Recognition: unknown

Optimal basis risk weighting in expectile-based parametric insurance

Pith reviewed 2026-05-08 13:22 UTC · model grok-4.3

The pith

Existence and uniqueness of the optimal basis risk weighting in expectile parametric insurance are fixed by boundary conditions in a utility maximization framework.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

In the utility-maximization setting for expectile-based parametric insurance, the optimal basis risk weighting exists and is unique precisely when a set of boundary conditions holds; otherwise the utility of the weighted contract is compared directly to no coverage and full indemnity. The analysis further establishes that conditional expectiles have separable derivatives precisely when the underlying loss distribution belongs to the location-scale family.

What carries the argument

The optimal basis risk weighting parameter, identified by solving the utility-maximization problem subject to boundary conditions on the expectile payment function.

If this is right

- When boundary conditions fail, the contract's utility is bounded by the no-insurance and full-indemnity utilities.

- Location-scale loss distributions allow the derivatives of conditional expectiles to factor into separate location and scale parts.

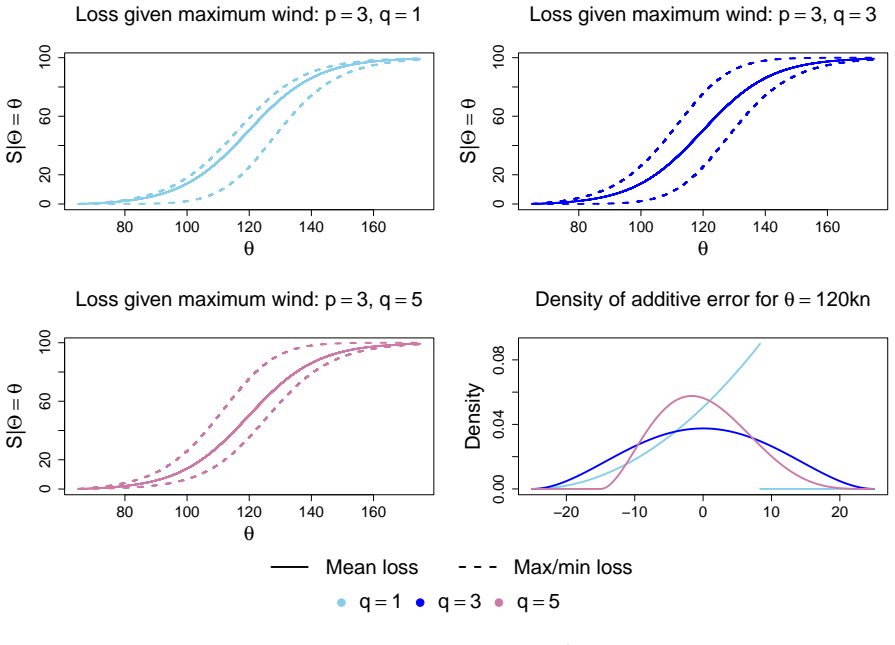

