Recognition: unknown

Modeling dependency between operational risk losses and macroeconomic variables using Hidden Markov Models

Pith reviewed 2026-05-08 12:56 UTC · model grok-4.3

The pith

An extended hidden Markov model uses an auxiliary variable to model how operational risk losses depend on macroeconomic variables.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

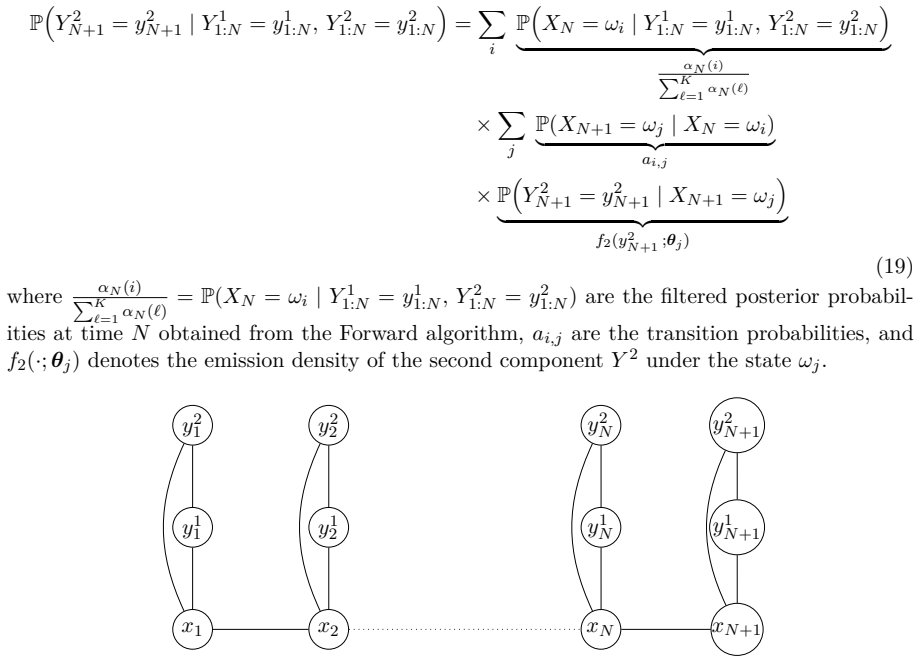

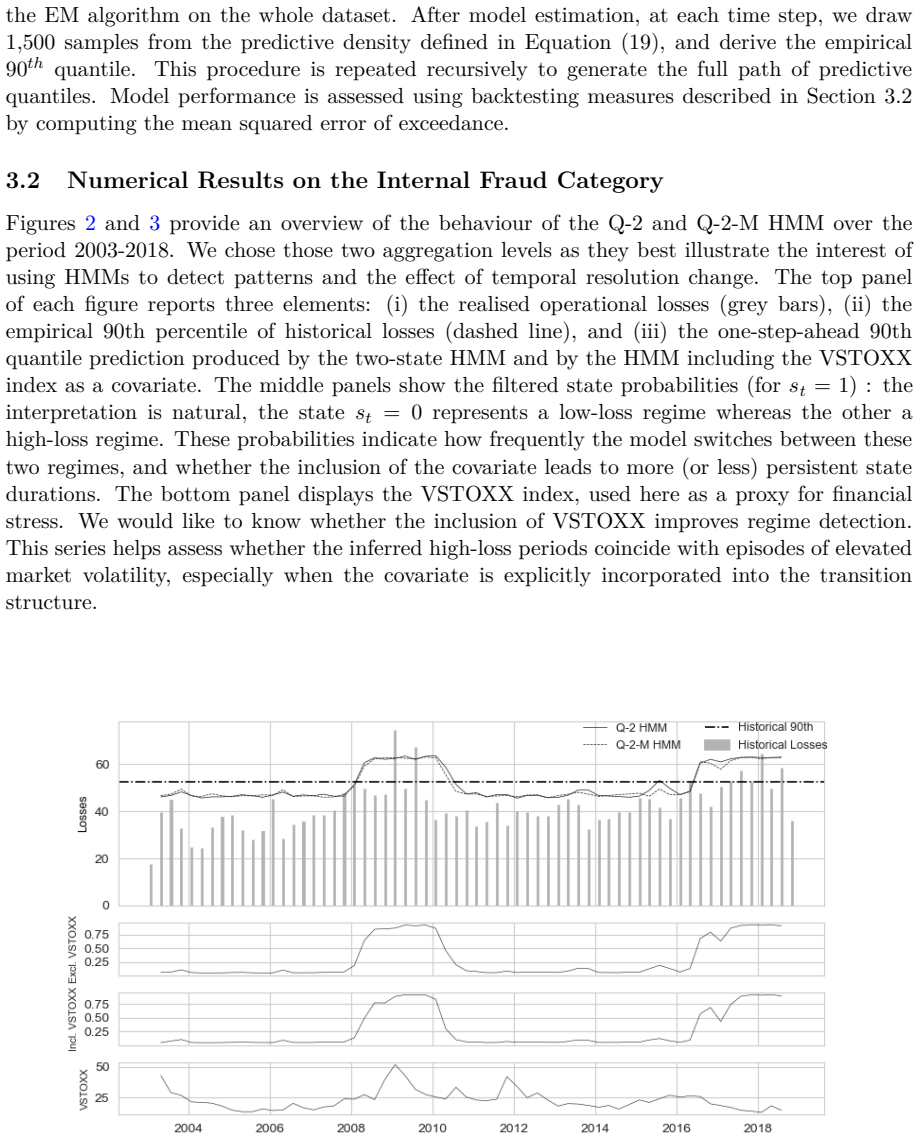

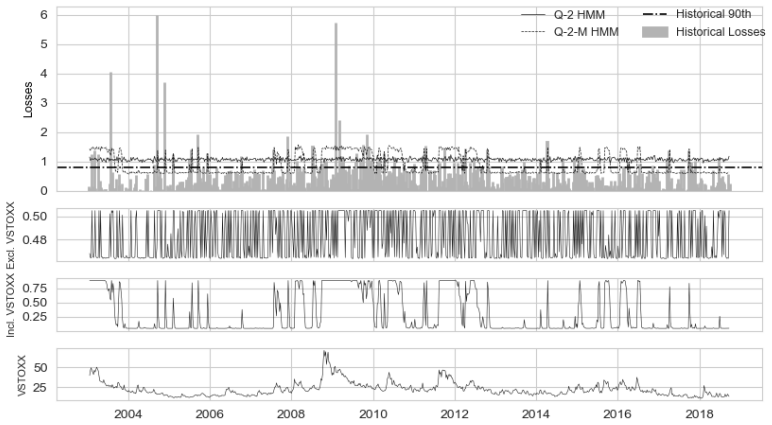

The authors introduce an extension of hidden Markov models for multivariate time-series data that adds an auxiliary variable to account for economic covariates. This allows the model to represent dependencies between operational risk losses and macroeconomic variables. The calibration is performed with the EM algorithm, and the results for various risk-event types demonstrate the relevance of the macroeconomic covariates.

What carries the argument

An extended hidden Markov model with a third auxiliary variable that accommodates economic covariates in the time-series observations.

If this is right

- The model can represent the heterogeneous and time-dependent dependencies in operational risk data.

- Calibration via the EM algorithm yields parameters suitable for different risk event types.

- Including macroeconomic covariates enhances the model's ability to support stress test exercises.

- The approach provides a way to analyze the relationship between losses and economic conditions over time.

Where Pith is reading between the lines

- Similar extensions could apply to other risk types like credit risk where macro factors play a role.

- Testing the model on out-of-sample data would verify its predictive power for future losses.

- Integration with existing bank risk systems might allow real-time stress scenario analysis.

Load-bearing premise

The extended hidden Markov model structure with the auxiliary variable can adequately capture the heterogeneous, time-dependent dependencies between operational risk losses and macroeconomic variables, with the EM algorithm producing reliable parameter estimates.

What would settle it

Observing that the fitted model fails to improve the likelihood or predictive accuracy on new operational risk data compared to a standard hidden Markov model without the auxiliary variable would indicate the extension does not add value.

