Recognition: unknown

Weighted Automata and Regular Expressions for Financial Systems

Pith reviewed 2026-05-10 05:37 UTC · model grok-4.3

The pith

Weighted finite finance automata correspond to weighted finance regular expressions via a Kleene-Schützenberger theorem, enabling formal analysis of quantitative financial properties.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

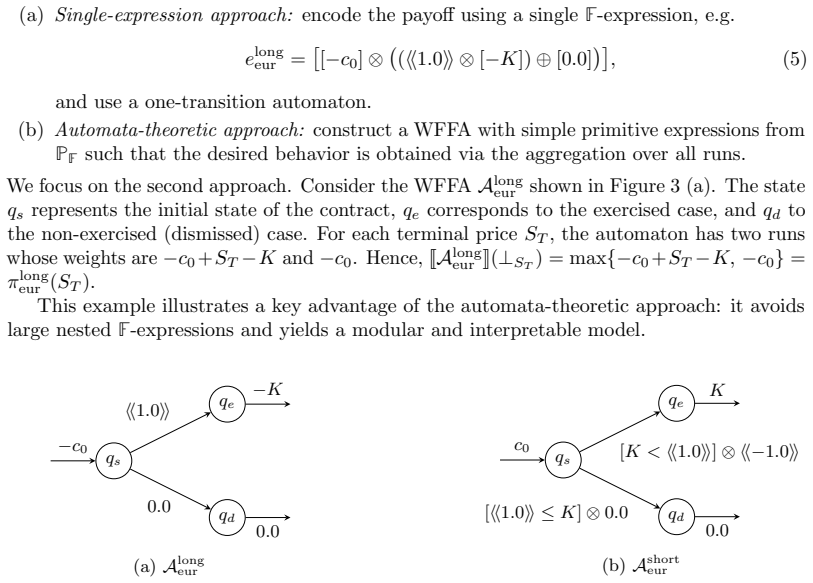

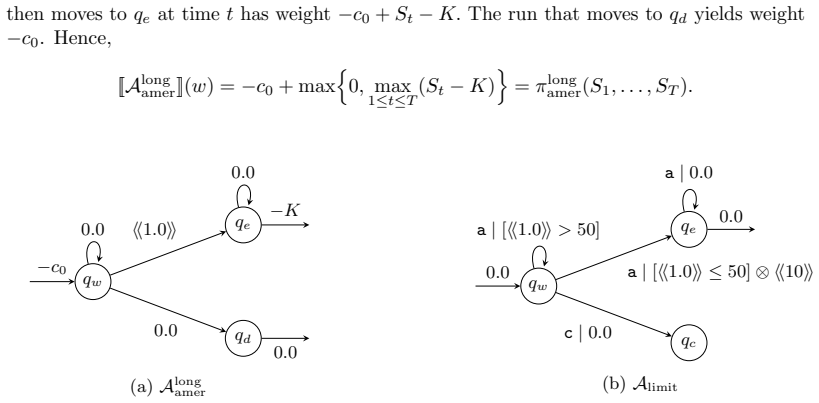

The paper establishes a Kleene-Schützenberger-type correspondence between weighted finite finance automata and weighted finance regular expressions, together with effective translation procedures between the two formalisms. This correspondence supplies a compositional language-theoretic model for quantitative financial properties driven by uncertain economic variables and permits algorithmic solution of decision and optimization problems such as extremal-payoff computation on expressive yet tractable subclasses.

What carries the argument

The Kleene-Schützenberger correspondence between weighted finite finance automata (WFFAs) and weighted finance regular expressions, which supplies bidirectional translations and supports evaluation of payoffs across market scenarios.

If this is right

- Financial instruments and trading strategies can be evaluated compositionally across multiple market scenarios.

- Extremal payoffs can be computed algorithmically for given automata or expressions.

- Expressive yet computationally tractable subclasses admit efficient decision procedures for optimization problems.

Where Pith is reading between the lines

- The same automata could serve as the backend for scenario generators that produce payoff distributions for risk calculations.

- Translations between automata and expressions might allow automatic verification of regulatory constraints expressed as regular properties.

Load-bearing premise

Financial systems driven by uncertain economic variables can be faithfully represented as weighted automata whose weights capture quantitative payoffs without losing essential market dynamics or requiring domain-specific extensions beyond the stated model.

What would settle it

A concrete financial scenario whose payoff sequence cannot be generated by any weighted finite automaton whose weights stay within the model’s finite state space and translation rules.

