Recognition: unknown

Sequential Estimation of Dynamic Discrete Choice Models with Unobserved Heterogeneity

Pith reviewed 2026-05-07 12:41 UTC · model grok-4.3

The pith

Truncating the inner fixed-point solver after any number of steps leaves the EM-NPL estimator numerically identical in linear-in-parameters models.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

For the workhorse class of linear-in-parameters models, for any q greater than or equal to 1 the EM-NPL(q) estimator is numerically identical to the EM-NPL estimator that solves the inner fixed-point problem to convergence. The choice of q therefore influences only computational cost and not statistical properties. The estimator is consistent and asymptotically normal, and the algorithm converges locally.

What carries the argument

The truncation-invariance property of the EM-NPL(q) algorithm for linear-in-parameters dynamic discrete choice models.

If this is right

- The estimator remains consistent and asymptotically normal for any fixed q greater than or equal to 1.

- Local convergence of the EM-NPL(q) algorithm is guaranteed under standard conditions.

- Runtime falls by at least 20 percent and can reach a factor of three to five in Monte Carlo designs.

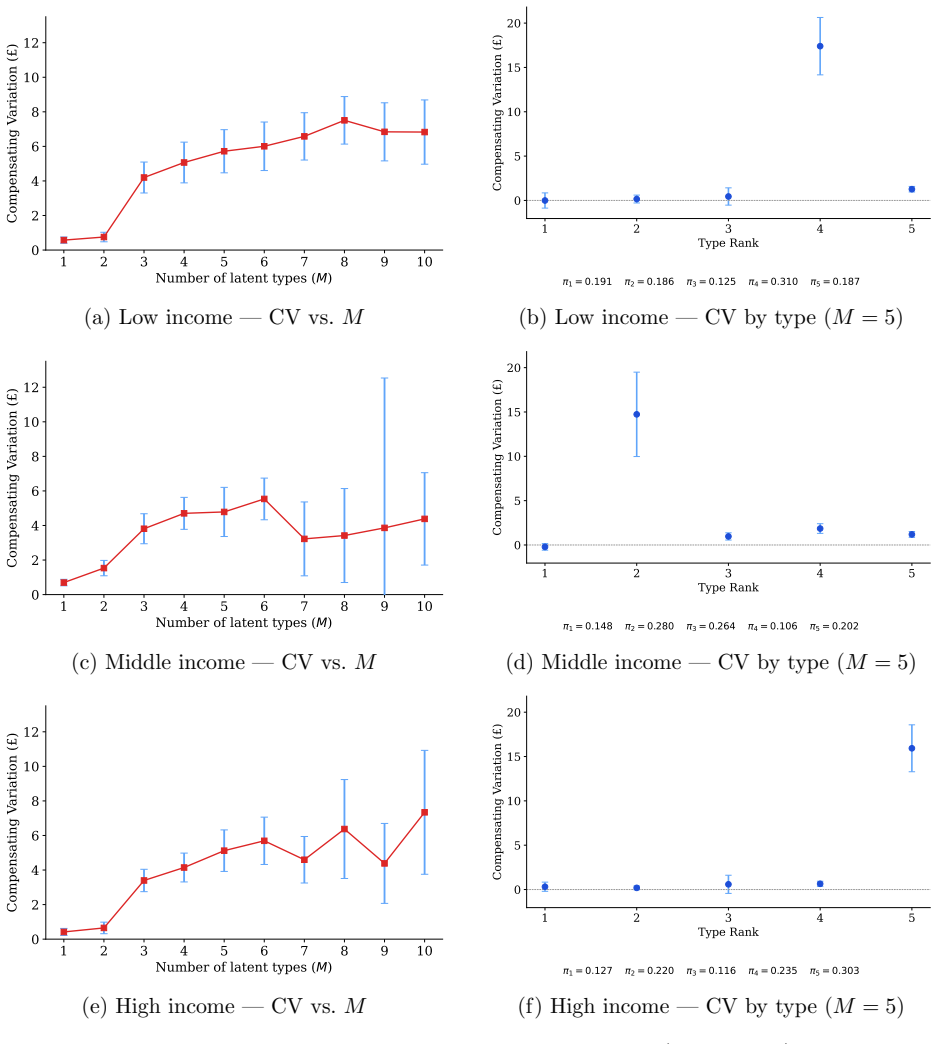

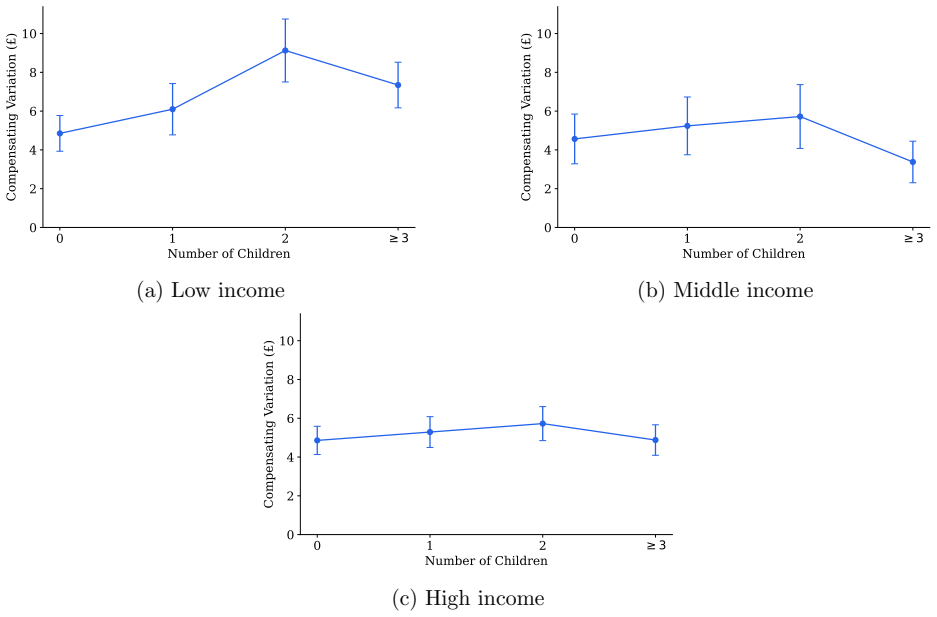

- Accounting for unobserved heterogeneity raises estimated long-run own-price elasticities by up to 60 percent, short-run elasticities by up to 85 percent, and compensating variation from a soda tax by up to 90 percent.

Where Pith is reading between the lines

- The invariance may allow researchers to estimate models with larger numbers of unobserved types than were previously practical.

- Small fixed values of q such as 1 or 2 can be adopted without any need to verify convergence of the inner loop.

- Related EM-based estimators outside dynamic discrete choice may possess analogous invariance properties that could be checked directly.

Load-bearing premise

The truncation-invariance result holds specifically for the workhorse class of linear-in-parameters models.

What would settle it

A concrete linear-in-parameters model in which the numerical value of the EM-NPL(1) estimate differs from the value obtained by solving the inner fixed-point problem to convergence would falsify the invariance claim.

Figures

read the original abstract

Estimating dynamic discrete choice models with unobserved heterogeneity is computationally costly because it requires repeatedly solving fixed-point equations for all unobserved types. We develop the EM-NPL(q) framework that combines the Expectation-Maximization (EM) algorithm with an inner fixed-point solver truncated to q iterations. For the workhorse class of linear-in-parameters models, we establish a truncation-invariance result: for any q$\geq$1, EM-NPL(q) is numerically identical to the EM-NPL estimator that solves the inner fixed-point problem to convergence. Therefore, the choice of q affects computation but not statistical properties. We also establish consistency, asymptotic normality of our estimator, and local convergence of the EM-NPL(q) algorithm. In Monte Carlo simulations, EM-NPL(q) reduces runtime by at least 20% and can be 3--5 times faster. In an application to cola demand, we show that ignoring unobserved heterogeneity understates long-run own-price elasticities by up to 60%, short-run elasticities by up to 85%, and compensating variation from a soda tax by up to 90%.