Recognition: unknown

Adaptive Conformal Anomaly Detection with Time Series Foundation Models for Signal Monitoring

Pith reviewed 2026-05-10 01:16 UTC · model grok-4.3

The pith

A post-hoc adaptive conformal method produces an interpretable anomaly score directly as a false alarm rate p-value from any time series foundation model.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

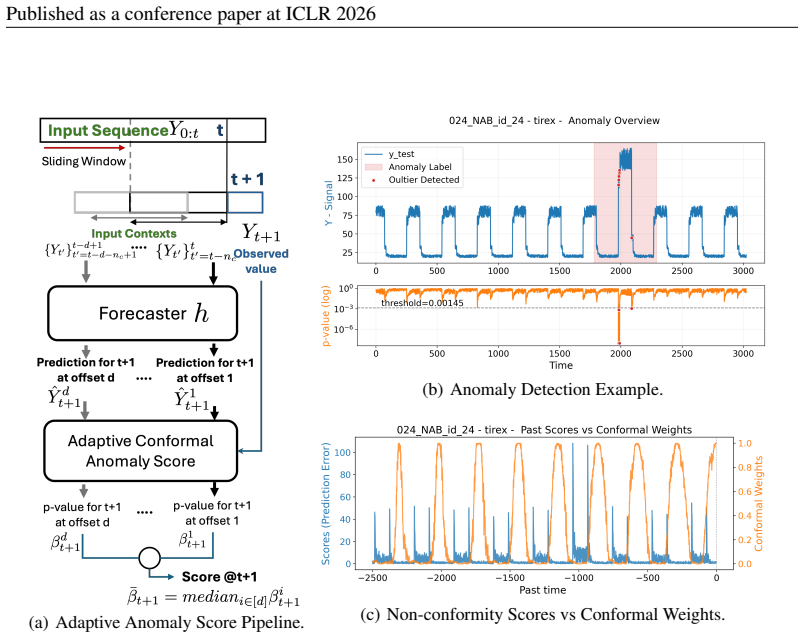

The proposed method employs weighted quantile conformal prediction bounds whose weighting parameters are learned adaptively from past predictions, yielding an interpretable anomaly score equivalent to a false alarm rate (p-value) that remains valid under distribution shifts while preserving out-of-sample guarantees.

What carries the argument

Weighted quantile conformal prediction bounds with adaptive learning of weighting parameters from past predictions, which dynamically adjusts the anomaly scoring for time series signals.

If this is right

- Integrates as a model-agnostic post-hoc step with any pre-trained foundation model.

- Maintains stable false alarm control during distribution shifts in time series data.

- Enables rapid deployment without additional training or fine-tuning expertise.

- Produces directly actionable decisions via the p-value interpretation of anomaly scores.

Where Pith is reading between the lines

- The adaptive weighting step may reduce manual calibration effort when applying foundation models to new monitoring tasks.

- This approach could be tested on non-time-series sequential data to check if similar adaptivity holds.

- Combining the method with different foundation model architectures would show how much the guarantees depend on the base predictor quality.

Load-bearing premise

That learning optimal weighting parameters adaptively from past predictions preserves the exchangeability and coverage guarantees of the underlying conformal prediction framework.

What would settle it

A dataset with strong distribution shifts where the observed false alarm rate for a nominal p-value level deviates substantially from the target rate.

Figures

read the original abstract

We propose a post-hoc adaptive conformal anomaly detection method for monitoring time series that leverages predictions from pre-trained foundation models without requiring additional fine-tuning. Our method yields an interpretable anomaly score directly interpretable as a false alarm rate (p-value), facilitating transparent and actionable decision-making. It employs weighted quantile conformal prediction bounds and adaptively learns optimal weighting parameters from past predictions, enabling calibration under distribution shifts and stable false alarm control, while preserving out-of-sample guarantees. As a model-agnostic solution, it integrates seamlessly with foundation models and supports rapid deployment in resource-constrained environments. This approach addresses key industrial challenges such as limited data availability, lack of training expertise, and the need for immediate inference, while taking advantage of the growing accessibility of time series foundation models. Experiments on both synthetic and real-world datasets show that the proposed approach delivers strong performance, combining simplicity, interpretability, robustness, and adaptivity.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a post-hoc adaptive conformal anomaly detection method for time series signal monitoring that uses predictions from pre-trained foundation models without fine-tuning. It applies weighted quantile conformal prediction with weighting parameters learned adaptively from past predictions to handle distribution shifts, claims that the resulting anomaly scores are valid p-values interpretable as false-alarm rates, and asserts that out-of-sample coverage guarantees are preserved.

