Recognition: unknown

Antitrust on Aisle Five: How Well Do Divestiture Remedies Work?

Pith reviewed 2026-05-10 09:55 UTC · model grok-4.3

The pith

Divestiture remedies in grocery mergers cause 31 percent employment declines at affected stores over five years due to weaker assets and buyer selection.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

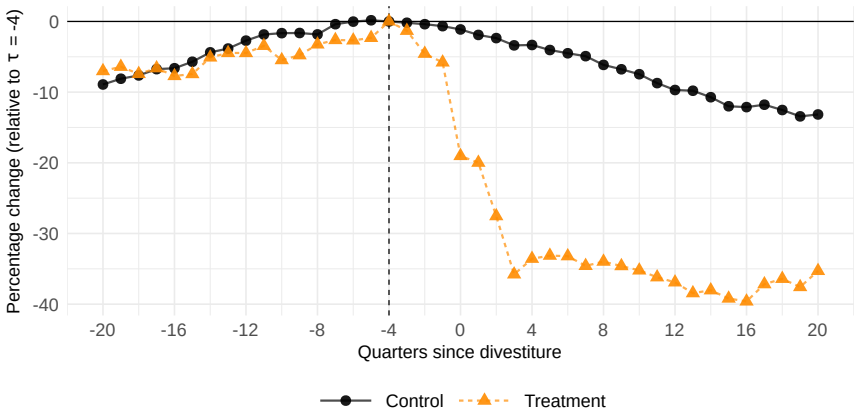

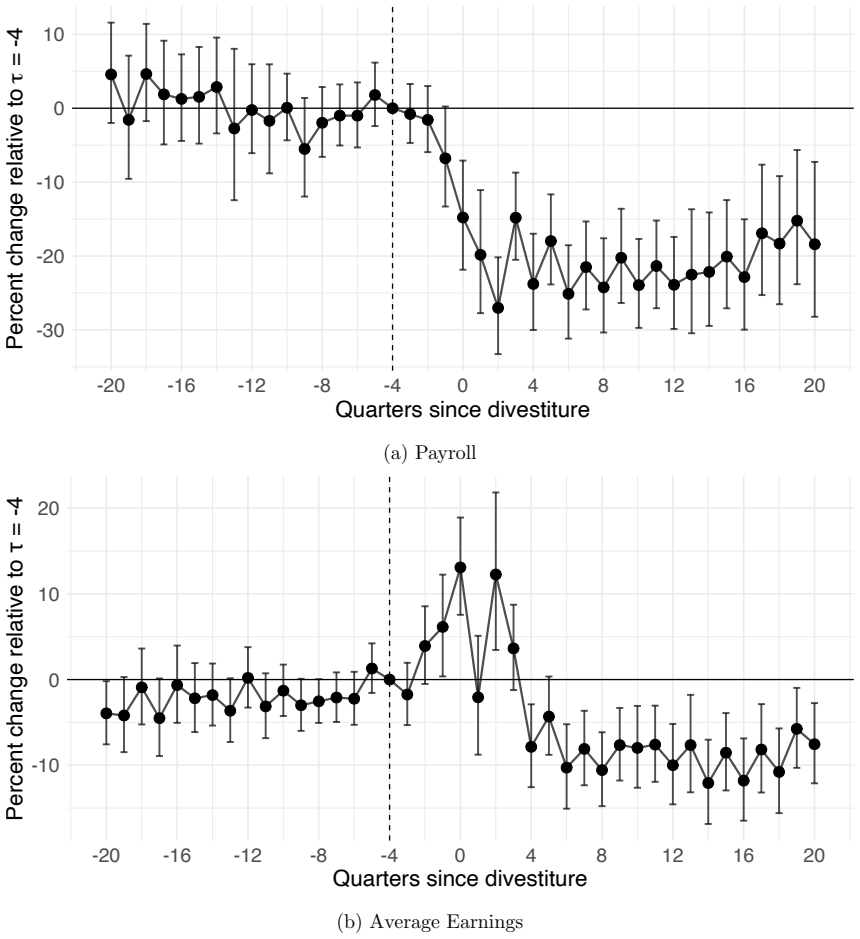

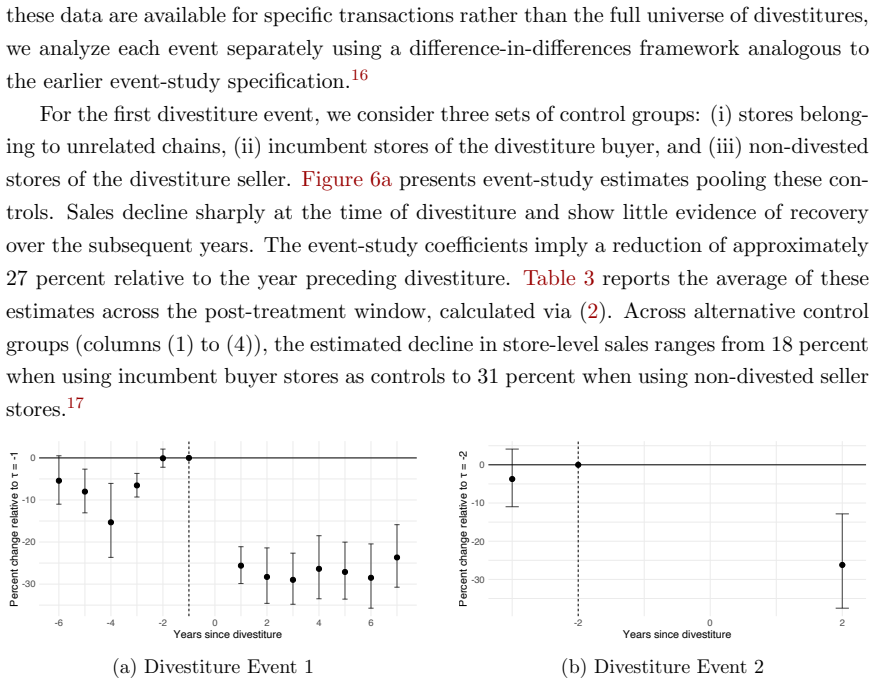

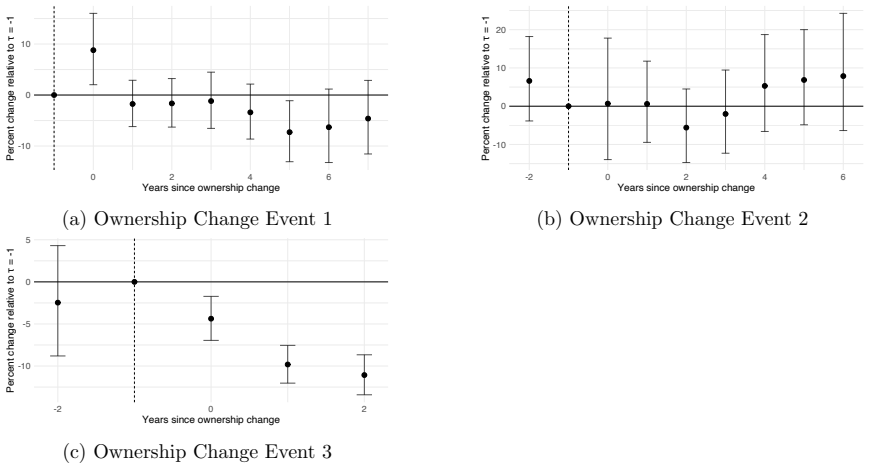

