Recognition: unknown

Testing replication for an agent-based model of market fragmentation and latency arbitrage

Pith reviewed 2026-05-09 23:06 UTC · model grok-4.3

The pith

A replication of the 2016 market fragmentation model finds that its main qualitative results reverse when the zero-intelligence traders use an alternative version of the greedy strategy.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

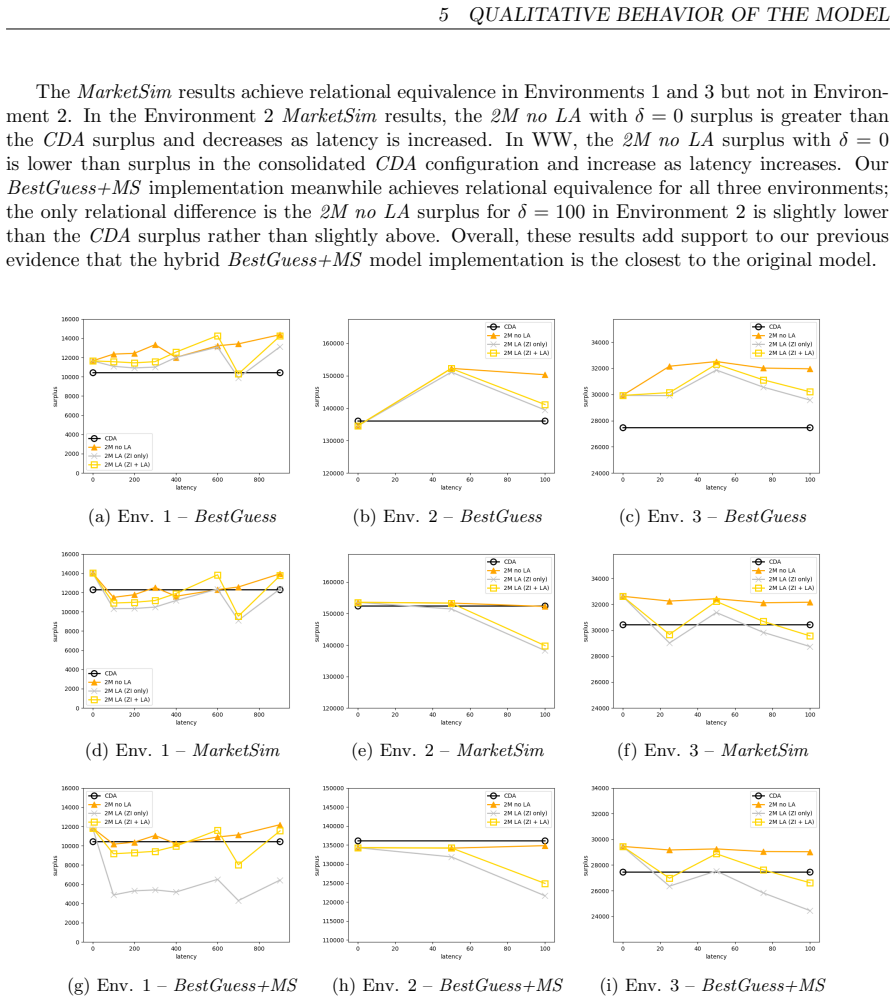

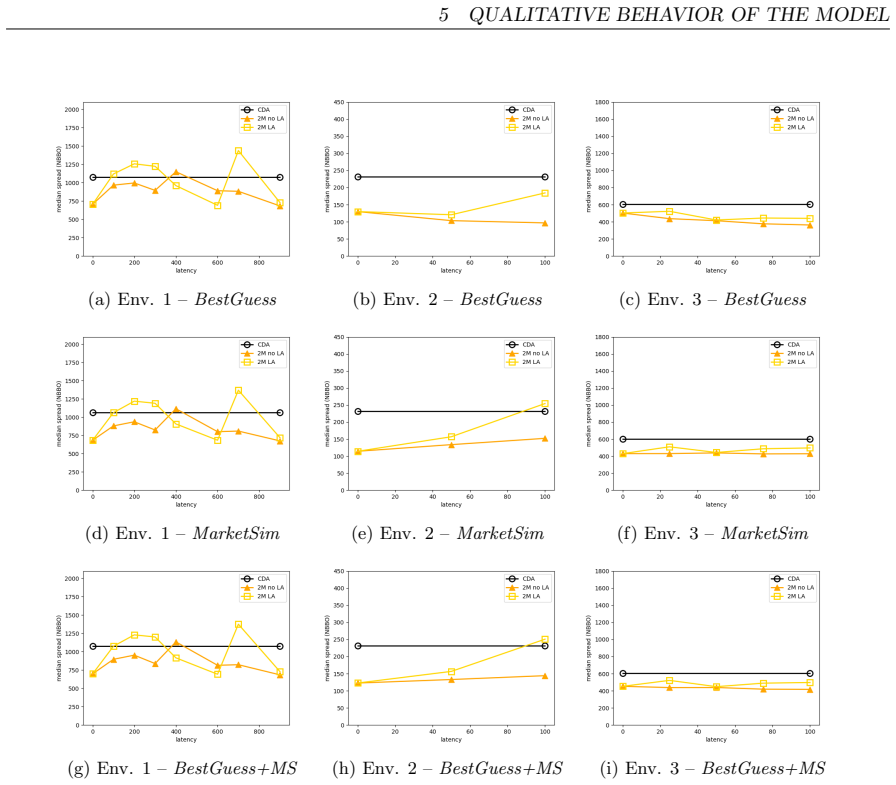

The central claim is that many qualitative takeaways from the original model are sensitive to the precise implementation of the greedy strategy given to zero-intelligence trader agents. When the authors substitute an alternative interpretation of that strategy, market fragmentation decreases execution times across all experiments and increases trader welfare in most experiments, while the original results do not hold.

What carries the argument

The zero-intelligence trader agents equipped with a greedy strategy extension, whose exact decision rule determines whether fragmentation improves or worsens execution speed and welfare.

If this is right

- More simulation runs allow bootstrap confidence intervals that support statistical tests of quantitative alignment in agent-based market models.

