifications.

- The revenue penalty from misspecification rises when inventory is tight and when willingness-to-pay increases sharply near the deadline.

- The average loss across misspecifications is small but measurable and accumulates across many events.

- Pricing decisions remain sensitive to the timing profile even when total demand volume is known.

Where Pith is reading between the lines

- Ticketing platforms could gain measurable revenue by investing in data sources that capture demand closer to the event date.

- Similar timing-misspecification costs are likely to appear in other perishable-inventory settings such as airline seats or hotel rooms.

- Forecasting methods that explicitly model the approach of the deadline may outperform those that treat demand as stationary.

- The results suggest testing whether real-time updates to the estimated L(t) as the event nears can offset part of the observed loss.

Load-bearing premise

The nine deterministic true-demand scenarios and the chosen collection of feature-aware misspecifications of L(t) sufficiently represent the demand-estimation errors that occur in practice.

What would settle it

In actual event-ticket sales data, the revenue gap between a policy using an accurate L(t) versus one using a misspecified L(t) (especially one omitting late demand) equals or exceeds the 0.42 percent average loss found in the simulations.

Figures

read the original abstract

We study a finite-horizon dynamic pricing problem for event tickets with limited inventory and time-varying demand. The central practical difficulty is that the total demand function $L(t)$ is not observed directly and must be estimated from data, while pricing decisions are sensitive to its temporal shape. The paper examines how the accuracy of this estimate affects revenue. We consider a model in which sales intensity is driven by the total demand $L(t)$, a price-response function $v(p)$, and a time-dependent willingness-to-pay factor $\varphi(t)$. The factor $\varphi(t)$ plays a central role: it captures the increase in customers' willingness to pay as the event date approaches and makes the temporal profile of demand economically important for pricing. Within this framework, the updated numerical study evaluates a benchmark dynamic-programming policy across nine deterministic true-demand scenarios, a collection of feature-aware misspecifications of $L(t)$, and multiple environment regimes induced by $v(p)=e^{-\eta p}$, the deadline factor $\varphi(t)$, and inventory level $Q$. The reported summaries are based on stochastic simulation and a ratio-of-means relative-loss metric. The results show that a more accurate representation of the temporal demand profile leads to more effective pricing decisions and higher revenue. Over the full misspecification collection the aggregate relative revenue loss is $0.42\%$, the upper decile exceeds $1\%$, and the most expensive errors are omissions of late-demand components. The average effect is therefore modest but non-negligible, and it becomes stronger when deadline effects are pronounced and inventory is tight.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript examines the revenue impact of misspecifying the temporal demand profile L(t) in a finite-horizon dynamic pricing problem for event tickets with limited inventory. Sales intensity depends on L(t), the price response v(p)=e^{-ηp}, and the deadline factor φ(t). A dynamic-programming policy is evaluated via stochastic simulation across nine deterministic true-demand scenarios and a collection of feature-aware misspecifications of L(t), under varying regimes of η, φ(t), and inventory Q. The central quantitative result is an aggregate relative revenue loss of 0.42% over the full misspecification collection, with the upper decile exceeding 1% and the largest losses arising from omissions of late-demand components.

Significance. If the reported magnitudes hold under broader conditions, the work supplies concrete, simulation-based evidence that accurate representation of temporal demand shape matters for revenue, with modest average effects but non-negligible tail risks when deadline effects are strong and inventory is tight. The use of a ratio-of-means relative-loss metric and multi-scenario forward simulation is a strength, providing a transparent way to quantify the cost of estimation errors without relying on fitted parameters or self-referential derivations.

major comments (3)

- [Numerical study] Numerical study section: the central claim that temporal misspecification produces only modest average revenue losses (0.42% aggregate) rests on nine fixed deterministic L(t) profiles and a discrete collection of feature-aware omissions. These choices are not shown to be representative of estimation errors arising from finite, noisy sales data, which typically induce continuous, correlated perturbations rather than isolated component omissions; without additional justification or sensitivity checks, the reported loss figures cannot be taken as general evidence for the broader conclusion.

- [Abstract and numerical results] Abstract and numerical results: the quantitative summaries (0.42% aggregate loss, upper decile >1%) are obtained from stochastic simulation, yet no information is provided on the number of runs, variance estimates, or standard errors of the relative-loss metric. This omission makes it impossible to assess whether the reported point estimates are statistically distinguishable from zero or sensitive to simulation noise.

