Recognition: unknown

Beyond Picking Winners: Correlation-Driven Tail Risk in Venture Capital Portfolio Construction

Pith reviewed 2026-05-08 07:02 UTC · model grok-4.3

The pith

Deal correlations in venture capital preserve expected success rates but create more extreme high-outcome portfolios.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

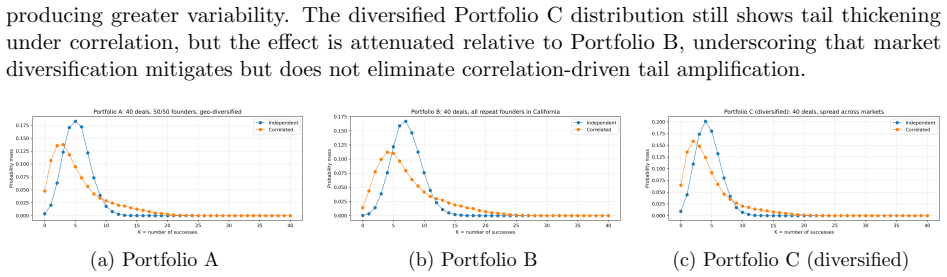

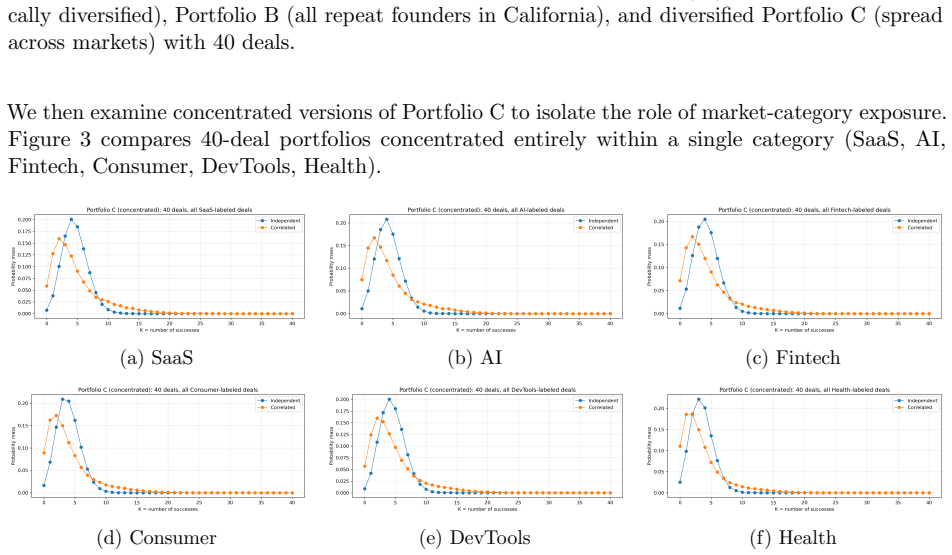

Holding marginal deal success probabilities fixed, deal-level correlation preserves expected portfolio outcomes but shifts the portfolio distribution toward heavier right tails and higher kurtosis. In portfolio simulations, correlation reduces the probability of modest success counts while sharply amplifying extreme upside outcomes, especially in structurally concentrated portfolios. The findings suggest that extreme venture capital outcomes may partly reflect correlation-induced tail amplification rather than solely higher average deal quality.