Figures

read the original abstract

Predicting future operational risk losses gives rise to a significant challenge due to the heterogeneous and time-dependent structures present in real-world data. Furthermore, stress test exercises require examining the relationship with operational losses. To capture such relationship, we propose to use an extension of Hidden Markov Models to multivariate observations. This model introduces a third auxiliary variable designed to accommodate the economic covariates in the time-series data. We detail the unique aspects of operational risk data and describe how model calibration is achieved via the Expectation-Maximization (EM) algorithm. Additionally, we provide the calibration results for the various risk-event types and analyze the relevance of the inclusion of the macroeconomic covariates.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes an extension of Hidden Markov Models to multivariate observations for capturing dependencies between operational risk losses and macroeconomic variables. It introduces a third auxiliary variable to accommodate economic covariates in the time-series data, details unique aspects of operational risk data, calibrates the model via the Expectation-Maximization algorithm, and presents calibration results for various risk-event types along with an analysis of the relevance of the macroeconomic covariates.

Significance. If the auxiliary-variable construction demonstrably improves representation of heterogeneous, time-dependent loss-macro relationships, the work would offer a structured approach to incorporating macroeconomic drivers into operational risk modeling, with direct relevance to stress-testing exercises. The use of standard EM calibration on real risk-event types provides a concrete starting point, though the absence of comparative benchmarks currently limits the assessed impact.

major comments (2)

- [Calibration results and parameter analysis] The central claim that the auxiliary variable produces a faithful representation of time-varying, heterogeneous dependencies requires evidence beyond in-sample parameter examination. The calibration results section reports EM fits and transition probabilities across risk-event types but provides no out-of-sample log-likelihood, no predictive scores, and no direct comparison against a baseline multivariate HMM without the auxiliary variable; this leaves open whether the auxiliary state improves fit or merely absorbs noise.

- [Model description] The model construction in the HMM extension section defines the auxiliary variable to accommodate economic covariates, yet the manuscript does not derive or test why this third variable is necessary rather than extending the emission distribution directly or using a standard multivariate HMM; without such justification or ablation, the load-bearing role of the auxiliary variable for the dependency claim remains unestablished.

minor comments (2)

- [Model description] Notation for the auxiliary variable and its integration into the emission and transition probabilities should be clarified with explicit equations to avoid ambiguity in the multivariate observation model.

- [Abstract] The abstract and introduction would benefit from a brief statement of the data sources, time span, and number of observations used in the calibration to allow readers to assess applicability to typical operational risk series.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which help clarify the validation needs for our proposed HMM extension. We address each major comment below, agreeing that additional evidence would strengthen the claims, and outline the planned revisions.

read point-by-point responses

-

Referee: The central claim that the auxiliary variable produces a faithful representation of time-varying, heterogeneous dependencies requires evidence beyond in-sample parameter examination. The calibration results section reports EM fits and transition probabilities across risk-event types but provides no out-of-sample log-likelihood, no predictive scores, and no direct comparison against a baseline multivariate HMM without the auxiliary variable; this leaves open whether the auxiliary state improves fit or merely absorbs noise.

Authors: We agree that the manuscript's current focus on in-sample EM calibration and parameter analysis leaves the improvement attributable to the auxiliary variable unquantified. In the revised version we will add out-of-sample log-likelihood comparisons, predictive scores on held-out periods, and a direct benchmark against a standard multivariate HMM without the auxiliary variable. These additions will be placed in a new subsection of the calibration results. revision: yes

-

Referee: The model construction in the HMM extension section defines the auxiliary variable to accommodate economic covariates, yet the manuscript does not derive or test why this third variable is necessary rather than extending the emission distribution directly or using a standard multivariate HMM; without such justification or ablation, the load-bearing role of the auxiliary variable for the dependency claim remains unestablished.

