Recognition: unknown

Misspecification-Averse Estimation

Pith reviewed 2026-05-08 07:03 UTC · model grok-4.3

The pith

Optimal estimators under likelihood misspecification are Bayes rules using an exponentially tilted likelihood with moment constraints.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Within a broad class of axiomatically grounded optimality criteria for misspecification-averse estimation, the constrained multiplier criterion admits a local asymptotic minimax theorem. Asymptotically optimal estimators are Bayes decision rules that use a flat prior and an exponentially tilted likelihood incorporating the moment constraints on possible misspecification. Feasible plug-in analogs of these rules are asymptotically optimal.

What carries the argument

The constrained multiplier criterion, which defines optimality by minimizing a worst-case risk that incorporates moment-constrained misspecification in the local asymptotic limit experiment.

If this is right

- The approach nests several existing misspecification-robust estimation objectives as special cases.

- Asymptotically optimal estimators can be implemented by solving the Bayes problem with the tilted likelihood and then plugging in consistent estimates of the tilting parameters.

- Classical efficiency bounds are recovered when the misspecification concerns are set to zero.

- The framework provides a unified way to compare different misspecification-averse estimators through their implied tilting parameters.

Where Pith is reading between the lines

- The tilted-likelihood construction may suggest new ways to adjust standard estimators in applied settings where researchers have specific moment conditions they wish to protect against violation.

- Extensions could examine whether similar tilting appears in finite-sample robust procedures or in problems with non-local misspecification.

- The decision-theoretic setup might connect to existing robust optimization methods used in related fields such as machine learning under distribution shift.

Load-bearing premise

Misspecification concerns of interest can be represented via moment constraints in the local asymptotic limit experiment, and decision-theoretic optimality criteria correctly capture attitudes toward misspecification.

What would settle it

A simulation or theoretical example in which a plug-in estimator derived from the tilted-likelihood Bayes rule fails to achieve the claimed local asymptotic minimax risk under the moment constraints.