Figures

read the original abstract

We introduce weighted finite finance automata (WFFA), a formal framework for modeling and analyzing quantitative properties of financial systems driven by uncertain economic variables such as stock prices, interest rates, and exchange rates. The model provides a compositional and language-theoretic approach to scenario-based financial analysis, enabling systematic evaluation of financial instruments and trading strategies. To specify such systems, we introduce weighted finance regular expressions, a declarative language for quantitative financial properties. We establish a Kleene-Sch\"utzenberger-type correspondence between WFFAs and weighted finance regular expressions, together with effective translation procedures between the two formalisms. On the algorithmic side, we investigate fundamental decision and optimization problems for WFFAs, including the computation of extremal payoffs, and identify expressive yet computationally tractable subclasses. These results provide a foundation for formal, compositional, and efficient analysis of financial systems under multiple market scenarios.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces weighted finite finance automata (WFFAs) to model quantitative properties of financial systems driven by uncertain variables such as stock prices and interest rates. It defines weighted finance regular expressions as a declarative specification language for these properties. The central result is a Kleene-Schützenberger-type equivalence between WFFAs and the expressions, accompanied by effective translations in both directions. The work further studies decision and optimization problems on WFFAs, including extremal-payoff computation, and identifies expressive yet tractable subclasses.

Significance. If the correspondence and translations hold, the manuscript supplies a compositional, language-theoretic framework for scenario-based financial analysis that directly leverages existing weighted-automata algorithms. The tractable-subclass results are especially useful for practical verification of trading strategies, while the effective translations enable declarative specification without sacrificing algorithmic access. These contributions extend standard semiring-weighted automata theory to a finance setting in a manner that preserves the usual inductive proofs.

major comments (1)

- [§3] §3, Theorem 3.1: the inductive proof of the expression-to-automaton direction assumes the underlying semiring is complete for the star operator, yet the paper does not verify that the chosen payoff semiring (with possible negative or unbounded weights) satisfies this; this property is load-bearing for the claimed effective translation.

minor comments (3)

- The abstract states that translations are 'effective' but never reports their asymptotic complexity; adding a brief complexity statement after each construction would clarify practicality.

- [§2] Notation for the semiring operations (⊕, ⊗) is used in §2 before being formally introduced; a short preliminaries subsection would prevent reader confusion.

- [§4] Figure 2 (example WFFA) omits explicit weight labels on two transitions; the accompanying text refers to them but the diagram itself is incomplete.

Simulated Author's Rebuttal

We appreciate the referee's positive assessment of the manuscript and the recommendation for minor revision. We address the major comment below and will revise the manuscript to incorporate the requested clarification.

read point-by-point responses

-

Referee: [§3] §3, Theorem 3.1: the inductive proof of the expression-to-automaton direction assumes the underlying semiring is complete for the star operator, yet the paper does not verify that the chosen payoff semiring (with possible negative or unbounded weights) satisfies this; this property is load-bearing for the claimed effective translation.

Authors: We agree that the completeness of the semiring for the star operator is essential to the inductive proof of Theorem 3.1. The payoff semiring is introduced in Section 2 as the structure (ℝ ∪ {−∞, +∞}, min, +) (or its max-plus dual) to model extremal payoffs. While this semiring is known to be complete in the literature on weighted automata when restricted to bounded weights or finite scenario sets (as assumed throughout our financial models), we did not explicitly verify the condition in the presence of negative or unbounded weights. We will add a short lemma or remark in the revised version confirming that the star operator remains well-defined under our modeling assumptions (finite automata and scenario-bounded payoffs), thereby preserving the effective translation. This is a clarification rather than a change to the results. revision: yes

Circularity Check

No significant circularity

full rationale

The paper defines weighted finite finance automata (WFFAs) and weighted finance regular expressions as new objects, then states a Kleene-Schützenberger-type correspondence together with effective translations. This is a standard inductive construction once the underlying semiring and semantics are fixed; the abstract gives no indication that the finance-specific weights or payoff computations are used to define the automata or expressions in terms of each other, nor does it rely on self-citation for the core theorem. The decision and optimization results are presented as separate algorithmic investigations rather than as inputs to the correspondence. No load-bearing step reduces by construction to a fitted parameter or prior self-referential claim.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Kleene-Schützenberger theorem holds for the chosen weight structure in the finance automata model

- domain assumption Financial systems with uncertain variables admit a compositional automata representation

invented entities (2)

-

Weighted finite finance automata (WFFA)

no independent evidence

-

Weighted finance regular expressions

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Almagor, U

S. Almagor, U. Boker, and O. Kupferman,What’s decidable about weighted automata?, Information and Computation282(2022)

2022

-

[2]

