Recognition: unknown

Rigidity and default in production networks

Pith reviewed 2026-05-08 05:03 UTC · model grok-4.3

The pith

In production networks, rigidity and leverage together cause defaults after productivity shocks and reduce welfare below the first best.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under proportional shock transmission, a unique Walrasian rigid equilibrium exists and equilibrium quantities, prices, and interest rates admit explicit expressions. Hulten's theorem fails under rigidity even without leverage. Welfare is smaller than in the first best if and only if both leverage and rigidity exist. Default depends solely on real shocks and network structure, while loss magnitudes also depend on connectedness and connected sectors' debt costs; conditions for default cascades are provided.

What carries the argument

The Walrasian rigid equilibrium under proportional shock transmission in a network of firms with informational rigidity and external debt.

Load-bearing premise

Shocks transmit proportionally through the production network.

What would settle it

An economy in which Hulten's theorem holds despite informational rigidity, or in which welfare equals the first best when both rigidity and leverage are present.

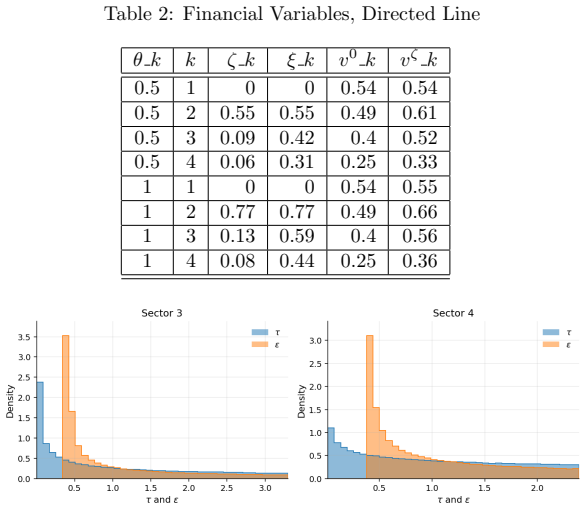

Figures

read the original abstract

This paper studies the transmission of productivity shocks in general equilibrium production networks, when firms in different sectors operate under informational rigidity and rely on external debt. Rigidity breaks the Modigliani-Miller irrelevance of leverage and may generate default following shocks, even in equilibrium. The economy consists of firms, banks, and consumers. Under proportional shock transmission, we prove that a unique Walrasian rigid equilibrium exists and provide explicit expressions for equilibrium quantities, prices, and interest rates. We show that, on the one hand, Hulten's theorem fails under rigidity, even without leverage. On the other hand, we prove that welfare is smaller than in the first best if and only if both leverage and rigidity exist. The latter increase the total cost of debt and have inflationary effects on the levered sectors, which propagate downstream, and shift consumption and labor upstream. The occurrence of default depends solely on real shocks and the network structure, while the magnitude of the losses depends also on the connectedness of the economy and the cost of debt of the connected sectors. We provide conditions for default cascades to occur and study two examples of default propagation.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies productivity shock transmission in general equilibrium production networks where firms face informational rigidity and rely on external debt. Under the maintained assumption of proportional shock transmission, it proves existence of a unique Walrasian rigid equilibrium and derives closed-form expressions for quantities, prices, and interest rates. It shows that Hulten's theorem fails under rigidity alone, that welfare is strictly below the first-best if and only if both rigidity and leverage are present, and that default occurs solely as a function of real shocks and network structure, with conditions for cascades and two illustrative examples of propagation.

Significance. If the derivations hold, the paper offers a tractable framework linking rigidity, leverage, and network structure to equilibrium default and welfare losses, with explicit formulas that could aid quantitative work. The iff welfare result and the demonstration that rigidity alone breaks Hulten's theorem are potentially useful contributions, as is the separation of default incidence from loss magnitude.

major comments (3)

- [Section 2 (model) and the existence theorem] The proportional shock transmission assumption is invoked for the existence proof, closed-form expressions, Hulten's theorem failure, and the welfare iff statement (abstract and the relevant theorem statements). A precise definition must be given (e.g., how productivity shocks scale across sectors or input-output links) together with an explicit proof that it is sufficient for uniqueness and the closed forms; without this, the scope of all headline results remains unclear.