Authors: The auxiliary variable is introduced to let the shared hidden chain govern regime-dependent dependence between losses and covariates while keeping their conditional distributions separate; a direct multivariate emission or standard HMM does not isolate this regime-switching dependence in the same way. We will insert a short derivation subsection explaining this choice and include an ablation study comparing the full model to the two alternatives mentioned. revision: yes

Circularity Check

No significant circularity: standard HMM extension and EM calibration

full rationale

The manuscript proposes an extension of Hidden Markov Models that adds an auxiliary variable to incorporate macroeconomic covariates, then applies the standard Expectation-Maximization algorithm for calibration on operational-risk time series. Calibration results and parameter analysis for different risk-event types are reported, but no derivation step reduces a claimed prediction or uniqueness result to a fitted quantity by construction, nor does any load-bearing premise rest on a self-citation chain. The model structure is introduced explicitly rather than defined in terms of its own outputs, and EM is invoked as the conventional estimation procedure without renaming fitted parameters as independent predictions. The paper therefore remains self-contained against external benchmarks and does not exhibit any of the enumerated circularity patterns.

Axiom & Free-Parameter Ledger

free parameters (1)

- transition and emission parameters

axioms (2)

- domain assumption Hidden states follow a first-order Markov chain

- domain assumption Observations are conditionally independent given hidden states and auxiliary variable

invented entities (1)

-

auxiliary variable for economic covariates

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Bae, T. and A. Kreinin (2017, January). A backward construction and simulation of corre- lated poisson processes.Journal of Statistical Computation and Simulation 87, 1–15

2017

-

[2]

An explanatory note on the Basel II IRB risk weight functions

Basel Committee on Banking Supervision (2005). An explanatory note on the Basel II IRB risk weight functions. Retrieved on July 19, 2021 onhttps://www.bis.org/bcbs/ irbriskweight.htm

2005

-

[3]

International convergence of capital mea- surement and capital standards: A revised framework — comprehensive version

Basel Committee on Banking Supervision (2006). International convergence of capital mea- surement and capital standards: A revised framework — comprehensive version

2006

-

[4]

Basel III: A global regulatory framework for more resilient banks and banking systems

Basel Committee on Banking Supervision (2011). Basel III: A global regulatory framework for more resilient banks and banking systems

2011

-

[5]

Finalising Basel III: In brief

Basel Committee on Banking Supervision (2017). Finalising Basel III: In brief

2017

-

[6]

Cr´ epey, S

Bastide, D., S. Cr´ epey, S. Drapeau, and M. Tadese (2023). Derivatives risks as costs in a one-period network model.Frontiers of Mathematical Finance 2(3), 283–312

2023

-

[7]

(2016).Stress Testing and Risk Integration in Banks: A Statistical Framework and Practical Software Guide(1 ed.)

Bellini, T. (2016).Stress Testing and Risk Integration in Banks: A Statistical Framework and Practical Software Guide(1 ed.). Elsevier

2016

-

[8]

Bishop, C. M. (2006).Pattern Recognition and Machine Learning. New York: Springer

2006

-

[9]

B¨ ocker, K. and C. Kl¨ uppelberg (2010, October). Multivariate models for operational risk. Quantitative Finance 10, 855–869

2010

-

[10]

Moulines, and T

Capp´ e, O., E. Moulines, and T. Ryden (2005).Inference in Hidden Markov Models. Springer Series in Statistics. New York: Springer

2005

-

[11]

Embrechts, and M

Chavez-Demoulin, V., P. Embrechts, and M. Hofert (2016). An extreme value approach for modeling operational risk losses depending on covariates.Journal of Risk and Insurance 83(3), 735–776

2016

-

[12]

Chernobai, A. S., S. T. Rachev, and F. J. Fabozzi (2011).Operational Risk: A Guide to Basel II Capital Requirements, Models, and Analysis. Hoboken, NJ: Wiley. 17

2011

-

[13]

Jackson, and A

Chiu, M., K. Jackson, and A. Kreinin (2017, February). Correlated multivariate poisson processes and extreme measures.Model Assisted Statistics and Applications 12

2017

-

[14]

Cope, E. W., M. T. Piche, and J. S. Walter (2012). Macroenvironmental determinants of operational losses.Journal of Banking & Finance 36(5), 1362–1380

2012

-

[15]