Significance. If the coverage guarantees are rigorously established under adaptive weighting, the work would offer a practical, model-agnostic way to deploy foundation models for interpretable anomaly detection in industrial settings with limited data and distribution shifts, combining simplicity with stable false-alarm control.

major comments (2)

- [theoretical analysis / §3] The central claim that out-of-sample guarantees are preserved rests on the adaptive learning of weighting parameters from past predictions. The manuscript must supply an explicit derivation (likely in the theoretical analysis section) showing that the data-dependent weights maintain the exchangeability or martingale property required for the weighted quantile to deliver marginal coverage at level 1-α; standard weighted conformal results assume fixed weights and do not automatically extend to this adaptation rule.

- [experiments section] The abstract states that experiments demonstrate strong performance and preserved guarantees, yet the experimental protocol (including how adaptive weights are updated on the data stream and how coverage is verified under shifts) is not detailed enough to confirm that the empirical results support the validity claim rather than merely showing competitive detection rates.

minor comments (2)

- [method description] Clarify the precise update rule and loss function used to learn the weighting parameters from past residuals or predictions.

- [related work] Add a short discussion of how the method differs from existing adaptive conformal prediction techniques for non-stationary data.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive feedback. We address each major comment below and will revise the manuscript to strengthen the theoretical justification and experimental documentation.

read point-by-point responses

-

Referee: [theoretical analysis / §3] The central claim that out-of-sample guarantees are preserved rests on the adaptive learning of weighting parameters from past predictions. The manuscript must supply an explicit derivation (likely in the theoretical analysis section) showing that the data-dependent weights maintain the exchangeability or martingale property required for the weighted quantile to deliver marginal coverage at level 1-α; standard weighted conformal results assume fixed weights and do not automatically extend to this adaptation rule.

Authors: We agree that an explicit derivation is required. In the revised manuscript we will expand Section 3 with a formal proof that the adaptive weights, computed exclusively from past observations, are predictable with respect to the natural filtration. This predictability preserves the martingale property of the weighted conformal p-values, yielding marginal coverage at level 1-α under the maintained exchangeability assumption on the underlying time series. The derivation will explicitly contrast the fixed-weight case with our online adaptation rule and state the precise conditions under which validity holds. revision: yes

-

Referee: [experiments section] The abstract states that experiments demonstrate strong performance and preserved guarantees, yet the experimental protocol (including how adaptive weights are updated on the data stream and how coverage is verified under shifts) is not detailed enough to confirm that the empirical results support the validity claim rather than merely showing competitive detection rates.

Authors: We acknowledge the need for greater transparency. The revised experimental section will include: (i) the precise online update rule for the weighting parameters together with the chosen learning rate and window size; (ii) pseudocode for the streaming procedure; and (iii) additional figures and tables reporting empirical coverage rates over time, both on stationary segments and under controlled distribution shifts. These diagnostics will directly verify that the observed false-alarm rates remain consistent with the nominal level, thereby supporting the validity claim beyond detection performance. revision: yes

Circularity Check

No significant circularity; derivation relies on external conformal theory

full rationale

The paper proposes a post-hoc adaptive conformal anomaly detection method using weighted quantile bounds with weights learned from past predictions, claiming preservation of out-of-sample guarantees and p-value interpretability. No quoted equation or step reduces the claimed validity or anomaly score to a self-definition, a fitted input renamed as prediction, or a self-citation chain. The adaptation is presented as an extension of standard conformal prediction (external to the paper), with experiments providing empirical support. The derivation chain is self-contained against the stated assumptions rather than tautological.

