Recognition: unknown

Corporate Bond Yield Curve Modeling: A Rating-Based Regime-Switching Generalized CIR Approach

Pith reviewed 2026-05-07 13:49 UTC · model grok-4.3

The pith

A two-state regime-switching generalized CIR model jointly prices Chinese government and corporate bond curves by conditioning credit factors on interest-rate regimes.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that persistent shifts in term-structure dynamics are captured by a two-state RS-GCIR short-rate process in the rate block, while corporate yields are priced by embedding CIR-type credit factors in an intensity framework that conditions on the prevailing rate regime; this block-recursive structure improves joint curve fit and yield decomposition relative to single-regime benchmarks.

What carries the argument

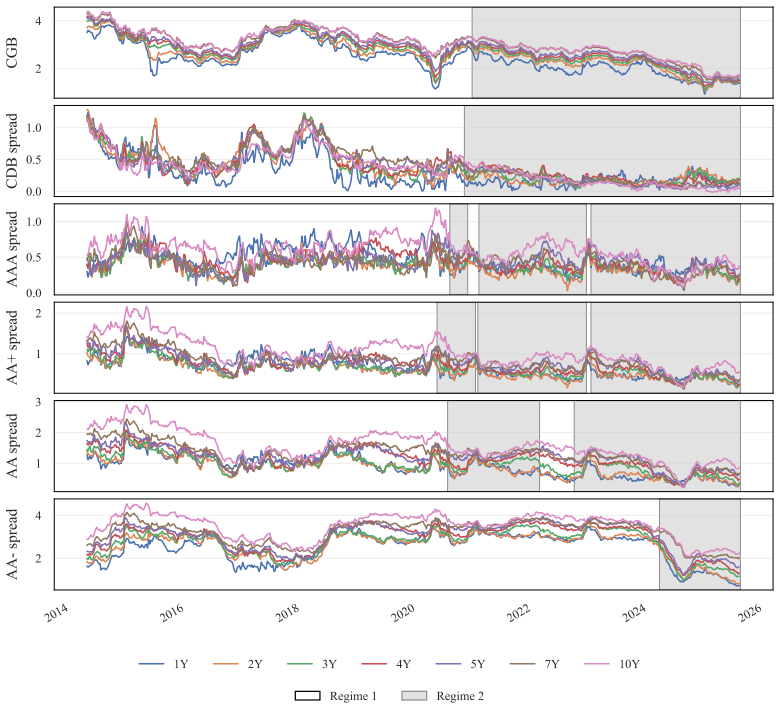

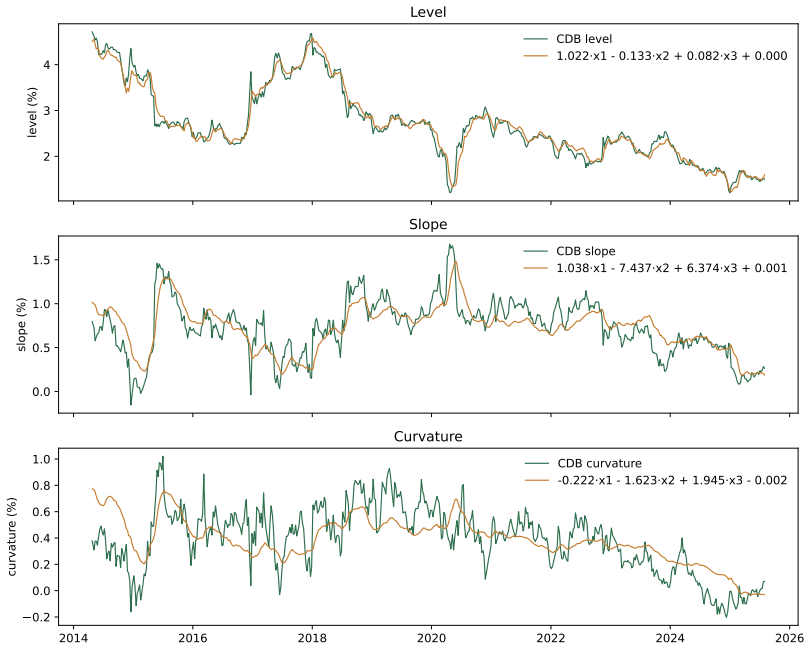

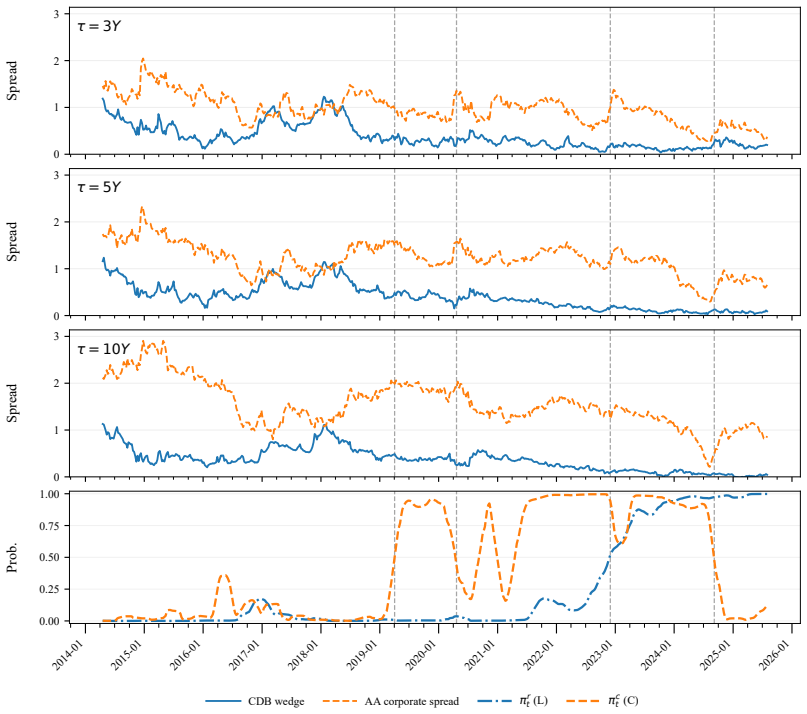

The two-block RS-GCIR structure: a two-state regime-switching generalized CIR short-rate process estimated from CGB curves, with corporate bonds priced via an intensity-based credit block that uses CIR-type factors for rating migration and default conditional on the rate regime.

If this is right

- Joint pricing errors for government and corporate curves fall relative to single-regime models.

- Filtered regime probabilities become economically interpretable as distinct level-volatility states.

- Corporate yields decompose more cleanly into interest-rate discounting and credit-spread components.

- The transmission from rate conditions to credit spreads is captured without explicit feedback loops.

Where Pith is reading between the lines

- The block-recursive UKF estimation could be adapted to other emerging markets that experienced a corporate default cycle.

- Regime probabilities might serve as real-time indicators for monitoring credit-market stress.

- Extending the credit block to allow limited feedback from credit factors to rates could be tested against the current no-feedback assumption.

Load-bearing premise

Corporate bond pricing can be separated into a rate block estimated only from government bonds and a credit block that conditions on the rate regime with no feedback requiring joint estimation.

What would settle it

Out-of-sample data after 2025 showing that the two filtered regimes no longer produce lower joint pricing errors than a single-regime GCIR model, or that the filtered regime probabilities fail to align with observable shifts in Chinese interest-rate or default conditions.

