Recognition: unknown

Comonotonic improvement under feasibility constraints

Pith reviewed 2026-05-07 17:33 UTC · model grok-4.3

The pith

A feasibility set is componentwise convex-order solid when replacing any agent's allocation with a less risky one keeps the overall allocation feasible.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that componentwise convex-order solidity of the feasible set is a sufficient condition for the comonotonic improvement theorem to survive feasibility constraints. Under this condition, and for any preferences that respect convex order, every feasible allocation admits a feasible comonotonic improvement. The paper shows by counterexample that Value-at-Risk constraints violate the solidity property and therefore admit optima that are not comonotonic in the aggregate loss, while many other common constraints satisfy it.

What carries the argument

Componentwise convex-order solidity: the property that any feasible allocation remains feasible after replacing one agent's payoff with any payoff that is smaller in convex order.

If this is right

- Mean-variance risk-sharing problems with solid constraints have optimal allocations that are comonotonic in the aggregate loss.

- Standard insurance constraints such as quota-share or stop-loss reinsurance satisfy the solidity condition and therefore preserve comonotonic optima.

- Value-at-Risk caps and idiosyncratic deductibles violate solidity, so optimal allocations under those rules need not be comonotonic.

- The improvement result holds for the entire class of convex-order preferences, not merely for specific families such as expected utility or mean-variance.

Where Pith is reading between the lines

- Regulators could use the solidity test to screen proposed capital or exposure rules before they distort risk-sharing incentives.

- When a constraint fails solidity, one could search for the nearest solid relaxation or for weaker improvement results that still hold.

- The same condition might apply to dynamic or multi-period risk-sharing problems where feasibility must be preserved period by period.

- Numerical checks of solidity for a new constraint could be implemented by solving convex-order comparison problems on discretized loss distributions.

Load-bearing premise

Preferences must be consistent with convex order, and the feasible set must stay feasible whenever one agent's allocation is replaced by a less risky one in convex order.

What would settle it

A concrete feasible set that is componentwise convex-order solid yet contains an allocation with no feasible comonotonic improvement, or a convex-order-consistent preference that strictly prefers the original allocation over every comonotonic alternative.