What carries the argument

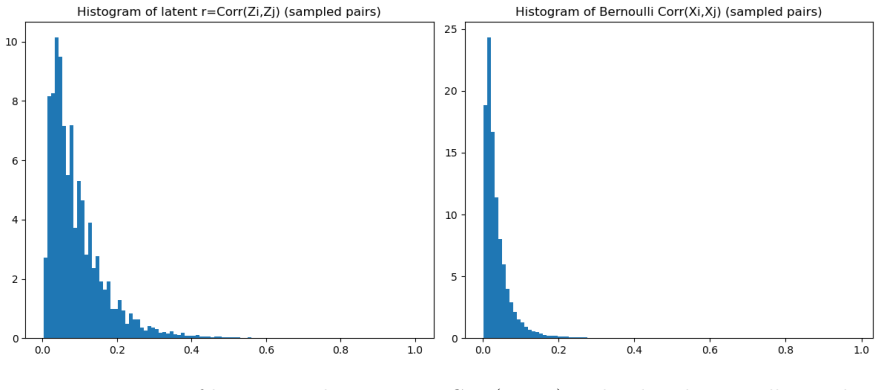

Gaussian-copula-based framework that learns deal-level dependence directly from observed joint success frequencies across founder, geography, and market attributes.

If this is right

- Correlation reduces the probability of modest success counts while amplifying extreme upside outcomes.

- The tail effect becomes stronger in structurally concentrated portfolios.

- Extreme VC outcomes can arise from dependence structure rather than from higher average deal quality.

- Portfolio construction and risk management should account for dependence-induced shape changes in addition to marginal probabilities.

Where Pith is reading between the lines

- Managers could deliberately seek or avoid certain attribute overlaps to control the probability of outlier portfolio results.

- The same mechanism might apply to other asset classes where deals or projects share observable attributes and exhibit positive dependence.

- Testing whether real-world VC portfolio outcome distributions match the simulated correlated versus independent cases would provide direct empirical validation.

Load-bearing premise

The Gaussian copula fitted to joint success frequencies in the selected dataset accurately reflects the true underlying dependence among deals.

What would settle it

A dataset of many actual VC portfolios in which the observed variance and kurtosis of success counts match those produced by independent draws at the same marginal success rates would falsify the tail-amplification claim.

Figures

read the original abstract

We propose a Gaussian-copula-based framework that learns deal-level dependence directly from observed joint success frequencies across founder, geography, and market attributes. Holding marginal deal success probabilities fixed, deal-level correlation preserves expected portfolio outcomes but shifts the portfolio distribution toward heavier right tails and higher kurtosis. In portfolio simulations, correlation reduces the probability of modest success counts while sharply amplifying extreme upside outcomes, especially in structurally concentrated portfolios. Our findings suggest that extreme venture capital outcomes may partly reflect correlation-induced tail amplification rather than solely higher average deal quality, with potential implications for portfolio construction and risk management. We note that the observed dataset reflects selected deals with observable outcomes, which inflates apparent success rates relative to the true population base rate; however, the core finding that correlation reshapes the distributional shape while leaving the mean unchanged is structurally robust to the level of marginal success probabilities.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a Gaussian-copula framework that estimates deal-level dependence from observed joint success frequencies across founder, geography, and market attributes in a selected VC dataset. Holding marginal success probabilities fixed, the model shows that positive correlations leave expected portfolio success counts unchanged while shifting the distribution toward heavier right tails, higher kurtosis, and amplified extreme upside outcomes, especially in concentrated portfolios. Simulations illustrate reduced probability of modest success counts under correlation. The authors acknowledge that the data reflect only observable, already-selected deals (inflating apparent success rates) but assert that the mean-invariance result is structurally robust to marginal levels.

Significance. If the fitted dependence structure holds, the work provides a clean separation of marginal quality from correlation-driven tail effects, with direct implications for VC portfolio construction and risk management. The structural result—that copula dependence preserves the mean while reshaping higher moments—is a methodological strength, as it follows directly from the construction without additional assumptions. This could inform diversification strategies by quantifying how correlation amplifies extreme outcomes beyond average deal quality.

major comments (2)

- [Abstract and Methods] Abstract and Methods: The manuscript provides no details on the copula parameter estimation procedure (e.g., how joint success frequencies are converted to correlation parameters), any validation against hold-out data, sensitivity checks, or error quantification. This omission makes it difficult to assess whether the reported tail shifts are robust or artifacts of the fitting process on the selected sample.