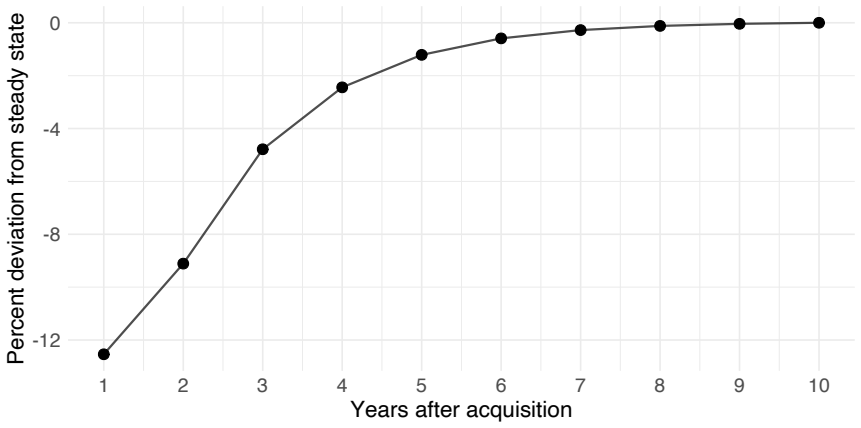

Using establishment-level data from the grocery sector, divested stores experience an average 31 percent decline in employment over five years, driven by elevated exit rates and persistent contraction among survivors. Sales decline as well. Transaction records show divested assets are systematically weaker and often go to lower-capability buyers, suggesting structural remedies are less effective when merging parties exercise substantial discretion in implementation.