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops the EM-NPL(q) framework for estimating dynamic discrete choice models with unobserved heterogeneity by combining the EM algorithm with a truncated inner fixed-point solver. It establishes a truncation-invariance result for linear-in-parameters models, showing that EM-NPL(q) is numerically identical to the fully converged version for any q ≥ 1. The paper also proves consistency, asymptotic normality, and local convergence of the estimator, demonstrates computational gains in Monte Carlo simulations, and applies the method to cola demand data to show the impact of ignoring unobserved heterogeneity on elasticities and welfare measures.

Significance. If the truncation-invariance result holds as an algebraic identity, the contribution is significant for applied econometrics: it decouples computational cost from statistical properties in a workhorse class of models, enabling faster estimation of DDC models with UH without approximation error. The explicit consistency and asymptotic normality results, plus Monte Carlo speedups of 20% to 5x and the empirical demonstration of large biases (up to 90% in compensating variation), add practical value. The paper earns credit for grounding the main claim in an exact identity rather than an approximation and for supplying supporting asymptotic theory.

major comments (1)

- [truncation-invariance result] The truncation-invariance result (abstract and the section establishing the identity): this is load-bearing for the central claim that statistical properties are unaffected by q. The manuscript should include the explicit algebraic steps showing why the EM update combined with NPL(q) iterations yields exactly the same fixed point as full inner-loop convergence when the model is linear in parameters; without this derivation visible, it is difficult to confirm the identity holds beyond the stated scope.

minor comments (3)

- Abstract: the reported runtime reductions ('at least 20%' and '3--5 times faster') should specify whether these are minima, averages, or medians across the Monte Carlo designs, and over what range of q values.

- [Monte Carlo simulations] Monte Carlo section: report the number of replications, the exact DGP parameter values, and the grid of q values tested so that the speed and statistical equivalence claims can be directly replicated.

- [cola demand application] Empirical application: a side-by-side table of short-run and long-run elasticities (and compensating variation) with and without unobserved heterogeneity would make the quantitative claims (understatement by up to 60%, 85%, 90%) easier to verify at a glance.