Axiom & Free-Parameter Ledger

free parameters (1)

- weighting parameters

axioms (1)

- domain assumption Conformal prediction assumptions (e.g., exchangeability or appropriate coverage conditions) hold for the weighted quantiles derived from foundation model predictions.

Reference graph

Works this paper leans on

-

[1]

Adaptive conformal prediction by reweighting noncon- formity score.arXiv preprint arXiv:2303.12695,

10 Published as a conference paper at ICLR 2026 Salim I Amoukou and Nicolas JB Brunel. Adaptive conformal prediction by reweighting noncon- formity score.arXiv preprint arXiv:2303.12695,

-

[2]

A Gentle Introduction to Conformal Prediction and Distribution-Free Uncertainty Quantification

Anastasios N Angelopoulos and Stephen Bates. A gentle introduction to conformal prediction and distribution-free uncertainty quantification.arXiv preprint arXiv:2107.07511,

work page internal anchor Pith review Pith/arXiv arXiv

-

[3]

Chronos: Learning the Language of Time Series

Abdul Fatir Ansari, Lorenzo Stella, Caner Turkmen, Xiyuan Zhang, Pedro Mercado, Huibin Shen, Oleksandr Shchur, Syama Sundar Rangapuram, Sebastian Pineda Arango, Shubham Kapoor, et al. Chronos: Learning the language of time series.arXiv preprint arXiv:2403.07815,

work page internal anchor Pith review arXiv

-

[4]

Tirex: Zero-shot forecasting across long and short horizons with enhanced in-context learning

Andreas Auer, Patrick Podest, Daniel Klotz, Sebastian B¨ock, G¨unter Klambauer, and Sepp Hochre- iter. Tirex: Zero-shot forecasting across long and short horizons with enhanced in-context learn- ing.arXiv preprint arXiv:2505.23719,

-

[5]

Dive into time- series anomaly detection: A decade review.arXiv preprint arXiv:2412.20512,

Paul Boniol, Qinghua Liu, Mingyi Huang, Themis Palpanas, and John Paparrizos. Dive into time- series anomaly detection: A decade review.arXiv preprint arXiv:2412.20512,

-

[6]

Dhruv Choudhary, Arun Kejariwal, and Francois Orsini. On the runtime-efficacy trade-off of anomaly detection techniques for real-time streaming data.arXiv preprint arXiv:1710.04735,

-

[7]

H., Dayama, P., Reddy, C., Gifford, W

Vijay Ekambaram, Arindam Jati, Nam H Nguyen, Pankaj Dayama, Chandra Reddy, Wesley M Gifford, and Jayant Kalagnanam. Ttms: Fast multi-level tiny time mixers for improved zero-shot and few-shot forecasting of multivariate time series.arXiv preprint arXiv:2401.03955,

-

[8]

Subhankar Ghosh, Taha Belkhouja, Yan Yan, and Janardhan Rao Doppa. Improving uncertainty quantification of deep classifiers via neighborhood conformal prediction: Novel algorithm and theoretical analysis.arXiv preprint arXiv:2303.10694,

-

[9]

Anomaly detection models for iot time series data.arXiv preprint arXiv:1812.00890,

Federico Giannoni, Marco Mancini, and Federico Marinelli. Anomaly detection models for iot time series data.arXiv preprint arXiv:1812.00890,

-

[10]

Conformal inference for online prediction with arbitrary distribution shifts.Journal of Machine Learning Research, 25(162):1–36,

11 Published as a conference paper at ICLR 2026 Isaac Gibbs and Emmanuel J Cand `es. Conformal inference for online prediction with arbitrary distribution shifts.Journal of Machine Learning Research, 25(162):1–36,

2026

-

[11]

arXiv preprint arXiv:2305.12616 , year=

Isaac Gibbs, John J Cherian, and Emmanuel J Cand`es. Conformal prediction with conditional guar- antees.arXiv preprint arXiv:2305.12616,

