Recognition: unknown

Generalized Autoregressive Multivariate Models: From Binary to Poisson

Pith reviewed 2026-05-10 11:28 UTC · model grok-4.3

The pith

Aggregates of binary autoregressive time series converge to Poisson autoregressions under rare-events scaling

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under a rare-events scaling, aggregates of binary autoregressive processes converge to a Poisson autoregressive process. This provides a micro-foundation for the Poisson autoregression model from a primitive binary autoregressive setup, with the dynamics of the success probabilities carrying over to the intensity of the Poisson process.

What carries the argument

The rare-events scaling that makes individual binary events infrequent enough for their sum to follow a Poisson limit with autoregressive dependence.

If this is right

- Stationarity holds for the binary models via the coupling argument adapted to discontinuities.

- Multivariate extensions allow for network interactions and cross-sectional dependence.

- Maximum likelihood estimation can be applied to fit these models to data.

- The convergence result justifies using Poisson autoregressions for aggregated binary outcomes in rare-event settings.

Where Pith is reading between the lines

- The result implies that Poisson count models may be preferred when data consists of aggregated binary events under low probability regimes.

- Applications could extend to modeling rare financial events such as defaults or large trades as limits of binary indicators.

- Similar scaling arguments might connect other binary or discrete processes to continuous or count limits in time series.

Load-bearing premise

The probability dynamics must be such that the rare-events scaling produces the Poisson limit and the coupling argument succeeds in proving stationarity for the binary case.

What would settle it

Generate many independent copies of the binary autoregressive process with success probability scaled inversely with the number of copies and check whether their sum follows the distribution of the corresponding Poisson autoregressive process; a systematic mismatch would falsify the convergence claim.

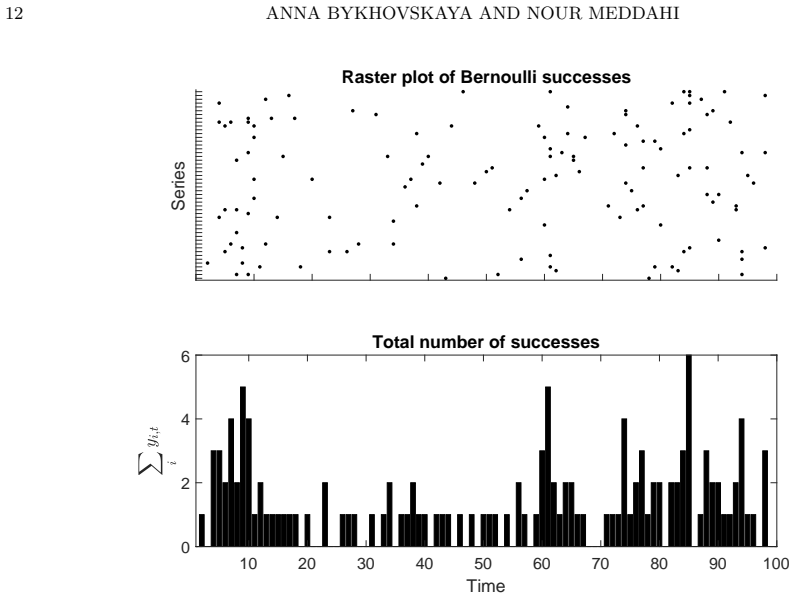

Figures

read the original abstract

This paper presents a framework for binary autoregressive time series in which each observation is a Bernoulli variable whose success probability evolves with past outcomes and probabilities, in the spirit of GARCH-type dynamics, accommodating nonlinearities, network interactions, and cross-sectional dependence in the multivariate case. Existence and uniqueness of a stationary solution is established via a coupling argument tailored to the discontinuities inherent in binary data. A key theoretical result, further supported by our empirical illustration on S&P 100 data, shows that, under a rare-events scaling, aggregates of such binary processes converge to a Poisson autoregression, providing a micro-foundation for this widely used count model. Maximum likelihood estimation is proposed and illustrated empirically.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a class of generalized autoregressive models for binary (Bernoulli) time series in which the success probability follows a GARCH-style recursion that can incorporate nonlinearities, network effects, and cross-sectional dependence. It proves existence and uniqueness of a stationary solution using a coupling argument adapted to the discontinuous nature of binary observations. The central theoretical claim is that, under a rare-events scaling (individual probabilities of order 1/N), the aggregate of these binary processes converges in law to a Poisson autoregressive process, thereby supplying a micro-foundation for the Poisson AR model. Maximum-likelihood estimation is proposed and illustrated on S&P 100 data.

Significance. If the convergence result is rigorously established, the paper would provide a valuable theoretical bridge between binary autoregressive specifications and the widely used Poisson autoregressive count models, particularly for rare-event data. The coupling-based stationarity proof is a technical strength for handling the binary discontinuities that standard contraction arguments cannot address directly. The empirical illustration offers a concrete check on practical applicability.

major comments (2)

- [§4] §4 (or the section containing the limit theorem): the rare-events scaling is stated as individual success probabilities of order 1/N, but the manuscript does not explicitly derive how the GARCH-type recursion for the binary success probability p_t maps onto the precise functional form of the Poisson intensity recursion λ_t = f(λ_{t-1}, y_{t-1}). Without this step-by-step expansion or application of the continuous-mapping theorem to the scaled aggregate, the claimed micro-foundation remains incomplete.