- [Welfare theorem (likely §4 or §5)] The claim that welfare is smaller than first-best if and only if both leverage and rigidity exist (abstract) is load-bearing for the paper's policy message. The proof should be checked for whether the 'only if' direction continues to hold when the proportional-shock restriction is relaxed or replaced by a weaker condition on shock support.

- [Default and cascade analysis (likely §6)] The statement that default depends solely on real shocks and network structure while loss magnitude also depends on connectedness and debt costs (abstract) requires verification that the equilibrium interest-rate expressions remain well-defined at the default boundary; any implicit assumption on limited liability or recovery rates should be stated explicitly.

minor comments (2)

- [Throughout] Notation for the rigidity parameter and the proportional transmission coefficient should be introduced once and used consistently; currently the abstract mixes 'rigidity' and 'informational rigidity' without cross-reference.

- [Examples subsection] The two examples of default propagation would benefit from a table reporting the network adjacency matrix, shock vector, and resulting equilibrium quantities for easy replication.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on our paper. We address each major comment point by point below, providing the strongest honest defense of the manuscript while acknowledging where revisions are needed to clarify assumptions and proofs.

read point-by-point responses

-

Referee: [Section 2 (model) and the existence theorem] The proportional shock transmission assumption is invoked for the existence proof, closed-form expressions, Hulten's theorem failure, and the welfare iff statement (abstract and the relevant theorem statements). A precise definition must be given (e.g., how productivity shocks scale across sectors or input-output links) together with an explicit proof that it is sufficient for uniqueness and the closed forms; without this, the scope of all headline results remains unclear.

Authors: We agree that the proportional shock transmission assumption requires a precise definition and an explicit proof of its role in the results. In the revised manuscript, we will add a formal definition stating that productivity shocks scale proportionally across sectors according to their input-output linkages (i.e., the effective shock to sector j is a weighted sum of upstream shocks with weights given by the input shares in the production network). We will also include a self-contained proof (in the main text or appendix) showing sufficiency for uniqueness of the Walrasian rigid equilibrium and derivation of the closed forms. This directly addresses the scope concern without altering the core results. revision: yes

-

Referee: [Welfare theorem (likely §4 or §5)] The claim that welfare is smaller than first-best if and only if both leverage and rigidity exist (abstract) is load-bearing for the paper's policy message. The proof should be checked for whether the 'only if' direction continues to hold when the proportional-shock restriction is relaxed or replaced by a weaker condition on shock support.

Authors: The iff welfare result is central, and the current proof of the 'only if' direction relies on the closed-form expressions under proportional transmission to show that rigidity alone does not generate welfare losses while the combination with leverage does (via increased debt costs and inflationary effects). We will re-check the proof to see if the 'only if' extends under weaker shock support conditions. If it does not, we will revise the theorem statement to specify the maintained assumption and add a remark discussing robustness; this preserves the policy message while clarifying its domain. revision: partial

-

Referee: [Default and cascade analysis (likely §6)] The statement that default depends solely on real shocks and network structure while loss magnitude also depends on connectedness and debt costs (abstract) requires verification that the equilibrium interest-rate expressions remain well-defined at the default boundary; any implicit assumption on limited liability or recovery rates should be stated explicitly.