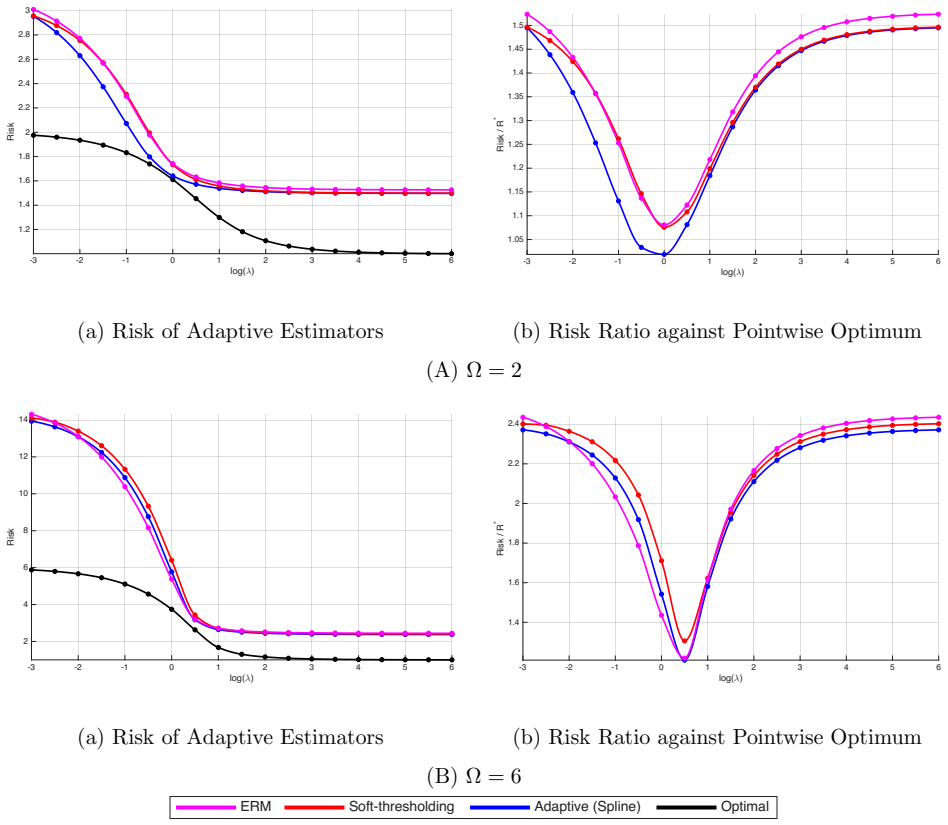

Figures

read the original abstract

We study optimal estimation when the likelihood may be misspecified. Building on tools from the theory of decision-making under uncertainty, we analyze a class of axiomatically grounded optimality criteria which nests several existing misspecification-robust objectives. Within this class, we introduce the constrained multiplier criterion, which allows for flexible misspecification attitudes. We prove a local asymptotic minimax theorem for this criterion, extending a classical efficiency bound to a limit experiment which incorporates moment-constrained misspecification concerns. We characterize asymptotically optimal estimators as Bayes decision rules under a flat prior and an exponentially tilted likelihood that incorporates the moment constraints, and show that feasible plug-in analogs are asymptotically optimal.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a decision-theoretic framework for optimal estimation under likelihood misspecification. It introduces a class of axiomatically grounded criteria that nests existing robust objectives, focuses on the constrained multiplier criterion for flexible misspecification attitudes, proves a local asymptotic minimax theorem extending classical efficiency bounds to a moment-constrained limit experiment, characterizes asymptotically optimal estimators as Bayes rules under a flat prior with exponentially tilted likelihood incorporating the constraints, and establishes asymptotic optimality of feasible plug-in analogs.

Significance. If the minimax theorem and characterization hold, the paper provides a principled extension of classical asymptotic efficiency results to incorporate misspecification aversion via moment constraints, offering a bridge between decision theory under uncertainty and econometric estimation. The explicit Bayes characterization and plug-in optimality could facilitate practical implementation in settings with model uncertainty, strengthening the case for robust procedures in large-sample econometrics.

minor comments (3)

- [Abstract and §1] The abstract and introduction could more explicitly state the precise regularity conditions required for the local asymptotic minimax theorem to ensure readers can assess applicability without consulting the full derivations.

- [Section on characterization] Notation for the exponentially tilted likelihood and moment constraints should be introduced with a clear reference to the underlying decision-theoretic axioms to avoid any ambiguity in how the tilting incorporates misspecification.

- [Empirical or simulation section (if present)] The paper would benefit from a brief discussion or simulation example illustrating how the constrained multiplier criterion differs numerically from standard robust alternatives in finite samples.

Simulated Author's Rebuttal

We thank the referee for their positive summary of the manuscript and for recommending minor revision. No specific major comments were raised in the report.

Circularity Check

No significant circularity; derivation self-contained

full rationale

The paper extends classical local asymptotic efficiency results via decision-theoretic axioms to a moment-constrained limit experiment. The minimax theorem and Bayes characterization under flat prior plus exponential tilting are derived from standard decision theory applied to the extended experiment, with moment constraints treated as modeling primitives. No load-bearing step reduces the optimality criterion to a fitted quantity defined from the same data, nor relies on self-citation chains or ansatzes smuggled from prior author work. The plug-in optimality follows directly from the characterization without circular renaming or self-definition.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Optimality criteria are axiomatically grounded in the theory of decision-making under uncertainty.

Reference graph

Works this paper leans on

-

[1]

You've Got to be Efficient: Ambiguity, Misspecification and Variational Preferences

Adusumilli, K.(2026): “You’ve Got to be Efficient: Ambiguity, Misspecification and Variational Preferences,”arXiv preprint arXiv:2604.05327. Aliprantis, C. D., and K. C. Border(2006):Infinite dimensional analysis: a hitch- hiker’s guide: Springer. Andrews, I., J. Chen, and O. Tecchio(2025): “The purpose of an estimator is what it does: Misspecification, e...

