0

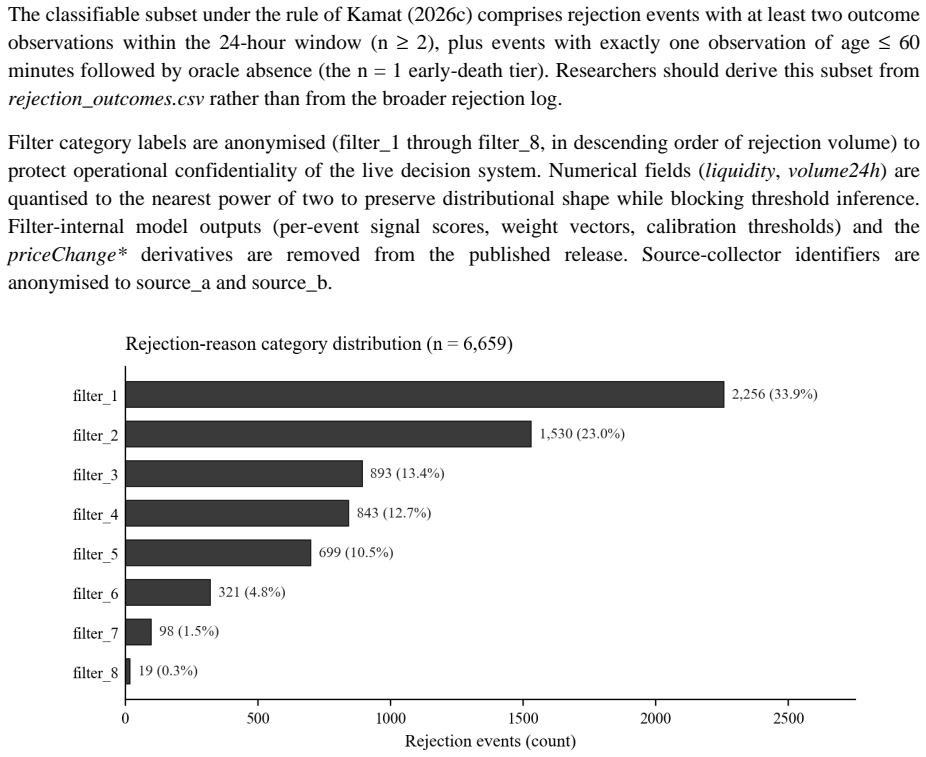

Benchmark dataset labels 6,659 rejected trades with five outcomes

RED-2400: A Public Benchmark of Algorithmically-Rejected Trading Events with Outcome Labels

RED-2400 records post-rejection price movements to let researchers test filter accuracy on the reject side directly.

full image

full image

abstract click to expand

RED-2400 is a public benchmark of algorithmically-rejected trading events from a live Solana decentralized-exchange filter stack. I logged the data continuously between 2026-04-10 and 2026-05-02. The benchmark contains 6,659 rejection events linked to 169,122 post-rejection price and liquidity observations and 1,836 graveyard-tracker snapshots. Outcome labels follow the five-tier classification of Kamat (2026c): saved (windowed), saved (early-death), missed, flat, and unclassifiable. Thresholds use the trough-to-reference and peak-to-reference price ratios within a 24-hour window. Most filter-design datasets cover the accept side only. That gap leaves reject-side outcomes unmeasured and biases filter validation. RED-2400 lets researchers replicate filter-precision claims directly. RED-2400 is the first window in a planned dataset series; subsequent windows will extend the time horizon and enable regime-stratified analysis.