- [Model formulation] Model formulation: the analysis assumes deterministic L(t) together with the specific functional forms v(p)=e^{-ηp} and φ(t). The paper does not examine how the revenue-loss magnitudes change under alternative price-response or willingness-to-pay specifications or under stochastic arrival processes; because the central claim concerns the practical cost of misspecification, this gap limits the robustness of the conclusion that the effect is “modest but non-negligible.”

minor comments (2)

- [Abstract] The abstract refers to an “updated numerical study” without indicating what prior version or results were revised.

- [Methods] Clarify the precise definition and normalization of the ratio-of-means relative-loss metric used to aggregate results across scenarios.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive suggestions. We address each major comment below and will incorporate revisions to improve the transparency and scope of the analysis.

read point-by-point responses

-

Referee: [Numerical study] Numerical study section: the central claim that temporal misspecification produces only modest average revenue losses (0.42% aggregate) rests on nine fixed deterministic L(t) profiles and a discrete collection of feature-aware omissions. These choices are not shown to be representative of estimation errors arising from finite, noisy sales data, which typically induce continuous, correlated perturbations rather than isolated component omissions; without additional justification or sensitivity checks, the reported loss figures cannot be taken as general evidence for the broader conclusion.

Authors: We agree that the chosen profiles and omissions do not directly replicate statistical estimation errors from finite noisy data. The design isolates the revenue consequences of specific, interpretable temporal-shape errors that arise in practice when forecasters omit late-demand features. In the revision we will add explicit justification for this choice, relate the scenarios to common estimation pitfalls, and include a supplementary sensitivity check with continuous, correlated perturbations drawn from a simple noise model. revision: partial

-

Referee: [Abstract and numerical results] Abstract and numerical results: the quantitative summaries (0.42% aggregate loss, upper decile >1%) are obtained from stochastic simulation, yet no information is provided on the number of runs, variance estimates, or standard errors of the relative-loss metric. This omission makes it impossible to assess whether the reported point estimates are statistically distinguishable from zero or sensitive to simulation noise.

Authors: The referee is correct; the simulation protocol details were inadvertently omitted. The revised manuscript will report the number of independent replications per scenario, the variance of the ratio-of-means estimator, and bootstrap standard errors so that readers can judge precision and statistical significance of the 0.42% aggregate figure. revision: yes

-

Referee: [Model formulation] Model formulation: the analysis assumes deterministic L(t) together with the specific functional forms v(p)=e^{-ηp} and φ(t). The paper does not examine how the revenue-loss magnitudes change under alternative price-response or willingness-to-pay specifications or under stochastic arrival processes; because the central claim concerns the practical cost of misspecification, this gap limits the robustness of the conclusion that the effect is “modest but non-negligible.”

Authors: We accept that the current results are tied to the deterministic setting and the chosen functional forms. The paper deliberately restricts attention to this environment to obtain clean, interpretable comparisons of temporal misspecification. In the revision we will expand the limitations section, discuss how the qualitative finding (larger losses when late demand is omitted and inventory is tight) is likely to persist under modest relaxations, and outline a clear agenda for future robustness checks with stochastic arrivals and alternative demand specifications. revision: partial

Circularity Check

No circularity: forward simulation on fixed scenarios

full rationale

The paper's central results (0.42% aggregate relative revenue loss, upper-decile effects, and identification of late-demand omissions as costly) are generated by evaluating a dynamic-programming policy on nine pre-specified deterministic L(t) profiles under a collection of feature-aware misspecifications, using explicit functional forms v(p)=e^{-ηp} and φ(t). These comparisons are independent forward simulations whose outputs are not algebraically or statistically forced to equal the chosen inputs; the scenarios and misspecification forms serve as exogenous test cases rather than being fitted or derived from the revenue metric itself. No self-citation chain, self-definitional loop, or renaming of a fitted quantity as a prediction appears in the reported derivation.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Bitran, Ren´ e Caldentey, and Susana V

[BCM98] Gabriel R. Bitran, Ren´ e Caldentey, and Susana V. Mondschein. Coordinat- ing clearance markdown sales of seasonal products in retail chains.Operations Research, 46(5):609–624, 1998. [BM97] GabrielR.BitranandSusanaV.Mondschein. Periodicpricingofseasonalproducts in retailing. Management Science, 43(1):64–79, 1997. [BM12] Omar Besbes and Costis Magl...

1998

-

[2]

[SD14] StephenL.ShapiroandJorisDrayer

Stanford, CA, 2 edition, 2021. [SD14] StephenL.ShapiroandJorisDrayer. Anexaminationofdynamicticketpricingand secondary market price determinants in major league baseball.Sport Management Review, 17(2):145–159, 2014. [SDD16] Stephen L. Shapiro, Joris Drayer, and Brendan Dwyer. Examining consumer per- ceptions of demand-based ticket pricing in sport. Sport ...

2021

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.