What carries the argument

The divestiture process itself, specifically the discretion allowed to merging parties in selecting which assets to transfer and to which buyers.

If this is right

- Divested stores show higher rates of exit from the market.

- Surviving divested establishments experience ongoing contraction in employment.

- Sales at divested stores decline over the five-year period.

- Structural remedies may fail to restore competition effectively when parties control asset and buyer choices.

Where Pith is reading between the lines

- Regulators could improve outcomes by taking a more active role in screening buyers and assets rather than relying on party proposals.

- Similar employment and performance declines might occur in divestitures from mergers in other retail or service sectors if discretion remains high.

- This pattern raises the possibility that requiring stronger pre-approval standards for buyers could change the results.

- Studies tracking buyer performance after acquisition could test whether capability gaps explain the gaps in store outcomes.

Load-bearing premise

The observed declines in employment, exits, and sales at divested stores result from the divestiture process, asset selection, and buyer choice rather than from pre-existing differences in store quality or unrelated market conditions.

What would settle it

Finding no difference in employment or sales trends between divested stores and comparable non-divested stores in the same markets after accounting for initial characteristics would falsify the claim that the divestiture causes the declines.

Figures

read the original abstract

Antitrust authorities frequently rely on structural divestitures to address competitive concerns raised by mergers. Using census-level establishment data and proprietary transaction records from the U.S. grocery sector, we provide systematic evidence on the long-run effects of such remedies. Divested stores experience an average 31 percent decline in employment over five years, driven by elevated exit rates and persistent contraction among surviving establishments. Sales similarly decline. Transaction-level evidence indicates that divested assets are systematically weaker and are often transferred to lower-capability buyers. These findings suggest that structural remedies may be less effective when the implementation of divestitures allows merging parties substantial discretion over the assets and buyers involved.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper analyzes the long-run effects of structural divestiture remedies in U.S. grocery mergers using census-level establishment data and proprietary transaction records. It reports that divested stores experience an average 31% decline in employment over five years, driven by elevated exit rates and persistent contraction among survivors, with similar declines in sales. Divested assets are shown to be systematically weaker and transferred to lower-capability buyers, suggesting that remedies are less effective when merging parties exercise substantial discretion over asset selection and buyer choice.

Significance. If the causal claims are robust, the study supplies systematic, large-scale evidence on divestiture outcomes in a key retail sector, with the transaction-level buyer capability findings offering a concrete mechanism for why remedies may underperform. The scale of the census and transaction data is a clear strength, enabling falsifiable quantitative claims about employment, exits, and sales trajectories that could inform antitrust policy on remedy design.

major comments (3)

- [Empirical Strategy] Empirical Strategy section: The analysis notes that divested assets are systematically weaker but provides no details on identification (e.g., store fixed effects, propensity-score matching on pre-merger characteristics, or difference-in-differences with pre-trends) to separate the effect of divestiture implementation and buyer selection from selection bias or pre-existing store trajectories. This is load-bearing for the central claim that the 31% employment decline and higher exit rates are caused by the remedy process rather than the fact that weaker stores were chosen for divestiture.

- [Results] Results on employment and sales (around the 31% figure and exit-rate tables): The reported declines lack reported robustness checks such as placebo tests on non-divested stores, alternative control groups, or specifications that account for market-wide shocks over the five-year window, leaving open the possibility that unrelated dynamics drive the patterns.

- [Transaction Evidence] Transaction-level evidence on buyer capability: The finding that assets are transferred to lower-capability buyers is presented as supporting the discretion mechanism, but the manuscript does not show specific regressions or comparisons demonstrating that buyer capability causally explains the worse post-divestiture performance (as opposed to correlation with asset weakness).

minor comments (2)

- [Abstract] Abstract: Adding the number of divestitures or stores in the sample would help readers gauge the precision of the 31% employment decline estimate.

- [Figures] Figures showing employment and sales trends: Legends and axis labels should explicitly distinguish divested vs. non-divested stores and pre- vs. post-merger periods for clarity.