-

[12]

Unsuper- vised model selection for time-series anomaly detection.arXiv preprint arXiv:2210.01078,

Mononito Goswami, Cristian Challu, Laurent Callot, Lenon Minorics, and Andrey Kan. Unsuper- vised model selection for time-series anomaly detection.arXiv preprint arXiv:2210.01078,

-

[13]

Moment: A family of open time-series foundation models

Mononito Goswami, Konrad Szafer, Arjun Choudhry, Yifu Cai, Shuo Li, and Artur Dubrawski. Moment: A family of open time-series foundation models.arXiv preprint arXiv:2402.03885,

-

[14]

Conformal prediction with localization.arXiv preprint arXiv:1908.08558,

Leying Guan. Conformal prediction with localization.arXiv preprint arXiv:1908.08558,

-

[15]

Split localized conformal prediction.arXiv preprint arXiv:2206.13092,

Xing Han, Ziyang Tang, Joydeep Ghosh, and Qiang Liu. Split localized conformal prediction.arXiv preprint arXiv:2206.13092,

-

[16]

A unifying method for outlier and change detection from data streams based on local polynomial fitting

Zhi Li, Hong Ma, and Yongbing Mei. A unifying method for outlier and change detection from data streams based on local polynomial fitting. InAdvances in Knowledge Discovery and Data Mining: 11th Pacific-Asia Conference, PAKDD 2007, Nanjing, China, May 22-25,

2007

-

[17]

The elephant in the room: Towards a reliable time-series anomaly detection benchmark

12 Published as a conference paper at ICLR 2026 Qinghua Liu and John Paparrizos. The elephant in the room: Towards a reliable time-series anomaly detection benchmark. InThe Thirty-eight Conference on Neural Information Processing Systems Datasets and Benchmarks Track,

2026

-

[18]

Deepant: A deep learning approach for unsupervised anomaly detection in time series.Ieee Access, 7:1991–2005,

Mohsin Munir, Shoaib Ahmed Siddiqui, Andreas Dengel, and Sheraz Ahmed. Deepant: A deep learning approach for unsupervised anomaly detection in time series.Ieee Access, 7:1991–2005,

1991

-

[19]

Inductive confidence machines for regression

Harris Papadopoulos, Kostas Proedrou, V olodya V ovk, and Alex Gammerman. Inductive confidence machines for regression. InMachine Learning: ECML 2002: 13th European Conference on Machine Learning Helsinki, Finland, August 19–23, 2002 Proceedings 13, pp. 345–356. Springer,

2002

-

[20]

k-shape: Efficient and accurate clustering of time series

John Paparrizos and Luis Gravano. k-shape: Efficient and accurate clustering of time series. In Proceedings of the 2015 ACM SIGMOD international conference on management of data, pp. 1855–1870,

2015

-

[21]

V olume under the surface: a new accuracy evaluation measure for time-series anomaly detection.Proceedings of the VLDB Endowment, 15(11):2774–2787, 2022a

John Paparrizos, Paul Boniol, Themis Palpanas, Ruey S Tsay, Aaron Elmore, and Michael J Franklin. V olume under the surface: a new accuracy evaluation measure for time-series anomaly detection.Proceedings of the VLDB Endowment, 15(11):2774–2787, 2022a. John Paparrizos, Yuhao Kang, Paul Boniol, Ruey S Tsay, Themis Palpanas, and Michael J Franklin. Tsb-uad:...