Figures

read the original abstract

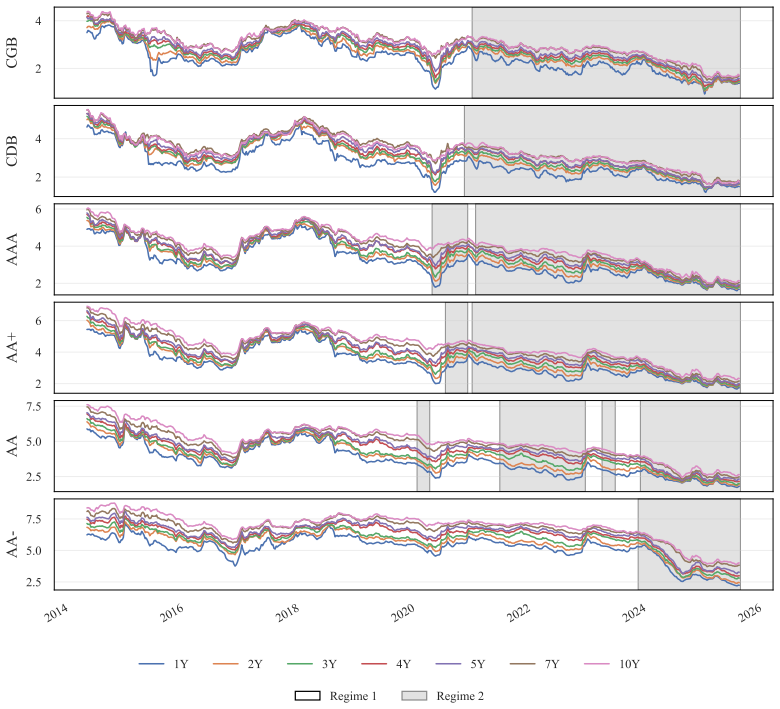

Persistent shifts in term-structure dynamics undermine the stability of single-regime models in long samples. We develop an arbitrage-free regime-switching generalized CIR (RS-GCIR) model that jointly prices the Chinese government bond (CGB) curve and corporate bond curves. To capture the systematic transmission from interest-rate conditions to credit spreads, we structure the model into two blocks and price corporate bonds conditional on the prevailing rate regime. The rate block features a two-state RS-GCIR short-rate process estimated from CGB zero-coupon curves, while the credit block embeds CIR-type credit factors in an intensity-based framework for rating migration and default. We implement a block-recursive Unscented Kalman Filter (UKF) procedure--filtering the rate block first and the credit block next--using weekly data from 2014--2025, a period that begins with the onset of China's modern corporate default cycle. We identify two persistent rate regimes with distinct level--volatility profiles. Relative to single-regime benchmarks, regime switching improves joint curve fit, delivers economically interpretable filtered regime probabilities, and sharpens the decomposition of corporate yields into discounting and credit compensation.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops an arbitrage-free two-block regime-switching generalized CIR (RS-GCIR) model for jointly pricing Chinese government bond (CGB) zero curves and corporate bond curves. The rate block employs a two-state RS-GCIR short-rate process estimated solely from CGB data; the credit block uses CIR-type intensity factors for rating migration and default, conditioned on the prevailing rate regime. Estimation proceeds via a block-recursive Unscented Kalman Filter on weekly 2014–2025 data, identifying two persistent regimes with distinct level-volatility profiles. The central claims are that regime switching improves joint curve fit, yields economically interpretable filtered regime probabilities, and sharpens the decomposition of corporate yields into discounting versus credit compensation relative to single-regime benchmarks.

Significance. If the no-feedback assumption between credit events and rate dynamics holds, the framework provides a tractable way to embed regime shifts into corporate bond pricing while preserving arbitrage-free conditions. The empirical application to China’s post-2014 default cycle supplies a relevant test case for emerging-market term-structure modeling with observable regime persistence. The block-recursive structure and UKF implementation are computationally attractive, though the absence of reported out-of-sample validation or robustness checks to feedback limits immediate applicability.

major comments (1)

- [§3.2] §3.2 (block-recursive UKF procedure): The rate block is filtered exclusively from CGB data and then used to condition the credit block without any reverse channel. This assumption is load-bearing for the claimed sharper yield decomposition and interpretable regime probabilities. If corporate defaults or spreads influence rate dynamics or regime persistence in the 2014–2025 sample, the sequential filtering will produce inconsistent regime probabilities and biased credit compensation estimates. The manuscript should either test for feedback (e.g., via Granger causality on filtered states or a joint estimation alternative) or quantify the bias under plausible feedback strengths.

minor comments (3)

- [Abstract] Abstract and §1: The term 'generalized CIR' is used without an immediate definition of which parameters are allowed to switch or depend on the regime; a one-sentence clarification would help readers before the model equations.

- [§4] §4 (empirical results): No table reports the reduction in RMSE or pricing errors for the credit component under regime switching versus the single-regime benchmark; adding such a metric would make the 'sharpened decomposition' claim directly verifiable.

- [Data section] Data description: The sample begins in 2014 'with the onset of China’s modern corporate default cycle,' but the exact first default date used for calibration and any liquidity filters applied to corporate bonds are not stated; these details affect reproducibility.