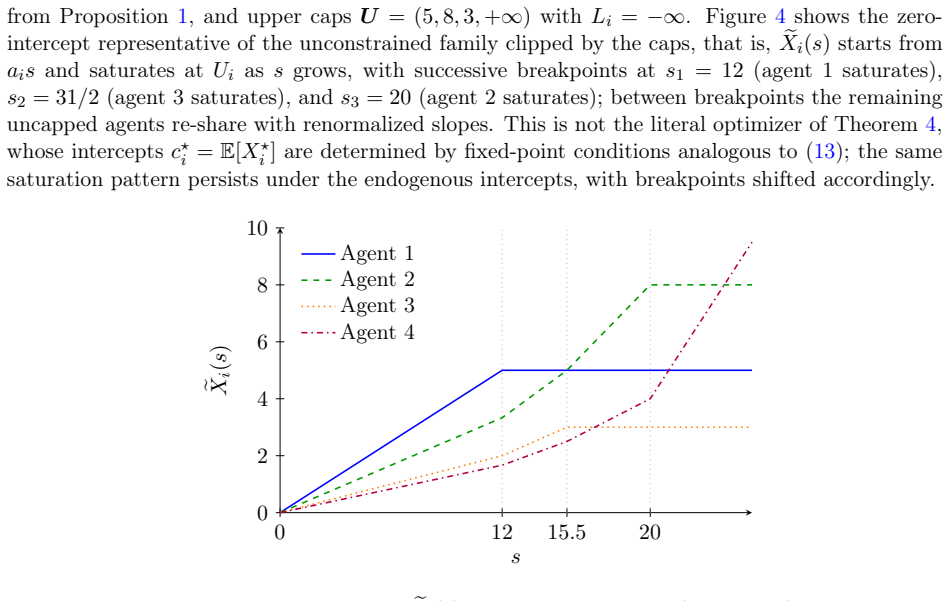

Figures

read the original abstract

Regulatory and contractual constraints on individual exposures are standard in insurance and reinsurance markets, but a poorly designed constraint can distort the economic incentives of risk-averse agents. In the unconstrained problem, the classical comonotonic improvement theorem guarantees Pareto-optimal allocations that are nondecreasing in the aggregate loss. A constraint that is not stable under risk reduction can destroy this property. We show by example that Value-at-Risk caps lead to optimal allocations that are non-comonotonic in the aggregate loss. We identify componentwise convex-order solidity as a sufficient condition on the feasible set that restores the comonotonic improvement under constraints. If replacing any agent's allocation by a less risky one preserves feasibility, then every feasible allocation admits a feasible comonotonic improvement for all convex-order-consistent preferences. This criterion covers many constraints typical in risk management, but excludes Value-at-Risk caps and idiosyncratic deductibles. We illustrate the implications of our main result in a mean-variance risk-sharing application.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper shows that standard feasibility constraints such as Value-at-Risk caps can destroy the comonotonicity property of Pareto-optimal risk-sharing allocations that holds in the unconstrained case. It supplies an explicit counter-example with VaR and then identifies componentwise convex-order solidity of the feasible set as a sufficient condition that restores the existence of a feasible comonotonic improvement for any allocation whenever all agents’ preferences are consistent with convex order. The condition is shown to be satisfied by many common regulatory and contractual constraints but violated by VaR caps and certain deductibles; the result is applied to a mean-variance risk-sharing problem.

Significance. If the central theorem holds, the paper supplies a clean, checkable criterion that regulators and contract designers can use to ensure that constrained risk-sharing problems retain the qualitative features of the unconstrained optimum. The counter-example is concrete and the sufficient condition is stated in terms of a standard stochastic order, making the contribution directly usable in applications.

minor comments (4)

- §2.2: the VaR counter-example would benefit from an explicit numerical table showing the aggregate loss, the individual allocations, and the resulting non-comonotonicity.

- Definition 3.1: the phrase “componentwise convex-order solidity” is introduced without a preceding sentence that contrasts it with ordinary solidity; a one-sentence comparison would improve readability.

- Theorem 3.2: the statement that the improved allocation “preserves the aggregate” should be accompanied by the exact equality that is preserved (i.e., sum of conditional expectations equals the original sum almost surely).

- §4: the mean-variance application assumes quadratic utility; a brief remark on how the result extends to other convex-order consistent preferences would strengthen the section.

Simulated Author's Rebuttal

We thank the referee for the careful reading and positive assessment of the manuscript. The summary accurately reflects the paper's contributions, and we appreciate the recommendation for minor revision. No specific major comments were raised in the report.

Circularity Check

No significant circularity detected

full rationale

The paper extends the classical comonotonic improvement theorem by defining componentwise convex-order solidity on the feasible set and showing it is sufficient for feasible comonotonic improvements. The proof applies the standard map of conditional expectations given the aggregate loss, invokes Jensen's inequality for convex order, and uses the solidity property directly; all steps rely on independent mathematical facts about convex order and conditional expectation rather than self-referential definitions, fitted parameters, or load-bearing self-citations. The VaR counterexample demonstrates when the condition fails without introducing circularity.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Preferences are convex-order consistent

- standard math Classical comonotonic improvement theorem holds without constraints

Reference graph

Works this paper leans on

-

[1]

Acciaio, B. (2007). Optimal risk sharing with non-monotone monetary functionals.Finance and Stochastics, 11(2):267–289

2007

-

[2]

Albrecher, H., Beirlant, J., and Teugels, J. L. (2017).Reinsurance: Actuarial and Statistical Aspects. Wiley Series in Probability and Statistics. Wiley

2017

-

[3]

and El Karoui, N

Barrieu, P. and El Karoui, N. (2005). Inf-convolution of risk measures and optimal risk transfer. Finance and Stochastics, 9(2):269–298. Bäuerle, N. and Müller, A. (2006). Stochastic orders and risk measures: consistency and bounds. Insurance: Mathematics and Economics, 38(1):132–148. BCBS (2019). Minimum capital requirements for market risk. Technical Re...

