Recognition: unknown

What Drives Contagion? Identifying and Attributing Cross-Border Transmission Mechanisms

Pith reviewed 2026-05-07 11:34 UTC · model grok-4.3

The pith

Cross-border financial contagion can be attributed to specific channels using a two-stage statistical framework.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We address the joint detection-and-attribution problem in cross-border financial contagion through a two-stage framework. The first stage applies wavelet-quantile transfer entropy across time-scales and lower, median, and upper-tail quantiles. The second stage attributes each significant link to one of five channels comprising of trade, financial, geopolitical, behavioural, and monetary policy, via instrumental-variables two-stage least squares with channel-specific external instruments, LASSO-based instrument selection, local projections at one-, five-, and twenty-two-day horizons, heteroskedasticity-based identification for episodes in which over-identification is rejected, and sensitivity

What carries the argument

The two-stage framework that first detects contagion links with wavelet-quantile transfer entropy and then attributes them to channels using IV-2SLS, heteroskedasticity-based identification, and sensitivity analysis.

Load-bearing premise

The external instruments for each channel are valid and the identification strategies correctly isolate each transmission mechanism without residual confounding.

What would settle it

Reapplying the framework to the same data but with a different set of external instruments that produces materially different channel attributions for the same crisis episodes.

Figures

read the original abstract

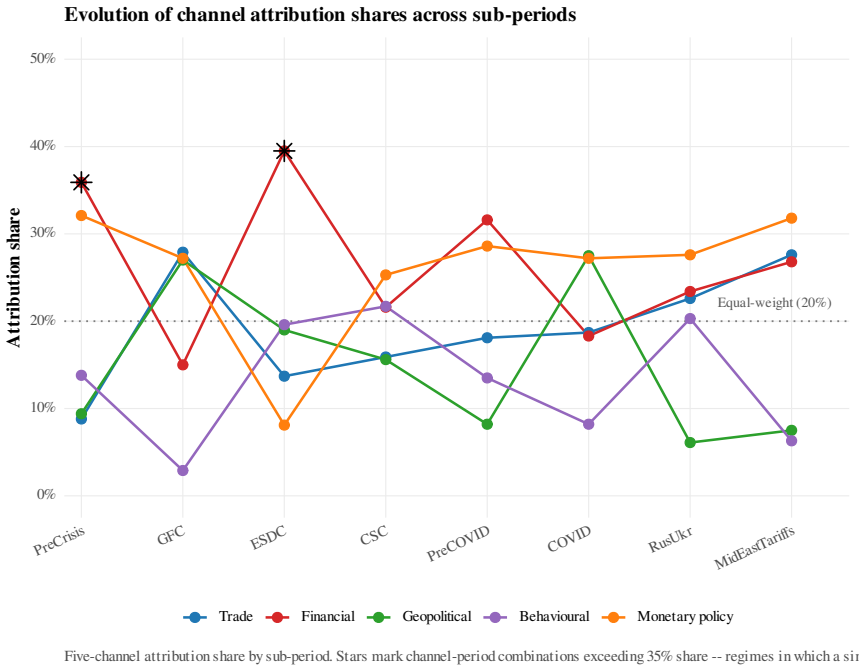

We address the joint detection-and-attribution problem in cross-border financial contagion through a two-stage framework. The first stage applies wavelet-quantile transfer entropy across time-scales and lower, median, and upper-tail quantiles. The second stage attributes each significant link to one of five channels comprising of i) Trade, ii) Financial, iii) Geopolitical, iv) Behavioural, and v) Monetary Policy, via instrumental-variables two-stage least squares with channel-specific external instruments, LASSO-based instrument selection (Belloni, Chernozhukov and Hansen, 2014), local projections at one-, five-, and twenty-two-day horizons (Jorda, 2005), heteroskedasticity-based identification (Rigobon, 2003) for episodes in which over-identification is rejected, and Cinelli-Hazlett (2020) sensitivity bounds. The framework is applied to 18 G20 equity markets across eight crisis sub-periods spanning January 2006 to March 2026. Network density varies meaningfully across sub-periods (range 14% to 32%). Dominant-channel identification is robust across methods in the Pre-Crisis baseline and the European Sovereign Debt Crisis, both dominated by financial frictions; for the remaining six episodes identification is method-sensitive, and we report the share posterior alongside an explicit identification-status classification. Trade is empirically prominent across all post-2007 episodes, ranging from 9% during Pre-Crisis to 28% during the Global Financial Crisis. The behavioural channel is bounded above by 22% across all eight episodes under the de-confounded composite. The framework provides a methodologically disciplined account of cross-border contagion mechanisms and offers identification-status disclosure not systematically present in the existing literature.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a two-stage framework for analyzing cross-border financial contagion. Stage 1 detects significant links among 18 G20 equity markets using wavelet-quantile transfer entropy across time scales and lower/median/upper-tail quantiles. Stage 2 attributes each detected link to one of five channels (Trade, Financial, Geopolitical, Behavioural, Monetary Policy) via IV-2SLS with LASSO-selected external instruments, local projections at 1/5/22-day horizons, Rigobon heteroskedasticity identification when over-identification is rejected, and Cinelli-Hazlett sensitivity bounds. Applied to eight crisis sub-periods (Jan 2006–Mar 2026), the paper reports network densities of 14–32%, Trade channel shares of 9–28%, Behavioural shares bounded above by 22%, and an explicit identification-status classification, with robustness in only two episodes and method-sensitivity in six.