- Relational equivalence can be achieved even when quantitative alignment fails in higher-complexity latency settings.

- Releasing an ODD protocol alongside code makes future independent replications and extensions of the model easier to perform.

- Qualitative policy conclusions about market structure can change when the same agent rule is implemented in a different but still plausible way.

Where Pith is reading between the lines

- Finance simulation studies may need explicit decision-rule variants documented at publication to avoid hidden sensitivity in reported outcomes.

- Regulators or exchange designers using such models should test multiple reasonable interpretations of trader behavior before acting on fragmentation effects.

- The bootstrap-interval method demonstrated here could be applied to other published agent-based studies that report only mean outcomes without variance data.

Load-bearing premise

The alternative interpretation of the greedy strategy counts as a fair robustness check on the original model rather than a material change to its intent, and relational equivalence on most metrics is enough to establish qualitative sensitivity even when quantitative alignment is rejected.

What would settle it

Running the released original codebase and the new replication side-by-side with identical random seeds, parameter values, and the two different greedy-strategy rules would show whether the reported reversal in execution times and welfare is reproduced or disappears.

Figures

read the original abstract

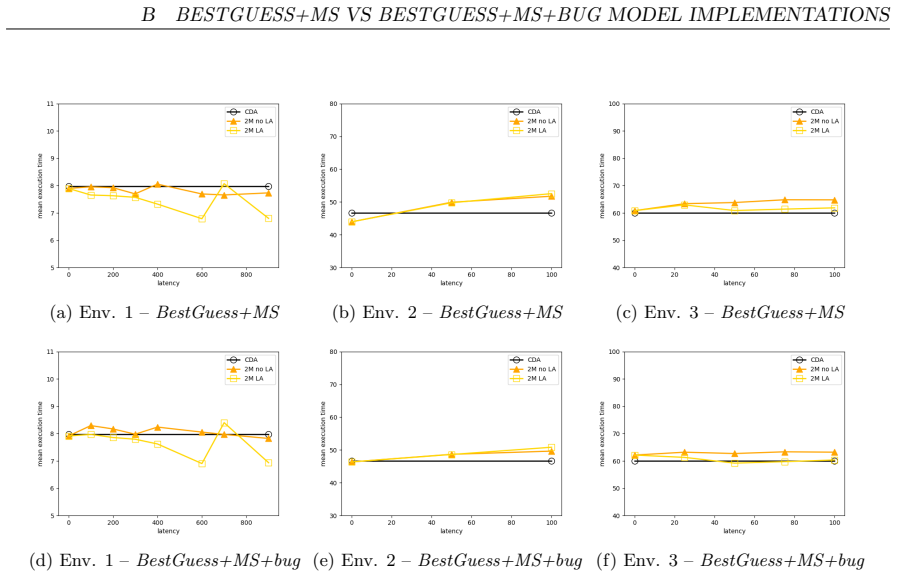

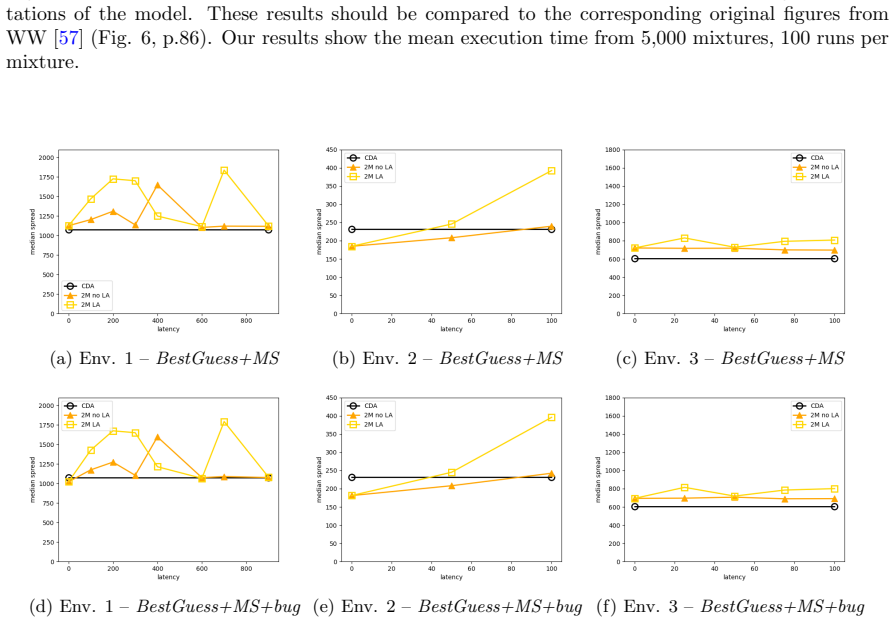

This study strengthens the foundations of multi-venue market modeling by attempting an independent replication of Wah and Wellman's 2016 model of latency arbitrage in a fragmented market. We find that faithful replication is hindered by missing implementation details in the original paper and limited quantitative reporting. We demonstrate that increasing the number of simulation runs beyond the original design allows for the creation of bootstrap confidence intervals to support rigorous tests of quantitative alignment, compensating for lacking distributional information (e.g. variance). We also demonstrate that increased complexity across the modeled scenarios corresponds with increased difficulty aligning to the original results. We draw on a codebase released by the original authors in connection with a later paper to recover additional implementation details; however, we reject quantitative alignment between that codebase and the published results. Combining information from the paper and the released code, we achieve relational equivalence for most metrics but reject quantitative alignment for model settings where latency is non-zero. We show that many of the qualitative takeaways from the original paper on the effects of market fragmentation and latency arbitrage are sensitive to the specifics of a `greedy strategy' extension given to the zero-intelligence (ZI) trader agents. Under an alternative interpretation of this strategy, we find that market fragmentation decreases execution times in all experiments and increases trader welfare in most experiments. Finally, to facilitate future replication, critique, and extension, we provide an ODD (Overview, Design concepts, Details) protocol for our implementations of the model.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript is an independent replication study of Wah and Wellman (2016) on an agent-based model of market fragmentation and latency arbitrage. It reports that faithful replication is impeded by missing implementation details and limited quantitative reporting in the original; the authors combine the paper with a later-released codebase, introduce bootstrap confidence intervals for alignment tests, achieve relational equivalence on most metrics while rejecting quantitative alignment for non-zero latency, and show that qualitative conclusions on fragmentation and latency-arbitrage effects are sensitive to the interpretation of the 'greedy strategy' extension to zero-intelligence traders. Under an alternative reading of that strategy, fragmentation reduces execution times in all experiments and raises trader welfare in most. An ODD protocol is supplied to support future work.