Simulated Author's Rebuttal

We thank the referee for their constructive and detailed comments, which have helped us clarify the identification strategy, strengthen robustness checks, and better articulate the limitations of the transaction-level evidence. We have revised the manuscript accordingly and respond to each major comment below.

read point-by-point responses

-

Referee: [Empirical Strategy] Empirical Strategy section: The analysis notes that divested assets are systematically weaker but provides no details on identification (e.g., store fixed effects, propensity-score matching on pre-merger characteristics, or difference-in-differences with pre-trends) to separate the effect of divestiture implementation and buyer selection from selection bias or pre-existing store trajectories. This is load-bearing for the central claim that the 31% employment decline and higher exit rates are caused by the remedy process rather than the fact that weaker stores were chosen for divestiture.

Authors: We agree that the original Empirical Strategy section lacked sufficient detail on identification. The revised manuscript now explicitly describes the use of establishment fixed effects to absorb time-invariant store heterogeneity, propensity-score matching on pre-merger employment, sales, age, and local market characteristics to construct comparable controls, and difference-in-differences specifications with explicit pre-trend tests. These additions clarify how we isolate the effects of divestiture and buyer selection from pre-existing trajectories and selection bias. revision: yes

-

Referee: [Results] Results on employment and sales (around the 31% figure and exit-rate tables): The reported declines lack reported robustness checks such as placebo tests on non-divested stores, alternative control groups, or specifications that account for market-wide shocks over the five-year window, leaving open the possibility that unrelated dynamics drive the patterns.

Authors: We have added multiple robustness checks to the Results section. These include placebo tests on non-divested stores in comparable markets, alternative control groups using unmatched and differently matched samples, and specifications that incorporate market-year fixed effects to absorb local economic shocks. The 31% employment decline, elevated exit rates, and sales patterns remain stable across these specifications. revision: yes

-

Referee: [Transaction Evidence] Transaction-level evidence on buyer capability: The finding that assets are transferred to lower-capability buyers is presented as supporting the discretion mechanism, but the manuscript does not show specific regressions or comparisons demonstrating that buyer capability causally explains the worse post-divestiture performance (as opposed to correlation with asset weakness).

Authors: We acknowledge that the original transaction evidence was primarily correlational. In the revision we have added regressions that control for pre-divestiture asset characteristics (employment, sales, and store age) and show that buyer capability retains an independent association with post-divestiture employment and exit outcomes. We also discuss the remaining limitations on causal identification given the absence of suitable instruments in the data. revision: partial

Circularity Check

No circularity: purely observational empirical analysis

full rationale

The paper is an observational study relying on external U.S. census establishment data and proprietary transaction records to document post-divestiture outcomes in grocery stores. No derivations, equations, fitted parameters presented as predictions, or self-citation chains appear in the abstract or described methodology. Claims about employment declines, exit rates, and buyer selection rest on direct data comparisons rather than any self-referential construction that reduces to inputs by definition. This is the standard non-circular finding for data-driven empirical work without theoretical modeling.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Verified Complaint: Albertsons Companies, Inc. v. The Kroger Company,

Albertsons Companies, Inc. (2024) “Verified Complaint: Albertsons Companies, Inc. v. The Kroger Company,” Court Filing, Court of Chancery of the State of Delaware,https: //fingfx.thomsonreuters.com/gfx/legaldocs/zjvqndzxmpx/frankel-albertsonsv kroger--albertsonscomplaint.pdf, Case No. 2024-1276-LWW, Filed: December 14,

2024

-

[2]

The effect of mergers on variety in grocery retailing,

Argentesi, Elena, Paolo Buccirossi, Roberto Cervone, Tomaso Duso, and Alessia Marrazzo (2021) “The effect of mergers on variety in grocery retailing,”International Journal of Industrial Organization, 79, 102789. Brown, David P, Andrew Eckert, and Blake Shaffer (2023) “Evaluating the impact of di- vestitures on competition: Evidence from Alberta’s wholesal...

-

[3]

Stacked difference-in- differences,

Wing, Coady, Seth M Freedman, and Alex Hollingsworth (2024) “Stacked difference-in- differences,”Technical report, National Bureau of Economic Research, 10.3386/w32054. Zhang, Zhou, Federico Ciliberto, and Jonathan Williams (2017) “Effects of mergers and divestitures on airline fares,”Transportation Research Record, 2603 (1), 98–104, https: //doi.org/10.3...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.