Significance. If the instrument validity and exclusion restrictions hold, the work offers a useful contribution by combining detection with channel attribution while explicitly disclosing identification strength—an improvement over much of the existing contagion literature that often omits such status reporting. The multi-method identification strategy, sensitivity bounds, and multi-episode application are constructive features that allow comparative statements (e.g., financial dominance in the baseline and sovereign-debt episodes). The framework could inform policy discussions on transmission mechanisms if the attribution step is further secured.

major comments (3)

- [§3 (Identification Strategy)] §3 (Identification Strategy): The attribution of links to channels rests on the exclusion restriction for the channel-specific instruments. For Behavioural and Geopolitical channels this restriction is difficult to maintain in equity-market data, where these factors can affect returns through pathways that overlap with Trade, Financial, or omitted variables. LASSO selection and Cinelli-Hazlett bounds mitigate but do not eliminate the risk of residual cross-channel confounding that would reallocate the reported shares (Trade 9–28 %, Behavioural ≤22 %). This is load-bearing for the central claim of a 'methodologically disciplined account'.

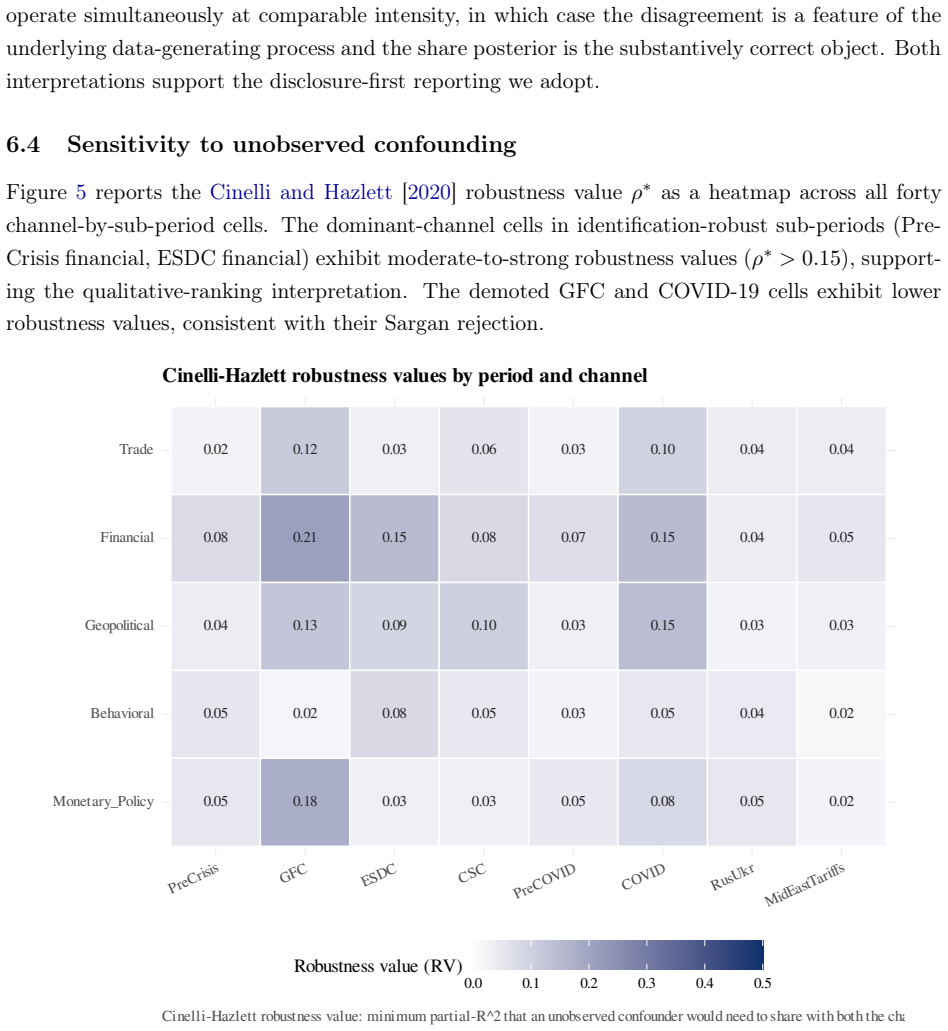

- [§4 (Results)] §4 (Results): Identification is reported as method-sensitive in six of the eight episodes, yet the paper presents channel shares and a classification without detailing how the 'share posterior' is constructed when IV-2SLS, Rigobon, and sensitivity bounds disagree. Without an explicit reconciliation rule or uncertainty quantification, the attribution results for these episodes rest on an unverified aggregation step.

- [Abstract and §5 (Conclusion)] Abstract and §5 (Conclusion): The claim that the framework 'provides a methodologically disciplined account' and 'offers identification-status disclosure not systematically present' is undercut by the method-sensitivity finding; the disclosure is valuable, but the paper must show that the two-stage procedure yields attributions that are robust to plausible instrument violations rather than merely documenting sensitivity.

minor comments (2)