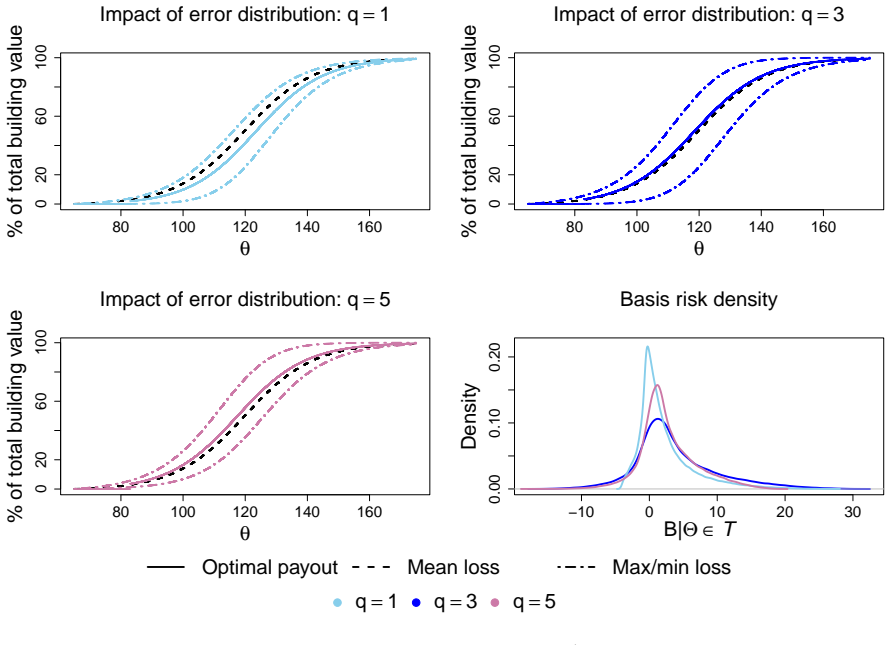

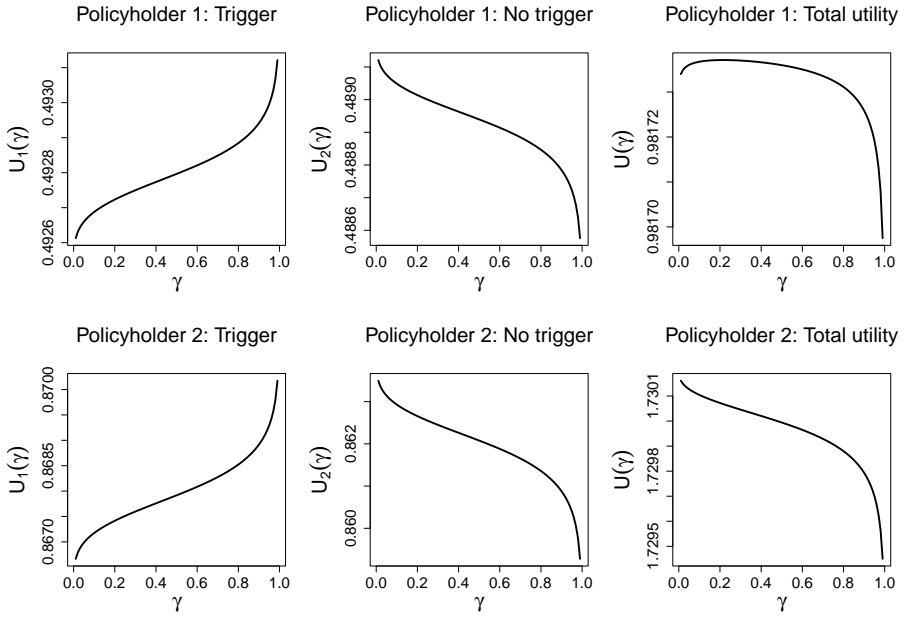

- The optimal weight increases with higher premium loadings and decreases with greater risk aversion in the hurricane simulation.

- Spatial loss dependence complicates but does not invalidate the boundary-condition approach.

Where Pith is reading between the lines

- Insurers could use the boundary conditions as a diagnostic before offering expectile contracts, checking whether a single weight will suffice for their client base.

- The separability result for location-scale families suggests that expectile-based pricing formulas simplify when losses are modeled as scaled shifts of a base distribution.

- Extending the framework to multi-period or multi-peril covers would require checking whether the same boundary conditions continue to guarantee uniqueness.

Load-bearing premise

The policyholder's attitude toward basis risk can be summarized by one fixed weighting parameter that does not change with the loss distribution or the expectile level.

What would settle it

An empirical case in which the utility-maximizing weight changes when the loss distribution or expectile level is altered, while all other model elements stay fixed, would show the boundary-condition characterization does not apply.