Babari, M

P. Babari, M. Droste, and V. Perevoshchikov,Weighted register automata and weighted logic on data words, Theoretical Computer Science744(2018), 3–21

2018

-

[3]

Babel, P

K. Babel, P. Daian, M. Kelkar, and A. Juels,Clockwork finance: automated analysis of economic security in smart contracts, IEEE Symposium on Security and Privacy (Los Alamitos, CA), IEEE Computer Society, 2023, pp. 622–639

2023

-

[4]

Bacci, P

G. Bacci, P. Bouyer, U. Fahrenberg, K. G. Larsen, N. Markey, and P.-A. Reynier, Optimal and robust controller synthesis using energy timed automata with uncertainty, Formal Aspects of Computing33(2021), no. 1, 3–25

2021

-

[5]

Baier and J.-P

C. Baier and J.-P. Katoen,Principles of model checking, MIT Press, Cambridge, MA, 2008

2008

-

[6]

J. C. Cox, S. A. Ross, and M. Rubinstein,Option pricing: a simplified approach, Journal of Financial Economics7(1979), no. 3, 229–263

1979

-

[7]

Droste, W

M. Droste, W. Kuich, and H. Vogler (eds.),Handbook of weighted automata, Springer, Berlin, 2009

2009

-

[8]

Droste and D

M. Droste and D. Kuske,Skew and infinitary formal power series, Theoretical Computer Science366(2006), no. 2, 199–227

2006

-

[9]

Droste and V

M. Droste and V. Perevoshchikov,Multi-weighted automata and MSO logic, Theory of Computing Systems59(2016), no. 2, 231–261

2016

-

[10]

Droste and G

M. Droste and G. Rahonis,Weighted automata and weighted logics with discounting, Theoretical Computer Science410(2009), no. 37, 3481–3494

2009

-

[11]

1, European Mathematical Society Publishing House, Z¨ urich, 2021, pp

Manfred Droste and Dietrich Kuske,Weighted automata, Handbook of Automata Theory (Jean-´Eric Pin, ed.), vol. 1, European Mathematical Society Publishing House, Z¨ urich, 2021, pp. 113–150

2021

-

[12]

Eilenberg,Automata, languages, and machines, vol

S. Eilenberg,Automata, languages, and machines, vol. b, Academic Press, New York, 1974

1974

-

[13]

F. J. Fabozzi (ed.),Handbook of finance: Valuation, financial modeling, and quantitative tools, Wiley, Hoboken, NJ, 2008

2008

-

[14]

Foucault, M

T. Foucault, M. Pagano, and A. R¨ oell,Market liquidity, Oxford University Press, Oxford, 2013. 25

2013

-

[15]

Garg and S

M. Garg and S. Sarswat,The design and regulation of exchanges: a formal approach, FSTTCS 2022 (Wadern), LIPIcs, vol. 250, Schloss Dagstuhl – Leibniz-Zentrum f¨ ur Informatik, 2022, pp. 1–21

2022

-

[16]

Gastin and B

P. Gastin and B. Monmege,A unifying survey on weighted logics and weighted automata, Soft Computing22(2018), no. 4, 1047–1065

2018

-

[17]

B. K. Hassani,Scenario analysis in risk management: Theory and practice in finance, Springer, Cham, 2016

2016

-

[18]

J. E. Hopcroft and J. D. Ullman,Introduction to automata theory, Addison-Wesley, Reading, MA, 1979

1979

-

[19]

J. C. Hull,Options, futures, and other derivatives, Prentice Hall, Upper Saddle River, NJ, 1993

1993

-

[20]

S. C. Kleene,Representation of events in nerve nets and finite automata, Automata Studies, Princeton University Press, Princeton, NJ, 1956, pp. 3–42

1956

-

[21]

Kruschwitz and A

L. Kruschwitz and A. Loeffler,Discounted cash flow, John Wiley & Sons, Chichester, 2005

2005

-

[22]

Kuich and A

W. Kuich and A. Salomaa,Semirings, automata, languages, Springer, Berlin, 1986

1986

-

[23]

K. G. Larsen, G. Behrmann, E. Brinksma, A. Fehnker, T. Hune, P. Pettersson, and J. Romijn,As cheap as possible: efficient cost-optimal reachability for priced timed automata, CAV 2001 (Berlin), LNCS, vol. 2102, Springer, 2001, pp. 493–505

2001

-

[24]

D. G. Luenberger,Investment science, Oxford University Press, Oxford, 1999

1999

-

[25]

Natenberg,Option volatility and pricing, McGraw-Hill, New York, 2014

S. Natenberg,Option volatility and pricing, McGraw-Hill, New York, 2014

2014

-

[26]