Significance. If the sensitivity result is robust, the work usefully illustrates how underspecified agent rules in ABMs can affect policy-relevant conclusions about market design, while the bootstrap-CI and relational-equivalence methods, together with the ODD protocol, supply concrete tools that strengthen replicability standards in quantitative finance. The explicit release of implementation details is a clear positive contribution.

major comments (2)

- [§5] §5 (alternative greedy-strategy results): The central claim that 'many of the qualitative takeaways ... are sensitive to the specifics of a greedy strategy extension' rests on comparing the authors' recovered implementation against an alternative interpretation. Because quantitative alignment is rejected for non-zero latency (both with the published results and the released codebase), the manuscript must demonstrate that the alternative is a minor clarification rather than a substantive change to order-placement or cancellation logic. No direct quotation or formal alignment to the original Wah & Wellman (2016) description is provided, so the observed reversal (fragmentation always lowers execution time, mostly improves welfare) could be an artifact of the chosen alternative rather than evidence of fragility in the original model.

- [Methods] Methods (relational-equivalence definition): The paper adopts relational equivalence as a proxy when quantitative matches cannot be achieved, citing an ad-hoc axiom that this is valid. Given that the sensitivity conclusion depends on this proxy, the decision procedure used to construct the alternative greedy strategy must be stated explicitly and shown to be independent of the authors' own implementation choices; otherwise the test does not isolate sensitivity of the original model.

minor comments (2)

- [Abstract] Abstract: the phrase 'many of the qualitative takeaways' is left unspecified; a short list of the affected metrics (execution time, welfare, etc.) would improve precision.

- [Tables and figures] Table/figure captions: several metric definitions (e.g., exact welfare calculation, execution-time aggregation) are referenced but not restated; a compact notation table would aid readability.

Simulated Author's Rebuttal

We thank the referee for their constructive and detailed comments, which have helped clarify how to strengthen the presentation of our replication results. We address each major comment below and indicate the revisions made to the manuscript.

read point-by-point responses

-

Referee: [§5] §5 (alternative greedy-strategy results): The central claim that 'many of the qualitative takeaways ... are sensitive to the specifics of a greedy strategy extension' rests on comparing the authors' recovered implementation against an alternative interpretation. Because quantitative alignment is rejected for non-zero latency (both with the published results and the released codebase), the manuscript must demonstrate that the alternative is a minor clarification rather than a substantive change to order-placement or cancellation logic. No direct quotation or formal alignment to the original Wah & Wellman (2016) description is provided, so the observed reversal (fragmentation always lowers execution time, mostly improves welfare) could be an artifact of the chosen alternative rather than evidence of fragility in the original model.

Authors: We agree that direct quotations and explicit alignment to the original description are necessary. In the revised manuscript we now include verbatim excerpts from Wah and Wellman (2016) on the greedy extension to ZI traders. The original wording is brief and leaves the precise scope of 'greedy' (venue selection for placement versus cancellation) ambiguous. Our alternative reading is constructed as one logically consistent interpretation of that ambiguity while preserving the zero-intelligence character of the agents. We have added a side-by-side comparison table that maps each interpretation to the original text, showing that the difference is confined to the scope of the greedy rule rather than a change in order-placement or cancellation mechanics. This addition supports our claim that the qualitative reversal illustrates sensitivity to underspecification rather than constituting an artifact. revision: yes

-

Referee: [Methods] Methods (relational-equivalence definition): The paper adopts relational equivalence as a proxy when quantitative matches cannot be achieved, citing an ad-hoc axiom that this is valid. Given that the sensitivity conclusion depends on this proxy, the decision procedure used to construct the alternative greedy strategy must be stated explicitly and shown to be independent of the authors' own implementation choices; otherwise the test does not isolate sensitivity of the original model.

Authors: We have revised the Methods section to provide an explicit, step-by-step decision procedure for constructing the alternative greedy strategy. The procedure is: (1) extract every sentence in Wah and Wellman (2016) that describes ZI trader behavior and the greedy extension; (2) flag all points of ambiguity in how 'greedy' is applied; (3) enumerate interpretations that remain consistent with zero-intelligence principles (no lookahead or global optimization); and (4) adopt the reading that differs from the recovered implementation only in the scope of the greedy choice. This procedure was derived exclusively from the published paper text before any code inspection or modification, thereby ensuring independence from our implementation choices. We also clarify that relational equivalence is used only where quantitative alignment is impossible due to missing variance statistics in the original work, and we rely on bootstrap confidence intervals for the statistical tests. revision: yes

Circularity Check

Replication uses external benchmarks and independent re-implementation with no reduction to self-fitted inputs

full rationale

The paper is a replication study of Wah & Wellman (2016). It compares an independent re-implementation against the original published results and a separately released codebase from the original authors' later work. Quantitative alignment is explicitly rejected for non-zero latency settings, and relational equivalence is reported only after combining external sources. The sensitivity claim on the greedy ZI strategy rests on an explicit alternative interpretation whose results are contrasted with the recovered implementation; no parameter is fitted from the present paper's own outputs and then renamed as a prediction. No self-citations are load-bearing, no uniqueness theorems are imported from the authors' prior work, and no ansatz or renaming of known results occurs. The ODD protocol is supplied to make the implementation self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Zero-intelligence traders operate with a greedy strategy extension whose implementation details are not fully specified in the original paper

- ad hoc to paper Relational equivalence on metrics is a valid proxy for model alignment when quantitative matches cannot be achieved due to missing original details