Figures

read the original abstract

Parametric insurance contracts translate index measurements to compensation for policyholders' losses using predefined payment schemes. These need to be designed carefully to keep basis risk, i.e. the disparity between payouts and true damages, small. Previous research has motivated the use of conditional expectiles as payment schemes, whose compensation is impacted by the policyholder's potentially unknown attitude towards basis risk. To alleviate this model uncertainty and to investigate the impact of (hidden) influencing factors, we characterize existence and uniqueness of the optimal basis risk weighting in a utility-maximization framework through a set of boundary conditions. In the absence of an optimal solution, we provide comparisons to the utility of no insurance and full indemnity coverage. We establish a link between location-scale distributions and separability of conditional expectiles' derivatives, thus improving the understanding of these statistical functionals. A simulation study on parametric hurricane insurance visualizes our results, investigates the influence of premium loading and risk aversion on the optimal weighting, and comments on the challenge of (spatial) loss dependence.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a utility-maximization framework for selecting the optimal weighting parameter that balances basis risk in expectile-based parametric insurance contracts. It characterizes existence and uniqueness of this optimum via a set of boundary conditions on the policyholder's utility, provides comparisons to no-insurance and full-indemnity utilities when no interior optimum exists, establishes a link between location-scale families and separability of derivatives of conditional expectiles, and illustrates the results with a simulation study on parametric hurricane insurance that examines the roles of premium loading and risk aversion.

Significance. If the boundary-condition characterization holds under the stated modeling assumptions, the work supplies a practical and theoretically grounded method for mitigating model uncertainty about basis-risk attitudes in parametric insurance design. The connection between location-scale distributions and conditional-expectile derivative separability strengthens the statistical foundation for using expectiles in this setting, while the simulation offers concrete guidance on how premium loading and risk aversion affect the optimal weighting. The explicit comparisons to corner solutions (no insurance or full indemnity) are a useful safeguard for cases where an interior optimum does not exist.

major comments (2)

- [§3] §3 (utility-maximization setup and boundary conditions): The claimed characterization of existence and uniqueness assumes that the policyholder's attitude toward basis risk can be captured by a single scalar weighting parameter that is independent of both the loss distribution and the chosen expectile level. The abstract notes a link to location-scale families and separability of conditional-expectile derivatives, but the manuscript must clarify whether the boundary conditions locate a unique optimum only under these restrictions or for arbitrary utilities and distributions; without this, the generality of the result is unclear and the independence assumption becomes load-bearing.

- [Simulation study] Simulation section (hurricane insurance example): The reported effects of premium loading and risk aversion on the optimal weighting are presented numerically, but the manuscript does not supply the exact functional forms of the utility function, the expectile level, or the loss dependence structure used in the Monte Carlo runs. Reproducibility of the visualized results therefore requires these details.

minor comments (3)

- [Abstract] The abstract states that the framework 'characterizes existence and uniqueness... through a set of boundary conditions' but does not indicate whether these conditions are derived from first-order conditions or imposed directly; a brief sentence clarifying this would improve readability.

- [Throughout] Notation for the basis-risk weighting parameter and the conditional expectile should be introduced once and used consistently; occasional switches between Greek letters and descriptive phrases make some passages harder to follow.

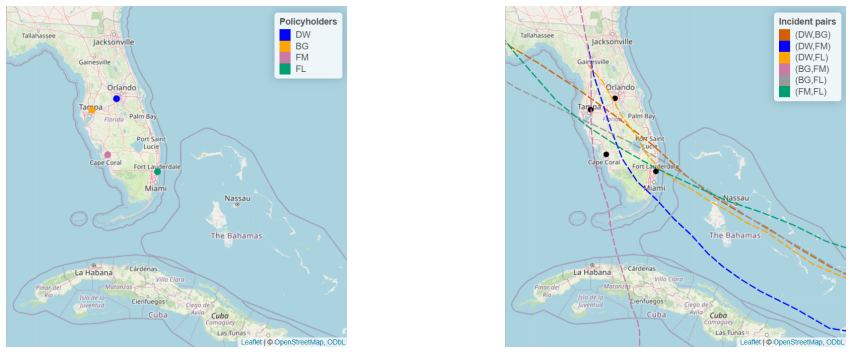

- [Simulation study] The discussion of spatial loss dependence in the simulation would benefit from a short statement on how the dependence structure was calibrated and whether results are robust to alternative copulas.