- [Theorem 3.2] Theorem 3.2 (stationarity via coupling): while the coupling argument is tailored to discontinuities, the proof sketch does not clarify whether the same contraction rate continues to hold uniformly under the rare-events scaling that is later imposed for the Poisson limit; any dependence of the contraction modulus on N would undermine the joint validity of stationarity and the limiting Poisson AR.

minor comments (2)

- [Abstract] The abstract and introduction refer to “aggregates of such binary processes” without defining the precise aggregation operator (sum, average, or intensity scaling) before the limit is taken; this notation should be fixed at first use.

- [Empirical illustration] The empirical section would benefit from reporting the estimated scaling parameter N and the implied average event probability to allow readers to judge whether the rare-events regime is plausible for the S&P 100 application.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed report. The comments highlight areas where the exposition of the limit theorem and the uniformity of the stationarity result can be strengthened. We address each major comment below and will revise the manuscript to incorporate the suggested clarifications.

read point-by-point responses

-

Referee: [§4] §4 (or the section containing the limit theorem): the rare-events scaling is stated as individual success probabilities of order 1/N, but the manuscript does not explicitly derive how the GARCH-type recursion for the binary success probability p_t maps onto the precise functional form of the Poisson intensity recursion λ_t = f(λ_{t-1}, y_{t-1}). Without this step-by-step expansion or application of the continuous-mapping theorem to the scaled aggregate, the claimed micro-foundation remains incomplete.

Authors: We agree that the mapping requires a more explicit derivation. The current manuscript states the rare-events scaling and asserts convergence of the aggregate to the Poisson AR process, but the step-by-step application of the continuous mapping theorem to the scaled sum of the binary processes (with the GARCH-style recursion for p_t) is only sketched. In the revision we will expand Section 4 to include the full expansion: first rescale the individual Bernoulli processes by N, apply the functional continuous mapping theorem to the recursion under the 1/N scaling, and verify that the limiting intensity satisfies λ_t = f(λ_{t-1}, y_{t-1}) with the same functional form as the binary recursion. This will make the micro-foundation rigorous and complete. revision: yes

-

Referee: [Theorem 3.2] Theorem 3.2 (stationarity via coupling): while the coupling argument is tailored to discontinuities, the proof sketch does not clarify whether the same contraction rate continues to hold uniformly under the rare-events scaling that is later imposed for the Poisson limit; any dependence of the contraction modulus on N would undermine the joint validity of stationarity and the limiting Poisson AR.

Authors: The coupling construction in Theorem 3.2 relies on the Lipschitz constant of the link function and the autoregressive coefficients, both of which are fixed and independent of the cross-sectional dimension N. The rare-events scaling affects only the level at which the success probabilities operate (order 1/N) but does not enter the contraction modulus of the recursion map. Consequently the same uniform contraction rate applies for all N large enough. We will insert a short remark immediately after the statement of Theorem 3.2 (and in the proof appendix) explicitly noting that the contraction modulus is uniform in N under the maintained assumptions, thereby confirming that stationarity holds jointly with the subsequent Poisson limit. revision: yes

Circularity Check

No circularity: Poisson limit derived as mathematical convergence from binary primitives under explicit scaling

full rationale

The paper establishes existence/uniqueness of stationary binary processes via a coupling argument that handles discontinuities, then proves convergence in law of scaled aggregates to a Poisson autoregressive process under a rare-events scaling (individual probabilities ~1/N). This is a limit theorem, not a self-definition or fitted parameter renamed as prediction. The Poisson recursion emerges from the scaled binary dynamics rather than being presupposed; the empirical S&P 100 illustration is separate and does not load-bear the theoretical claim. No self-citation chain, ansatz smuggling, or uniqueness imported from prior author work is required for the core derivation. The result is self-contained against external benchmarks (standard weak-convergence arguments for dependent processes).

Axiom & Free-Parameter Ledger

free parameters (1)

- coefficients in the success-probability recursion

axioms (1)

- standard math The binary process admits a unique stationary solution via a coupling argument tailored to discontinuities

Reference graph

Works this paper leans on

-

[1]

Count and duration time series with equal condi- tional stochastic and mean orders.Econometric Theory,37(2), 248–280

Aknouche, A.andFrancq, C.(2021). Count and duration time series with equal condi- tional stochastic and mean orders.Econometric Theory,37(2), 248–280

2021

-

[2]

J.andLucas, A.(2014)