- [Simulation Results] Simulation setup and results: Although the mean-invariance result is structural and independent of specific fitted values, the magnitude and direction of the right-tail amplification and kurtosis increase are sensitive to the Gaussian copula choice (which imposes zero upper-tail dependence) and the absence of selection-bias corrections. No comparisons to alternative copulas or adjusted marginals are reported, undermining claims about the practical size of the tail effect in real VC portfolios.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments on our manuscript. We address each major comment below and indicate the specific revisions planned for the next version.

read point-by-point responses

-

Referee: [Abstract and Methods] Abstract and Methods: The manuscript provides no details on the copula parameter estimation procedure (e.g., how joint success frequencies are converted to correlation parameters), any validation against hold-out data, sensitivity checks, or error quantification. This omission makes it difficult to assess whether the reported tail shifts are robust or artifacts of the fitting process on the selected sample.

Authors: We agree that the current manuscript lacks sufficient detail on the estimation procedure. In the revised version we will expand the Methods section with an explicit description of how observed joint success frequencies are mapped to the Gaussian copula correlation parameters, including the pairwise conversion step and any regularization applied. We will also add sensitivity checks that vary the fitted correlations within bootstrap-derived intervals and report the resulting changes in tail probabilities and kurtosis. Error quantification via resampling of the frequency counts will be included. Hold-out validation is not feasible with the present dataset size and structure; we will state this limitation explicitly and note that future work with larger samples could address it. These additions will allow readers to evaluate the robustness of the reported tail shifts. revision: yes

-

Referee: [Simulation Results] Simulation setup and results: Although the mean-invariance result is structural and independent of specific fitted values, the magnitude and direction of the right-tail amplification and kurtosis increase are sensitive to the Gaussian copula choice (which imposes zero upper-tail dependence) and the absence of selection-bias corrections. No comparisons to alternative copulas or adjusted marginals are reported, undermining claims about the practical size of the tail effect in real VC portfolios.

Authors: We acknowledge that the Gaussian copula imposes zero upper-tail dependence and that this choice affects the precise magnitude of extreme outcomes. The Gaussian specification was selected because it directly incorporates the empirically estimated linear correlations without additional parameters. The mean-invariance property is structural and holds for any copula; the directional tail amplification under positive correlation is likewise preserved, though its size varies with the dependence structure. In the revision we will add a short discussion of this modeling choice and include a limited comparison using a Student-t copula with low degrees of freedom to illustrate sensitivity. For selection bias, the data contain only funded deals with observed outcomes, precluding direct population-level marginal adjustment. We will emphasize that the qualitative reshaping of the distribution remains robust when marginal success probabilities are lowered, and we will report additional simulations under reduced marginals to demonstrate this. These changes will better bound the practical size of the tail effect. revision: partial

Circularity Check

Mean preservation follows from linearity of expectation with fixed marginals; tail effects are model consequences

specific steps

-

self definitional

[Abstract]

"Holding marginal deal success probabilities fixed, deal-level correlation preserves expected portfolio outcomes but shifts the portfolio distribution toward heavier right tails and higher kurtosis."

The 'preserves expected portfolio outcomes' clause is true by construction for any dependence structure (including the Gaussian copula) once marginals are fixed, via linearity of expectation: E[sum X_i] = sum E[X_i] regardless of correlation. It is not derived from the fitted joint frequencies, the simulations, or any external principle but is tautological given the setup.

full rationale

The paper's core structural claim—that fixing marginal success probabilities while introducing deal-level correlation via Gaussian copula leaves E[portfolio successes] unchanged but alters higher moments—is presented as a derived result. However, the invariance of the mean is a direct mathematical identity (linearity of expectation) that holds for any joint distribution with those marginals and requires no fitting, simulation, or copula. The tail amplification is a non-trivial but expected consequence of positive dependence in the chosen copula family. No load-bearing step reduces the central finding to a self-citation chain or renames a fitted quantity as an independent prediction; the framework is self-contained once the modeling assumptions are granted. This yields low but non-zero circularity from the rhetorical framing of a built-in identity as a 'finding.'