Reference graph

Works this paper leans on

-

[1]

When finance meets physics: The impact of the speed of light on financial markets and their regulation.Financial Review, 49(2):271–281, 2014

James J Angel. When finance meets physics: The impact of the speed of light on financial markets and their regulation.Financial Review, 49(2):271–281, 2014

2014

-

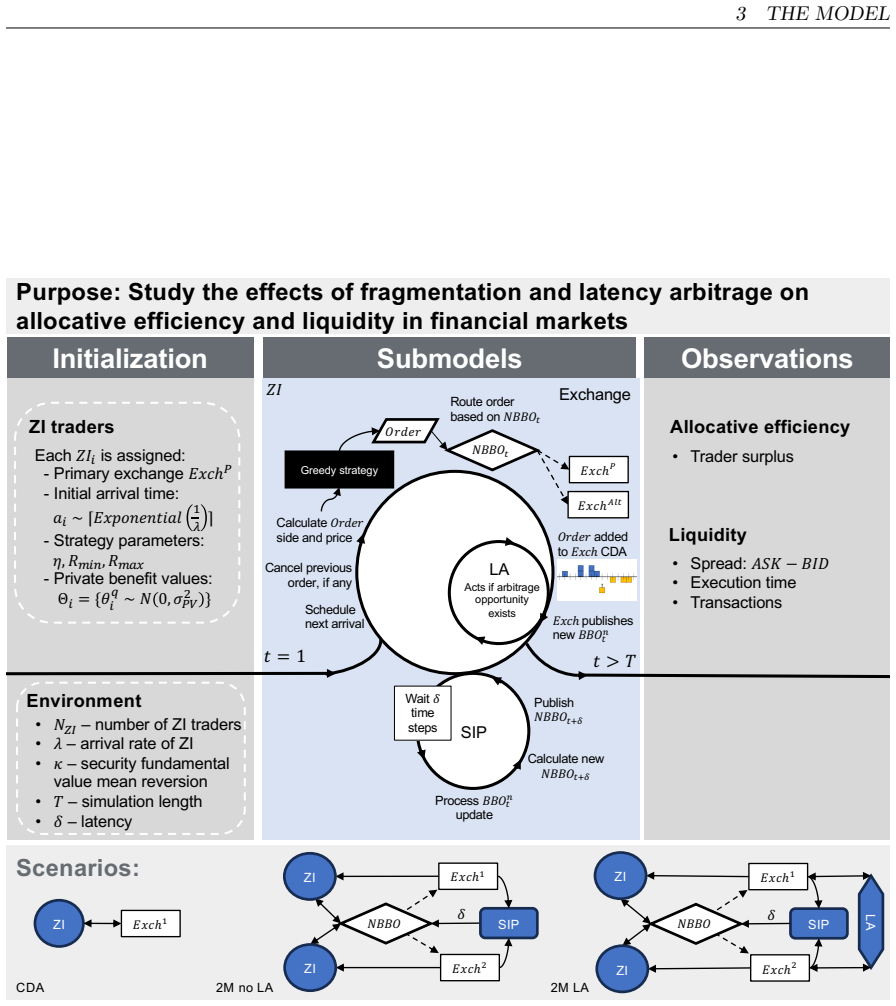

[2]