Blasques, F.,Koopman, S. J.andLucas, A.(2014). Stationarity and ergodicity of univariate generalized autoregressive score processes.Electronic Journal of Statistics,8, 1088–1112. —,van Brummelen, J.,Koopman, S. J.andLucas, A.(2022). Maximum likelihood estimation for score-driven models.Journal of Econometrics,227(2), 325–346

2014

-

[3]

Generalized autoregressive conditional heteroskedasticity.Journal of econometrics,31(3), 307–327

Bollerslev, T.(1986). Generalized autoregressive conditional heteroskedasticity.Journal of econometrics,31(3), 307–327

1986

-

[4]

Time series approach to the evolution of networks: Prediction and estimation.Journal of Business & Economic Statistics,41(1), 170–183

Bykhovskaya, A.(2022). Time series approach to the evolution of networks: Prediction and estimation.Journal of Business & Economic Statistics,41(1), 170–183

2022

-

[5]

J.andLucas, A.(2013)

Creal, D.,Koopman, S. J.andLucas, A.(2013). Generalized autoregressive score models with applications.Journal of applied econometrics,28(5), 777–795. De Jong, R. M.andWoutersen, T.(2011). Dynamic time series binary choice.Econo- metric Theory,27(4), 673–702

2013

-

[6]

Frailty correlated default

Duffie, D.,Eckner, A.,Horel, G.andSaita, L.(2009). Frailty correlated default. The Journal of Finance,64(5), 2089–2123

2009

-

[7]

Integer-valued GARCH process

Ferland, R.,Latour, A.andOraichi, D.(2006). Integer-valued GARCH process. Journal of time series analysis,27(6), 923–942

2006

-

[8]

Binary time series models driven by a latent process.Econometrics and Statistics,2, 117–130

Fokianos, K.andMoysiadis, T.(2017). Binary time series models driven by a latent process.Econometrics and Statistics,2, 117–130. —,Rahbek, A.andTjøstheim, D.(2009). Poisson autoregression.Journal of the Amer- ican Statistical Association,104(488), 1430–1439

2017

-

[9]

John Wiley & Sons

Francq, C.andZakoian, J.-M.(2019).GARCH models: structure, statistical inference and financial applications. John Wiley & Sons

2019

-

[10]

S.(2016)

Graham, B. S.(2016). Homophily and transitivity in dynamic network formation.working paper

2016

-

[11]

Princeton University Press

Hayashi, F.(2000).Econometrics. Princeton University Press

2000

-

[12]

J.(1981)

Heckman, J. J.(1981). Heterogeneity and state dependence. InStudies in labor markets, University of Chicago Press, pp. 91–140

1981

-

[13]

Predicting US recessions with dynamic binary response models.The Review of Economics and Statistics,90(4), 777–791

Kauppi, H.andSaikkonen, P.(2008). Predicting US recessions with dynamic binary response models.The Review of Economics and Statistics,90(4), 777–791

2008

-

[14]

John Wiley & Sons

Kedem, B.andFokianos, K.(2005).Regression models for time series analysis. John Wiley & Sons. GENERALIZED AUTOREGRESSIVE MULTIV ARIATE MODELS: FROM BINARY TO POISSON 39

2005

-

[15]

Modeling and inference for multivariate time series of counts based on the INGARCH scheme.Computational Statistics & Data Analysis,177, 107579

Lee, S.,Kim, D.andKim, B.(2023). Modeling and inference for multivariate time series of counts based on the INGARCH scheme.Computational Statistics & Data Analysis,177, 107579

2023

-

[16]

P.andTweedie, R

Meyn, S. P.andTweedie, R. L.(2009).Markov chains and stochastic stability. Cam- bridge University Press

2009

-

[17]

On binary and categorical time series models with feedback.Journal of Multivariate Analysis,131, 209–228

Moysiadis, T.andFokianos, K.(2014). On binary and categorical time series models with feedback.Journal of Multivariate Analysis,131, 209–228

2014

-

[18]

Predicting bear and bull stock markets with dynamic binary time series models.Journal of Banking & Finance,37(9), 3351–3363

Nyberg, H.(2013). Predicting bear and bull stock markets with dynamic binary time series models.Journal of Banking & Finance,37(9), 3351–3363

2013

-

[19]

Optimal replacement of GMC bus engines: An empirical model of Harold Zurcher.Econometrica, pp

Rust, J.(1987). Optimal replacement of GMC bus engines: An empirical model of Harold Zurcher.Econometrica, pp. 999–1033

1987

-

[20]

H.andShephard, N.(2000)

Rydberg, T. H.andShephard, N.(2000). A modelling framework for the prices and times of trades made on the New York stock exchange. InNonlinear and Nonstationary Signal Processing, Cambridge University Press, pp. 217–246

2000

-

[21]

Streett, S.(2000).Some observation driven models for time series of counts. Ph.D. thesis, Ph. D. thesis, Colorado State University, Department of Statistics. (Anna Bykhovskaya)Duke University Email address:anna.bykhovskaya@duke.edu (Nour Meddahi)Toulouse School of Economics Email address:nour.meddahi@tse-fr.eu

2000

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.