Axiom & Free-Parameter Ledger

free parameters (1)

- deal-level correlation parameters

axioms (1)

- domain assumption Gaussian copula adequately captures the dependence structure among binary deal success indicators.

Reference graph

Works this paper leans on

-

[1]

Buchner, A., Mohamed, A., and Schwienbacher, A. (2017). Diversification, risk, and returns in venture capital.Journal of Business Venturing, 32(5):519–535

2017

-

[2]

Cochrane, J. H. (2005). The risk and return of venture capital.Journal of Financial Economics, 75(1):3–52

2005

-

[3]

and McNeil, A

Frey, R. and McNeil, A. J. (2003). Dependent defaults in models of portfolio credit risk.Journal of Risk, 6(1):59–92

2003

-

[4]

Gordy, M. B. (2003). A risk-factor model foundation for ratings-based bank capital rules.Journal of Financial Intermediation, 12(3):199–232

2003

-

[5]

and Nagel, S

Korteweg, A. and Nagel, S. (2016). Risk-adjusting the returns to venture capital.The Journal of Finance, 71(3):1437–1470

2016

-

[6]

Koyluoglu, H. U. and Hickman, A. (1998). Reconcilable differences.Risk, 11:56–62

1998

-

[7]

Li, D. X. (2000). On default correlation: A copula function approach.Journal of Fixed Income, 9(4):43–54

2000

-

[8]

Nelsen, R. B. (2006).An Introduction to Copulas. Springer, New York, 2 edition

2006

-

[9]

Oh, D. H. and Patton, A. J. (2017). Modeling dependence in high dimensions with factor copulas. Journal of Business & Economic Statistics, 35(1):139–154

2017

-

[10]

Sklar, A. (1959). Fonctions de r´ epartition ` a n dimensions et leurs marges.Publications de l’Institut de Statistique de l’Universit´ e de Paris, 8:229–231

1959

-

[11]

