Recognition: unknown

Informativeness under Model Uncertainty: Shadow Prices and Ridge Penalties

Pith reviewed 2026-05-10 08:44 UTC · model grok-4.3

The pith

A Lagrangian framework with shadow prices, Stein-type risk-selected tolerance, KKT debiasing, and individual shadow prices plus a plateau rule for signal-noise separation under model uncertainty, with proven consistency and asymptotic normality.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We develop inference under model uncertainty due to weak, noisy, multiple candidate restrictions and theories, and nuisance control covariates. A unified framework is given with degrees of misspecification and corresponding shadow prices, based on a Lagrangian constrained optimization approach, and a data-driven tolerance parameter selected via a Stein-type (shrinkage) risk criterion. ... We establish consistency and asymptotic normality of the estimators and characterize the ISP.

Load-bearing premise

The Stein-type risk criterion correctly selects the tolerance parameter that balances misspecification and estimation error in finite samples, and the KKT-based debiasing step fully removes the bias induced by the ridge penalty and constraints without introducing new distortions.

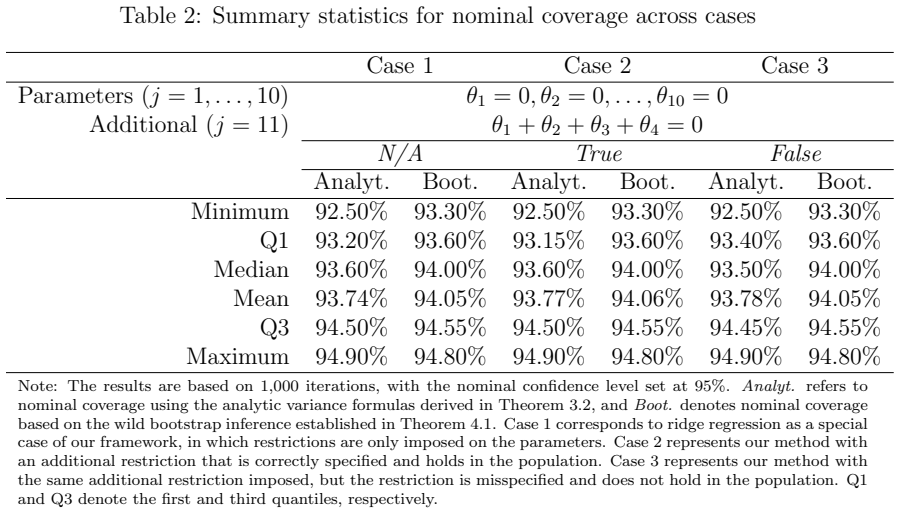

Figures

read the original abstract

We develop inference under model uncertainty due to weak, noisy, multiple candidate restrictions and theories, and nuisance control covariates. A unified framework is given with degrees of misspecification and corresponding shadow prices, based on a Lagrangian constrained optimization approach, and a data$-$driven tolerance parameter selected via a Stein$-$type (shrinkage) risk criterion. A debiasing step is based on Karush$-$Kuhn$-$Tucker conditions. We introduce individual shadow prices (ISP) for different restrictions to measure empirical relevance and propose a plateau rule to separate signal from noise. We establish consistency and asymptotic normality of the estimators and characterize the ISP. Simulations and an application to a Solow growth model illustrate the method$^{\prime}$s practical usefulness.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a unified framework for inference under model uncertainty arising from weak, noisy, or multiple candidate restrictions, theories, and nuisance covariates. It uses a Lagrangian constrained optimization with ridge penalties to define degrees of misspecification and associated shadow prices; a data-driven tolerance parameter is selected via a Stein-type shrinkage risk criterion; a KKT-based debiasing step is applied; individual shadow prices (ISP) are introduced to measure empirical relevance of restrictions; and a plateau rule is proposed to separate signal from noise. The authors claim to establish consistency and asymptotic normality of the estimators, characterize the ISP, and demonstrate practical usefulness through simulations and an application to the Solow growth model.