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[2]

Distributionally Robust Stochastic Optimization with Wasserstein Distance,

33 Eaton, M. L.(1989):Group Invariance Applications in Statistics, Hayward, CA: Institute of Mathematical Statistics and American Statistical Association. Gao, R., and A. Kleywegt(2023): “Distributionally Robust Stochastic Optimization with Wasserstein Distance,”Mathematics of Operations Research, 48, 603–655, 10.1287/ moor.2022.1275. Ghirardato, P., and ...

-

[3]

Estimation of the mean of a univariate normal distribution with known variance,

Magnus, J.(2002): “Estimation of the mean of a univariate normal distribution with known variance,”The Econometrics Journal, 5, 225–236. 34 Newey, W. K., and R. J. Smith(2004): “Higher Order Properties of GMM and Gener- alized Empirical Likelihood Estimators,”Econometrica, 72, 219–255. Olea, J. L. M., C. Rush, A. Velez, and J. Wiesel(2026): “The distribut...

-

[4]

We abuse notation and identify this set with the set of simple, Borel measurable functionsf:X →R

of≿ θ onF, it suffices to obtain a variational representationU θ of≿ θ on the domain F0(X)⊆ Fofsimple(finitely-valued) Borel measurable functionsfsuch thatf(·, x) is constant inθ. We abuse notation and identify this set with the set of simple, Borel measurable functionsf:X →R. Lemma 3.Assume that≿ θ satisfies the basic axioms (θ-Relevance, Nontrivial Weak...

2006

-

[5]

Part (ii): SinceRis unbounded, uniqueness and the given expression immediately follow from Proposition 6 of Maccheroni et al. (2006). Part (iii): Additionally suppose that≿ θ satisfies Axiom

2006

-

[6]

(2006),c θ(Qθ) =

By Lemma 32 of Maccheroni et al. (2006),c θ(Qθ) =

2006

-

[7]

The equalities {P∈∆ F (X) :c θ(P)≤t}= {P∈∆(X) :c θ(P)≤t} ∀t≥0 immediately follow from Parts (i) and (ii). It remains to show Vθ(L) = sup P∈∆(X) Z Lθ(x)dP(x)−c θ(P) ∀L∈ L or equivalently by Lemma 2, min P∈∆ F (X) Z fθ dP+c θ(P) =U θ(f) = inf P∈∆(X) Z fθ(x)dP(x) +c θ(P) ∀f∈ F forU θ as defined in Equation (17). Fix anyf∈ F. The inequality≤follows immediatel...

2006

-

[8]

By definition,c θ : ∆(X)→[0,∞] is weakly lower-semicontinuous

By Parts (i) and (ii), this implies: for eacht≥0, the set {P∈∆(X) :c θ(P)≤t} is weakly closed. By definition,c θ : ∆(X)→[0,∞] is weakly lower-semicontinuous. A.3 Axioms for Aggregation AcrossΘ While the preferences{≿ θ:θ∈Θ}describe the researcher’s preferences under knownθ, θis unknown in practice, so our ultimate interest is in the overall preference≿ Θ....

2025

-

[9]

Part (i): By Lemmas 2 and 3 and Proposition 19(iii) of Maccheroni et al

In this case, Vθ(L) = sup P∈P θ∩∆(X) Z Lθ dP Proof of Theorem 6.Necessity of the axioms (the backwards directions of each part) is straightforward, so we prove sufficiency. Part (i): By Lemmas 2 and 3 and Proposition 19(iii) of Maccheroni et al. (2006),c θ takes only values 0 and∞. By Lemma 32 of Maccheroni et al. (2006), Pθ ={P∈∆ F (X) :c θ(P) = 0} Since...