Simulated Author's Rebuttal

We thank the referee for the constructive comments on our manuscript. The primary concern centers on the validity of the no-feedback assumption underlying our block-recursive UKF estimation. We respond to this point below and commit to revisions that directly address the suggestion.

read point-by-point responses

-

Referee: [§3.2] §3.2 (block-recursive UKF procedure): The rate block is filtered exclusively from CGB data and then used to condition the credit block without any reverse channel. This assumption is load-bearing for the claimed sharper yield decomposition and interpretable regime probabilities. If corporate defaults or spreads influence rate dynamics or regime persistence in the 2014–2025 sample, the sequential filtering will produce inconsistent regime probabilities and biased credit compensation estimates. The manuscript should either test for feedback (e.g., via Granger causality on filtered states or a joint estimation alternative) or quantify the bias under plausible feedback strengths.

Authors: We acknowledge that the no-feedback assumption is central to the tractability and interpretability of the block-recursive procedure. In the Chinese institutional setting, CGB yields are predominantly shaped by monetary policy, fiscal conditions, and macroeconomic aggregates, whereas corporate defaults (even during the post-2014 cycle) have remained limited in aggregate size and have not produced measurable spillovers into the government yield curve. Nevertheless, to strengthen the empirical grounding of this modeling choice, we will add to the revised manuscript (i) a Granger-causality analysis between the filtered rate-regime probabilities and corporate credit-spread series, and (ii) a brief discussion of the likely magnitude of any omitted feedback bias. These additions will be placed in §3.2 and the robustness section. We do not believe a full joint estimation is required for the present application, but the proposed tests will allow readers to assess the assumption directly. revision: yes

Circularity Check

No significant circularity in derivation or estimation chain

full rationale

The paper defines an explicit two-block RS-GCIR structure with rate dynamics estimated solely from CGB data and credit factors conditioned on the resulting regimes via block-recursive UKF. This is a modeling assumption (no credit-to-rate feedback) rather than a self-referential derivation. Reported improvements in joint fit and regime interpretability are comparative outcomes against single-regime benchmarks on the 2014-2025 sample; they do not reduce by construction to the fitted parameters themselves. No self-citation load-bearing steps, uniqueness theorems, or ansatz smuggling appear in the provided derivation. The procedure is self-contained against external data and standard UKF filtering.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Term structure of interest rates with regime shifts.The Journal of Finance, 57(5):1997–2043,

Ravi Bansal and Hao Zhou. Term structure of interest rates with regime shifts.The Journal of Finance, 57(5):1997–2043,

1997

-

[2]

China chengxin pengyuan credit rating co., ltd

CSCI Pengyuan Credit Rating Co., Ltd. China chengxin pengyuan credit rating co., ltd. 2024 migration matrixstatisticalreport.Technicalreport,CSCIPengyuanCreditRatingCo.,Ltd.,February2025.URL https://www.cspengyuan.com/pengyuancmscn/disclosure/grade/20250225175451807. Information disclosure: rating performance statistics (migration matrices). Qiang Dai, Ke...

-

[3]

doi: 10.26599/CJE.2025.9300306. (in Chinese). Li-Wen Lin and Curtis J Milhaupt. Bonded to the state: a network perspective on china’s corporate debt market.Journal of Financial Regulation, 3(1):1–39,

-

[4]

(𝑒𝛾′ 𝜏 −1 ) ! . (118) In the discounting case (𝑐1 =1, 𝑐 2 =0) with𝛾 ′ = √︁ 𝜅′2 +2𝛽, 𝐵(𝜏)= 2 𝑒𝛾′ 𝜏 −1 2𝛾′ + (𝛾 ′ +𝜅 ′) (𝑒𝛾′ 𝜏 −1 ) ,(119) 𝐴(𝜏)= 𝛼 𝛽 𝜏− 2𝛼 𝛽 𝑒𝛾′ 𝜏 −1 2𝛾′ + (𝛾 ′ +𝜅 ′) (𝑒𝛾′ 𝜏 −1 ) + 2(𝛽𝜃 ′ +𝛼)𝜅 ′ 𝛽2 ln 2𝛾′𝑒 (𝛾 ′ +𝜅 ′ )𝜏 2 2𝛾′ + (𝛾 ′ +𝜅 ′) (𝑒𝛾′ 𝜏 −1 ) ! .(120) Thus, the closed-form solutions of𝐴(𝜏)and𝐵(𝜏)expressed by parameters underPare: 𝐴(𝜏)...

1998

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.