2000

-

[22]

Gecco 2018 industrial challenge: Monitoring of drinking-water quality.Accessed: Feb, 19:2019,

Frederik Rehbach, Steffen Moritz, Sowmya Chandrasekaran, Margarita Rebolledo, Martina Friese, and Thomas Bartz-Beielstein. Gecco 2018 industrial challenge: Monitoring of drinking-water quality.Accessed: Feb, 19:2019,

2018

-

[23]

Anomaly detection in iiot: A case study using machine learning

13 Published as a conference paper at ICLR 2026 Gauri Shah and Aashis Tiwari. Anomaly detection in iiot: A case study using machine learning. In Proceedings of the ACM India joint international conference on data science and management of data, pp. 295–300,

2026

-

[24]

Deep Time Series Models: A Comprehensive Survey and Benchmark

Yuxuan Wang, Haixu Wu, Jiaxiang Dong, Yong Liu, Mingsheng Long, and Jianmin Wang. Deep time series models: A comprehensive survey and benchmark.arXiv preprint arXiv:2407.13278,

work page internal anchor Pith review Pith/arXiv arXiv

-

[25]

TimesNet: Temporal 2D-Variation Modeling for General Time Series Analysis,

Haixu Wu, Tengge Hu, Yong Liu, Hang Zhou, Jianmin Wang, and Mingsheng Long. Timesnet: Tem- poral 2d-variation modeling for general time series analysis.arXiv preprint arXiv:2210.02186,

-

[26]

(2018), where anomalies are identified by deviations between predicted and observed values

14 Published as a conference paper at ICLR 2026 A RELATEDWORKEXTENDED Time Series Anomaly DetectionA key class of anomaly detection methods is prediction-based Giannoni et al. (2018), where anomalies are identified by deviations between predicted and observed values. These approaches assume that a well-trained forecaster captures normal temporal patterns,...

2026

-

[27]

The results indicate thatW 1-ACAS consistently outperforms the baseline methods, highlighting the advantages of an adaptive approach that dynamically learns how to weight past observations in a principled manner, rather than relying on a fixed number of past samples. (a) Random Shift Signal (b) Random Shift Calibration (c) Random Shift Error (d) Jump Shif...

2026

-

[28]

It supports zero-shot anomaly scoring using masked-token reconstruction error and is pretrained on a broad corpus including anomaly detection datasets (Liu & Paparrizos, 2024)

is a general-purpose TSFM based on a T5-style en- coder trained via masked time-series modeling. It supports zero-shot anomaly scoring using masked-token reconstruction error and is pretrained on a broad corpus including anomaly detection datasets (Liu & Paparrizos, 2024). For these approaches we adopt the implementations from Liu & Paparrizos (2024) with...

2024

-

[29]

Rows correspond to datasets (NAB, NEK, MSL, Y AHOO, Stock, WSD) and columns to metrics (PA-F1, Affiliation-F, AUC-PR, VUS-PR)

22 Published as a conference paper at ICLR 2026 (a) NAB — PA-F1 (b) NAB — Affiliation-F (c) NAB — AUC-PR (d) NAB — VUS-PR (e) NEK — PA-F1 (f) NEK — Affiliation-F (g) NEK — AUC-PR (h) NEK — VUS-PR (i) MSL — PA-F1 (j) MSL — Affiliation-F (k) MSL — AUC-PR (l) MSL — VUS-PR (m) Y AHOO — PA-F1 (n) Y AHOO-Affiliation-F (o) Y AHOO — AUC-PR (p) Y AHOO — VUS-PR Fig...

2026

-

[30]

(5 curated sequences, each with 2 features and approximately 100k samples). We evaluate our multivariate extensions,W1-ACAS-F andW 1-ACAS-H, combined with Chronos and TiRex forecasters that leverage all available historical context (up to their maximum context window, with a minimum of 52 past points). These are compared against strong semi-supervised dee...

2024

-

[31]

Dataset Forecaster AD Model PA-F1↑Affiliation-F↑FPR↓CalErr↓AUC-PR↑VUC-PR↑ TAO - CNN* 0.998 ± 0.001 0.999 ± 0.0000.000 ± 0.0000.612 ± 0.044 0.895 ± 0.094 0.999 ± 0.001 TAO - OmniAnomaly* 0.377 ± 0.021 0.863 ± 0.053 0.321 ± 0.153 0.497 ± 0.136 0.311 ± 0.039 0.940 ± 0.051 TAO - USAD* 0.172 ± 0.061 0.679 ± 0.006 0.986 ± 0.018 0.033 ± 0.027 0.018 ± 0.005 0.097...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.