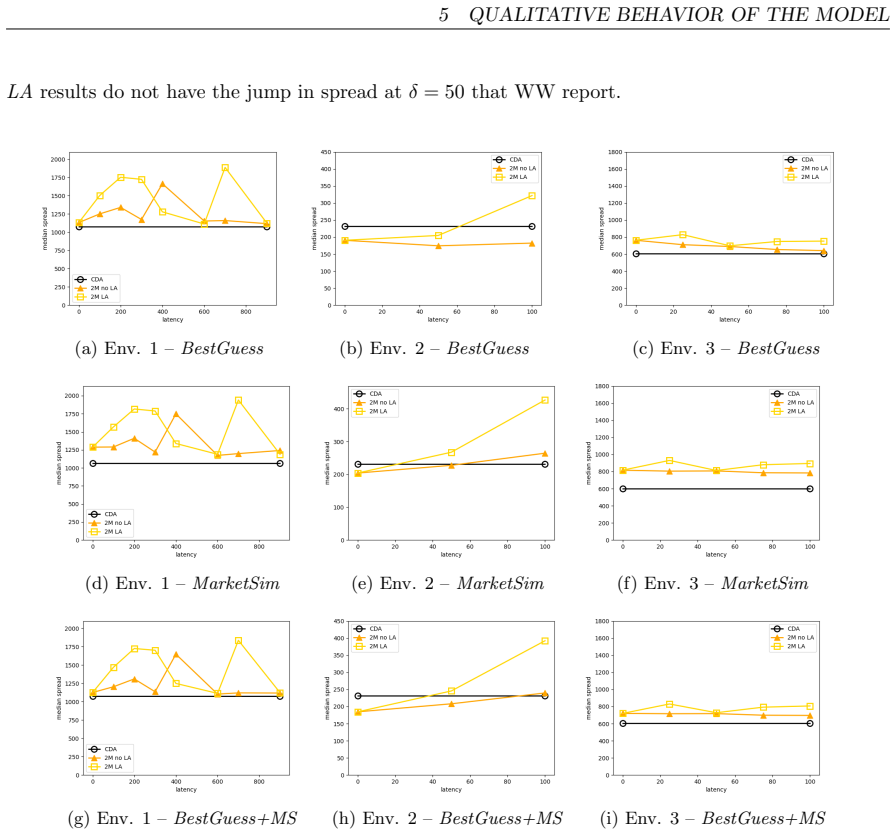

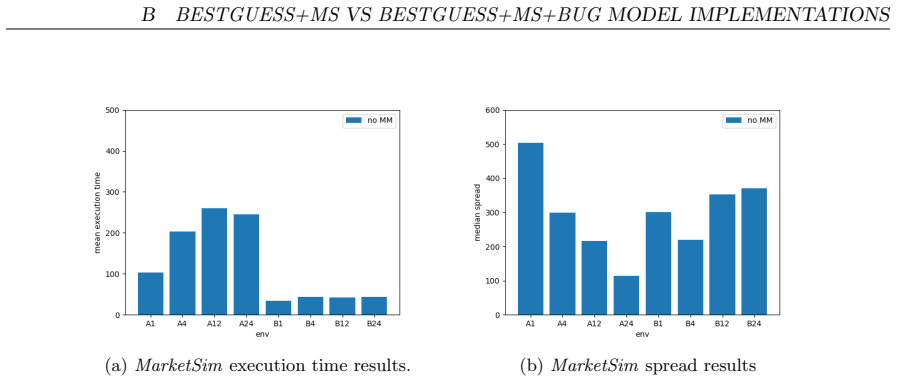

Advancing the art of simulation in the social sciences

Robert Axelrod. Advancing the art of simulation in the social sciences. InSimulating social phenomena, pages 21–40. Springer, 1997

1997

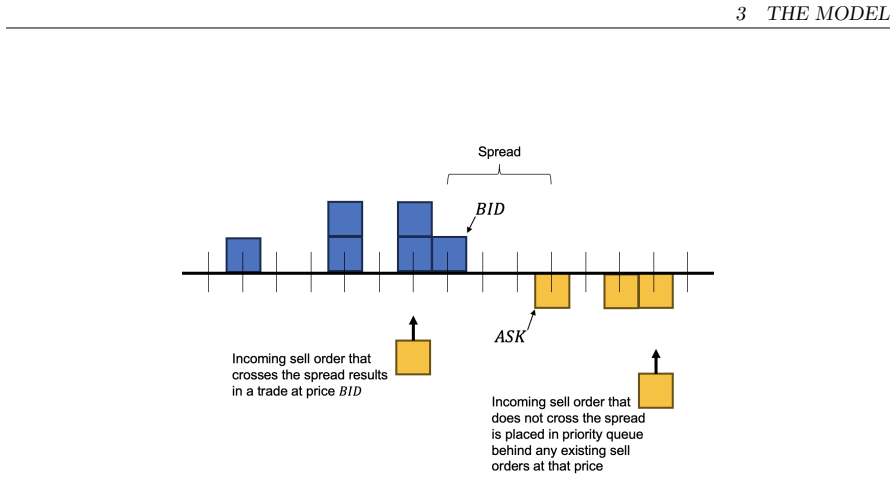

-

[3]

Epstein, and Michael D

Robert Axtell, Robert Axelrod, Joshua M. Epstein, and Michael D. Cohen. Aligning simulation models: A case study and results.Computational & Mathematical Organization Theory, 1(2):123– 141, February 1996. ©2026 The MITRE Corporation. ALL RIGHTS RESER VED. Approved for Public Release; Distribution Unlimited. Public Release Case Number 25-1956. 31 REFERENCE...

1996

-

[4]

High-frequency trading and market performance.The Journal of Finance, 75(3):1495–1526, 2020

Markus Baldauf and Joshua Mollner. High-frequency trading and market performance.The Journal of Finance, 75(3):1495–1526, 2020. Publisher: Wiley Online Library

2020

-

[5]

Fast agent-based simulation framework with applications to reinforcement learning and the study of trading latency effects

Peter Belcak, Jan-Peter Calliess, and Stefan Zohren. Fast agent-based simulation framework with applications to reinforcement learning and the study of trading latency effects. InInternational Workshop on Multi-Agent Systems and Agent-Based Simulation, pages 42–56. Springer, 2021

2021

-

[6]

Foley, and Brian F

Richard Bookstaber, Michael D. Foley, and Brian F. Tivnan. Toward an understanding of market resilience: market liquidity and heterogeneity in the investor decision cycle.Journal of Economic Interaction and Coordination, 11(2):205–227, October 2016

2016

-

[7]

Order-flow segmentation, liquidity, and price discovery: The role of latency delays.Journal of Financial and Quantitative Analysis, 55(8):2555–2587, 2020

Michael Brolley and David A Cimon. Order-flow segmentation, liquidity, and price discovery: The role of latency delays.Journal of Financial and Quantitative Analysis, 55(8):2555–2587, 2020. Publisher: Cambridge University Press

2020

-

[8]

The high-frequency trading arms race: Frequent batch auctions as a market design response.The Quarterly Journal of Economics, 130(4):1547– 1621, 2015

Eric Budish, Peter Cramton, and John Shim. The high-frequency trading arms race: Frequent batch auctions as a market design response.The Quarterly Journal of Economics, 130(4):1547– 1621, 2015. Publisher: MIT Press

2015

-

[9]

A call for replication studies.Public Finance Review, 38(6):787–793, 2010

Leonard E Burman, W Robert Reed, and James Alm. A call for replication studies.Public Finance Review, 38(6):787–793, 2010. Publisher: SAGE Publications Sage CA: Los Angeles, CA

2010

-

[10]

David Byrd, Maria Hybinette, and Tucker Hybinette Balch. Abides: Towards high-fidelity market simulation for ai research.arXiv preprint arXiv:1904.12066, 2019

-

[11]

EGTAOnline: An experiment manager for simulation-based game studies

Ben-Alexander Cassell and Michael P Wellman. EGTAOnline: An experiment manager for simulation-based game studies. InInternational Workshop on Multi-Agent Systems and Agent- Based Simulation, pages 85–100. Springer, 2012

2012

-

[12]

Comment Letter to the U.S

Chicago Stock Exchange, Inc. Comment Letter to the U.S. Securities and Exchange Commission Regarding SR-CHX-2016-16 (CHX Liquidity Taking Access Delay), October 2016. Published: Comment letter to Brent J. Fields, Secretary, U.S. Securities and Exchange Commission

2016

-

[13]

An open-source limit-order-book exchange for teaching and research

Dave Cliff. An open-source limit-order-book exchange for teaching and research. In2018 IEEE Symposium Series on Computational Intelligence (SSCI), pages 1853–1860. IEEE, 2018

2018

-

[14]