Simulated Author's Rebuttal

We thank the referee for the positive assessment and constructive comments. We respond point by point to the major comments and indicate planned revisions.

read point-by-point responses

-

Referee: [§3] §3 (utility-maximization setup and boundary conditions): The claimed characterization of existence and uniqueness assumes that the policyholder's attitude toward basis risk can be captured by a single scalar weighting parameter that is independent of both the loss distribution and the chosen expectile level. The abstract notes a link to location-scale families and separability of conditional-expectile derivatives, but the manuscript must clarify whether the boundary conditions locate a unique optimum only under these restrictions or for arbitrary utilities and distributions; without this, the generality of the result is unclear and the independence assumption becomes load-bearing.

Authors: We thank the referee for this observation. The framework models the policyholder's attitude toward basis risk via a single scalar weighting parameter that is independent of the loss distribution and expectile level. The boundary conditions characterize existence and uniqueness of the optimum under this setup. The link to location-scale families is used to establish that separability of the derivatives of conditional expectiles holds for this class of distributions, which supports treating the weighting as independent in those cases. For arbitrary utilities and distributions lacking this separability, the optimal weighting may depend on the distribution and expectile level. We will revise the relevant sections to explicitly state the scope of the boundary conditions and the role of the location-scale assumption. revision: yes

-

Referee: [Simulation study] Simulation section (hurricane insurance example): The reported effects of premium loading and risk aversion on the optimal weighting are presented numerically, but the manuscript does not supply the exact functional forms of the utility function, the expectile level, or the loss dependence structure used in the Monte Carlo runs. Reproducibility of the visualized results therefore requires these details.

Authors: We agree that these details are required for reproducibility. In the revised manuscript we will add the exact functional form of the utility function, the specific expectile level, and the precise loss dependence structure (including any copula or correlation parameters) used in the Monte Carlo simulations. revision: yes

Circularity Check

No significant circularity detected in derivation chain

full rationale

The paper begins with a standard utility-maximization setup that explicitly introduces a single scalar weighting parameter to capture attitude toward basis risk. It then derives boundary conditions characterizing existence and uniqueness of the optimum under that modeling choice, together with an auxiliary result linking location-scale families to separability of conditional-expectile derivatives. These steps are direct mathematical consequences of the stated assumptions and do not reduce the claimed characterization to a fitted quantity, a self-citation, or an unverified ansatz. The framework remains self-contained against external benchmarks; the independence of the weighting parameter from loss law and expectile level is an explicit modeling premise rather than a derived or smuggled result.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Policyholder utility can be expressed as a function of a single basis-risk weighting parameter

- domain assumption Conditional expectiles are well-defined and differentiable for the relevant loss distributions

Reference graph

Works this paper leans on

-

[1]

Parametric insurance market size, 2024

Global Market Insights. Parametric insurance market size, 2024. Accessed on 15th December 2025 viahttps://www.gminsights.com/industry-analysis/ parametric-insurance-market

2024

-

[2]

Parametric solutions

Munich Re. Parametric solutions. Accessed on 7th January 2026 athttps://www. munichre.com/en/solutions/for-industry-clients/parametric-solutions.html

2026

-

[3]

Comprehensive guide to parametric insurance, 2024

Swiss Re. Comprehensive guide to parametric insurance, 2024. Available for down- load athttps://corporatesolutions.swissre.com/alternative-risk-transfer/ parametric-solutions.html

2024

-

[4]

X. Lin and W.J. Kwon. Application of parametric insurance in principle-compliant and innovative ways.Risk Management and Insurance Review, 23(2):121–150, 2020. doi: https://doi.org/10.1111/rmir.12146. URLhttps://onlinelibrary.wiley.com/doi/abs/ 10.1111/rmir.12146

-

[5]

Garcia Ocampo and C

D. Garcia Ocampo and C. Lopez Moreira. Uncertain waters: can paramet- ric insurance help bridge natcat protection gaps?, 2024. ISSN 2522-249X. Accessed on 15th December 2025 viahttps://www.iais.org/uploads/2024/12/ FSI-IAIS-Insights-on-parametric-insurance.pdf

2024

-

[6]

A. Louaas and P. Picard. On the design of optimal parametric insurance.The Geneva Risk and Insurance Review, 2026. ISSN 1554-9658. doi: 10.1057/s10713-026-00113-x. URL https://doi.org/10.1057/s10713-026-00113-x

