Recognition: unknown

The realized copula of volatility

Pith reviewed 2026-05-10 07:35 UTC · model grok-4.3

The pith

The realized copula of volatility consistently estimates the dependence structure of latent stochastic volatilities from high-frequency returns.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

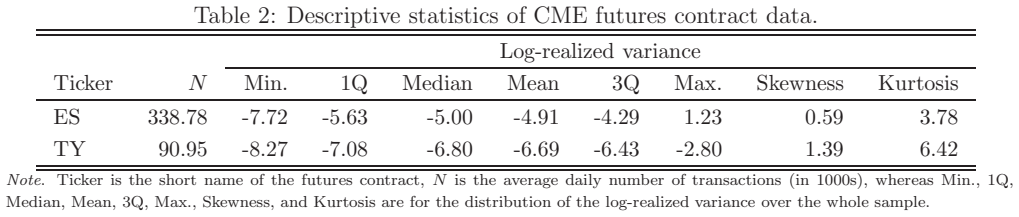

The realized copula of volatility is defined as the empirical copula computed from local volatility estimates obtained via high-frequency returns. This statistic converges in probability to the true copula of the latent volatility processes under in-fill asymptotics. When the observation period lengthens, the associated empirical process for the measurement error satisfies a functional central limit theorem. The framework further supplies a goodness-of-fit test for the time-invariant marginal copula of volatility.

What carries the argument

The realized copula of volatility, formed by applying the empirical copula function to locally estimated volatility measures constructed from high-frequency asset returns.

If this is right

- The estimator serves as a reliable proxy for both the empirical and marginal copulas of volatility even when only moderate amounts of high-frequency data are available over short samples.

- The associated goodness-of-fit test exhibits correct size and high power in finite-sample simulations.

- In U.S. equity and treasury bond futures markets the dependence structure between realized variances is captured almost exactly by a Gumbel copula.

- The asymptotic results cover both fixed-horizon and expanding-horizon settings.

Where Pith is reading between the lines

- The nonparametric nature of the estimator allows examination of volatility codependence across asset classes without committing to a specific parametric copula family in advance.

- The Gumbel shape implies stronger joint movements during high-volatility episodes than during low-volatility episodes, which could guide the design of tail-risk hedging strategies.

- Relaxing the time-invariant marginal copula assumption would permit study of how volatility dependence evolves over longer horizons.

- The framework could be applied to other continuous-time processes, such as interest rates or exchange rates, to map out cross-market volatility linkages.

Load-bearing premise

The latent volatility processes are continuous and high-frequency returns permit consistent estimation of local volatility.

What would settle it

A Monte Carlo experiment in which the true volatility process is discontinuous would show whether the realized copula estimator fails to converge to the known copula of the latent processes.

Figures

read the original abstract

We study a new measure of codependency in the second moment of a continuous-time multivariate asset price process, which we name the realized copula of volatility. The statistic is based on local volatility estimates constructed from high-frequency asset returns and affords a nonparametric estimator of the empirical copula of the latent stochastic volatility. We show consistency of our estimator with in-fill asymptotic theory, either with a fixed or increasing time span. In the latter setting, we derive a functional central limit theorem for the empirical process associated with the measurement error of the time-invariant marginal copula of volatility. We also develop a goodness-of-fit test to evaluate hypotheses about the shape of the latter. In a simulation study, we demonstrate that our estimator is a good proxy of both the empirical and marginal copula of volatility, even with a moderate amount of high-frequency data recorded over a relatively short sample. The goodness-of-fit test is found to exhibit size control and excellent power. We implement our framework on high-frequency transaction data from futures contracts that track the U.S. equity and treasury bond market. A Gumbel copula is found to offer a near-perfect bind between the realized variance processes in these data.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces the realized copula of volatility, a nonparametric estimator of the empirical copula of latent stochastic volatilities constructed from high-frequency local volatility estimates. It establishes consistency of the estimator under in-fill asymptotics (fixed or expanding time span), derives a functional central limit theorem for the associated empirical process, develops a goodness-of-fit test for the shape of the time-invariant marginal copula, validates performance via simulations, and applies the method to high-frequency futures data on U.S. equity and Treasury bonds, concluding that a Gumbel copula provides a near-perfect fit to the dependence between the realized variance processes.

Significance. If the continuity assumption holds, the framework supplies a new nonparametric tool for measuring volatility codependence with explicit asymptotic theory and a GoF test, supported by simulations that demonstrate reliable proxy performance even with moderate high-frequency samples. The empirical finding of strong upper-tail dependence via the Gumbel copula between equity and bond volatility processes would be of interest for multivariate volatility modeling and risk applications.

major comments (3)

- [§2, Theorem 1] §2 (model setup) and Theorem 1 (consistency): the estimator and its consistency rest on the maintained assumption that the latent price process is a continuous semimartingale, allowing consistent local-volatility recovery by in-fill asymptotics. The empirical application in §5 uses equity and bond futures transaction data, which standardly contain price jumps; the paper does not report jump-robustness checks or simulations with jumps, so the measurement-error propagation into the copula estimator and the Gumbel fit remain unexamined.

- [§5] §5 (empirical results): the headline claim that 'a Gumbel copula is found to offer a near-perfect bind' is obtained by feeding the local-volatility estimates directly into the empirical copula. Because the consistency and FCLT results are derived only under continuity, any jump-induced inconsistency in the local-vol estimates directly affects the reported copula shape and GoF statistic; no alternative jump-robust local-vol estimator or sensitivity analysis is provided.