M. O. Rabin,Probabilistic automata, Information and Control6(1963), no. 3, 230–245

1963

-

[27]

M. O. Rabin and D. Scott,Finite automata and their decision problems, IBM Journal of Research and Development3(1959), no. 2, 114–125

1959

-

[28]

Salomaa and M

A. Salomaa and M. Soittola,Automata-theoretic aspects of formal power series, Text and Monographs in Computer Science, Springer, New York, 1978

1978

-

[29]

M. P. Sch¨ utzenberger,On the definition of a family of automata, Information and Control 4(1961), no. 2–3, 245–270

1961

-

[30]

Z. Wei, X. Zhang, Y. Zhang, and M. Sun,Weighted automata extraction and explanation of recurrent neural networks for natural language tasks, Journal of Logical and Algebraic Methods in Programming136(2023), 100907. 26 Appendices A Detailed Proofs This appendix provides detailed proofs of the main results as well as additional technical arguments omitted f...

2023

-

[31]

∈ T2; •for (i 1, i2)∈I, wt I(i1, i2) = wtI1(i1)⊗wt I2(i2); •for (f 1, f2)∈F, wt F (f1, f2) = wtF1(f1)⊗wt F2(i2); • for t = ((q1, q2), a,(q′ 1, q′ 2)) ∈T , wtT (t) = [wtT1(q1, a, q′

-

[32]

Note that here⊗is applied toF-expressions

⊗wt T2(q2, a, q′ 2)]. Note that here⊗is applied toF-expressions. It can be shown that [ [A⊗] ]= [ [A1] ]⊗[ [A2] ]. The idea is that, for each word w, there is a one-to-one correspondence between the runs of A⊗ and the pairs of runs of A1 and A2 on the same word w. By pairing states and synchronizing transitions on the same input symbol, each accepting run...

-

[33]

Since [ [A] ](ε) = 0, we have qI ̸= qF

Summing over all runs then yields the Cauchy product of [ [A 1] ] and [ [A2] ] (b) Let A = (Q,{q I }, T,{q F }, [qI 7→1 ],wt T , [qF 7→1 ]). Since [ [A] ](ε) = 0, we have qI ̸= qF . We defineA ∗ fromAby merging the statesq I andq F , i.e. A∗ = (Q\ {q F },{q I }, T ′,{q I },[q I 7→1],wt ′ T ,[q I 7→1]). where: •T ′ =T ′ 1 ∪T ′ 2 such that –T ′ 1 ={(q, a, q...

-

[34]

By merging the initial state qI and the final state qF , every run of A∗ corresponds to a sequence of one or more runs of A concatenated end-to-end

and, for all ( q, a, qI) ∈T ′ 2, by wtT ′(q, a, qI) = wtT (q, a, qF ). By merging the initial state qI and the final state qF , every run of A∗ corresponds to a sequence of one or more runs of A concatenated end-to-end. Each transition in A∗ that originally ended at qF now loops back to qI, so the weight of a run in A∗ is exactly the product of the weight...

-

[35]

,| |qf | |E}} and, for every q′ f = (qf , i) ∈F ′, we let wtF ′(q′ f) = wtF (qf); • for every t = (p, a, q) ∈T , every ip ∈ {1,

= wtI(q0); •F ′ = {(qf , i) |q f ∈Fandi∈ { 1, . . . ,| |qf | |E}} and, for every q′ f = (qf , i) ∈F ′, we let wtF ′(q′ f) = wtF (qf); • for every t = (p, a, q) ∈T , every ip ∈ {1, . . . ,| |p| |E} and every iq ∈ {1, . . . ,| |wtT (t)| |E}, we lett ′ = ((p, ip), a,(q, i q))∈T ′ and wtT ′(t′) = (wtT (t))(iq) E . Then, [ [AE] ]= [ [A⟨E⟩⊕] ]and hence [ [WFFAΣ...

-

[36]

lM i=1 ⟨ ⟨πi⟩ ⟩ # , e <0 =

∈S for all i∈ [k]. Then, again, by (b), e can also be replaced with an equivalent expression from⟨E⟩ ⊕. 30 These observations imply that, by modifying only transition weights, we may transform A∗ into an automaton A∗ ⟨E⟩⊕ ∈WFFA Σ,F(⟨E⟩⊕) without changing its behavior, i.e., [ [A∗ ⟨E⟩⊕ ] ]= F ∗. By Lemma 6.7, there exists an automaton A∗ E ∈WFFA Σ,F(E) wit...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.