Authors: We thank the referee for highlighting the need for boundary verification. In the revision, we will explicitly state the assumptions: firms have limited liability (default occurs when realized revenue falls below debt obligations), and creditors recover a fixed fraction of assets upon default (recovery rate as a model parameter between 0 and 1). We will verify that the closed-form interest-rate expressions remain well-defined and continuous at the default boundary by direct substitution and showing no indeterminacy arises. This strengthens the default cascade analysis without changing the separation of incidence from magnitude. revision: yes

Circularity Check

No circularity; results derived from explicit model assumptions and proofs

full rationale

The paper is a theoretical general-equilibrium analysis. It states an assumption of proportional shock transmission and then proves existence of a unique Walrasian rigid equilibrium, supplies closed-form expressions, and derives welfare and default results under that assumption. No step reduces a claimed prediction or theorem to a fitted parameter, a self-referential definition, or a load-bearing self-citation whose content is itself unverified. The derivations are presented as direct consequences of the stated primitives and network structure, with no renaming of known empirical patterns or smuggling of ansatzes via prior work. The analysis is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Walrasian equilibrium exists in the rigid economy

- ad hoc to paper Proportional shock transmission

Reference graph

Works this paper leans on

-

[1]

Acemoglu, V

D. Acemoglu, V. M. Carvalho, A. Ozdaglar, and A. Tahbaz-Salehi. The network origins of aggregate fluctuations.Econometrica, 80(5):1977–2016, 2012

1977

-

[2]

Acemoglu and A

D. Acemoglu and A. Tahbaz-Salehi. The macroeconomics of supply chain disruptions.Rev. Econ. Stud., 92(2):656–695, 2024

2024

-

[3]

Angeletos, L

G.-M. Angeletos, L. Iovino, and J. La’o. Real rigidity, nominal rigidity, and the social value of information.Am. Econ. Rev., 106(01):200–227, 2016

2016

-

[4]

Baqaee and E

D. Baqaee and E. Rubbo. Micro propagation and macro aggregation.Annu. Rev. Econ., 15(1):91–123, 2023

2023

-

[5]

D. R. Baqaee and E. Farhi. The macroeconomic impact of microeconomic shocks: Beyond hulten’s theorem.Econometrica, 87(4):1155–1203, 2019

2019

-

[6]

D. R. Baqaee and E. Farhi. Entry vs. rents: Aggregation with economies of scale.NBER Working Paper No. 27140, 2020

2020

-

[7]

D. R. Baqaee and E. Farhi. Productivity and misallocation in general equilibrium.Q. J. Econ., 135(1):105–163, 2020

2020

-

[8]

Battiston, D

S. Battiston, D. Delli Gatti, M. Gallegati, B. Greenwald, and J. E. Stiglitz. Credit chains and bankruptcy propagation in production networks.J. Econ. Dyn. Control, 31(6):2061–2084, 2007

2061

-

[9]

Bigio and J

S. Bigio and J. La’o. Distortions in production networks.Q. J. Econ., 135(4):2187–2253, 2020

2020

-

[10]

V. M. Carvalho, M. Nirei, Y. U. Saito, and A. Tahbaz-Salehi. Supply chain disruptions: Evidence from the great east japan earthquake.Q. J. Econ., 136(2):1255–1321, 2021

2021

-

[11]

V. M. Carvalho and A. Tahbaz-Salehi. Production networks: A primer. Annu. Rev. Econ., 11(1):635–663, 2019

2019

-

[12]

Elliott and B

M. Elliott and B. Golub. Networks and economic fragility.Annu. Rev. Econ., 14(1):665–696, 2022

2022

-

[13]

Elliott and M

M. Elliott and M. O. Jackson. Supply chain disruptions, the struc- ture of production networks, and the impact of globalization.SSRN: https://ssrn.com/abstract=4580819, 2026

2026

-

[14]

C. R. Hulten. Growth accounting with intermediate inputs.Rev. Econ. Stud., 45(3):511–518, 1978

1978

-

[15]

Huremovic, G

K. Huremovic, G. Jim´ enez, E. Moral-Benito, F. Vega-Redondo, et al. Production and financial networks in interplay.SSRN: https://ssrn.com/abstract=4657236, 2025. 57

2025

-

[16]

J. B. Long and C. I. Plosser. Real business cycles.J. Polit. Econ., 91(1):39– 69, 1983

1983

-

[17]

Pellet and A

T. Pellet and A. Tahbaz-Salehi. Rigid production networks.J. Monetary Econ., 137:86–102, 2023. 58

2023

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.