-

[7]

What is the most popular parametric solution?, 2020

Swiss Re. What is the most popular parametric solution?, 2020. Accessed on 14th October 2025 athttps://corporatesolutions.swissre.com/insights/knowledge/ what-is-the-most-popular-parametric-solution-cat-in-a-box-explained.html

2020

-

[8]

O. Mahul. Optimum Area Yield Crop Insurance.American Journal of Agricultural Economics, 81(1):75–82, 1999. doi: https://doi.org/10.2307/1244451. URLhttps:// onlinelibrary.wiley.com/doi/abs/10.2307/1244451

-

[9]

O. Mahul. Optimal insurance against climatic experience.American Journal of Agricul- tural Economics, 83(3):593–604, 2001. doi: https://doi.org/10.1111/0002-9092.00180. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/0002-9092.00180

-

[10]

O. Mahul and B.D. Wright. Designing optimal crop revenue insurance.American Journal of Agricultural Economics, 85(3):580–589, 2003. doi: https://doi.org/10.1111/1467-8276. 00457. URLhttps://onlinelibrary.wiley.com/doi/abs/10.1111/1467-8276.00457

-

[11]

Bourgeon and R.G

J.-M. Bourgeon and R.G. Chambers. Optimal area-yield crop insurance reconsidered, 2003

2003

-

[12]

J. Zhang, K.S. Tan, and C. Weng. INDEX INSURANCE DESIGN.ASTIN Bulletin, 49 (2):491–523, 2019. doi: 10.1017/asb.2019.5

-

[13]

C. Brown and M. Carriquiry. Managing hydroclimatological risk to water supply with option contracts and reservoir index insurance.Water Resources Research, 43(11), 2007. doi: https://doi.org/10.1029/2007WR006093

-

[14]

C.B. Steinmann, B.P. Guillod, C. Fairless, and D.N. Bresch. A generalized framework for designing open-source natural hazard parametric insurance.Environment Systems and Decisions, 43(4):555–568, 2023. ISSN 2194-5411. doi: 10.1007/s10669-023-09934-x. URL https://doi.org/10.1007/s10669-023-09934-x

-

[15]

M. Stigler and D. Lobell. Optimal index insurance and basis risk decomposition: an appli- cation to Kenya.American Journal of Agricultural Economics, 106(1):306–329, 2024. doi: https://doi.org/10.1111/ajae.12375. URLhttps://onlinelibrary.wiley.com/doi/abs/ 35 10.1111/ajae.12375

-

[16]

M.J. Maier and M. Scherer. Expectiles as basis risk-optimal payment schemes in para- metric insurance.European Actuarial Journal, 2026. ISSN 2190-9741. doi: 10.1007/ s13385-026-00447-w. URLhttps://doi.org/10.1007/s13385-026-00447-w

-

[17]

F. Bellini, V. Bignozzi, and G. Puccetti. Conditional expectiles, time consistency and mixture convexity properties.Insurance: Mathematics and Economics, 82:117–123, 2018. ISSN 0167-6687. doi: https://doi.org/10.1016/j.insmatheco.2018.07.001. URLhttps:// www.sciencedirect.com/science/article/pii/S0167668717303578

-

[18]

Bellini and V

F. Bellini and V. Bignozzi. On elicitable risk measures.Quantitative Finance, 15(5):725–733,

-

[19]

URLhttps://doi.org/10.1080/14697688

doi: 10.1080/14697688.2014.946955. URLhttps://doi.org/10.1080/14697688. 2014.946955

-

[20]

F. Delbaen, F. Bellini, V. Bignozzi, and J.F. Ziegel. Risk measures with the CxLS prop- erty.Finance and Stochastics, 20(2):433–453, 2016. ISSN 1432-1122. doi: 10.1007/ s00780-015-0279-6. URLhttps://doi.org/10.1007/s00780-015-0279-6

-

[21]

J.F. Ziegel. Coherence and elicitability.Mathematical Finance, 26(4):901–918, 2016. doi: https://doi.org/10.1111/mafi.12080

-

[22]