Simulated Author's Rebuttal

We thank the referee for the thoughtful and positive report, which recognizes the significance of the truncation-invariance result for applied work. We address the single major comment below and will incorporate the requested clarification in the revision.

read point-by-point responses

-

Referee: [truncation-invariance result] The truncation-invariance result (abstract and the section establishing the identity): this is load-bearing for the central claim that statistical properties are unaffected by q. The manuscript should include the explicit algebraic steps showing why the EM update combined with NPL(q) iterations yields exactly the same fixed point as full inner-loop convergence when the model is linear in parameters; without this derivation visible, it is difficult to confirm the identity holds beyond the stated scope.

Authors: We agree that an expanded, line-by-line algebraic derivation will improve transparency. In the revised manuscript we will augment the section on the truncation-invariance result with the explicit steps: (i) write the EM update for the type-specific value functions as a linear function of the parameter vector; (ii) show that each NPL iteration preserves this linearity; (iii) demonstrate that the fixed-point mapping after any q ≥ 1 iterations is identical to the fully converged mapping because the linear structure makes the contraction invariant to truncation; and (iv) confirm that the subsequent M-step therefore produces the identical parameter update. This derivation will be placed immediately after the statement of the result and will be self-contained so that readers can verify the identity without reference to external lemmas. revision: yes

Circularity Check

No significant circularity detected

full rationale

The paper's central truncation-invariance result is presented as an algebraic identity established specifically for linear-in-parameters models, showing that EM-NPL(q) equals the converged EM-NPL estimator for any q ≥ 1. This identity is used to argue that q affects only computation, after which standard consistency, asymptotic normality, and local convergence results are stated to follow. No step reduces a claimed prediction or uniqueness result to a fitted parameter or self-citation by construction; the derivation chain relies on the EM and NPL frameworks as external building blocks without redefining outputs in terms of inputs. The Monte Carlo and application sections treat the estimator as a computational device whose statistical properties are inherited from the invariance, with no evidence of self-definitional loops or renamed empirical patterns.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Standard regularity conditions for consistency and asymptotic normality of the estimator

- domain assumption The model belongs to the linear-in-parameters class

Reference graph

Works this paper leans on

-

[1]

and Eckardt, D

Adusumilli, K. and Eckardt, D. (2025). Temporal-difference estimation of dynamic discrete choice models.Review of Economic Studies. Forthcoming. Aguirregabiria, V. and Magesan, A. (2023). Solving discrete choice dynamic programming models using euler equations.Working Paper. Aguirregabiria, V. and Marcoux, M. (2021). Imposing equilibrium restrictions in t...

2025

-

[2]

w∗ TX t=1 JX j=1 ∇θQ(θ0,Γ q, P0)(ajt|xt)∇ θQ(θ0,Γ q, P0)(ajt|xt)′ # , Ωq θx :=E

Bugni, F. A. and Bunting, J. (2021). On the iterated estimation of dynamic discrete choice games.The Review of Economic Studies, 88(3):1031–1073. Bunting, J. and Ura, T. (2025). Faster estimation of dynamic discrete choice models using index invertibility.Journal of Econometrics, 250:106004. Chu, K.-w. E. (1986). Generalization of the bauer-fike theorem.N...

2021

-

[3]

Part (ii).RecallS q = Ωq α ˜θ (IM dθ,0) + Ω q αY Yα + Ωq αP Pα

The proof then follows similarly to Lemma 4: applying Lemma 1 to Ω q αα −Ω ∞ αα =E[s q i (sq i )′ −s ∞ i (s∞ i )′] yieldsO(f(q)). Part (ii).RecallS q = Ωq α ˜θ (IM dθ,0) + Ω q αY Yα + Ωq αP Pα. Sq −S ∞ = (Ωq α ˜θ −Ω ∞ α ˜θ)(IM dθ,0) + (Ω q αY −Ω ∞ αY)Yα + (Ωq αP −Ω ∞ αP)Pα. 45 By the similar argument as in Part (i),∥Ω q α ˜θ −Ω ∞ α ˜θ∥F =O(f(q)),∥Ω q αY −...

2007

-

[4]

Step 2:∥A(q)−A(∞)∥ F =O(f(q)).By Lemma 9,∥(Ω q αα +S q)−(Ω ∞ αα +S ∞)∥F = O(f(q))

Step 1:∥B(q)−B(∞)∥ F =O(f(q)).This is Lemma 9(i). Step 2:∥A(q)−A(∞)∥ F =O(f(q)).By Lemma 9,∥(Ω q αα +S q)−(Ω ∞ αα +S ∞)∥F = O(f(q)). Since Ω ∞ αα +S ∞ is invertible by Assumption 5(v), the matrix inverse perturbation bound gives: ∥A(q)−A(∞)∥ F =∥A(q)∥ F ∥(Ωq αα +S q)−(Ω ∞ αα +S ∞)∥F ∥A(∞)∥F =O(f(q)), where∥A(q)∥ F is uniformly bounded for sufficiently lar...

2014

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.