- [§2 (Detection Stage)] The wavelet-quantile transfer entropy implementation would benefit from an explicit statement of the chosen quantile levels, decomposition levels, and the precise definition of 'significant link' (e.g., threshold or p-value adjustment for multiple testing across quantiles and horizons).

- [Tables in §4] Tables reporting channel shares should include the full instrument diagnostics (first-stage F, over-identification tests) and the exact Cinelli-Hazlett bound values for each episode-channel pair to allow readers to assess the sensitivity results directly.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments. We respond point by point to the major comments below, indicating planned revisions where appropriate.

read point-by-point responses

-

Referee: §3 (Identification Strategy): The attribution of links to channels rests on the exclusion restriction for the channel-specific instruments. For Behavioural and Geopolitical channels this restriction is difficult to maintain in equity-market data, where these factors can affect returns through pathways that overlap with Trade, Financial, or omitted variables. LASSO selection and Cinelli-Hazlett bounds mitigate but do not eliminate the risk of residual cross-channel confounding that would reallocate the reported shares (Trade 9–28 %, Behavioural ≤22 %). This is load-bearing for the central claim of a 'methodologically disciplined account'.

Authors: We agree that the exclusion restriction is particularly difficult to maintain for the Behavioural and Geopolitical channels given potential overlapping pathways in equity returns. While LASSO selection, Rigobon identification, and Cinelli-Hazlett bounds reduce the scope for confounding, they cannot eliminate it entirely. We will revise §3 to expand the discussion of these limitations, add further sensitivity checks on channel reallocation under plausible violations, and clarify the resulting bounds on reported shares. This addresses the concern directly while preserving the framework's transparency. revision: partial

-

Referee: §4 (Results): Identification is reported as method-sensitive in six of the eight episodes, yet the paper presents channel shares and a classification without detailing how the 'share posterior' is constructed when IV-2SLS, Rigobon, and sensitivity bounds disagree. Without an explicit reconciliation rule or uncertainty quantification, the attribution results for these episodes rest on an unverified aggregation step.