Galai, and R

Crouhy, M., D. Galai, and R. Mark (2014).The essentials of Risk Management, second edition. New York: McGraw Hill

2014

-

[16]

Cruz, M. G., G. W. Peters, and P. V. Shevchenko (2015).Fundamental Aspects of Opera- tional Risk and Insurance Analytics: A Handbook of Operational Risk. John Wiley & Sons, Ltd

2015

-

[17]

Dionne, G. and S. Saissi Hassani (2016). Hidden markov regimes in operational loss data: Application to the 2007–2009 financial crisis.CIRRELT

2016

-

[18]

Jiang, and A

Duch, K., Y. Jiang, and A. Kreinin (2014, July). New approaches to operational risk modeling.IBM Journal of Research and Development 58(3), 3:1–3:9

2014

-

[19]

2021 eu-wide stress test – methodological note

European Banking Authority (2021, January). 2021 eu-wide stress test – methodological note. Retrieved on July 19, 2021 onhttps://www.eba.europa.eu/ eba-launches-2021-eu-wide-stress-test-exercise

2021

-

[20]

Stress-test analytics for macro- prudential purposes in the euro area

European Central Bank (2017, February). Stress-test analytics for macro- prudential purposes in the euro area. Retrieved on April 26, 2025 onhttps: //www.ecb.europa.eu/press/conferences/shared/pdf/20170511_2nd_mp_policy/ DeesHenryMartin-Stampe-Stress-Test_Analytics_for_Macroprudential_Purposes_ in_the_euro_area.en.pdf

-

[21]

Fiordelisi, F., M. G. Soana, and P. Schwizer (2014). The determinants of reputational risk in the banking sector.Journal of Banking & Finance 37(5), 1359–1371

2014

-

[22]

Fung, T. C., A. L. Badescu, and X. S. Lin (2019). Multivariate cox hidden markov models with an application to operational risk.Scandinavian Actuarial Journal 2019(2), 93–118

2019

-

[23]

Hambuckers, J. and T. Kneib (2018). A markov-switching generalized additive model for compound poisson processes, with applications to operational loss models.Journal of Business & Economic Statistics 36(4), 610–622

2018

-

[24]

Hess, C. (2011). The impact of the financial crisis on operational risk in banks.Journal of Operational Risk 6(1), 23–35

2011

-

[25]

(2011).Financial Risk Manager Handbook

Jorion, P. (2011).Financial Risk Manager Handbook. New Jersey: Wiley

2011

-

[26]

(2017, December)

Kreinin, A. (2017, December). Correlated poisson processes

2017

-

[27]

Lindskog, F. and A. J. McNeil (2003). Common poisson shock models: Applications to insurance and credit risk.ASTIN Bulletin: The Journal of the IAA 33(2), 209–238

2003

-

[28]

McLachlan, G. J. and D. Peel (2000).Finite Mixture Models. Wiley Series in Probability and Statistics. New York: Wiley

2000

-

[29]

McNeil, A. J., R. Frey, and P. Embrechts (2015).Quantitative Risk Management: Concepts, Techniques and Tools(Revised ed.). Princeton, NJ: Princeton University Press

2015

-

[30]

Murphy, K. P. (2012).Machine Learning: A Probabilistic Perspective. Cambridge, MA: MIT Press

2012

-

[31]

Rabiner, L. R. (1989). A tutorial on hidden markov models and selected applications in speech recognition.Proceedings of the IEEE 77(2), 257–286

1989

-

[32]

(2016, December)

Tankov, P. (2016, December). L´ evy copulas: Review of recent results. 18

2016

-

[33]

(2019, October)

Tankov, P. (2019, October). Simulation and option pricing in l´ evy copula models

2019

-

[34]

Tukey, J. W. (1977).Exploratory Data Analysis. Reading, MA: Addison-Wesley

1977

-

[35]

Brady, and S

Zhang, Y., M. Brady, and S. Smith (2001). Segmentation of brain mr images through a hidden markov random field model and the expectation–maximization algorithm.IEEE Transactions on Medical Imaging 20(1), 45–57. 19

2001

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.