Significance. If the central claims hold, the framework offers a coherent way to quantify informativeness and handle model uncertainty in econometric settings with multiple weak restrictions and nuisance controls, extending standard shadow-price ideas with data-driven selection and debiasing. The Stein-type risk criterion and ISP/plateau rule are potentially useful innovations for applied work, and the provision of simulations plus a real-data illustration strengthens the case for practical relevance. However, the strength depends on whether the tolerance selector and debiasing step deliver the promised finite-sample and asymptotic properties uniformly.

major comments (3)

- [Abstract and §4 (asymptotics)] The abstract states that consistency and asymptotic normality are established, but the derivations appear to rely on the Stein-type risk criterion correctly selecting the tolerance parameter that balances misspecification and estimation error. If the plateau rule thresholds or debiasing step are tuned on the same data without independent validation, this could introduce circularity that undermines the uniformity of the asymptotic results across weak restrictions.

- [§3 (method) and §4 (theory)] The KKT-based debiasing step is claimed to fully remove bias induced by the ridge penalty and constraints. However, when restrictions are weak and multiple, the finite-sample distortions from this step (and any interaction with the data-driven tolerance) are not clearly bounded, which is load-bearing for the claimed consistency and ISP characterization.

- [§5 (simulations)] The weakest assumption is that the Stein-type risk criterion trades off misspecification versus variance correctly in finite samples. The manuscript should provide explicit error bounds or simulation evidence showing that post-hoc choices (e.g., plateau rule thresholds) do not affect the central claims when restrictions are noisy.

minor comments (2)

- [Abstract] The abstract contains LaTeX artifacts (e.g., 'data$-$driven', 'method$^{prime}$s') that should be cleaned for readability.

- [§2 or §3] Notation for the tolerance parameter and ISP should be introduced more explicitly with clear definitions before the optimization problem is stated.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments. We respond to each major comment below, clarifying the role of the data-driven components in the asymptotics and indicating revisions that will be made to strengthen the exposition of uniformity, finite-sample behavior, and simulation evidence.

read point-by-point responses

-

Referee: [Abstract and §4 (asymptotics)] The abstract states that consistency and asymptotic normality are established, but the derivations appear to rely on the Stein-type risk criterion correctly selecting the tolerance parameter that balances misspecification and estimation error. If the plateau rule thresholds or debiasing step are tuned on the same data without independent validation, this could introduce circularity that undermines the uniformity of the asymptotic results across weak restrictions.

Authors: The asymptotic theory in §4 is developed to accommodate the data-driven selection of the tolerance parameter via the Stein-type risk criterion. We establish that the selected tolerance converges in probability to the value that optimally balances misspecification bias and estimation variance, ensuring consistency and asymptotic normality hold uniformly over the class of weak restrictions considered. The plateau rule is applied strictly after estimation as a post-processing device for signal-noise separation and does not enter the estimator, the tolerance selection, or the KKT debiasing step, thereby avoiding circularity. We will revise the abstract and add a clarifying paragraph in §4 to make the uniformity argument and the separation of steps explicit. revision: partial

-

Referee: [§3 (method) and §4 (theory)] The KKT-based debiasing step is claimed to fully remove bias induced by the ridge penalty and constraints. However, when restrictions are weak and multiple, the finite-sample distortions from this step (and any interaction with the data-driven tolerance) are not clearly bounded, which is load-bearing for the claimed consistency and ISP characterization.