2006

-

[10]

(2006), for anyt≥0, Pθ ={P∈∆ F (X) :c θ(P) = 0}={P∈∆ F (X) :c θ(P)≤t} Hence,≿ θ satisfies Axiom 18 if and only if it satisfies Axioms 14 and

By Lemma 32 of Maccheroni et al. (2006), for anyt≥0, Pθ ={P∈∆ F (X) :c θ(P) = 0}={P∈∆ F (X) :c θ(P)≤t} Hence,≿ θ satisfies Axiom 18 if and only if it satisfies Axioms 14 and

2006

-

[11]

49 (i) Fix anyθ∈Θ

Theorem 7.Throughout this result, assume that for eachθ∈Θ,Xhas at least three disjoint events that are nonnull under≿ θ. 49 (i) Fix anyθ∈Θ. The preference≿ θ satisfies Axioms 6–13, Monotone Continuity, and the Sure Thing Principle if and only if≿ θ has amultiplier representationwith reference probabilityQ θ: there existsλ θ ∈(0,∞]such that the function Vθ...

2011

-

[12]

For eachλ∈(0,∞], define: ϕλ(x) = −exp(−λ −1x)λ <∞ −x λ=∞ By the dual representation of multiplier preferences: for anyλ θ, λθ′ ∈(0,∞], Uθ(fθ) =ϕ −1 λθ Z ϕλθ(fθ)dQ θ =ϕ −1 λθ qϕλθ(1) + (1−q)ϕ λθ(0) 18More precisely, by the portion of the argument for the proof of Theorem 1 of Strzalecki (2011) which delivers the representation for utility acts. 50 an...

2011

-

[13]

Thestrict epigraphof a functionF:V→[−∞,+∞] is the set epiS(F) :={(v, r)∈V×R:F(v)< r}

LetV be a real vector space. Thestrict epigraphof a functionF:V→[−∞,+∞] is the set epiS(F) :={(v, r)∈V×R:F(v)< r}. Definition 4(Z˘ alinescu (2002) Theorem 2.1.3(ix)).Given functionsF, G:V→(−∞,+∞], theirinf-convolutionis the functionF□G:V→[−∞,+∞], where: (F□G)(v) = inf v1,v2∈V:v 1+v2=v F(v

2002

-

[14]

LetL(X) be the Banach space of bounded, Borel measurable functionsL:X →R, endowed with the sup norm

+G(y 2)< r 1 +r 2 and hence (y 1 +y 2, r1 +r 2)∈epi S(F□G). LetL(X) be the Banach space of bounded, Borel measurable functionsL:X →R, endowed with the sup norm. 20 Letba(X) be the real vector space of bounded, finitely 19This relation is stated without proof as Equation (2.6) of Z˘ alinescu (2002). For completeness, we provide a proof here, which follows ...

2002

-

[15]

Let Yn,h = 1√n nX i=1 ψ(θn,h, Xi). Under Assumption 1, ifT n is a sequence ofR d-valued statistics that is tight underQ n,0, then for every subsequence there exists a further subsequence{s}and a possibly randomized measurable functiont:R p ×R k ×[0,1]→R d such that, withU∼Unif[0,1]independent of (X, Y)in the limit experiment(12)andT=t(X, Y, U), (Ts, Ys,h)...

1998

-

[16]

Therefore there exist a bounded open setB⊂R k andc >0 such thatu ′w(y)≥2cfor ally∈B

Thenu ′WM,h is again a nonzero polynomial, and because each component ofW M,h is centered underQ h,u ′WM,h has mean zero and hence takes strictly positive values on a nonempty open set ofYvalues. Therefore there exist a bounded open setB⊂R k andc >0 such thatu ′w(y)≥2cfor ally∈B. By continuity ofw, for all sufficiently largenwe haveu ′ nw(y)≥conB. SinceA≥...

2019

-

[17]

and level-compactness ofℓ, for anyδthere exists an equivariantδ E such that sup g∈Rp EP(g◦(h,ϕ)) [ℓ(δ(X, Y)−K(g+h))]≥E P(0,ϕ) ℓ δE (X, Y) ,∀ϕ Sinceg∈G=R p operates transitively onH=R p, this is equivalent to sup h∈Rp EP(h,ϕ) [ℓ(δ(X, Y)−Kh)]≥E P(0,ϕ) ℓ δE (X, Y) ,∀ϕ 65 Notice that for givenϕ, KL(P(h, ϕ)∥Q h) = KL(P(g+h, ϕ)∥Q g+h). Therefore, sup h∈Rp EP(h,...

1989

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.