Zero is not enough: on the lower limit of agent intelligence for continuous double auction markets.Hewlett-Packard Labs Technical Reports (1997), 1997

Dave Cliff and Janet Bruten. Zero is not enough: on the lower limit of agent intelligence for continuous double auction markets.Hewlett-Packard Labs Technical Reports (1997), 1997

1997

-

[15]

A call to arms: stan- dards for agent-based modeling and simulation.Journal of Artificial Societies and Social Simu- lation, 18(3):12, 2015

Andrew Collins, Mikel Petty, Daniele Vernon-Bido, and Solomon Sherfey. A call to arms: stan- dards for agent-based modeling and simulation.Journal of Artificial Societies and Social Simu- lation, 18(3):12, 2015

2015

-

[16]

R. Cont. Empirical properties of asset returns: stylized facts and statistical issues.Quantitative Finance, 1(2):223–236, 2001

2001

-

[17]

Quantitative Model of Price Diffusion and Market Friction Based on Trading<? format?>as a Mechanistic Random Process.Physical review letters, 90(10):108102, 2003

Marcus G Daniels, J Doyne Farmer, L´ aszl´ o Gillemot, Giulia Iori, and Eric Smith. Quantitative Model of Price Diffusion and Market Friction Based on Trading<? format?>as a Mechanistic Random Process.Physical review letters, 90(10):108102, 2003. Publisher: APS

2003

-

[18]

Open Exchange (OpEx) / Wiki / Home, 2012

Marco De Luca. Open Exchange (OpEx) / Wiki / Home, 2012

2012

-

[19]

Agent-based model exploration of latency arbitrage in fragmented financial markets

Matthew Duffin and John Cartlidge. Agent-based model exploration of latency arbitrage in fragmented financial markets. In2018 IEEE Symposium Series on Computational Intelligence (SSCI), pages 2312–2320. IEEE, 2018

2018

-

[20]

Replication, replication and replication: Some hard lessons from model alignment.Journal of Artificial Societies and Social Simulation, 6(4), 2003

Bruce Edmonds and David Hales. Replication, replication and replication: Some hard lessons from model alignment.Journal of Artificial Societies and Social Simulation, 6(4), 2003

2003

-

[21]

Springer, 2008

Norman Ehrentreich.Agent-based modeling: The Santa Fe Institute artificial stock market model revisited. Springer, 2008

2008

-

[22]

TXSE Fact Sheet, October 2025

Texas Stock Exchange. TXSE Fact Sheet, October 2025. ©2026 The MITRE Corporation. ALL RIGHTS RESER VED. Approved for Public Release; Distribution Unlimited. Public Release Case Number 25-1956. 32 REFERENCES REFERENCES

2025

-

[23]

Heterogeneity and feedback in an agent- based market model.Journal of Physics: Condensed Matter, 17(14):S1259, March 2005

Fran¸ cois Ghoulmie, Rama Cont, and Jean-Pierre Nadal. Heterogeneity and feedback in an agent- based market model.Journal of Physics: Condensed Matter, 17(14):S1259, March 2005

2005

-

[24]

Allocative efficiency of markets with zero-intelligence traders: Market as a partial substitute for individual rationality.Journal of political economy, 101(1):119–137, 1993

Dhananjay K Gode and Shyam Sunder. Allocative efficiency of markets with zero-intelligence traders: Market as a partial substitute for individual rationality.Journal of political economy, 101(1):119–137, 1993

1993

-

[25]

Informed traders and limit order markets.Journal of Financial Economics, 93(1):67–87, 2009

Ronald L Goettler, Christine A Parlour, and Uday Rajan. Informed traders and limit order markets.Journal of Financial Economics, 93(1):67–87, 2009. Publisher: Elsevier

2009

-

[26]

A standard protocol for describing individual-based and agent-based models.Ecological modelling, 198(1-2):115–126, 2006

Volker Grimm, Uta Berger, Finn Bastiansen, Sigrunn Eliassen, Vincent Ginot, Jarl Giske, John Goss-Custard, Tamara Grand, Simone K Heinz, Geir Huse, and others. A standard protocol for describing individual-based and agent-based models.Ecological modelling, 198(1-2):115–126, 2006

2006

-

[27]

Using the ODD protocol and NetLogo to replicate agent-based models.Ecological Modelling, 501:110967,

Volker Grimm, Uta Berger, Justin M Calabrese, Ainara Cort´ es-Avizanda, Jordi Ferrer, Mathias Franz, J¨ urgen Groeneveld, Florian Hartig, Oliver Jakoby, Roger Jovani, and others. Using the ODD protocol and NetLogo to replicate agent-based models.Ecological Modelling, 501:110967,

-

[28]

The odd protocol: a review and first update.Ecological modelling, 221(23):2760–2768, 2010

Volker Grimm, Uta Berger, Donald L DeAngelis, J Gary Polhill, Jarl Giske, and Steven F Rails- back. The odd protocol: a review and first update.Ecological modelling, 221(23):2760–2768, 2010

2010

-

[29]

Theory Development Via Replicated Simu- lations and the Added Value of Standards.Journal of Artificial Societies and Social Simulation, 23(1), 2020

Jonas Hauke, Sebastian Achter, and Matthias Meyer. Theory Development Via Replicated Simu- lations and the Added Value of Standards.Journal of Artificial Societies and Social Simulation, 23(1), 2020

2020

-

[30]

A survey of agent-based modeling practices (January 1998 to July 2008).Journal of Artificial Societies and Social Simulation, 12(4):9, 2009

Brian Heath, Raymond Hill, and Frank Ciarallo. A survey of agent-based modeling practices (January 1998 to July 2008).Journal of Artificial Societies and Social Simulation, 12(4):9, 2009

1998

-

[31]

Agent-based modeling: What I learned from the artificial stock market.Social Science Computer Review, 20(2):174–186, 2002

Paul E Johnson. Agent-based modeling: What I learned from the artificial stock market.Social Science Computer Review, 20(2):174–186, 2002. Publisher: Sage Publications Sage CA: Thousand Oaks, CA

2002

-

[32]