F. Bellini, B. Klar, A. M¨ uller, and E. Rosazza Gianin. Generalized quantiles as risk mea- sures.Insurance: Mathematics and Economics, 54:41–48, 2014. ISSN 0167-6687. doi: https://doi.org/10.1016/j.insmatheco.2013.10.015. URLhttps://www.sciencedirect. com/science/article/pii/S0167668713001698

-

[23]

S. Girard, G. Stupfler, and A. Usseglio-Carleve. Nonparametric extreme conditional ex- pectile estimation.Scandinavian Journal of Statistics, 49(1):78–115, 2022. doi: https: //doi.org/10.1111/sjos.12502

-

[24]

Daouia, S

A. Daouia, S. Girard, and G. Stupfler. Estimation of Tail Risk Based on Extreme Expectiles. Journal of the Royal Statistical Society Series B: Statistical Methodology, 80(2):263–292,

- [25]

-

[26]

Bloemendaal, I.D

N. Bloemendaal, I.D. Haigh, H. de Moel, S. Muis, R.J. Haarsma, and J.C.J.H. Aerts. Storm ibtracs present climate synthetic tropical cyclone tracks, 2022. Version 4. 4TU.ResearchData. dataset

2022

-

[27]

W.K. Newey and J.L. Powell. Asymmetric Least Squares Estimation and Testing.Econo- metrica, 55(4):819–847, 1987. ISSN 00129682, 14680262. URLhttp://www.jstor.org/ stable/1911031

-

[28]

M.C. Jones. Expectiles and m-quantiles are quantiles.Statistics & Probability Letters, 20 (2):149–153, 1994. ISSN 0167-7152. doi: https://doi.org/10.1016/0167-7152(94)90031-0. URLhttps://www.sciencedirect.com/science/article/pii/0167715294900310

-

[29]

F. Bellini, B. Klar, and A. M¨ uller. Expectiles, Omega Ratios and Stochastic Ordering. Methodology and Computing in Applied Probability, 20(3):855–873, 2018. ISSN 1573-7713. doi: 10.1007/s11009-016-9527-2. URLhttps://doi.org/10.1007/s11009-016-9527-2

-

[30]

C. De Vecchi and M. Scherer. On expectiles and almost stochastic dominance.In- surance: Mathematics and Economics, 126:103179, 2026. ISSN 0167-6687. doi: https: //doi.org/10.1016/j.insmatheco.2025.103179. URLhttps://www.sciencedirect.com/ science/article/pii/S016766872500126X

-

[31]

A. Daouia, G. Stupfler, and A. Usseglio-Carleve. An expectile computation cook- book.Statistics and Computing, 34(3):103, 2024. ISSN 1573-1375. doi: 10.1007/ s11222-024-10403-x. URLhttps://doi.org/10.1007/s11222-024-10403-x

-

[32]

R.M. Corless, G.H. Gonnet, D.E.G. Hare, D.J. Jeffrey, and D.E. Knuth. On the lambert w 36 function.Advances in Computational Mathematics, 5(1):329–359, 1996. ISSN 1572-9044. doi: 10.1007/BF02124750

-

[33]

N.D. Jensen, A.G. Mude, and C.B. Barrett. How basis risk and spatiotemporal adverse selection influence demand for index insurance: Evidence from northern kenya.Food Pol- icy, 74:172–198, 2018. ISSN 0306-9192. doi: https://doi.org/10.1016/j.foodpol.2018.01.002. URLhttps://www.sciencedirect.com/science/article/pii/S0306919217301392

-

[34]

M.E. Batts, E. Simiu, and L.R. Russell. Hurricane wind speeds in the united states.Journal of the Structural Division, 106(10):2001–2016, 1980. doi: 10.1061/JSDEAG.0005541. URL https://ascelibrary.org/doi/abs/10.1061/JSDEAG.0005541

-

[35]

Vickery and L.A

P.J. Vickery and L.A. Twisdale. Prediction of hurricane wind speeds in the united states.Journal of Structural Engineering, 121(11):1691–1699, 1995. doi: 10.1061/ (ASCE)0733-9445(1995)121:11(1691). URLhttps://ascelibrary.org/doi/abs/10. 1061/(ASCE)0733-9445(1995)121:11(1691)