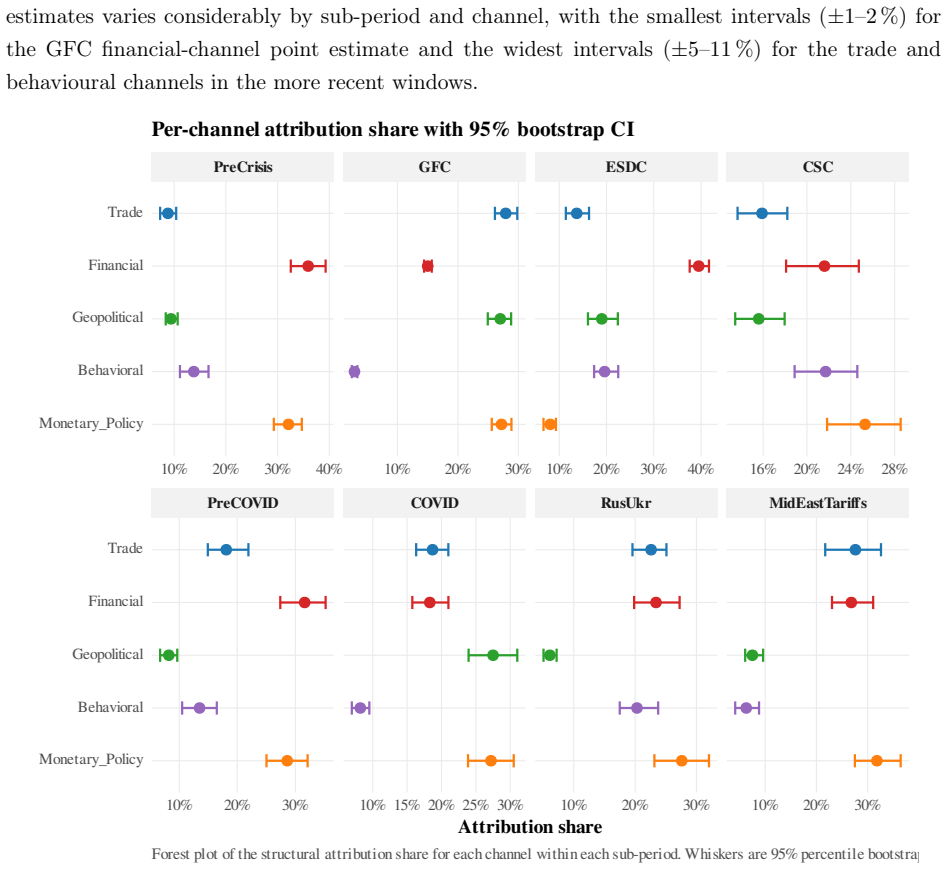

Authors: We thank the referee for highlighting this gap. The share posterior is formed by averaging attributions from methods that satisfy their respective validity tests, with priority given to stronger identification outcomes, but the exact rule was not stated explicitly. In the revision we will insert a dedicated paragraph in §4 describing the reconciliation procedure, including tie-breaking criteria and bootstrap-derived uncertainty intervals around the shares for the six method-sensitive episodes. revision: yes

-

Referee: Abstract and §5 (Conclusion): The claim that the framework 'provides a methodologically disciplined account' and 'offers identification-status disclosure not systematically present' is undercut by the method-sensitivity finding; the disclosure is valuable, but the paper must show that the two-stage procedure yields attributions that are robust to plausible instrument violations rather than merely documenting sensitivity.

Authors: We maintain that explicitly classifying episodes as robust or method-sensitive and reporting the share posterior already constitutes a disciplined account, because it avoids overstating precision where identification is weak—an improvement over much of the literature. Nevertheless, we accept that additional evidence of robustness to instrument violations would strengthen the claim. We will revise the Abstract and §5 to moderate the language, add further robustness exercises (alternative instrument sets and relaxed exclusion assumptions), and emphasize that the framework's contribution is its transparent disclosure of identification status rather than universal robustness. revision: partial

Circularity Check

No circularity: empirical two-stage framework relies on external instruments and standard methods

full rationale

The paper presents a two-stage empirical procedure: wavelet-quantile transfer entropy detects significant cross-border links, after which each link is attributed to one of five channels via IV-2SLS, LASSO-selected external instruments (Belloni et al. 2014), local projections (Jorda 2005), Rigobon heteroskedasticity identification, and Cinelli-Hazlett sensitivity bounds. No equation or result is defined in terms of another result within the paper; the attributed shares are not fitted parameters renamed as predictions, nor does any uniqueness theorem or ansatz reduce to self-citation. All identification tools are drawn from independent prior literature and applied to external G20 equity data across eight sub-periods. The reported identification-status classification is a transparent disclosure of method sensitivity rather than a self-referential equivalence. The derivation chain is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (2)

- Quantile levels

- Local projection horizons

axioms (2)

- domain assumption Validity of channel-specific external instruments

- domain assumption Correct specification of LASSO instrument selection and Cinelli-Hazlett sensitivity bounds

Reference graph

Works this paper leans on

-

[1]

doi: 10.1287/mnsc.2021.3984. Isaiah Andrews, James H. Stock, and Liyang Sun. Weak instruments in instrumental variables regression: Theory and practice.Journal of Economic Literature, 57(3):727–768, 2019. doi: 10.1257/jel.20181361. Susan Athey and Guido W. Imbens. The state of applied econometrics: Causality and policy evaluation.Journal of Economic Persp...

-

[2]

doi: 10.1017/CBO9780511803161. 25 Donald B. Percival and Andrew T. Walden.Wavelet Methods for Time Series Analysis. Cambridge University Press, 2000. ISBN 978-0521685085. Marcello Pericoli and Massimo Sbracia. A primer on financial contagion.Journal of Economic Surveys, 17(4):571–608, 2003. doi: 10.1111/1467-6419.00205. Mikkel Plagborg-Møller and Christia...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.