Building the Santa Fe artificial stock market.Physica A, 1:20, 2002

Blake LeBaron. Building the Santa Fe artificial stock market.Physica A, 1:20, 2002

2002

-

[33]

The surprising success of a replication that failed.Journal of Artificial Societies and Social Simulation, 13(2):9, 2010

Michael Macy and Yoshimichi Sato. The surprising success of a replication that failed.Journal of Artificial Societies and Social Simulation, 13(2):9, 2010

2010

-

[34]

A Finan- cial Market Simulation Environment for Trading Agents Using Deep Reinforcement Learning

Chris Mascioli, Anri Gu, Yongzhao Wang, Mithun Chakraborty, and Michael Wellman. A Finan- cial Market Simulation Environment for Trading Agents Using Deep Reinforcement Learning. In Proceedings of the 5th ACM International Conference on AI in Finance, pages 117–125, 2024

2024

-

[35]

Horizontal and vertical multiple im- plementations in a model of industrial districts.JASSS, 11:1–25, 2008

Ugo Merlone, Michele Sonnessa, Pietro Terna, and others. Horizontal and vertical multiple im- plementations in a model of industrial districts.JASSS, 11:1–25, 2008

2008

-

[36]

An artificial stock market.Artificial Life and Robotics, 3(1):27–31, 1999

Richard G Palmer, W Brian Arthur, John H Holland, and Blake LeBaron. An artificial stock market.Artificial Life and Robotics, 3(1):27–31, 1999. Publisher: Springer

1999

-

[37]

Lessons learned from converting the artificial stock market to interval arithmetic.Journal of Artificial Societies and Social Simulation, 8(2), 2005

Gary Polhill and Luis Izquierdo. Lessons learned from converting the artificial stock market to interval arithmetic.Journal of Artificial Societies and Social Simulation, 8(2), 2005

2005

-

[38]

The ghost in the model (and other effects of floating point arithmetic).Journal of Artificial Societies and Social Simulation, 8(1), 2005

J Gary Polhill, Luis R Izquierdo, and Nicholas M Gotts. The ghost in the model (and other effects of floating point arithmetic).Journal of Artificial Societies and Social Simulation, 8(1), 2005

2005

-

[39]

Preis, S

T. Preis, S. Golke, W. Paul, and J. J. Schneider. Multi-agent-based Order Book Model of financial markets.Europhysics Letters, 75(3):510, July 2006

2006

-

[40]

Prospects and pitfalls of statistical testing: Insights from replicating the demographic prisoner’s dilemma.Journal of Artificial Societies and Social Simu- lation, 13(4):1, 2010

Wolfgang Radax and Bernhard Rengs. Prospects and pitfalls of statistical testing: Insights from replicating the demographic prisoner’s dilemma.Journal of Artificial Societies and Social Simu- lation, 13(4):1, 2010. ©2026 The MITRE Corporation. ALL RIGHTS RESER VED. Approved for Public Release; Distribution Unlimited. Public Release Case Number 25-1956. 33...

2010

-

[41]

Revisiting Cont’s stylized facts for modern stock markets.Quantitative Finance, 25(9):1343–1373, 2025

Ethan Ratliff-Crain, Colin M Van Oort, Matthew TK Koehler, and Brian F Tivnan. Revisiting Cont’s stylized facts for modern stock markets.Quantitative Finance, 25(9):1343–1373, 2025. Publisher: Taylor & Francis

2025

-

[42]

A replication and analysis of tiebout competition using an agent-based com- putational model.Social Science Computer Review, 33(2):198–216, 2015

Chad W Seagren. A replication and analysis of tiebout competition using an agent-based com- putational model.Social Science Computer Review, 33(2):198–216, 2015. Publisher: SAGE Publications Sage CA: Los Angeles, CA

2015

-

[43]

Self-Regulatory Organizations; Chicago Stock Exchange, Inc.; Notice of Filing of Proposed Rule Change to Adopt the CHX Liquidity Taking Access Delay

Securities and Exchange Commission. Self-Regulatory Organizations; Chicago Stock Exchange, Inc.; Notice of Filing of Proposed Rule Change to Adopt the CHX Liquidity Taking Access Delay. Securities Exchange Act Release 34-78860, U.S. Securities and Exchange Commission, September 2016

2016

-

[44]

Self-Regulatory Organizations; Chicago Stock Exchange, Inc.; Notice of Filing of Proposed Rule Change to Adopt the CHX Liquidity Enhancing Access Delay

Securities and Exchange Commission. Self-Regulatory Organizations; Chicago Stock Exchange, Inc.; Notice of Filing of Proposed Rule Change to Adopt the CHX Liquidity Enhancing Access Delay. Securities Exchange Act Release 34-80041, U.S. Securities and Exchange Commission, February 2017

2017

-

[45]

Statistical theory of the continuous double auction.Quantitative finance, 3(6):481, 2003

Eric Smith, J Doyne Farmer, L´ aszl´ o Gillemot, and Supriya Krishnamurthy. Statistical theory of the continuous double auction.Quantitative finance, 3(6):481, 2003. Publisher: IOP Publishing

2003

-

[46]

Visual ODD: A standardised visualisation illustrating the narrative of agent-based models.Journal of Artificial Societies and Social Simulation, 27(4), 2024

Leonna Szangolies, Marie-Sophie Rohw¨ ader, Hazem Ahmed, Fatima Jahanmiri, Alexander Wag- ner, Rodrigo Souto-Veiga, Volker Grimm, and Cara Gallagher. Visual ODD: A standardised visualisation illustrating the narrative of agent-based models.Journal of Artificial Societies and Social Simulation, 27(4), 2024. Publisher: JASSS

2024

-

[47]

Replicating and breaking models: good for you and good for ecology.Oikos, 124(6):691–696, 2015

Jan C Thiele and Volker Grimm. Replicating and breaking models: good for you and good for ecology.Oikos, 124(6):691–696, 2015. Publisher: Wiley Online Library

2015

-

[48]

Adding to the Regulator’s Toolbox: Integration and Extension of Two Leading Market Models.Papers, May 2011