1995

-

[36]

P.J. Vickery, P.F. Skerlj, and L.A. Twisdale. Simulation of Hurricane Risk in the U.S. Using Empirical Track Model.Journal of Structural Engineering, 126(10):1222–1237, 2000. doi: 10.1061/(ASCE)0733-9445(2000)126:10(1222). URLhttps://ascelibrary.org/doi/ abs/10.1061/(ASCE)0733-9445(2000)126:10(1222)

-

[37]

R. Snaiki and T. Wu. Revisiting hurricane track model for wind risk assessment. Structural Safety, 87:102003, 2020. ISSN 0167-4730. doi: https://doi.org/10.1016/j. strusafe.2020.102003. URLhttps://www.sciencedirect.com/science/article/pii/ S0167473020300825

work page doi:10.1016/j 2020

-

[38]

N. Bloemendaal, I.D. Haigh, H. de Moel, S. Muis, R.J. Haarsma, and J.C.J.H. Aerts. Generation of a global synthetic tropical cyclone hazard dataset using storm.Scientific Data, 7(1):40, 2020. ISSN 2052-4463. doi: 10.1038/s41597-020-0381-2. URLhttps://doi. org/10.1038/s41597-020-0381-2

-

[39]

K. Gade. A non-singular horizontal position representation.Journal of Navigation, 63(3): 395–417, 2010. doi: 10.1017/S0373463309990415

-

[40]

B. Efron. Bootstrap methods: Another look at the jackknife.The Annals of Statistics, 7 (1):1–26, 1979

1979

-

[41]

Tibshirani and B

R.J. Tibshirani and B. Efron.An introduction to the bootstrap. Chapman & Hall, 1993

1993

-

[42]

Snaiki and S.S

R. Snaiki and S.S. Parida. Climate change effects on loss assessment and mitigation of residential buildings due to hurricane wind.Journal of Building Engineering, 69:106256,

-

[43]

doi: https://doi.org/10.1016/j.jobe.2023.106256

ISSN 2352-7102. doi: https://doi.org/10.1016/j.jobe.2023.106256. URLhttps:// www.sciencedirect.com/science/article/pii/S2352710223004357

-

[44]

E. Benami, Z. Jin, M.R. Carter, A. Ghosh, R.J. Hijmans, A. Hobbs, B. Kenduiywo, and D.B. Lobell. Uniting remote sensing, crop modelling and economics for agricultural risk man- agement.Nature Reviews Earth & Environment, 2(2):140–159, 2021. ISSN 2662-138X. doi: 10.1038/s43017-020-00122-y. URLhttps://doi.org/10.1038/s43017-020-00122-y

-

[45]

S. Chatterjee. A new coefficient of correlation.Journal of the American Statistical As- sociation, 116(536):2009–2022, 2021. doi: 10.1080/01621459.2020.1758115. URLhttps: //doi.org/10.1080/01621459.2020.1758115

-

[46]

R. Schmidt and U. Stadtm¨ uller. Non-parametric estimation of tail dependence.Scan- dinavian Journal of Statistics, 33(2):307–335, 2006. doi: https://doi.org/10.1111/j. 1467-9469.2005.00483.x. URLhttps://onlinelibrary.wiley.com/doi/abs/10.1111/j. 1467-9469.2005.00483.x

work page doi:10.1111/j 2006

-

[47]

R.H. Jerry. Understanding parametric insurance: A potential tool to help manage pandemic 37 risk. In M.L. Mu˜ noz Paredes and A. Tarasiuk, editors,Covid-19 and Insurance, pages 17–

-

[48]

ISBN 978-3-031-13753-2

Springer International Publishing, Cham, 2023. ISBN 978-3-031-13753-2. doi: 10.1007/ 978-3-031-13753-2 2

2023

-

[49]

Nelsen.An Introduction to Copulas

R.B. Nelsen.An Introduction to Copulas. Springer New York, New York, NY, 2006. ISBN 978-0-387-28678-5. doi: 10.1007/0-387-28678-0. URLhttps://doi.org/10.1007/ 0-387-28678-0. 38

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.