2005

-

[4]

and Tian, W

Bernard, C. and Tian, W. (2009). Optimal reinsurance arrangements under tail risk measures. Journal of Risk and Insurance, 76(3):709–725

2009

-

[5]

and Vanduffel, S

Bernard, C. and Vanduffel, S. (2025). Risk sharing under ambiguity.Working paper

2025

-

[6]

Boonen, T. J. and Ghossoub, M. (2020). Bilateral risk sharing with heterogeneous beliefs and exposure constraints.ASTIN Bulletin, 50(1):293–323

2020

-

[7]

Borch, K. (1962). Equilibrium in a reinsurance market.Econometrica, 30(3):424–444

1962

-

[8]

and Dana, R.-A

Carlier, G. and Dana, R.-A. (2003). Pareto efficient insurance contracts when the insurer’s cost function is discontinuous.Economic Theory, 21(4):871–893

2003

-

[9]

Cummins, J. D. (2008). CAT bonds and other risk-linked securities: state of the market and recent developments.Risk Management and Insurance Review, 11(1):23–47

2008

-

[10]

(1994).Non-Additive Measure and Integral

Denneberg, D. (1994).Non-Additive Measure and Integral. Springer Science & Business Media

1994

-

[11]

Denuit, M. (2020). Investing in your own and peers’ risks: the simple analytics of P2P insurance. European Actuarial Journal, 10(2):335–359. 19

2020

-

[12]

J., Kaas, R., and Vyncke, D

Dhaene, J., Denuit, M., Goovaerts, M. J., Kaas, R., and Vyncke, D. (2002). The concept of comonotonicity in actuarial science and finance: theory.Insurance: Mathematics and Economics, 31(1):3–33

2002

-

[13]

Embrechts, P., Liu, H., and Wang, R. (2018). Quantile-based risk sharing.Operations Research, 66(4):936–949. European Commission (2009). Directive 2009/138/EC of the European Parliament and of the Council of 25 November 2009 on the taking-up and pursuit of the business of insurance and reinsurance (Solvency II). Technical report, Official Journal of the E...

2018

-

[14]

Jouini, E., Schachermayer, W., and Touzi, N. (2008). Optimal risk sharing for law invariant mone- tary utility functions.Mathematical Finance, 18(2):269–292

2008

-

[15]

and Meilijson, I

Landsberger, M. and Meilijson, I. (1994). Co-monotone allocations, Bickel–Lehmann dispersion and the Arrow–Pratt measure of risk aversion.Annals of Operations Research, 52(2):97–106

1994

-

[16]

Lauzier, J.-G., Lin, L., and Wang, R. (2023). Pairwise counter-monotonicity.Insurance: Mathe- matics and Economics, 111:279–287

2023

-

[17]

Lauzier, J.-G., Lin, L., and Wang, R. (2026). Risk sharing, measuring variability, and distortion riskmetrics.Mathematical Finance, 36(2):330–351

2026

-

[18]

and Rüschendorf, L

Ludkovski, M. and Rüschendorf, L. (2008). On comonotonicity of Pareto optimal risk sharing. Statistics and Probability Letters, 78(10):1181–1188

2008

-

[19]

OxfordUniversity

Mas-Colell, A., Whinston, M.D., andGreen, J.R.(1995).Microeconomic Theory. OxfordUniversity

1995

-

[20]

and Stiglitz, J

Rothschild, M. and Stiglitz, J. E. (1970). Increasing risk: I. A definition.Journal of Economic Theory, 2(3):225–243. Rüschendorf, L.(2013).Mathematical Risk Analysis: Dependence, Risk Bounds, Optimal Allocations and Portfolios. Springer, Berlin, Heidelberg

1970

-

[21]

Wang, S. S. and Young, V. R. (1998). Ordering risks: Expected utility theory versus Yaari’s dual theory of risk.Insurance: Mathematics and Economics, 22(2):145–161

1998

-

[22]

S., Young, V

Wang, S. S., Young, V. R., and Panjer, H. H. (1997). Axiomatic characterization of insurance prices. Insurance: Mathematics and Economics, 21(2):173–183

1997

-

[23]

Weber, S. (2018). Solvency II, or how to sweep the downside risk under the carpet.Insurance: Mathematics and Economics, 82:191–200

2018

-

[24]

Xia, Z., Zou, Z., and Hu, T. (2023). Inf-convolution and optimal allocations for mixed-VaRs. Insurance: Mathematics and Economics, 108:156–164. 20

2023

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.