Brian Tivnan, Matthew Koehler, Matthew McMahon, Matthew Olson, Neal Rothleder, and Ra- jani Shenoy. Adding to the Regulator’s Toolbox: Integration and Extension of Two Leading Market Models.Papers, May 2011

2011

-

[49]

Tivnan, Matthew T

Brian F. Tivnan, Matthew T. K. Koehler, David Slater, Jason Veneman, and Brendan F. Tivnan. Towards a model of the U.S. stock market: How important is the securities information processor? In2017 Winter Simulation Conference (WSC), pages 1181–1192, December 2017

2017

-

[50]

Securities and Exchange Commission

U.S. Securities and Exchange Commission. Regulation NMS. Technical Report Release No. 34- 51808, U.S. Securities and Exchange Commission, 2005

2005

-

[51]

Securities and Exchange Commission

U.S. Securities and Exchange Commission. Regulation NMS: Minimum Pricing Increments, Access Fees, and Transparency of Better Priced Orders. Technical Report Release No. 34-101070, U.S. Securities and Exchange Commission, 2024

2024

-

[52]

Colin M Van Oort, Ethan Ratliff-Crain, Brian F Tivnan, and Safwan Wshah. Adaptive Agents and Data Quality in Agent-Based Financial Markets.arXiv preprint arXiv:2311.15974, 2023

-

[53]

Wouter Vermeer, Arthur Hjorth, Samuel M Jenness, Hendrick Brown, and Uri Wilensky. Leverag- ing modularity during replication of high-fidelity models: lessons from replicating an agent-based model for HIV prevention.Journal of artificial societies and social simulation: JASSS, 23(4):7, 2020

2020

-

[54]

Christian E Vincenot. How new concepts become universal scientific approaches: insights from citation network analysis of agent-based complex systems science.Proceedings of the Royal Society B: Biological Sciences, 285(1874):20172360, 2018. Publisher: The Royal Society

2018

-

[55]

Elaine Wah.Computational Models of Algorithmic Trading in Financial Markets.PhD Thesis, 2016

2016

-

[56]

Latency arbitrage, market fragmentation, and efficiency: A two-market model

Elaine Wah and Michael P Wellman. Latency arbitrage, market fragmentation, and efficiency: A two-market model. InProceedings of the fourteenth ACM conference on Electronic commerce, pages 855–872, 2013. ©2026 The MITRE Corporation. ALL RIGHTS RESER VED. Approved for Public Release; Distribution Unlimited. Public Release Case Number 25-1956. 34 A USINGMARK...

2013

-

[57]

Latency arbitrage in fragmented markets: A strategic agent-based analysis.Algorithmic Finance, 5(3-4):69–93, 2016

Elaine Wah and Michael P Wellman. Latency arbitrage in fragmented markets: A strategic agent-based analysis.Algorithmic Finance, 5(3-4):69–93, 2016

2016

-

[58]

Welfare effects of market making in contin- uous double auctions.Journal of Artificial Intelligence Research, 59:613–650, 2017

Elaine Wah, Mason Wright, and Michael P Wellman. Welfare effects of market making in contin- uous double auctions.Journal of Artificial Intelligence Research, 59:613–650, 2017

2017

-

[59]

Empirical game theoretic analysis: A survey.Journal of artificial intelligence research, 82:1017–1076, 2025

Michael P Wellman, Karl Tuyls, and Amy Greenwald. Empirical game theoretic analysis: A survey.Journal of artificial intelligence research, 82:1017–1076, 2025

2025

-

[60]

Making models match: Replicating an agent-based model

Uri Wilensky and William Rand. Making models match: Replicating an agent-based model. Journal of Artificial Societies and Social Simulation, 10(4):2, 2007

2007

-

[61]

Resolving a replication that failed: News on the Macy & Sato model.Journal of Artificial Societies and Social Simulation, 12(4):11, 2009

Oliver Will. Resolving a replication that failed: News on the Macy & Sato model.Journal of Artificial Societies and Social Simulation, 12(4):11, 2009

2009

-

[62]

The background traders arrive at the market according to a Poisson process with rateλ

Oliver Will and Rainer Hegselmann. A Replication That Failed on the Computational Model in’Michael W. Macy and Yoshimichi Sato: Trust, Cooperation and Market Formation in the US and Japan. Proceedings of the National Academy of Sciences, May 2002’.Journal of Artificial Societies and Social Simulation, 11(3):3, 2008. A UsingMarketSimto replicate WWW In ord...

2002

-

[63]

They do not specify how the ZI arrival times are made to be discrete

(p.75). They do not specify how the ZI arrival times are made to be discrete. We draw the ZI arrival times independently from an exponential distribution (⌈Exponential(1/λ)⌉). We choose to take the ceiling such that no event will be scheduled at timet= 0. We account for this by letting arrivals occur on times 1 throughT(inclusive), givingTtotal time steps...

2026

-

[64]

[E]vents are maintained in a queue ordered by time of occurrence

except forα. Theαvalue is based on the 2013 paper [56] and Wah’s dissertation [55], and it is further confirmed by looking at the default valueαinMarketSim. ID Rmin Rmax η ZI 1 0 125 1 ZI 2 0 250 1 ZI 3 0 500 1 ZI 4 250 500 1 ZI 5 0 1000 1 ZI 6 500 1000 0.4 ZI 7 500 1000 1 ZI 8 0 1500 0.6 ZI 9 1000 2000 0.4 ZI 10 0 2500 0.4 ZI 11 0 2500 1 Table 19: ZI str...

2013

-

[65]

Orders: map from order IDs to their respective orders

-

[66]

Bids: map from price to the queue of buy order IDs at that price

-

[67]

We measure execution time by the interval between order submission and transaction for orders that eventually trade

Asks: map from price to the queue of sell order IDs at that price The exchange publishes a BBO to its subscribers, a feed containing the best bid and offer prices in the LOB at that moment. LOBs are initialized with no bids or asks at the start. The BBO has null prices for its best available bid and ask whenever their respective side of the LOB is empty (...

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.