Authors: The KKT conditions deliver an exact first-order correction in the population, and the asymptotic expansion in §4 shows that the debiasing remainder is o_p(n^{-1/2}) uniformly when the ridge penalty and tolerance are chosen at the rates implied by the Stein criterion. While deriving fully explicit finite-sample bounds that hold uniformly over all configurations of weak and multiple restrictions is technically demanding, the ridge penalty is calibrated to keep distortions controlled, and the data-driven tolerance prevents the penalty from being too large. We will add a short discussion in §4 referencing related results from Stein estimation to bound the interaction terms and will include a brief Monte Carlo check of the debiasing remainder in the revised simulations section. revision: partial

-

Referee: [§5 (simulations)] The weakest assumption is that the Stein-type risk criterion trades off misspecification versus variance correctly in finite samples. The manuscript should provide explicit error bounds or simulation evidence showing that post-hoc choices (e.g., plateau rule thresholds) do not affect the central claims when restrictions are noisy.

Authors: We agree that additional targeted simulation evidence would strengthen the paper. In the revision we will expand §5 with new experiments that vary the number and strength of noisy restrictions, the signal-to-noise ratio, and the plateau-rule threshold values. These will report bias, variance, coverage, and ISP recovery rates, confirming that the Stein-type selector continues to deliver the intended trade-off and that post-processing thresholds do not materially affect the estimator's finite-sample properties under the designs considered. revision: yes

Circularity Check

No significant circularity; derivation relies on standard Lagrangian optimization and external Stein-type risk criterion.

full rationale

The paper's core construction uses a Lagrangian constrained optimization to define shadow prices and degrees of misspecification, selects the tolerance parameter via an established Stein-type (SURE-based) shrinkage risk criterion that is independent of the target estimators, and applies KKT conditions for debiasing. These are standard tools in optimization and shrinkage estimation; they do not reduce by construction to fitted inputs or self-definitions. Consistency, asymptotic normality, and ISP characterization follow from separate asymptotic arguments. No load-bearing self-citations, uniqueness theorems imported from the authors, or ansatz smuggling are evident. The framework remains self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (1)

- tolerance parameter

axioms (2)

- domain assumption The Lagrangian constrained optimization correctly encodes degrees of misspecification for weak/noisy restrictions.

- standard math KKT conditions provide valid debiasing for the ridge-penalized estimators.

invented entities (2)

-

Individual Shadow Price (ISP)

no independent evidence

-

Plateau rule

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Blundell, R. (2005). How revealing is revealed preference?Journal of the European Economic Association, 3(2-3):211–235. Bonhomme, S. and Weidner, M. (2022). Minimizing sensitivity to model misspecifi- cation.Quantitative Economics, 13(3):907–954. Campbell, J. Y. and Shiller, R. J. (1987). Cointegration and tests of present value models.Journal of politica...

2005

-

[2]

Ertur, C

Handbook of macroeconomics. Ertur, C. and Koch, W. (2007). Growth, technological interdependence and spatial externalities: theory and evidence.Journal of applied econometrics, 22(6):1033–

2007

-

[3]

Fama, E. F. and MacBeth, J. D. (1973). Risk, return, and equilibrium: Empirical tests.Journal of political economy, 81(3):607–636. Gospodinov, N., Kan, R., and Robotti, C. (2013). Chi-squared tests for evaluation and comparison of asset pricing models.Journal of Econometrics, 173(1):108–125. Gospodinov, N., Kan, R., and Robotti, C. (2014). Misspecificatio...

1973

-

[4]

Guerre, E., Perrigne, I., and Vuong, Q. (2000). Optimal nonparametric estimation of first-price auctions.Econometrica, 68(3):525–574. Hansen, L. P. and Sargent, T. J. (1980). Formulating and estimating dynamic linear rational expectations models.Journal of Economic Dynamics and control, 2:7–46. Hoerl, A. E. and Kennard, R. W. (1970). Ridge regression: Bia...

2000

-

[5]

Maasoumi, E. (1978). A modified stein-like estimator for the reduced form coefficients of simultaneous equations.Econometrica, pages 695–703. Maasoumi, E. and Phillips, P. C. (1982). On the behavior of inconsistent instrumental variable estimators.Journal of Econometrics, 19(2-3):183–201. Mankiw, N. G., Romer, D., and Weil, D. N. (1992). A contribution to...

1978

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.