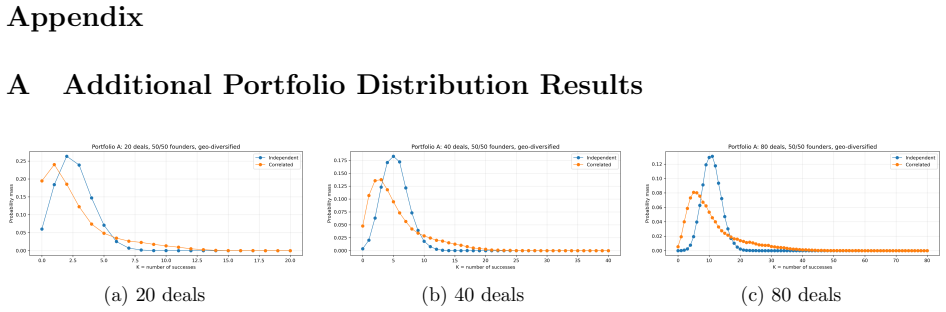

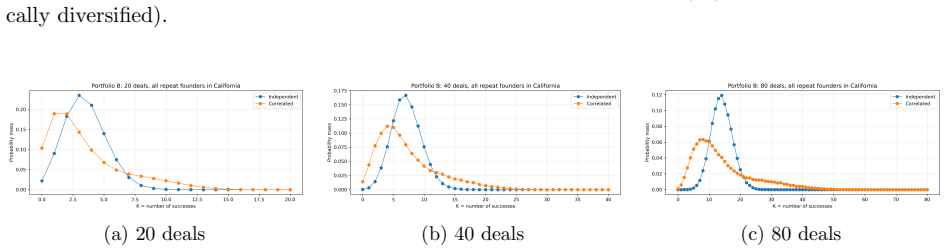

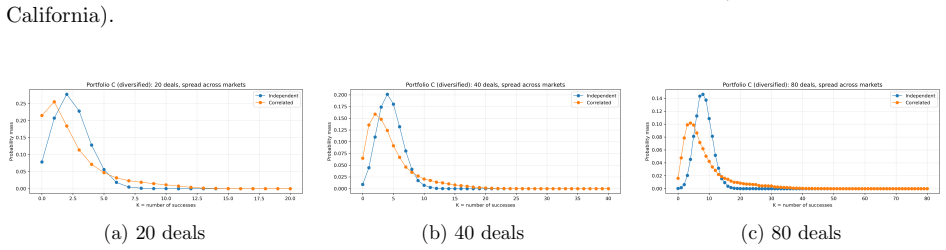

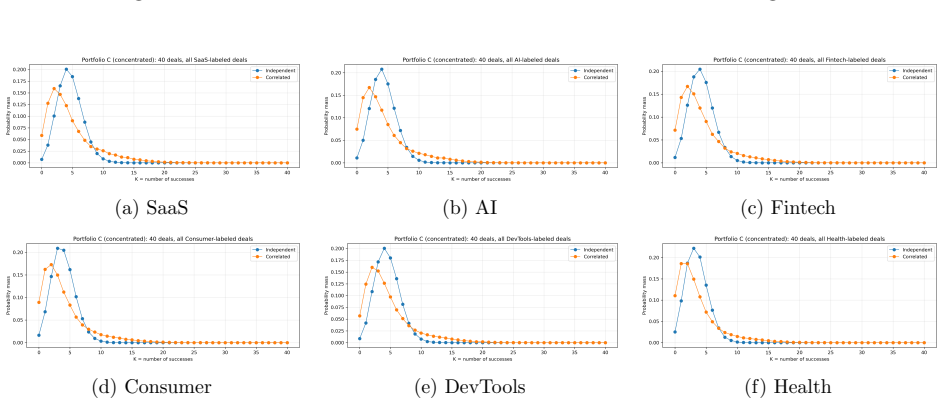

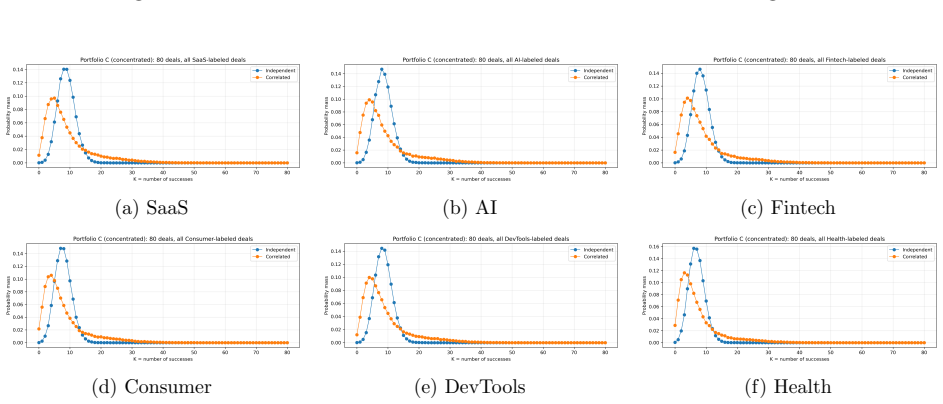

Teti, E., Dell’Acqua, A., and Bovsunovsky, A. (2024). Diversification and size in venture capital investing.Eurasian Business Review, 14(2):475–500. 15 Appendix A Additional Portfolio Distribution Results (a) 20 deals (b) 40 deals (c) 80 deals Figure 4: Distribution of the number of successful deals for Portfolio A (50/50 founders, geographi- cally divers...

2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.