- [Theorem 3] Theorem 3 (functional CLT): the limiting process is derived for the measurement error of the time-invariant marginal copula under the continuous-semimartingale assumption. It is unclear whether the result extends when the local-volatility estimator is inconsistent at jump times, which would alter the rate and the form of the empirical process used for the GoF test.

minor comments (3)

- [Abstract, §5] The phrase 'near-perfect bind' in the abstract and §5 is informal; replace with a quantitative statement of the GoF statistic or distance to the Gumbel copula.

- [§3] Notation for the realized copula estimator and the local-volatility kernel should be introduced once and used consistently; some passages mix 'realized variance' and 'local volatility' without explicit linkage.

- [§4] The simulation design in §4 could usefully report coverage of the functional CLT bands or finite-sample bias of the copula estimator under increasing jump intensity.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive report. We address each major comment below and indicate the revisions we will make to strengthen the manuscript while remaining faithful to its theoretical scope.

read point-by-point responses

-

Referee: [§2, Theorem 1] §2 (model setup) and Theorem 1 (consistency): the estimator and its consistency rest on the maintained assumption that the latent price process is a continuous semimartingale, allowing consistent local-volatility recovery by in-fill asymptotics. The empirical application in §5 uses equity and bond futures transaction data, which standardly contain price jumps; the paper does not report jump-robustness checks or simulations with jumps, so the measurement-error propagation into the copula estimator and the Gumbel fit remain unexamined.

Authors: We agree that Theorem 1 and the consistency of the realized copula estimator are derived under the continuous semimartingale assumption. Futures transaction data can contain jumps, and we did not previously examine their effect on the copula estimates. We will add Monte Carlo experiments that inject jumps into the price process and report the resulting bias in the empirical copula and the Gumbel goodness-of-fit statistic. A brief discussion of this robustness exercise will be inserted in §5. revision: yes

-

Referee: [§5] §5 (empirical results): the headline claim that 'a Gumbel copula is found to offer a near-perfect bind' is obtained by feeding the local-volatility estimates directly into the empirical copula. Because the consistency and FCLT results are derived only under continuity, any jump-induced inconsistency in the local-vol estimates directly affects the reported copula shape and GoF statistic; no alternative jump-robust local-vol estimator or sensitivity analysis is provided.

Authors: The referee is correct that the reported Gumbel fit and GoF p-value rest on the local-volatility estimates. We will revise §5 to include a sensitivity analysis that replaces the baseline local-volatility estimator with two jump-robust alternatives (truncated realized volatility and bipower-variation-based local volatility). We will report the resulting changes, if any, in the estimated copula and the GoF test outcome. revision: yes

-

Referee: [Theorem 3] Theorem 3 (functional CLT): the limiting process is derived for the measurement error of the time-invariant marginal copula under the continuous-semimartingale assumption. It is unclear whether the result extends when the local-volatility estimator is inconsistent at jump times, which would alter the rate and the form of the empirical process used for the GoF test.

Authors: Theorem 3 is stated and proved under the continuous-semimartingale assumption maintained throughout the paper. Deriving the corresponding functional CLT when local-volatility estimates are inconsistent at jump times would require a new theoretical argument that lies outside the present contribution. We will add an explicit caveat in the text of §4 and §5 stating that the asymptotic justification of the GoF test applies under continuity and that the empirical results should be interpreted with this qualification. revision: partial

- Extension of the functional central limit theorem in Theorem 3 to price processes containing jumps

Circularity Check

No circularity: estimator and asymptotics are defined from high-frequency data and standard in-fill theory without self-referential reduction.

full rationale

The realized copula is constructed directly as the empirical copula of local volatility estimates extracted from high-frequency returns. Consistency and the functional CLT for the measurement-error process are derived from in-fill asymptotics under the maintained continuous semimartingale assumption; these steps invoke standard stochastic calculus results rather than any fitted parameter or prior self-citation that encodes the target copula shape. The Gumbel-copula finding is an empirical observation on futures data, not a prediction forced by the estimator definition. No self-definitional, fitted-input, or uniqueness-imported steps appear in the derivation chain.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Asset price processes are continuous semimartingales with stochastic volatility

- domain assumption The marginal copula of volatility is time-invariant

Reference graph

Works this paper leans on

-

[1]

Answering the skeptics: Yes, standard volatility models do provide accurate forecasts,

Andersen, T. G., and T. Bollerslev, 1998, “Answering the skeptics: Yes, standard volatility models do provide accurate forecasts,” International Economic Review , 39, 885–905. Andersen, T. G., T. Bollerslev, F. X. Diebold, and H. Ebens, 2001, “T he distribution of realized stock return volatility,” Journal of Financial Economics , 61, 43–76. Andersen, T. ...

1998

-

[2]

Variance Risk Premiums,

Carr, P., and L. Wu, 2009, “Variance Risk Premiums,” Review of Financial Studies , 22, 1311–1341. Chong, C. H., and V. Todorov, 2023, “The fine structure of volatilit y dynamics,” Working paper. Christensen, K., R. C. A. Oomen, and R. Ren` o, 2022, “The drift bu rst hypothesis,” Journal of Econometrics, 227, 461–497. Christensen, K., M. Thyrsgaard, and B. ...

2009

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.